Contents

I last reviewed Goldman Sachs (GS) in this October 23, 2023 post at which time the most recent financial results were for Q3 and YTD2023. Based on my analysis, I concluded that the firm's stumble had created a buying opportunity.

Fast forward to April 15, 2024 and we now have Q1 2024 results. I, therefore, take this opportunity to briefly revisit this existing holding.

Business Overview

A good description of the business is provided in Part 1 Item 1 within the 2023 Form 10-K which is accessible here.

Financial Review

Q1 2024 Results

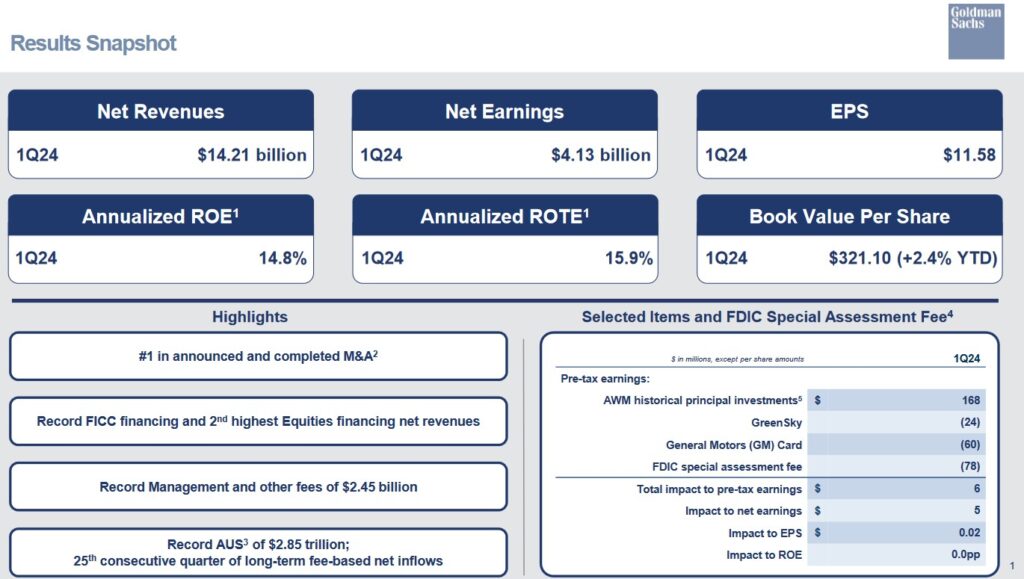

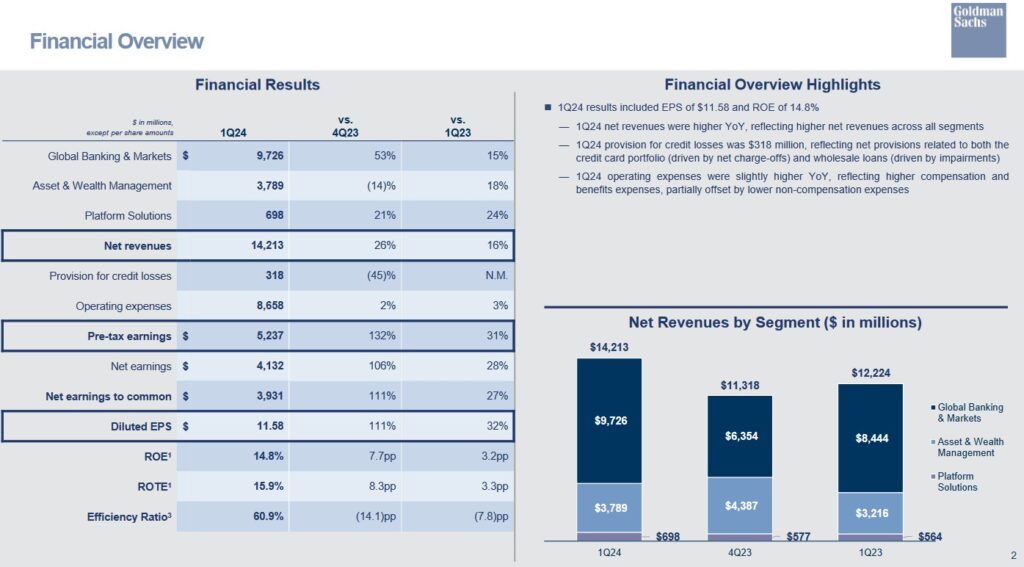

The following images provide a high-level overview of GS's results. However, more detail is provided in the April 15 Earnings Release and Earnings Presentation from which the following images have been extracted.

GS posted strong trading results and investment banking revenue is exhibiting a recovery from recently depressed levels.

During Q1, commissions and market-making revenue of ~$7.1B was ~8% higher than the previous year and 60% higher sequentially. Furthermore, annualized return on equity (ROE) in Q1 was 14.8% and return on tangible common equity (ROTE) was 15.9%.

The US economy remains strong and while expectations are for interest rates to trend lower over the next couple of years, the timing and magnitude of interest-rate cuts is uncertain. With a generally positive economic backdrop, GS's investment banking activity should continue to be healthy over the remainder of the current fiscal year.

Trading revenue at just over $7B represented ~50% of total revenue in Q1. This highly transactional component of GS's business makes it very difficult to estimate future quarterly results. I have absolutely no idea whether a normal level is closer to the pre-covid level of ~$3.5B or the $5B - $6B post-covid level. In addition, GS's investment banking revenue is also transactional and difficult to forecast.

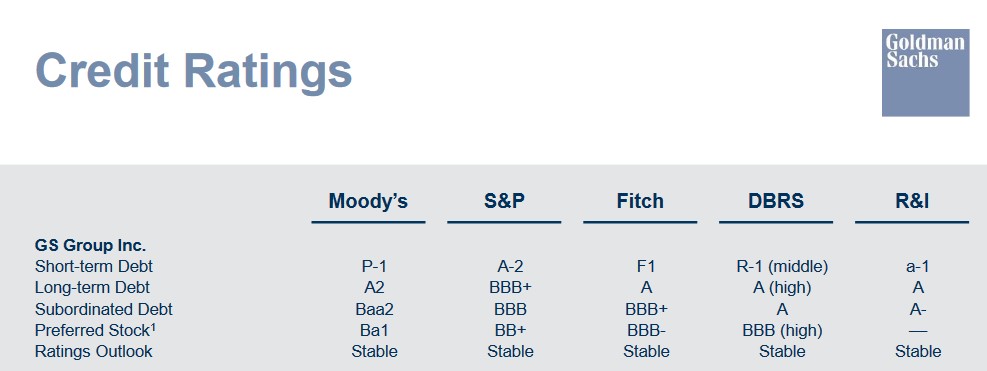

Credit Ratings

GS's current credit ratings are accessible here and there have been no changes subsequent to my last review. The ratings assigned to The Goldman Sachs Group, Inc. are of interest to me since this is the company in which I hold shares.

Each rating agency views GS's risk differently. Looking at GS's subordinated debt, for example, we see that Moody's and S&P Global assign a rating that is the middle tier of the lower medium grade investment grade category. Fitch assigns a rating that is one tier higher and Rating and Investment Information, Inc. (R&I) assigns a rating that is 1 tier higher than that of Fitch. DBRS assigns a rating that is 1 tier higher than that assigned by R&I.

Fitch assigns the lowest investment grade rating to GS's preferred stock and DBRS assigns a rating that is comparable to Moody's Baa1 rating and S&P Global's BBB+ rating. Interestingly, Moody's and S&P Global assign a rating that is one tier below investment grade.

For comparison, these are the ratings at the time of my last GS review.

Based on my analysis, I think the preferred stock non-investment grade ratings assigned by Moody's and S&P Global are the most accurate. Given this, my risk as a common shareholder is closer to Ba2 and BB. I typically avoid companies with such poor credit ratings but have made an exception with GS.

Dividend and Dividend Yield

GS does not maintain a dividend history on its website. This history is accessible here.

In Q1, GS distributed $0.929B of common stock dividends.

On April 11, 2024, GS's Board declared a dividend of $2.75 per common share to be paid on June 27, 2024 to common shareholders of record on May 30, 2024. In mid-July, I anticipate GS will declare a $0.25 increase in its quarterly dividend. Should this increase materialize, the next 4 quarterly dividend payments will total $11.75 ($2.75 + (3 x $3.00)). With shares trading having closed at $400.88 on April 15, I estimate the forward dividend yield to be ~2.93%.

When I wrote my January 18, 2023 post, GS's Board had just declared the 3rd consecutive $2.50 quarterly dividend. With shares trading at ~$350, the dividend yield was ~2.86%.

When I wrote my October 23, 2023 post, GS had declared its second $2.75/share quarterly dividend on October 12, 2023 for distribution on December 28. I expected dividends at this level to be distributed at the end of March and end of June. In mid-July, 2024, I expected GS to declare at least a $0.25/share increase in its quarterly dividend. If this materialized, I calculated a forward dividend yield of ~3.75% calculated by using the current ~$300 share price and $11.25 of dividends (($2.75 *3) + ($3.00 * 1)).

As noted in several previous posts, focusing on dividend income and dividend yield metrics can lead to flawed investment decisions. Investors would be better served by focusing on an investment's TOTAL potential return.

In the FY2009 - FY2023 time frame, GS's weighted average number of diluted shares outstanding (in millions) was 550.9, 585.3, 556.9, 516.1, 499.6, 473.2, 458.6, 435.1, 409.1, 390.2, 375.5, 360.3, 355.8, 358.1, and 345.8. This has been reduced to 339.5 in the quarter ending on March 31.

GS has a share repurchase program which is intended to help maintain the appropriate level of common equity.

In February 2023, GS announced that its Board had approved a new share-repurchase program authorizing as much as $30B in stock buybacks with no expiration date.

During the quarter, GS repurchased $1.5B of common shares or 3.9 million shares at an average cost of $384.55.

Valuation

GS's valuation at the time of prior reviews is found in October 23, 2023 post.

When I wrote my October 23, 2023 post, GS shares traded at ~$300. Using this share price and broker estimates, the following were the forward-adjusted diluted PE levels.

- FY2023: 19 brokers, mean estimate $23.15, low/high range $20.34 - $25.52. Valuation using the mean estimate was ~12.96.

- FY2024: 19 brokers, mean estimate $34.76, low/high range $29.40 - $40.00. Valuation using the mean estimate was ~8.6.

- FY2025: 12 brokers, mean estimate $39.44, low/high range $35.51 - $42.00. Valuation using the mean estimate was ~7.6.

GS's FY2023 valuation is distorted because of the write-downs. If we add the $6.36 impact to EPS reflected above to the FY2023 mean EPS estimate, we get ~$29.51. Using the current ~$300 share price, the forward adjusted diluted PE is closer to 10.17. I, however, stated that we can not merely overlook these writedowns; GS spent a ton of money to expand its business with disastrous results.

Shares now trade at $400.88 and GS's valuation based on forward adjusted diluted EPS broker estimates is:

- FY2024: 22 brokers, mean estimate $35.69, low/high range $30.06 - $39.85. Valuation using the mean estimate is ~11.2.

- FY2025: 23 brokers, mean estimate $39.62, low/high range $29.94 - $43.00. Valuation using the mean estimate is ~10.1.

- FY2026: 13 brokers, mean estimate $43.40, low/high range $34.69 - $47.56. Valuation using the mean estimate is ~9.3.

Given that GS just released its Q1 earnings on April 15, I suspect the current data may change over the coming days but I do not expect a significant change. Having said this, the disparity in the forward adjusted diluted earnings estimates from the brokers is generally significant.

Final Thoughts

I initiated a GS position on November 21, 2018, with the purchase of 150 shares @ ~$200/share in one of the 'Side' accounts within the FFJ Portfolio. My GS exposure is currently 192 shares which was insufficient to make it a top 30 holding when I completed my 2023 Year End FFJ Portfolio Review; it is still not a top 30 holding.

Several companies to which I have exposure generate annual recurring revenue and estimating their results over the upcoming year or two is less of a crapshoot than trying to forecast GS's future earnings. I am, apparently, not the only investor who has difficulty in forecasting GS's results as we see quite the disparity in brokers' earnings estimates. Even GS does not provide any earnings estimates!

As noted earlier, I consider my GS credit risk to be higher than what I typically target. As an equity shareholder, I think GS is non-investment grade.

In addition, GS's results are highly unpredictable and can be volatile, I would like to have a higher margin of safety when it comes to its valuation. Currently, I do not think the margin of safety is sufficient for me to add to my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to [email protected].

Disclosure: I am long GS.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.