I last reviewed Goldman Sachs (GS) in this January 18, 2023 post at which time GS had just released Q4 and FY2022 results and I concluded shares to be too richly valued. Much has changed since that last review. At GS’s first Investor Day in January 2020, David Solomon, Chairman and CEO laid out a clear and comprehensive strategy to strengthen and grow the firm and to run the firm more efficiently. Not everything has proceeded according to plan and I view Goldman Sachs’s stumble as a buying opportunity.

The first priority the leadership laid out in January 2020 was to invest in the core business.

Secondly, senior management identified 4 opportunities to grow the business:

- asset management

- wealth management

- transaction banking

- consumer platform

Third, the firm would be run more efficiently and for the first time, public, firmwide financial targets were set to help investors hold the leadership team accountable.

On February 28, 2023, GS held its second Investor Day in the firm’s history. Should you want more information about the leadership team’s plan for GS, I suggest you listen to the presentations from the 2023 Investor Day. You might not have 3 hours to listen to all the presentations. At the very least, however, please listen to the Welcome and Opening Remarks and the Q&A segments.

Furthermore, you are encouraged to read the Letter to Shareholders that accompanies the 2002 Annual Report.

At the February 28, 2023 Investor Day, senior management stated that it might explore strategic alternatives for some, or all, of the underperforming segments of the firm.

Subsequently, GS has taken measures to narrow its consumer ambitions and to transition the Asset and Wealth Management business to a less capital-intensive model. When GS reported its Q2 and Q3 results, it disclosed selected items that the firm sold, is selling, or for which the firm has announced the exploration of a sale (see Q2 earnings release and Q3 earnings release).

While GS’s initiative to diversify its business toward consumer finance and mass affluent wealth management made strategic sense, not everything went according to plan. On a positive note, GS has recognized that it can not successfully compete in all the areas of business in which it diversified and it has cut its losses.

With the sale of GreenSky and Personal Financial Management, GS is now returning to being primarily an investment bank and investment manager. Despite the divestiture of GreenSky and Personal Financial Management, it has retained its credit card business with Apple and General Motors, online deposit gathering, and transaction banking.

While GS has stumbled I think this creates a buying opportunity.

With the release of Q3 and YTD2023 results on October 17, I revisit this existing holding.

Business Overview

A good description of the business is provided on page 7 of 217 in the Q2 2023 Form 10-Q.

Financial Review

Q3 and YTD2023 Results

The following images provide a high-level overview of GS’s results. However, more detail is provided in the October 17 Earnings Release and Earnings Presentation.

Source: GS – Q3 Earnings Presentation – October 17, 2023

GS’s YTD compensation ratio, net of provisions, is 34.5%, inclusive of ~$0.275B of YTD severance costs. At the 2023 Investor Day, GS’s leadership articulated a goal of $0.6B in run rate payroll efficiencies to be achieved in 2023 and 2024, and GS is currently tracking to surpass that goal.

Quarterly non-compensation expenses were $0.9B with the YoY increase driven by the write-down of $0.506B of intangibles related to GreenSky as well as consolidated investment entity impairments of $0.358B.

YTD Onetime expenses are elevated but GS continues to focus on reducing non-compensation expenses and progress is being made on GS’s $0.4B run rate efficiency goal.

The YTD effective tax rate was 23.3%. This is high due to the write-off of deferred tax assets related to GreenSky and the geographic mix of GS’s earnings; GS expects FY2023’s tax rate to be under 23%.

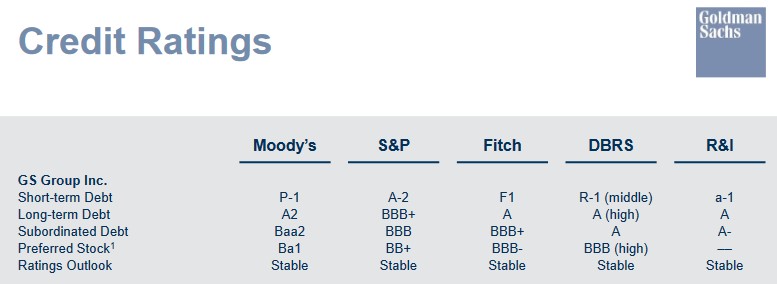

Credit Ratings

GS’s current credit ratings are accessible here. While several GS entities are rated, the ratings assigned to The Goldman Sachs Group, Inc. are of interest to me since this is the company in which I hold shares.

Each rating agency views GS’s risk differently. Looking at GS’s subordinated debt, for example, we see that Moody’s and S&P Global assign a rating that is the middle tier of the lower medium grade investment grade category. Fitch assigns a rating that is one tier higher and Rating and Investment Information, Inc. (R&I) assigns a rating that is 1 tier higher than that of Fitch. DBRS assigns a rating that is 1 tier higher than that assigned by R&I.

Fitch assigns the lowest investment grade rating to GS’s preferred stock and DBRS assigns a rating that is comparable to Moody’s Baa1 rating and S&P Global’s BBB+ rating. Interestingly, Moody’s and S&P Global assign a rating that is one tier below investment grade.

For comparison, these are the ratings at the time of my last GS review.

GS – August 2022 Overview Presentation

Based on my analysis, I think the preferred stock non-investment grade ratings assigned by Moody’s and S&P Global are the most accurate. Given this, my risk as a common shareholder is closer to Ba2 and BB. I typically avoid companies with such poor credit ratings but have made an exception with GS.

Dividends and Share Repurchases

Dividend and Dividend Yield

GS does not maintain a dividend history on its website. This history is accessible here.

In the first 3 quarters of FY2023, GS has distributed $2.669B of common stock dividends. GS distributed $3.20B of common stock dividends in FY2022 of which $0.88 million was distributed in Q4 2022.

In June 2023, GS declared a $0.25/share increase in its quarterly dividend from $2.50 to $2.75.

On October 12, GS declared its second $2.75/share quarterly dividend which is to be distributed on December 28. I expect dividends at this level to be distributed at the end of March and end of June. In mid-July, 2024, I expect GS to declare at least a $0.25/share increase in its quarterly dividend. If this materializes, the forward dividend yield is ~3.75% calculated by using the current ~$300 share price and $11.25 of dividends (($2.75 *3) + ($3.00 * 1)).

When I wrote my January 18 post, GS’s Board had just declared the 3rd consecutive $2.50 quarterly dividend. With shares trading at ~$350, the dividend yield was ~2.86%.

As noted in several previous posts, focusing on dividend income and dividend yield metrics can lead to flawed investment decisions. Investors would be better served by focusing on an investment’s TOTAL potential return.

Share Repurchases

GS has a share repurchase program which is intended to help maintain the appropriate level of common equity.

In February 2023, GS announced that its Board had approved a new share-repurchase program authorizing as much as $30B in stock buybacks with no expiration date.

Previously, GS had provided the number of shares it had the ability to repurchase. This time, it has provided investors with a dollar figure of the total amount available for repurchase over an undefined timeline.

In the FY2009 – FY2022 timeframe, GS’s weighted average number of diluted shares outstanding (in millions) was 550.9, 585.3, 556.9, 516.1, 499.6, 473.2, 458.6, 435.1, 409.1, 390.2, 375.5, 360.3, 355.8, and 358.1. This has been reduced to 343.9 in the quarter ending on September 30.

In the first 3 quarters of FY2023, GS repurchased:

- 7.1 million common shares at an average cost of $359.77 for a total cost of $2.55B in Q1;

- 2.2 million common shares at an average cost of $335.03 for a total cost of $0.75B in Q2; and

- 4.2 million common shares at an average cost of $354.79 for a total cost of $1.50B in Q3.

Given the current uncertainty around capital rules, GS expects to moderate Q4 share repurchases relative to Q3.

Valuation

GS’s valuation at the time of prior reviews is found in my January 18 2023 post. For ease of comparison, however, I provide GS’s valuation at the time of my previous 2 posts.

When I wrote my July 8, 2022 post, shares were trading at ~$296.50. Its valuation based on current adjusted diluted earnings estimates were:

- FY2022: 25 brokers, mean estimate $35.19, low/high range $28.70 – $41.25. Valuation using the mean estimate is ~8.4.

- FY2023: 26 brokers, mean estimate $38.70, low/high range $26.10 – $45.30. Valuation using the mean estimate is ~7.7.

- FY2024: 16 brokers, mean estimate $42.72, low/high range $32.56 – $48.50. Valuation using the mean estimate is ~6.9.

When I wrote my January 18 2023 post, there was a significant variance in forward-adjusted diluted earnings broker estimates. I expected these estimates to be lowered following GS’s earnings release, however, based on the currently available estimates and the current ~$350 share price, GS’s valuation was:

- FY2023: 25 brokers, mean estimate $35.28, low/high range $27.01 – $41.95. Valuation using the mean estimate is ~9.92.

- FY2024: 20 brokers, mean estimate $41.21, low/high range $33.29 – $48.00. Valuation using the mean estimate is ~8.49.

Expectations were that at least the first half of FY2023 would be challenging and I concluded shares were too richly valued. I expected revisions to broker estimates to lower the FY2023 and FY2024 mean adjusted diluted EPS estimates to ~$35 and $40.5. Using these adjusted estimates and a forward adjusted diluted PE of 8.5 and 8.2 for FY2023 and FY2024, a more reasonable share price would be ~$300 – ~$330.

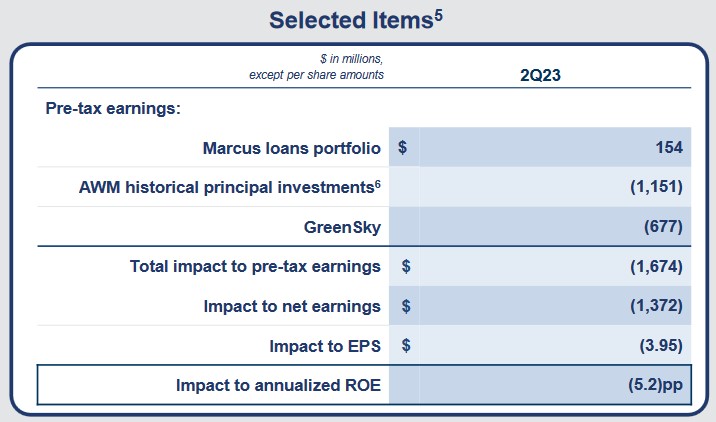

In the first 3 quarters of FY2023, GS has generated $17.39 in diluted EPS versus $26.71 by the end of Q3 2022. Of this $9.32 negative variance, $6.36 is attributed to GS’s decision to sell portions of the firm as it transitions to a less capital-intensive business.

In Q2, GS’s EPS was negatively impacted by $3.95/share.

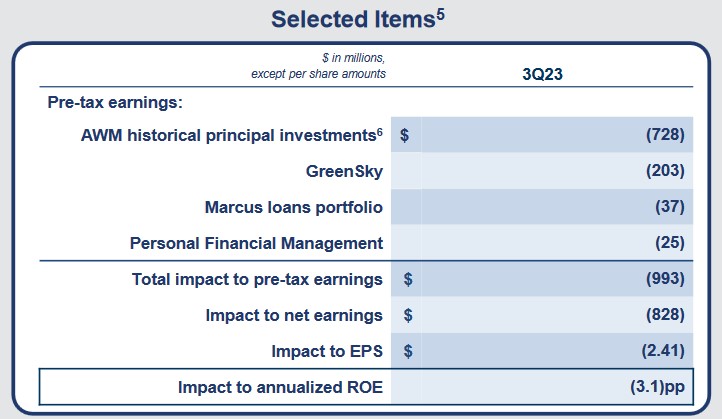

In Q3, GS’s EPS was negatively impacted by $2.41/share.

Source: GS – Q3 2023 Earnings Presentation – October 17, 2023

Using GS’s current ~$300 share price and broker estimates, we get the following forward-adjusted diluted PE levels.

- FY2023: 19 brokers, mean estimate $23.15, low/high range $20.34 – $25.52. Valuation using the mean estimate is ~12.96.

- FY2024: 19 brokers, mean estimate $34.76, low/high range $29.40 – $40.00. Valuation using the mean estimate is ~8.6.

- FY2025: 12 brokers, mean estimate $39.44, low/high range $35.51 – $42.00. Valuation using the mean estimate is ~7.6.

GS’s FY2023 valuation is distorted because of the write-downs. If we add the $6.36 impact to EPS reflected above to the FY2023 mean EPS estimate, we get ~$29.51. Using the current ~$300 share price, the forward adjusted diluted PE is closer to 10.17.

We can not, however, merely overlook these writedowns. GS spent a ton of money to grow the business which resulted in the destruction of shareholder value.

Final Thoughts

I initiated a GS position on November 21, 2018, with the purchase of 150 shares @ ~$200/share. I subsequently acquired a few additional shares bringing my total exposure to 190 shares. For tax planning reasons, the GS shares were transferred from one investment account to another. Unfortunately, I had to initiate this transfer when GS’s share price had appreciated considerably which explains why I reflect a ~$388 average cost in my monthly FFJ Portfolio reports.

Obviously, I am not pleased that GS’s leadership spent a ton of money that destroyed shareholder value. Had some of this money been redirected toward share buybacks, GS’s share price would likely be very different from the current ~$300 level.

Now that GS’s leadership has learned its lesson and has refocused the business, I envision an improvement in results going forward. I also take solace that GS’s leadership has far more ‘skin in the game’ than my measly 190 shares and am certain GS’s leadership and employees want GS to generate a far superior total shareholder return than what has been produced of late.

GS’s stumble has led to it falling out of favour with many investors thus creating a buying opportunity. I should be acquiring additional shares but the liquidity in the account that holds GS shares is earmarked for other purposes. I will not, therefore, be adding to my exposure other than through the automatic reinvestment of the quarterly dividend income. If you have sufficient liquidity, you may wish to seriously consider investing in GS before it resumes ‘firing on all cylinders’. Be forewarned, however, that GS’s business is cyclical so earnings can fluctuate widely from quarter to quarter. Even broker estimates for FY2024 (see above) vary considerably.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long GS.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.