When I last reviewed Danaher (DHR) in this July 31 post, it had recently released its Q2 and YTD2023 results and the spin-off of Veralto Corporation (VLTO) was on schedule to close on September 30. With the spin-off completed and the October 24 release of Q3 and YTD results and guidance for the remainder of FY2023, I revisit this existing holding.

Overview

Please read Part 1 of DHR’s FY2022 Form 10-K if you wish to familiarize yourself with DHR. I also encourage you to read Notes 2 and 3 in the Q3 2023 Form 10-Q because DHR has:

- spun off its former Environmental & Applied Solutions business by distributing to Danaher stockholders on a pro-rata basis all of the issued and outstanding common stock of Veralto Corporation;

- has entered into a definitive agreement to acquire all of the outstanding shares of Abcam plc for a cash purchase price of ~$5.7B, including assumed indebtedness and net of acquired cash. The Abcam acquisition is anticipated to close mid-2024 and DHR expects to finance the acquisition using cash on hand and/or the proceeds from the issuance of commercial paper.

On the Q3 2023 earnings call, management stated:

Abcam is a leading producer of protein consumables that are critical for advancing drug discovery, life science research and diagnostics. Abcam has a long track record of innovation, outstanding product quality and breadth of antibody portfolio, which positions them as a key partner for the scientific community.

The addition of Abcam will give Danaher entry into this highly attractive market, furthering our strategy to help map complex diseases and accelerate the drug discovery process.

We expect Abcam will be accretive on multiple levels, including core growth, earnings and talent, and look forward to welcoming this incredibly innovative team to Danaher once the transaction closes.

Rebranding

DHR has recently undergone a rebranding; the old (left) and new (right) logos are reflected above. The rebranding has given DHR a more modern and more noticeable identity. There is, however, a hidden meaning to the logo design which is explained here.

Financials

Q3 and YTD2023 Results

Material related to DHR’s Q3 and YTD2023 results is accessible here. Since VLTO was part of DHR through the end of Q3, the financial highlights include VLTO’s results.

Sales were $6.9B in Q3 and core revenue declined 11.5%. This consists of a 3% decline in DHR’s base business and a COVID-19 revenue headwind of ~8.5%.

Geographically, core revenues in developed markets declined by low double digits, primarily driven by lower COVID-19 revenues. High-growth markets were down high single digits, including a mid-teens decline in China where the economic landscape remains challenging.

Gross profit margin in Q3 was 58.2%. with a 20.9% operating margin being down 540 bps, primarily due to the impact of lower volume in the Biotechnology and Diagnostics segment and costs related to the separation of VLTO.

Biotechnology

The Biotechnology segment which provides bioproduction tools for drug makers benefitted from COVID-19 vaccine production in recent years.

Post-pandemic boom years, however, this segment’s results have been resetting. Core revenue declined over 20% primarily because of lower demand from DHR’s earlier-stage research and lab filtration customers.

Base business core revenue declined mid-teens, and market conditions were consistent with DHR’s expectations coming into Q3. Its customers are still working through inventory built up during the pandemic while also continuing to conserve capital as a result of funding pressures. China was down ~45% in Q3, driven by a weak funding environment and lower underlying activity levels. On the Q3 earnings call, however, DHR noted that the business hit its expectations and may be in the process of finding a bottom in demand.

Life Sciences

The life sciences instrument businesses declined mid-single digits. This was driven in part driven by China where an already challenging funding environment further deteriorated as the quarter progressed. Outside of China, DHR continues to see softness at pharma and biopharma customers while demand remains stable in life science research and applied markets.

Diagnostics

Revenue declined 16% and core revenue declined 15.5%, with mid-single-digit growth in the base business more than offset by lower COVID-related respiratory testing volumes at Cepheid.

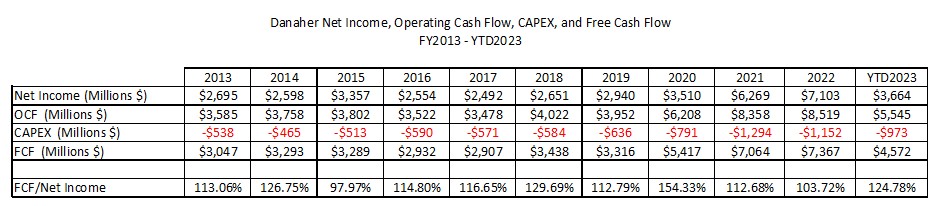

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

Since DHR actively acquires and divests assets, its diluted EPS is deceiving. ‘Amortization of intangible assets’ and ‘amortization of acquisition-related inventory fair value step-up’ are line items that consistently appear in the Consolidated Condensed Statements of Cash Flows. Investors should, therefore, pay particularly close attention to DHR’s OCF and FCF.

Comparing DHR YoY is difficult because of its extensive acquisition/divestiture track record. Nevertheless, we see that DHR generally has an attractive FCF conversion ratio.

Source: DHR – Q3 2023 Earnings Supplement – October 24, 2023

FY2023 Guidance

DHR’s Q4 and FY2024 guidance include only DHR’s continuing operations and exclude VLTO.

The following are some of the highlights of DHR’s FY2023 guidance that were communicated on the Q3 earnings call.

DHR is maintaining its FY2023 outlook of a ~10% base business decline in bioprocessing. This assumes that market conditions in Q4 are consistent with those in Q3.

Although these market dislocations are impacting DHR’s recent performance, global demand for biologic medicines continues to increase. Since 2018, underlying demand for biologics has grown at an average annual rate of ~10% and is continuing to grow.

In addition to more patients using biologic medicines, 2023 is on pace to be a record year for FDA approvals of biologics. These approvals include approvals for meaningful indications such as Alzheimer’s disease and several cancer immunotherapies.

DHR now expects ~$1.6B of respiratory testing revenue for FY2023 versus its previous expectation of $1.2B in its Diagnostics segment.

In Q4, expectations are for core revenue in the base business to be down mid-single digits YoY. Total core revenue is also expected to decline in the high-teens percent range primarily as a result of lower demand for COVID-19 testing, vaccines and therapeutics.

The projected Q4 ~28% adjusted operating profit margin includes additional anticipated productivity initiatives to further adjust DHR’s cost structure.

On a full-year basis, core revenues in the base business will be down slightly and total core revenue is expected to decline low double digits as a result of lower demand for COVID-19 testing, vaccines and therapeutics. The full-year adjusted operating profit margin is expected to be ~29%.

Source: DHR – Q3 2023 Earnings Supplement – October 24, 2023

Credit Ratings

We see from DHR’s debt schedule at the end of Q3 2023 that debt has been raised at very attractive rates. Furthermore, maturity dates are well-balanced and go far out on the calendar.

DHR initially guaranteed the VLTO debt. The guarantee automatically terminated effective as of September 30 when DHR received net cash distributions of ~$2.6B from VLTO as partial

consideration for DHR’s contribution of assets to VLTO in connection with the Separation Date. As of September 29, 2023, VLTO was a wholly-owned, consolidated subsidiary of DHR. DHR’s Consolidated Balance Sheet as of September 29, 2023, therefore, includes the VLTO debt.

The transfer of the liabilities associated with the VLTO debt, as well as all other assets and liabilities transferred to VLTO, will be reflected in DHR’s Q4 2023 financial statements.

In accordance with applicable tax rules, DHR intends to use a portion of ~$2.6B to meet upcoming commercial paper and bond maturities and to use the balance of the proceeds to partially fund certain of the regular, quarterly cash dividends to shareholders.

Source: DHR – Q3 2023 Form 10-Q

The following schedule of long-term debt at the end of Q2 2023 is provided for comparison.

Source: DHR – Q2 2023 Form 10-Q

DHR’s credit ratings are unchanged from my last review.

- Moody’s: Upgraded to A3 from Baa1 on October 10, 2022;

- S&P Global: Upgraded to A- from BBB+ on June 14, 2022.

Both ratings are at the bottom tier of the upper-medium investment-grade tier. This rating defines DHR as having a STRONG capacity to meet its financial commitments. However, DHR is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

These ratings satisfy my conservative investment profile.

Dividend and Dividend Yield

DHR distributes a quarterly dividend.

When I wrote my October 21, 2022 post, DHR’s share price was ~$243 and the quarterly dividend was $0.25; the dividend yield was ~0.41%.

At the time of my July 31 post, shares were trading at $260 and the $0.27 quarterly dividend yielded ~0.41%.

On September 12, DHR declared its 3rd consecutive $0.27/share quarterly dividend which is payable on October 27.

I anticipate DHR will declare one more $0.27/share quarterly dividend in early December for distribution near the end of January. In late February, I expect DHR will declare a ~$0.02/share increase in its quarterly dividend. If this materializes, the next 4 quarterly dividends will total $1.12 (($0.27 x 2) + ($0.29 x 2)). With shares currently trading at ~$197, the forward dividend yield is ~0.57%.

DHR is hyper-focused on capital allocation. The reason for the low dividend yield is that the Board feels superior long-term investor returns can be generated by retaining funds in the company.

Investors who rely on dividend income might immediately pass on DHR because of this low dividend yield. However, investors should not fixate on dividend metrics. The focus should be on total potential long-term investment returns.

On July 16, 2013, DHR’s Board approved a repurchase program authorizing the repurchase of up to 20 million shares from time to time on the open market or in privately negotiated transactions. As of September 29, 2023, ~20 million shares remain available for repurchase under the Repurchase Program.

The diluted average common stock and common equivalent shares outstanding (in millions) in FY2012 – FY2022 are 713, 711, 716, 709, 700, 706, 710, 726, 719, 737, and 737. The average common stock and common equivalent shares outstanding for the 3 months ending September 29, 2023 is ~745.9.

The increase in diluted average common stock and common equivalent shares outstanding in recent years is primarily the result of the conversion of On April 15, 2022, all outstanding shares of the 4.75% MCPS Series A converted and on April 15, 2023, the 5% MCPS Series B converted.

Valuation

Please refer to my July 31, 2023 post in which I compare DHR’s valuation at the time of previous posts.

DHR’s FY2012 – FY2021 diluted PE levels are 17.31, 21.56, 22.44, 25.80, 19.66, 27.63, 26.51, 45.41, 51.90, and 42.34. Trying to compare DHR’s current valuation relative to its historical valuation is difficult because it has undergone a radical transformation over the last few years after having divested slower-growing businesses and acquiring several faster-growing businesses. As a result, comparing historical PE levels against current levels can lead to misleading conclusions. Furthermore, the active acquisition/divestiture of businesses distorts EPS which is why I also look at DHR’s Price/FCF to gauge its valuation.

When I last reviewed DHR, it had reported an adjusted diluted EPS of $4.42 in the first half of FY2023. With shares trading at ~$260, DHR’s forward-adjusted diluted PE levels using current forward-adjusted diluted EPS broker estimates were:

- FY2023 – 22 brokers – mean of $8.86 and low/high of $8.67 – $9.27. Using the mean estimate, the forward adjusted diluted PE is ~29.3.

- FY2024 – 21 brokers – mean of $9.70 and low/high of $8.75 – $10.23. Using the mean estimate, the forward adjusted diluted PE is ~26.8.

- FY2025 – 19 brokers – mean of $10.87 and low/high of $9.95 – $11.45. Using the mean estimate, the forward adjusted diluted PE is ~23.9.

In the first half of FY2023, DHR reported a YTD2023 FCF to net income conversion of 128%. I was unsure if DHR could maintain such a high ratio for the entire fiscal year, and therefore, arbitrarily lowered it to 120%.

Multiplying the FY2023 $8.86 mean adjusted diluted EPS guidance from analysts by 120%, I arrived at $10.63 FCF/share. I then divided the $260 share price by $10.63 to give me a ~24.5 P/FCF.

The Abcam acquisition is likely to close in mid-2024, and therefore, FY2024 and FY2025 earnings estimates reflected below are likely to change.

Shares currently trade at ~$197. The forward-adjusted diluted PE levels using current forward-adjusted diluted EPS broker estimates are:

- FY2023 – 29 brokers – mean of $8.57 and low/high of $8.21 – $9.01. Using the mean estimate, the forward adjusted diluted PE is ~23.

- FY2024 – 14 brokers – mean of $8.05 and low/high of $7.27 – $9.80. Using the mean estimate, the forward adjusted diluted PE is ~23.7.

- FY2025 – 11 brokers – mean of $8.95 and low/high of $8.14 – $10.19. Using the mean estimate, the forward adjusted diluted PE is ~21.5.

In the first 9 months of FY2023, DHR reported a YTD2023 FCF to net income conversion of 124%. I am, however, sticking with my arbitrary 120% in the event the Q4 conversion ratio is similar to the Q3 conversion ratio of 116%.

Multiplying the FY2023 $8.60 mean adjusted diluted EPS guidance from analysts by 120%, I arrive at $10.32 FCF/share. I then divide the $197 share price by $10.32 to give me a ~19.1 P/FCF.

Final Thoughts

The time to invest in great companies is when they have fallen out of favour with the broad investment community. DHR is such a company.

Although earnings are likely to remain weak during Q4 2023 and most of FY2024, investors would be wise to pay particularly close attention to DHR’s ability to generate strong FCF.

DHR is known for its intense focus on continuous improvement, and I expect we will witness a return to high-single-digit revenue growth and low-double-digit earnings growth in the long run. In the short term, however, the environment is likely to remain challenging. This is when investors should look to invest in great companies.

I currently hold 445 shares in a ‘Core’ account in the FFJ Portfolio. In conjunction with the VLTO spin-off, I received 148 VLTO shares at an average cost of ~$77.22. VLTO is a very small position and since I have no intention of increasing my exposure, I intend to exit this position within 24 hours.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long DHR.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.