In my February 2, 2024 Nasdaq (NDAQ) post, I state that the success of the Nasdaq 100 index makes NDAQ sensitive to the volatile technology sector. Inevitably this leads to volatile quarterly results.

To reduce the volatility of its results, NDAQ undertook a strategic review which led to the beefing up of its anti-financial-crimes business (now known as regulatory technologies).

Sensing that NDAQ’s strategic direction would lead to more stable results (higher annual recurring revenue (ARR), I envisioned NDAQ’s earnings multiple would increase once NDAQ achieved its deleveraging objectives.

Given my long-term outlook for NDAQ, I initiated a 500 share position in a ‘Core’ account within the FFJ Portfolio at ~$51/share on June 12, 2023; I disclosed this purchase in my June 13, 2023 post. I subsequently acquired another 100 shares at ~$50.75 on July 19 and disclosed this purchase in this July 20, 2023 post.

At the time of my February 2 review, NDAQ had just released Q4 and FY2023 results.

With the release of Q1 2024 results on April 25, 2024, I revisit this holding.

Business Overview

The best way to learn about NDAQ is to review its website. Part 1 Items 1 (Business) and 1A (Risk Factors) in the FY2023 Form 10-K is also a great source of information.

Financials

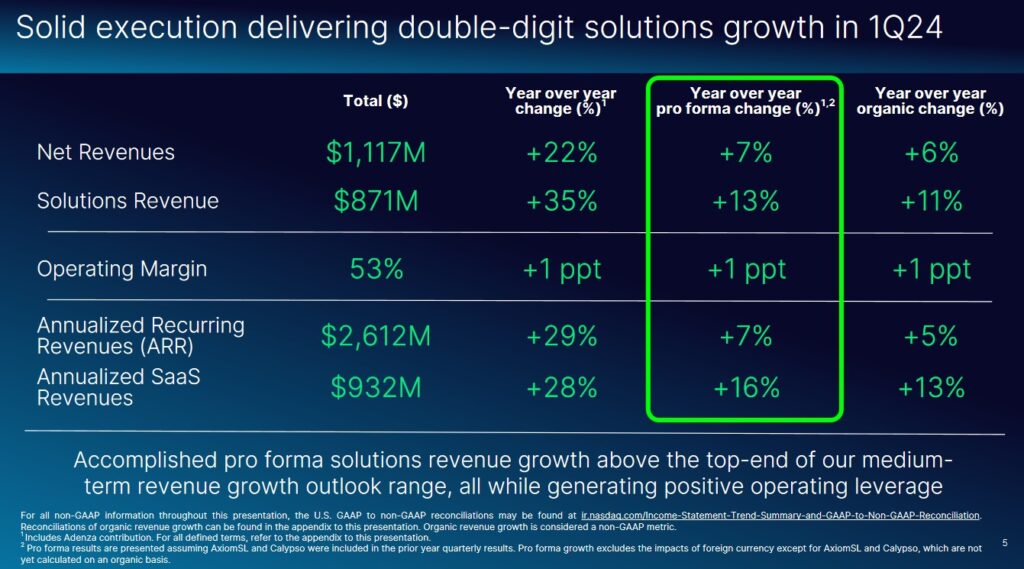

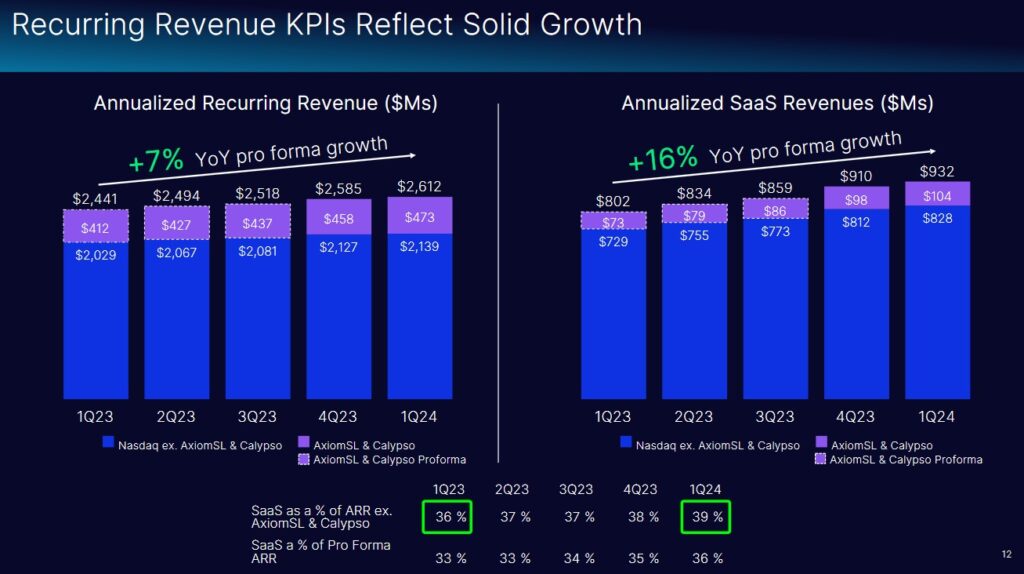

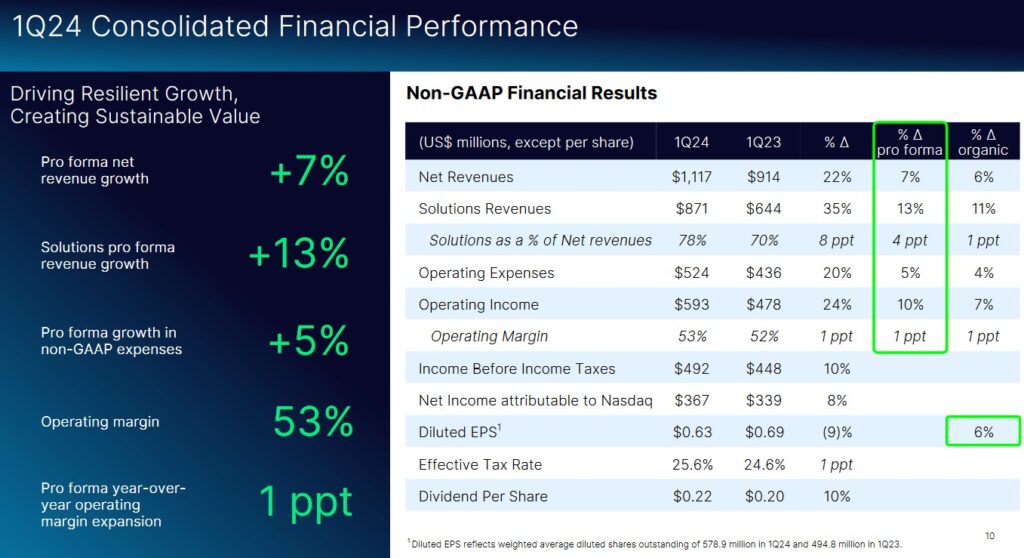

Q1 2024 Results

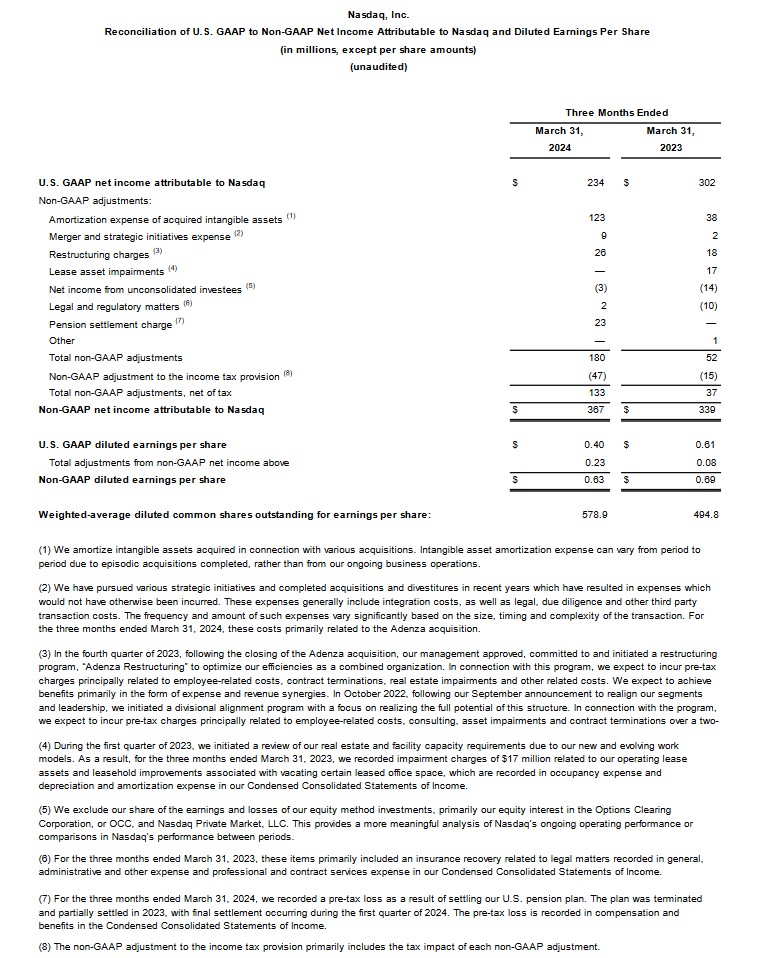

Investors might be disappointed with NDAQ’s Q1 results given that adjusted diluted EPS fell to $0.63 from $0.69 the prior year. It is important to remember, however, that last year’s major Adenza acquisition was financed with debt and the issuance of shares to the seller Thoma Bravo. Now, NDAQ’s interest carrying costs are much higher and earnings are spread over a larger number of shares.

Revenue from NDAQ’s index business segment increased 53% from last year and 15% from Q4 2023. NDAQ receives most of its index revenue from fees based on the amount of assets linked to its index. This creates a direct link between market valuations and NDAQ’s results.

Given that the Nasdaq 100 Index is heavily exposed to the technology sector, it stands to reason that NDAQ has benefited greatly. It is, however, important to recognize that NDAQ’s results can be volatile from quarter to quarter. This explains why NDAQ made the strategic Adenza acquisition in an effort to make its earnings less volatile by strengthening its annual recurring revenue (ARR).

The Data and Listings business was only up 1% YoY, as global growth in the data business was offset by headwinds from delistings and a muted initial public offering (IPO) environment.

During the quarter, NDAQ’s US listings business achieved a 69% win rate when considering NDAQ-eligible operating company listings. It welcomed 22 operating company IPOs, raising nearly $4B in proceeds. In addition, 4 companies, representing $9B in market value switched their listings to NDAQ during Q1.

The following images are extracted from the Q1 2024 Earnings Presentation that is accessible here.

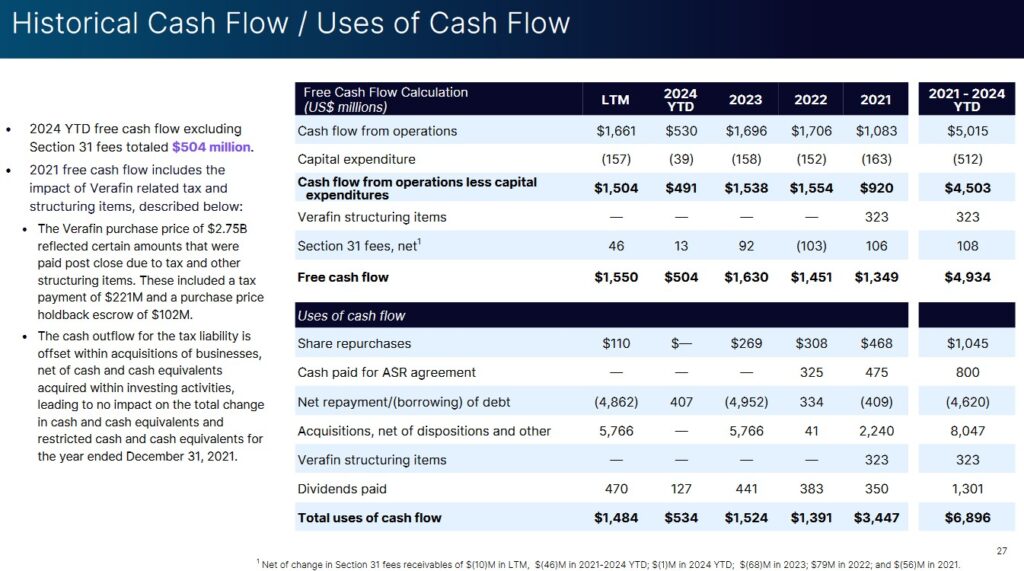

Operating Cash Flow (OCF) and Free Cash Flow (FCF)

NDAQ’s OCF and FCF in FY2021 – Q1 2024 is reflected below.

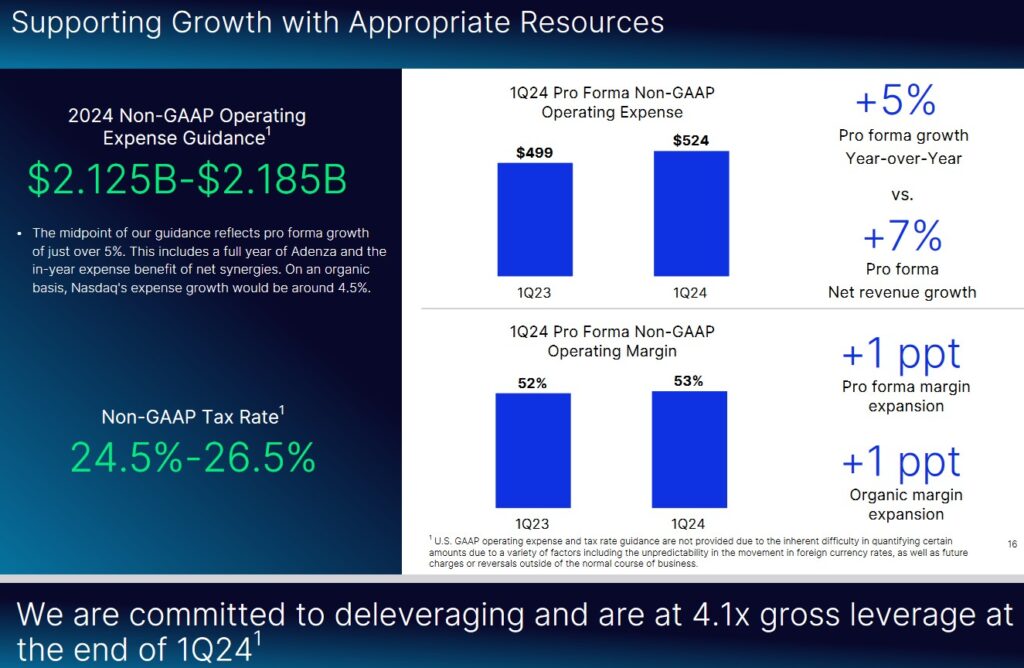

FY2024 Guidance

The following is NDAQ’s FY2024 guidance.

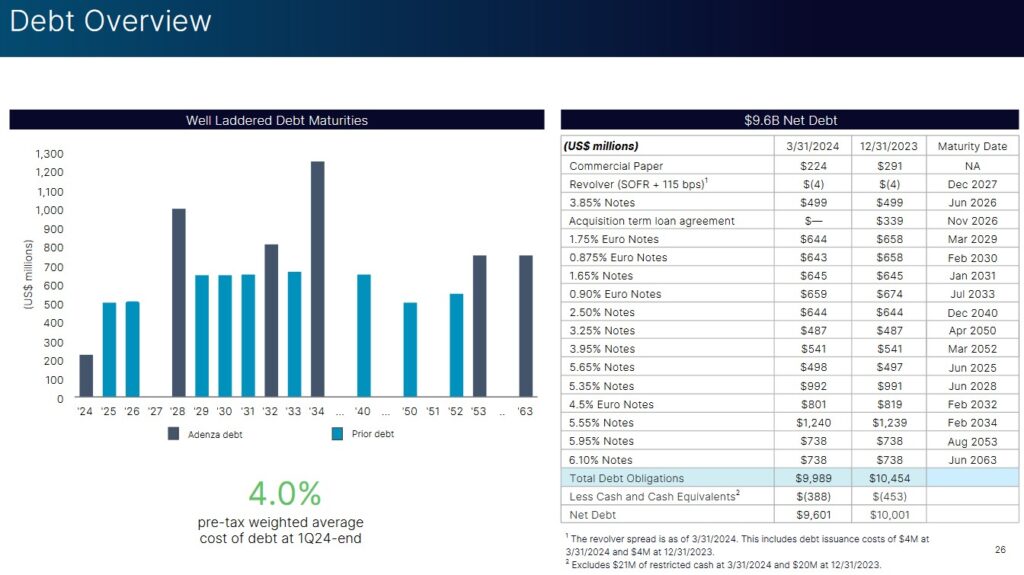

Credit Ratings

The following reflects NDAQ’s current net debt position at the end of Q1 2024 and FYE2023.

Immediately upon announcing the Adenza acquisition, NDAQ’s domestic unsecured long-term debt was downgraded from Baa1 to Baa2 by Moody’s and from BBB+ to BBB by S&P Global. These new ratings are the middle tier of the lower medium grade investment grade category. They define NDAQ as having an adequate capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to a weakened capacity for NDAQ to meet its financial commitments.

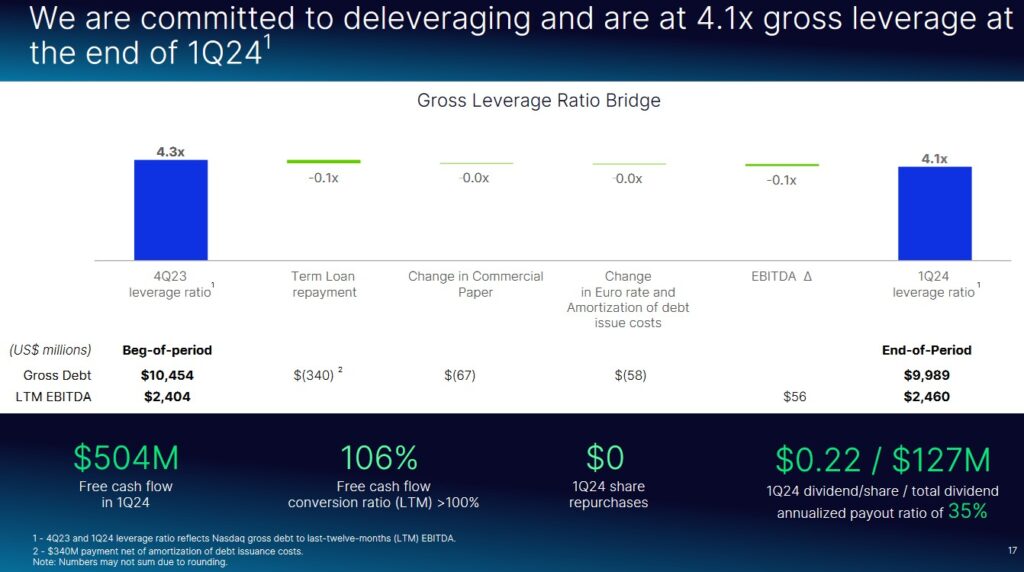

Despite the ratings downgrades, NDAQ has demonstrated its ability to reduce leverage within a reasonable time frame following major acquisitions. NDAQ’s capital allocation priority over the next 3 years will be to reduce Gross Debt / Non-GAAP EBITDA to 4.0x in 18 months and to 3.3x in 36 months.

NDAQ’s gross leverage ratio at FYE2023 and Q1 2024 are 4.3x and 4.1x.

Dividends, Share Repurchases, and Stock Splits

Dividend and Dividend Yield

NDAQ’s dividend history is accessible here.

On April 25, NDAQ’s Board declared a regular quarterly dividend of $0.24/share on the company’s outstanding common stock. This represents a ~9% increase from the previous quarter. The dividend is payable on June 28, 2024 to shareholders of record at the close of business on June 14, 2024.

The next 4 dividend distributions will total $0.96 (4 x $0.24). Using the current $60.30 share price, the forward dividend yield is ~1.6%.

NDAQ plans to increase the dividend to achieve a 35% – 38% payout ratio over the next 3 or 4 years; this implies a ~10% CAGR in the dividend payout ratio over this time frame. Calculation of this payout ratio annualizes the last paid quarterly dividend divided by the last 12 months of non-GAAP net income.

Share Repurchases

In September 2023, NDAQ’s Board approved an increase in its share repurchase authorization to a total of $2B. As of FYE2023 and Q1 2024, there was $1.9B remaining under the board authorized share repurchase program.

The weighted average number of shares outstanding in FY2013 – FY2023 (in millions of shares rounded) is 514, 519, 514, 506, 509, 503, 501, 501, 505, 49, and 508.4. The weighted average number of shares outstanding in Q1 2024 is 578.9.

The reason for the increase is because NDAQ issued 85.6 million common shares to Thoma Bravo for the Adenza purchase.

In FY2023, NDAQ repurchased $269 million of its common shares including $110 million in Q4 2023. Debt reduction is a priority so no shares were repurchased in Q1. NDAQ, however, plans to continue share repurchases to offset employee stock compensation.

After NDAQ’s leverage reaches target levels, the vast majority of remaining FCF will be applied toward share buybacks. Management states it does not anticipate making any significant acquisition-related capital allocation decisions that would deter the company from sizable stock buybacks over the coming years.

Stock Splits

NDAQ initiated a 3 for 1 stock split in 2022.

Valuation

In FY2013 – FY2023, NDAQ generated diluted EPS of $0.75, $0.80, $0.83, $0.21, $1.43, $0.91, $1.54, $1.86, $2.35, and $2.26. Its diluted PE levels were 20.52, 17.70, 27.31, 23.63, 49.57, 18.25, 33.89, 24.31, 30.57, and 26.91.

I reference my February 2, 2024 post in which I reflect NDAQ’s valuation at the time of my prior posts.

When I wrote my February 2 post, the following was NDAQ’s valuation using the current ~$57.80 share price and the current forward-adjusted diluted broker estimates:

- FY2024 – 15 brokers – mean of $2.77 and low/high of $2.59 – $3.03. Using the mean estimate, the forward-adjusted diluted PE is ~20.8.

- FY2025 – 14 brokers – mean of $3.10 and low/high of $2.93 – $3.34. Using the mean estimate, the forward-adjusted diluted PE is ~18.6.

- FY2026 – 6 brokers – mean of $3.47 and low/high of $3.27 – $3.60. Using the mean estimate, the forward-adjusted diluted PE is ~16.6.

I indicated that NDAQ’s primary focus is debt reduction so any shares repurchases in FY2024 will likely merely offset shares issued as part of the firm’s employee compensation packages. We can, therefore, expect the weighted average shares outstanding in FY2024 to be ~550.6 million. If it is able to generate $1.7B of FCF in FY2024, the forward FCF/share should be ~$3.09 which results in a forward P/FCF value of ~18.4 when I use the current ~$57 share price.

Using the current $60.30 share price and the forward adjusted diluted EPS broker estimates, NDAQ’s forward adjusted diluted PE levels are:

- FY2024 – 16 brokers – mean of $2.74 and low/high of $2.63 – $3.03. Using the mean estimate, the forward-adjusted diluted PE is ~22.

- FY2025 – 16 brokers – mean of $3.08 and low/high of $2.95 – $3.34. Using the mean estimate, the forward-adjusted diluted PE is ~19.6.

- FY2026 – 9 brokers – mean of $3.47 and low/high of $3.35 – $3.53. Using the mean estimate, the forward-adjusted diluted PE is ~17.4.

Clearly, my prior estimate of ~550.6 million was well off the mark. The weighted average number of shares outstanding in Q1 2024 is 578.9; I do not foresee a significant change over the remainder of FY2024.

In Q1, NDAQ generated ~$0.504B of FCF. I, therefore, think achieving $1.7B of FCF is attainable. If we divide $1.7B by 580 million shares, the FY2024 FCF/share should be ~$2.93. Divide the current $60.30 share price by $2.93 and the forward P/FCF is ~20.6.

Final Thoughts

I have no changes to my final thoughts reflected in my February 2 post.

The fruits of the Adenza acquisition will not come about overnight. NDAQ has higher interest costs resulting from the issuance of additional debt to assist in the financing of the acquisition. Furthermore, its earnings are now spread over a larger number of shares; shares were issued to Thoma Bravo as partial consideration of the Adenza acquisition. Thoma Bravo recognize the value of NDAQ will likely be much higher in the future.

In the short-term, investors should expect muted results from NDAQ. Once it reduces its Gross Debt / Non-GAAP EBITDA to target levels and the Adenza business is demonstrating steady growth, I expect NDAQ’s financial picture will permit it to resume the repurchase of issued and outstanding shares. This should contribute to stronger future EPS results.

I currently hold 606 shares in a ‘Core’ account within the FFJ Portfolio. NDAQ was not a top 30 holding when I completed my 2023 Year End FFJ Portfolio Review.

I intend to increase my NDAQ exposure but am looking to acquire shares in great companies that have temporarily fallen out of favor with investors. My hope is to acquire NDAQ shares at a better valuation and do not intend to immediately acquire additional shares.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long NDAQ.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.