Genuine Parts’ (GPC) has grown its dividend for 68 consecutive years thereby qualifying it for Dividend King status. Unfortunately, some investors base their investment decisions primarily/solely on dividend metrics. Do not let its Dividend King status influence your investment decision! Focus on the company’s underlying fundamentals, competitive strengths, risk, and total potential long-term shareholder return.

When I last reviewed Genuine Parts (GPC) in my October 20, 2023 post, it had just released its Q3 and YTD2023 results and once again increased its FY2023 outlook.

On April 18, 2024, GPC released its Q1 results and revised FY2024 outlook. I, therefore, revisit this existing holding.

Business Overview

GPC consists of two segments: Automotive Parts and Industrial Parts.

The company’s website and Part 1 Item 1 in GPC’s FY2023 Form 10-K are good sources of information to learn about the company.

Acquisitions

GPC continues to evolve its US Automotive operating model and is more intentional about owning more stores in selected priority markets. The company, however, continues to partner with its existing network of independent owners who play an important role in helping GPC serve its local markets.

In Q1, GPC made strategic acquisitions of 45 NAPA stores from independent owners. This was an increase from the acquisition of 33 NAPA stores in Q4 2023 and 16 in Q1 2023.

Financials

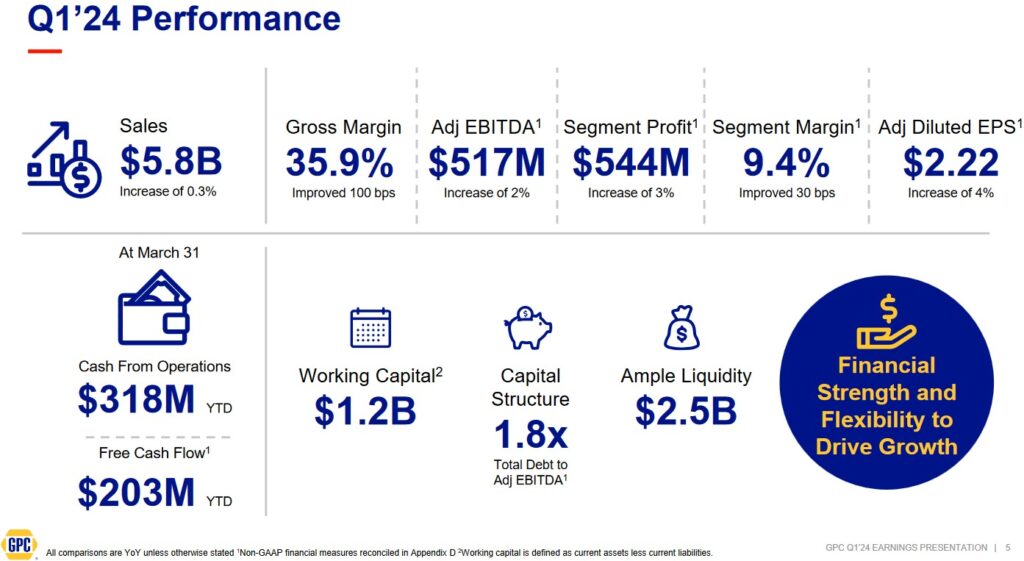

Q1 2024 Results

GPC’s Q1 2024 results are accessible here.

Lackluster demand across GPC’s automotive and industrial distribution businesses was offset by expanding segment margins (up 30 basis points to 9.4%).

After reporting steep market share losses in the US toward the end of FY2023, an improvement in inventory availability and in-store service levels contributed to better results. However, weakness in Canada and soft pricing gains contributed to the reporting of flat automotive comparable sales.

The industrial business segment results were in-line with management’s expectations. The company continues to see sales growth and strong renewal rates with corporate account customers; this represents 45% of the business. Furthermore, continued discipline on costs contributed to margin expansion.

During Q1, GPC incurred ~$83 million of nonrecurring costs on a pretax basis or $62 million after tax related to the global restructuring program.

On the Q1 earnings call, management stated that the start of 2024 continues to present a mix of challenges and opportunities. Higher interest rates and persistent cost inflation are pressuring businesses and consumers alike. Supportive industry fundamentals, however, are providing a positive backdrop for growth.

Within GPC’s global automotive business, there continues to be an increase in the number of miles driven. The fleet continues to age and new and used car pricing remains elevated, particularly with financing costs.

On the industrial side of GPC’s business, recent positive movement with key industry metrics supports management’s positive outlook for the balance of the year and business is expected to accelerate in the second half of 2024.

Motion, GPC’s industrial side of the company, benefits from a highly diverse portfolio of customers and end markets; it serves nearly all aspects of the industrial and manufacturing economy and is not heavily exposed to any one end market or customer.

GPC continues to expand into new areas of opportunities such as semiconductor technology. In the long term, trends around reshoring present a significant opportunity for Motion.

As expected, Motion’s sales were challenged in Q1 as it posted a slight YoY sales decline. Despite the more challenging top-line environment, the Motion segment of the business delivered an increase in profit conversion from Q1 2023.

Cash Flow

In Q1, GPC generated ~$0.318B in cash from operations and ~$0.203B in free cash flow (FCF).

At the end of Q1, GPC had $2.5B in available liquidity. Its debt-to-adjusted EBITDA ratio was 1.8x versus its 2 – 2.5x target range.

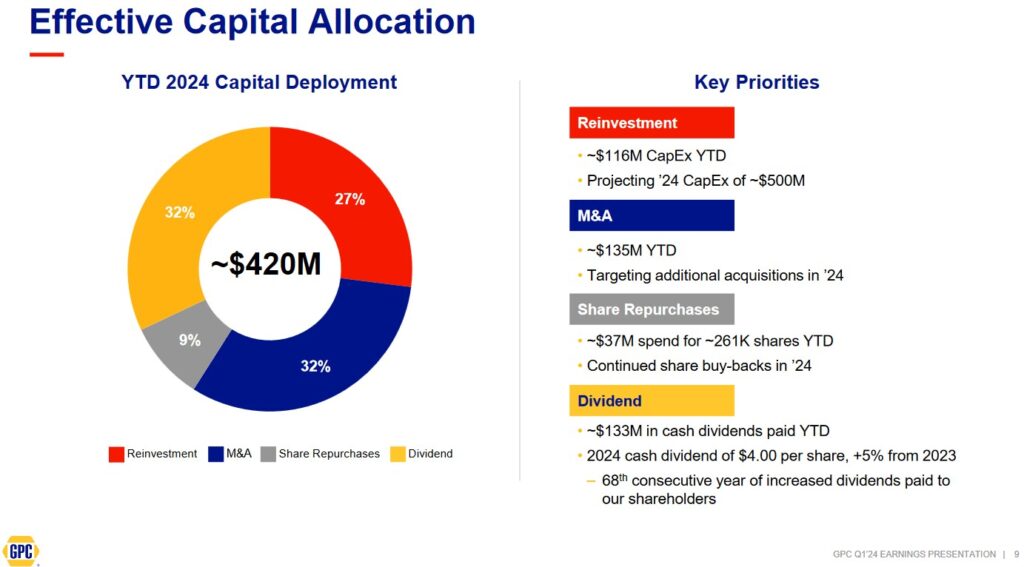

GPC reinvested $0.116B in the form of CAPEX and $0.135B in the form of strategic acquisitions, including bolt-on acquisitions in the U.S. to support the strategy to own more NAPA stores.

It also made a small acquisition for its Motion business in North America to expand its value-added service capabilities like fluid power and repair solutions.

The planed global restructuring efforts commenced in Q1. GPC continues to expect costs of ~$01.B – ~$0.2B of which most will be incurred in 2024. These costs will be reported as nonrecurring expenses.

The restructuring efforts are expected to deliver a benefit of $20 – $40 million in 2024 and $45 – $90 million on an annualized basis.

Costs related to the restructuring program in Q1 amounted to ~ $83 million These costs are categorized as:

- costs associated with the voluntary retirement program; and

- facility optimization.

In Q1, ~65% of the restructuring expenses were associated with the voluntary retirement offer. The remaining costs are related to facility closures and start-up costs associated with new facilities that replaced those that were shut down.

The Q1 restructuring activities, including the voluntary retirement offer, were completed in line with management’s expectations, and management expects to start realizing benefits in Q2.

Capital Allocation

This is GPC’s YTD2024 capital allocation.

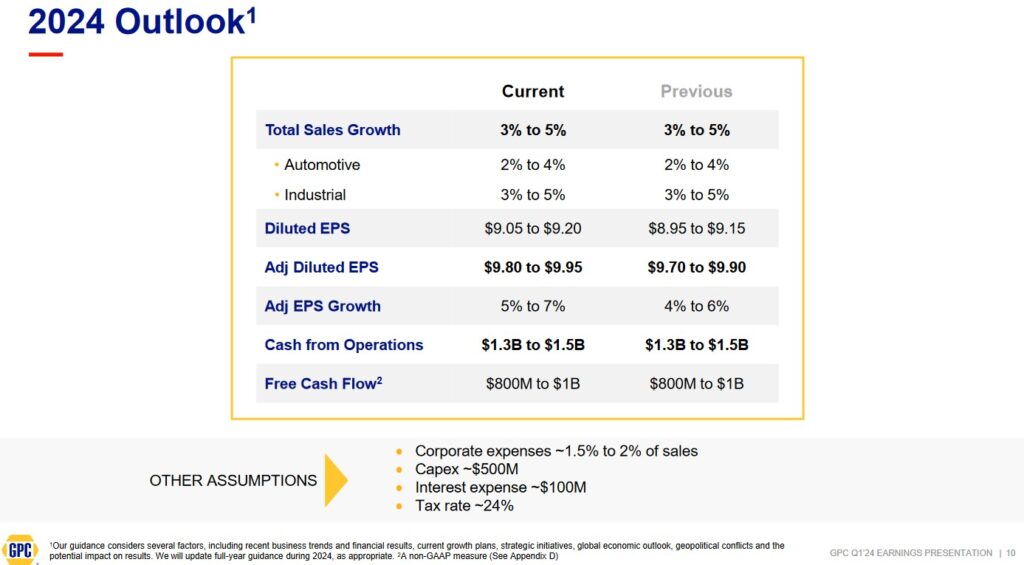

FY2024 Outlook

The following reflects GPC’s updated FY2024 outlook.

GPC expects 3% – 5% total sales growth with a more moderated first half and stronger second half for both automotive and industrial. The outlook includes the assumption that the benefit from inflation remains at more normalized levels contributing less than 1% for both business segments.

Full year gross margin expansion is now forecast at 30 – 50 bps. This increase is driven by the company’s continued focus on strategic sourcing and pricing initiatives. This gross margin expansion is an increase from the previous 20 – 40 bps guidance.

The outlook also assumes that SG&A will deleverage between 20 – 30 bps with most of this being derived through further investments in technology.

FY2025 Financial Targets

GPC’s FY2025 financial targets are presented in my March 23 post. I, however, provide them again for ease of reference.

Source: GPC Investor Day Presentation – March 23, 2023

Credit Ratings

GPC’s unsecured long-term debt ratings remain unchanged from the time of my October 2023 review.

- Moody’s: Baa1 (stable outlook)

- S&P Global: BBB (stable outlook)

Moody’s rating is the top tier of the lower medium grade. S&P Global’s rating is the middle tier of the lower medium grade. Both ratings are investment grade and are defined as an obligor having ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

On December 1, 2023, S&P Global assigned an A2 short-term issuer credit rating stating:

The ‘A2’ short-term rating reflects our ‘BBB’ long-term issuer credit rating on GPC. Our rating reflects the company’s leading positions in both the automotive maintenance and repair and industrial maintenance and repair industries. We believe GPC’s scale, distribution capabilities, and brand recognition through the NAPA banner support its long-term market position. Our view also reflects its business and geographic diversity, consistent profit growth, and healthy free cash generation. We assess GPC’s liquidity as strong, supported by its solid free operating cash flow generation, which has averaged $1 billion annually for the past five years. The company plans to use its $1.5 billion revolving credit facility due 2026 as a liquidity backstop for the notes issued under its Commercial Paper program. We expect GPC will maintain sufficient capacity to cover its Commercial Paper maturities.

GPC’s ratings are satisfactory for my purposes.

Dividends and Share Repurchases

Dividend and Dividend Yield

GPC’s dividend history is accessible here.

Investors fixated on dividend metrics will be impressed with GPC’s track record of 68 consecutive years of dividend increases. My interest, however, lies in an investment’s TOTAL potential long-term shareholder return. I, therefore, am indifferent if a company distributes no/little dividend IF the retention of earnings translates into attractive long-term investor returns.

At the beginning of May, investors can expect GPC to declare another $1.00 quarterly dividend for distribution at the beginning of July.

I anticipate that in February 2025, GPC will increase its quarterly dividend by ~$0.05. If this does occur, the next 4 quarterly dividend payments will total $4.05 ((3 x $1.00) + $1.05. Using the current ~$160 share price, the forward dividend yield is ~2.53%.

Share Repurchases

GPC’s approximate weighted average shares outstanding in FY2012 – FY2023 are (in millions of shares) 156, 156, 154, 152, 150, 148, 147, 146, 145, 144.2, 142.3, and 141.

In Q1 2024, GPC repurchased ~261,000 shares for $37.5 million (average cost ~$143.7). The weighted average common shares outstanding for the quarter ending March 31 was ~140.1.

The company expects to remain active in its share repurchase program. However, the amount and value of shares repurchased will vary and is at the discretion of the Board.

Valuation

When I wrote my October 20, 2023 post, GPC shares were trading at ~$133. Using this share price and the forward-adjusted diluted earnings estimates from the brokers that cover GPC, the forward-adjusted diluted PE levels were:

- FY2023 – 15 brokers – ~14.4 based on a mean of $9.23 and low/high of $9.16 – $9.32.

- FY2024 – 15 brokers – ~13.3 based on a mean of $9.97 and low/high of $9.49 – $10.25.

- FY2025 – 9 brokers – ~12.05 based on a mean of $11.04 and low/high of $10.65 – $11.59.

I have been a GPC shareholder since July 24, 2017. Other than roughly mid/late March 2020 when the North American economy shut down because of COVID, I do not recall GPC having ever been valued so attractively. I had hoped GPC would be aggressively repurchasing shares but that did not happen!

Following the release of Q1 2024 earnings and amended FY2024 outlook on April 18, GPC’s share price surged to ~$160 from the prior day’s $144 closing share price. Using the company’s revised FY2024 adjusted diluted EPS outlook of $9.80 – $9.95, the forward adjusted diluted PE range is ~16.1 – ~16.3.

Its valuation using current broker estimates, which will undoubtedly be revised over the coming days, is:

- FY2024 – 13 brokers – ~16.3 based on a mean of $9.84 and low/high of $9.76 – $9.98.

- FY2025 – 13 brokers – ~15 based on a mean of $10.66 and low/high of $9.84 – $11.02.

- FY2026 – 6 brokers – ~ 14.1 based on a mean of $11.37 and low/high of $10.39 – $11.72.

If GPC repurchases shares at a similar rate over the next 3 quarters, I envision the weighted average outstanding shares in FY2024 will be ~139.5 million. Using the $0.9B mid-point of GPC’s FY2024 FCF outlook, GPC should generate ~$6.45 of FCF per share. Using the current ~$160 share price, we get a P/FCF share value of ~24.8. In comparison, GPC’s FY2014 – FY2023 P/FCF is 20.38, 12.00, 14.30, 18.85, 11.80, 16.15, 9.17, 12.82, 16.55, and 15.02. Looking at GPC’s valuation on a P/FCF basis, it appears shares are now overvalued relative to historical levels. It is important to remember, however, that results prior to FY2020 are not a good comparison because GPC owned two underperforming business segments (see below).

Final Thoughts

When I last wrote about GPC, I disclosed the purchase of additional shares on October 19 @ $130.61 bringing my GPC exposure to 465 GPC shares in a ‘Core’ account within the FFJ Portfolio.

I initiated a 300 share GPC position on July 24, 2017 @ ~$82.22/share. Over the years, this has grown to 471 shares. My exposure, however, is negligible and GPC did not come remotely close to being a top 30 holding when I completed my 2023 Year End FFJ Portfolio Review.

While GPC’s Dividend King status may appeal to some investors, my decision to invest in GPC was not influenced by dividend metrics.

When I initiated my GPC position, I saw a company that was being dragged down by its non-core Electrical/Electronics Materials Group and Office Products Group. Both businesses were underperforming and I envisioned that GPC would divest itself of these businesses and thus hopefully improve its overall performance.

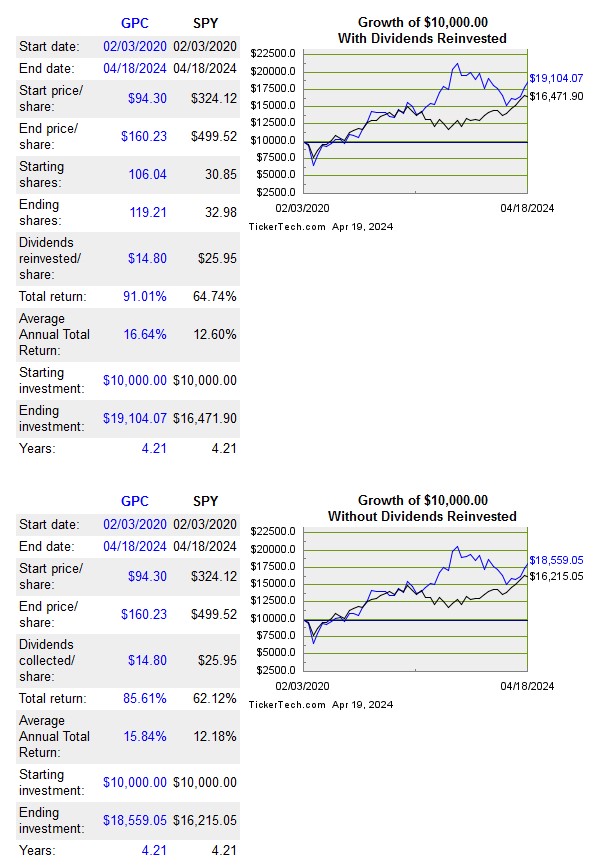

GPC completed the divestiture of its Electrical/Electronics Materials Group in September 2019 and the divestiture of its Office Products Group in January 2020. Subsequent to these divestitures, GPC’s average annual total return has improved considerably.

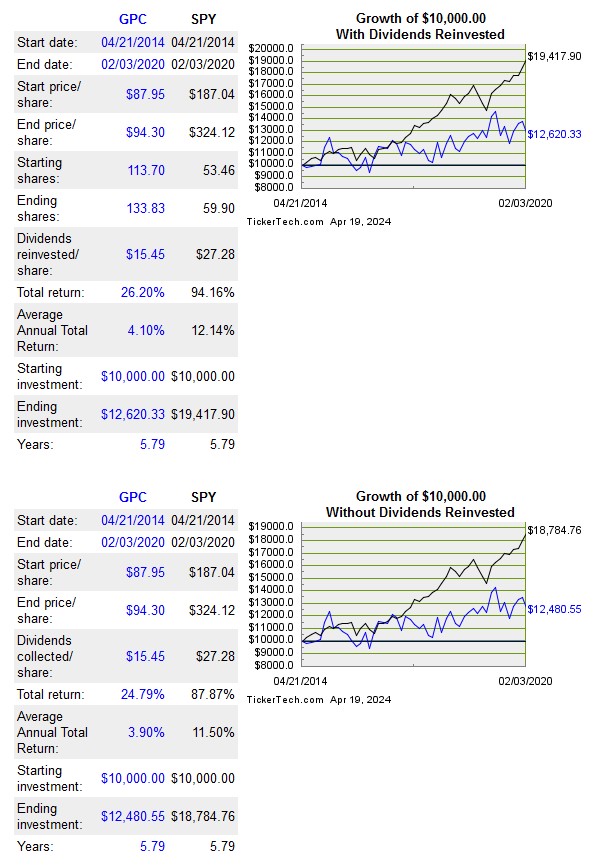

While past performance is not indicative of future performance, the following reflects how GPC has performed following the divestiture of 2 non-core business segments.

Source: Tickertech

We see a noticeable improvement in GPC’s recent performance with its performance for the 5.79 years PRIOR to the divestiture of of 2 non-core business segments!

Source: Tickertech

GPC stated at its March 23, 2023 Investor Day that it is targeting $11.00 – $11.50 in diluted EPS in FY2025. If we use this range and a 14.5 PE multiple, we end up with a ~$160 – ~167 price range. GPC shares, however, are currently trading at ~$160. If GPC’s PE multiple expands to 16, we get a ~$176 – ~$184 share price range. I, however, think a PE multiple of 16 is too high. If we conservatively use $11 and a 14 PE multiple, a price below ~$154 appears to be closer to a fair value.

As noted in several prior posts, I prefer to acquire shares in great companies that appear to have temporarily fallen out of favor. GPC’s ~$16 share price surge following the release of Q1 results suggests investors have warmed up to GPC. I do not, therefore, intend to add to my exposure at the current valuation.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long GPC.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.