In my April, June, and July 2022 Intuitive Surgical (ISRG) posts, I deemed shares to be attractively valued and disclosed the purchase of additional shares. In subsequent ISRG posts that are accessible through the FFJ Archives, however, I have disclosed my decision not to add to my exposure because I felt shares were overvalued.

I last reviewed ISRG in this January 24 post at which time the most currently available financial information was for Q4 and FY2023.

Following the April 18 market close, ISRG released its Q1 2024 results thus prompting me to revisit this existing holding.

Business Overview

I recommend you review the company’s website and FY2023 Form 10-K to gain an understanding of the business if you are unfamiliar with the company.

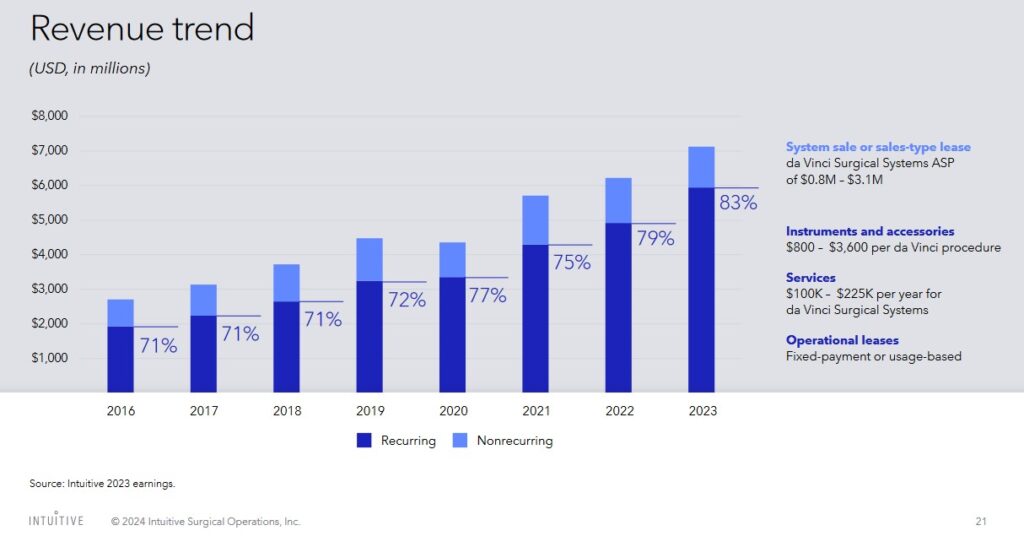

We see from ISRG’s recent results that a significant number of medical procedures are being performed using ISRG’s various systems.

Source: ISRG – Q1 2024 Investor Presentation

An attractive feature of the company is the extent to which it has increased its recurring revenue over the past several years. This makes it easier to gauge how a company is likely to perform over the next several quarters versus a company which generates difficult to predict transactional revenue.

Source: ISRG – Q1 2024 Investor Presentation

Financials

Q1 2024 Results

ISRG’s Q1 results are provided in the Form 8-K released on April 18; the Q1 2024 Form 10-Q is also available in the SEC Filings section of the company’s website.

First quarter revenue was $1.891B, an increase of 11% from Q1 2023. On a constant currency basis, revenue growth was 12%.

Leasing represented 51% of Q1 placements compared with 42% in Q1 2023.

During the quarter, ISRG witnessed elevated patient volume from the return of patients post pandemic. Procedure performance was led by broad growth in general surgery in the United States, and by procedures beyond urology outside the United States. Globally, cholecystectomy, colon resection and foregut procedures led the way.

Regional performance included strength in China, Germany and the United Kingdom.

In Japan, ISRG experienced a moderation of growth in urology as it has achieved higher levels of penetration and Q1 2023 benefited from the return of patients in backlog.

In Korea, growth was lower than expected. This was primarily due to the continuation of a physician strike which began in February.

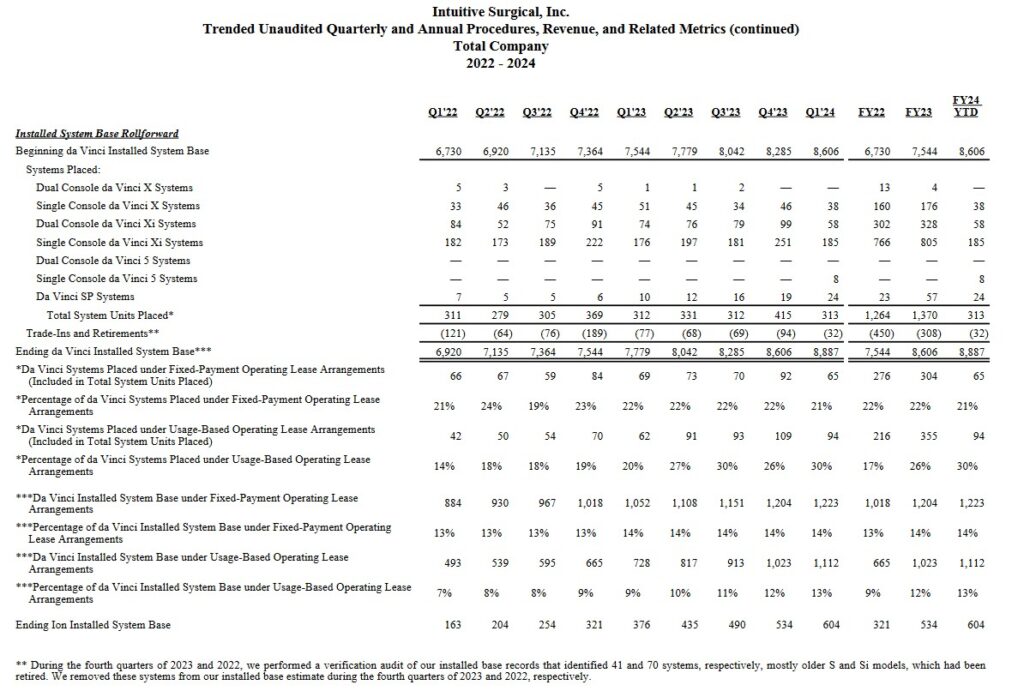

A wealth of information is found in the Q1 2024 Financial Data Tables. For ease of reference, however, I provide the following table which reflects how many systems have been placed in recent quarters and the extent to which ISRG’s installed system base has grown.

Given customer preference for ISRG’s usage-based models in the U.S. and the launch of da Vinci 5, ISRG continues to expect the proportion of systems placed under lease arrangements to grow over time; ISRG announced FDA clearance of its Fifth-Generation Robotic System, da Vinci 5 in this March 14, 2024 press release.

The Q1 system average selling prices (ASP) were $1.39 million as compared to $1.47 million in Q1 2023. System ASPs were negatively impacted by regional and platform mix and lower pricing in China, partially offset by lower trade-ins. Product margins, however, were within management’s expectations.

Operating expenses came in slightly below plan, resulting in pro forma operating profit growth of 18%.

In the quarter, ISRG made good progress with its new platforms. In March, it received FDA clearance for the next-generation multiport platform, da Vinci 5; 8 da Vinci 5 systems were placed in Q1 and surgeons completed their first cases.

With respect to the ION platform, there were ~19,500 ION procedures in Q1 2024 representing a ~90% increase from Q1 2023. Since launching the ION platform in 2019, on a cumulative basis, more than 100,000 procedures have now been performed.

In Q1, ISRG placed 70 ION systems compared to 55 in Q1 2023 and 44 in Q4 2023; Q1 results reflect a partial recovery from Q4 as catheter supply improved.

Q1 results included 4 ION system placements in the U.K. following European clearance last year. The installed base of ION Systems increased to 604 systems of which 244 are under operating lease arrangements.

FY2024 Outlook

At the end of Q4 2023, ISRG forecast 13% – 16% FY2024 procedure growth. ISRG is now revising this forecast to reflect 14% – 17% growth.

The low end of the range assumes further weakness in bariatric procedures, along with challenges in China from increasing provincial robotic competition and delayed tenders impacting capital placements. The assumption also assumes no benefit of patient backlog in the year.

At the high end of the range, ISRG assumes bariatrics continues at flat to slightly positive growth rates and factors in China do not have a significant impact on the business. Furthermore, the assumption is that the patient backlog will decline over the remainder of the year.

The expectation is that pro forma gross profit margin will be within 67% – 68% of net revenue. Pro forma gross profit margin in 2024 reflects the impact of growth in newer products, da Vinci 5, ION and SP and the impact of capital investments that will come on to support business growth. The actual gross profit margin will vary quarterly depending largely on product, regional and trade-in mix and the impact of new product mix.

Guidance for pro forma operating expense growth remains at 11% – 15%.

Non-cash stock compensation expense of $0.68B – $0.71B is forecast for FY2024.

FY2024 guidance for other income, comprised mostly of interest income, remains unchanged at $0.29B – $0.32B.

The FY2024 CAPEX forecast remains unchanged at $1B – $1.2B (primarily for planned facility construction activities).

There is no change to the FY2024 pro forma income tax rate of 22% and 24% of pretax income.

Credit Ratings

No rating agency rates ISRG because it has no debt.

Dividend and Dividend Yield

ISRG does not distribute a dividend.

Share Repurchases

The weighted average number of diluted shares outstanding in FY2013 – FY2023 (in millions) is 339, 341, 354, 349, 356, 358, 361, 366, 362, and 357.4. ISRG repurchased no shares in Q1 2024 to offset the issuance of common stock relating to employee stock plans. As a result, the weighted average number of diluted shares outstanding in Q1 2024 rose to 360.5.

There is currently a remaining authorization to repurchase $1.1B of shares.

Valuation

FY2011 – FY2023 PE ratios based on GAAP earnings are 40.02, 30.69, 22.97, 46.20, 37.72, 34.17, 47.07, 72.02, 53.69, 93.18, 77.44, 70.38, and 79.38.

At the time of my January 24 post, I anticipated revisions to broker estimates over the coming days. The forward-adjusted diluted PE estimates using the current ~$370 share price, however, were:

- FY2024 – 26 brokers – ~59 based on a mean of $6.29 and low/high of $5.96 – $6.76.

- FY2025 – 21 brokers – ~50 based on a mean of $7.36 and low/high of $6.76 – $8.34.

- FY2026 – 14 brokers – ~43 based on a mean of $8.63 and low/high of $7.84 – $10.12.

Shares currently trade at ~$366 as I compose this post. Revisions to broker estimates are likely over the coming days. For now, however, the forward-adjusted diluted PE estimates are:

- FY2024 – 26 brokers – ~58.4 based on a mean of $6.27 and low/high of $5.96 – $6.58.

- FY2025 – 26 brokers – ~50 based on a mean of $7.34 and low/high of $6.87 – $7.76.

- FY2026 – 18 brokers – ~42.6 based on a mean of $8.60 and low/high of $7.85 – $9.29.

In essence, there has been virtually no change in ISRG’s rich valuation.

Final Thoughts

My thoughts on ISRG remain the same from those presented in recent previous posts.

In ISRG, we have a profitable growing company that generates very strong free cash flow. Furthermore, it has sufficient liquidity that it could eliminate 100% of its total liabilities and still have a few billion dollars of available liquidity.

ISRG will not appeal to some investors because it does not distribute a dividend. Focusing exclusively on dividend metrics, however, can lead to poor investment decisions. A preferable way to look at an investment is the potential total investment return (don’t forget the risk aspect of an investment!).

Naturally, a company that distributes no dividend means 100% of any investment return will be derived from capital appreciation. It is, therefore, imperative we pay particularly close attention to valuation.

It is very easy to get caught up in the euphoria and to invest in great companies when everyone and their dog want a ‘piece of the action’. Investing based on share price behavior with no regard to valuation, however, can often lead to unpleasant consequences.

No investor makes a perfect investment decision 100% of the time. We should, however, at least stack the odds of a favorable outcome in our favor.

I choose to bide my time in the hope of an event that leads to ISRG becoming more attractively valued. Until such time as this occurs, I will continue to be satisfied with my 450 share exposure in a ‘Core’ account in the FFJ Portfolio; it was my 15th largest holding when I completed my 2023 Year End FFJ Portfolio Review.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long ISRG.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.