![]()

Summary

- SJM is facing headwinds and revenue growth and profit margins are expected to remain under pressure amid a competitive environment and challenging retailer dynamics.

- SJM is currently exploring the divestiture of its US baking business and a sale of this business will likely impact FY2019 projections.

- Shareholders have been aptly rewarded over the long-term but returns over a 10 year or shorter timeframe have been inferior to returns generated by the S&P500.

- The stock is trading at an attractive valuation which should bode well for investors with a long-term investment time horizon.

- There are far more attractive companies in which to invest but they are overvalued. Investors anticipating a market correction in the not too distant future might be wise to pass on SJM and to wait for more attractive valuations from superior companies.

Introduction

On May 30, 2017, just prior to me initiating a position in The J.M. Smucker Company (NYSE: SJM) in early June 2017, SJM announced the signing of a definitive agreement to acquire the Wesson® oil brand from Conagra Brands, Inc.. In my June 10, 2017 article I outlined my rationale for initiating a 200 shares position in the company; my analysis was based on the following guidance from the company.

Source: SJM – Q4 and FY2017 Earnings Presentation – June 8 2017

SJM’s stock price dropped subsequent to my purchase but I still felt comfortable with my decision to invest in the company and viewed the price drop as an opportunity to acquire another 200 shares in July 2017.

On August 24, 2017, SJM released its Q1 2018 results and revised its adjusted EPS forecast for FY2018 downward.

Source: SJM – Q1 2018 Earnings Presentation – August 24 2017

Despite the downward revision in projections I viewed a 10,000 share purchase by Richard K Smucker (Chairman) as a vote of confidence in the company; this purchase increased the total holdings in his name to more than 652,000 shares.

Based on my review of the Q1 2018 results and projections I continued to be satisfied that SJM warranted a place in the FFJ Portfolio.

SJM’s stock price rebounded in November 2017 but had still not retraced to the level of my average cost. Based on further analysis, I decided that I would write 4 July 2018 out-of-the-money covered call contracts with a 125 strike price when SJM was trading at ~$111,; 4 option contracts represents 400 shares.

By the second last week of January 2018, SJM had risen to ~$131 meaning that the buyer(s) of the option contracts could have exercised their option to acquire my SJM shares for $125. Same was not done.

The stock pulled back below $125 in late January but subsequently rose to the ~$130 level around the beginning of March.

In early March, the US Federal Trade Commission filed an administrative complaint challenging SJM’s proposed acquisition. While SJM and Conagra objected to the complaint, on March 6, 2018 they mutually agreed to terminate the definitive agreement.

Subsequent to the mutually agreeable announcement to terminate the Wesson® oil brand acquisition, SJM’s tock price retraced to just below $100; it has recently risen to ~$106.

Since SJM has just released its FY2018 results and has provided its FY2019 forecast I am now taking this opportunity to reanalyze SJM.

Q1 2018 Financial Results

SJM’s Q4 and FY2018 results released June 7, 2018 can be found here.

I also encourage you to review the February 21, 2018 CAGNY presentation to get a more comprehensive overview of all the initiatives in progress which are expected to translate into improved results.

Investors did not initially react positively to SJM’s FY2018 results. One of the factors that impacted market sentiment was SJM’s apparent need to increase spending on ads in 2019 in order to increase sales as its base business continues to remain under pressure amid a competitive environment and challenging retailer dynamics.

On an encouraging note, SJM generated ~$0.896B in free cash flow in FY2018 versus ~$0.866B in FY2017.

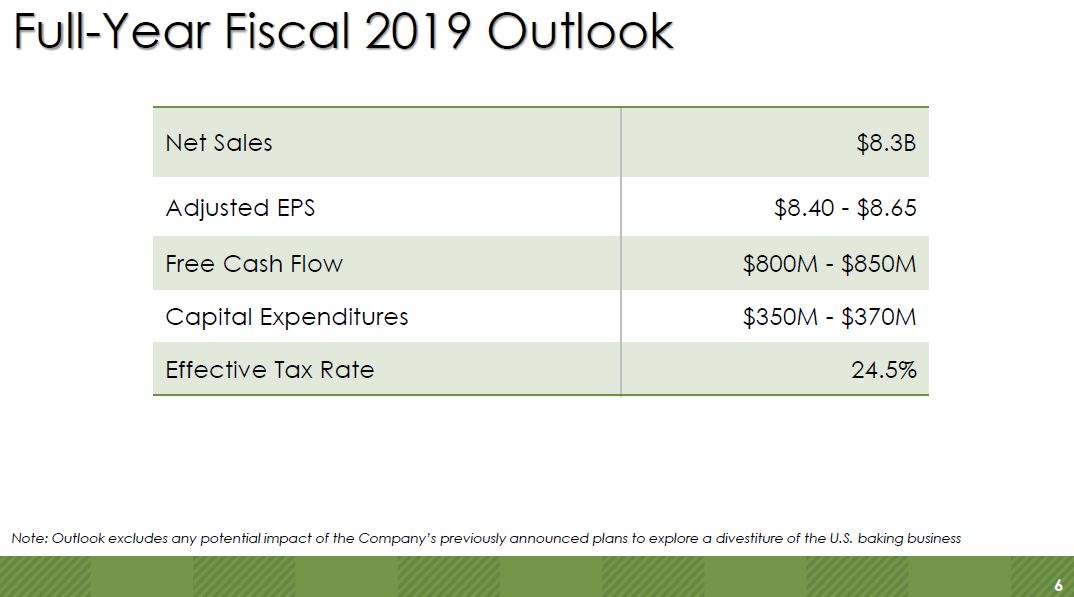

2019 Guidance

SJM provided the following FY2019 guidance on June 7, 2018 which is based on based on 113.6 million shares outstanding.

Source: SJM – Q4 and FY2018 Earnings Presentation – June 7 2018

This guidance does not include any potential impact from the previously announced plans to explore the divestiture of the US baking business.

Net sales are expected to increase 13% compared to FY2018. This increase is primarily attributed to the acquisition of Ainsworth Pet Nutrition, LLC., the full-year benefit of a lower effective tax rate as a result of U.S. income tax reform, and cost savings initiatives. These benefits, however, are expected to be partially offset by anticipated raw materials and freight cost increases and higher interest expense. In addition, marketing expense is expected to increase significantly, including approximately $50 million in support of the launch of 1850TM coffee and Jif® PowerUps TM.

Credit Ratings

Moody’s downgraded SJM two notches from A3 (lowest tier of the upper medium grade category) to Baa2 (middle tier of the lower medium grade category) in March 2015. Despite this downgrade, SJM is still classified as investment grade.

S&P Global downgraded SJM’s long-term debt to BBB in February 2015 and reaffirmed this rating in April 2018. This rating is the middle tier of the lower medium grade category.

I view the risk level associated with these ratings as acceptable.

My Current Average Cost

As previously indicated, I wrote 4 covered call option contracts with a $125 strike price which expire July 20th. I have no way of knowing whether SJM’s stock price will rise above this level before the expiry date but I strongly suspect it will not. I SJM’s stock price is below $125 at expiry, I will retain the~$1160 in option premium I collected at the time I wrote the contracts.

Taking into consideration the price I paid for the 2 blocks of 200 shares I purchased, the cost of the additional shares I acquired through the automatic reinvestment of the SJM quarterly dividend income, and the option premium noted above, my average cost is ~$120/share. I am currently underwater given the current ~$106 price but this does not concern me as I purchased SJM as a long-term investment.

Valuation

In my June 9, 2017 article I indicated I had just acquired 200 SJM shares @ $127.52. When I made this initial purchase, management had provided a 2018 full year adjusted EPS outlook of $7.85 – $8.05 at the time of its Q4 2017 and FY2017 earnings announcement on June 8, 2017. I chose to be conservative and used the lower end of this range in my analysis and came away with a forward adjusted PE of ~16.25.

My second 200 share purchase was at $118.629. Using the low end of the above noted full year adjusted EPS outlook I came away with a ~15.11 forward adjusted PE.

In August 2017, SJM revised its adjusted EPS outlook to $7.75 – $7.95. In November 2017, this outlook was revised to $7.75 – $7.90. In all three of these projections, management anticipated free cash flow (FCF) would be $0.775B and capital expenditures would be $0.31B.

On February 16, 2018, SJM revised its adjusted EPS outlook to $8.20 – $8.30 with FCF of $0.825B and capital expenditures remaining unchanged at $0.31B. As a result of the Tax Cut and Jobs Act, SJM revised its adjusted tax rate from 32.5% – 33% to 28%.

At the time of the release of Q3 2018 results on February 16, 2018, SJM was trading at ~$125. Using the low end of the revised adjusted EPS outlook, I arrived at a forward adjusted PE level of ~15.24.

Now, SJM’s FY2019 guidance calls for adjusted EPS of $8.40 – $8.65. Using the current ~$106 stock price, we get a forward adjusted PE of ~12.4. This valuation level is even more attractive than that of my second 200 share purchase; this is due to the headwinds SJM faces in its business. Having said this, the valuation level is such that investors initiating a purchase at current levels will very likely be reasonably rewarded over the long-term.

Dividend, Dividend Yield, and Dividend Payout Ratio

SJM’s dividend history can be found here. On the basis of the current ~$106 stock price, SJM’s dividend yield is ~2.94%.

The June 1, 2018 dividend payment marked the 4th consecutive $0.78 quarterly dividend. The next dividend should be declared mid-July at which time I anticipate at $0.03 increase to $0.81.

If my dividend increase projection is correct, the annual dividend of $3.24 will represent a ~38.6% dividend payout ratio using the low end of the projected 2019 adjusted EPS ($8.40). This low dividend payout ratio gives me a reasonable level of confidence that SJM will have no difficulty in increasing the quarterly dividend by my $0.03 projection.

Historical Returns

The following graph compares the cumulative total shareholder return on SJM’s common stock for the last five years with the cumulative total return on the S&P 500 Index and its peer group; dividend reinvestment is assumed.

This graph has been extracted from SJM’s FY2017 10-K as the FY2018 10-K is not yet available. As you can see, the 5 year period analyzed indicates SJM has not been an exceptionally strong investment over the short-term.

Source: SJM 2017 10-K (page 70 of 150)

If we look at SJM’s performance over a 10, 15, and 17.8 year timeframe (the site I use to obtain these graphs will not allow me to go beyond the 17.8 year timeframe), we see that SJM’s total investment returns with reinvested dividends slightly exceed those generated by the S&P500 over the 10 and 15 year periods. The return over the 20 year time horizon, however, far exceeds that of the S&P500.

Source: TickerTech.com

Final Thoughts

I recognize SJM is not my most astute investment decision to date. This is a company that is currently undergoing a transformation and is facing some headwinds. I am not, however, giving up on this investment as I am confident management will guide the company through this challenging period.

Having said this, I am not about to acquire additional shares despite the attractive valuation since I have a full position. I will, however, continue to automatically reinvest the quarterly dividends; this adds a couple of shares per quarter to my SJM position.

If you do not currently hold a SJM position I would refrain from initiating one. I think there are better companies out there in which to invest although they may not be currently attractively valued. Keep your ‘powder’ dry for when some of these companies become more attractively valued.

I hope you enjoyed this post and I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long SJM.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.