Genuine Parts – Fairly Valued Dividend King

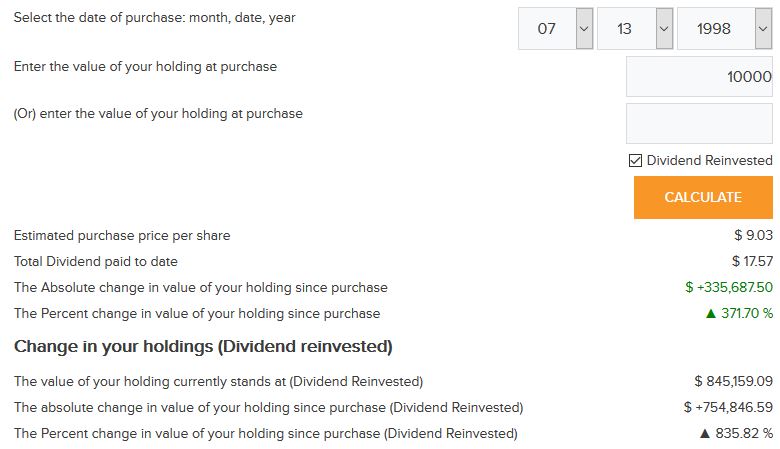

Summary Strong Q2 results recently reported and projected earnings for FY2018 reaffirmed. Shareholder returns on the basis of dividends reinvested over the past 20 years are almost double that of the S&P500. Share price has risen ~10% from the level at which my previous article indicated shares were attractively valued. Despite this increase, shares are [...]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}