Summary

Summary

- Alimentation Couche-Tard released its Q4 and FY2018 results at the close of business July 9th.

- On March 22nd, I wrote that the pullback in the company’s stock price presented investors with a window in which to acquire shares in the world’s 2nd largest convenience store operator at an attractive valuation.

- The company is now the largest company on the basis of revenue of any Canadian based company.

- Being extremely cost conscious and focusing on meeting customer needs presents the company with ample growth opportunities in this highly fragmented industry.

Alimentation Couche-Tard Inc. (TSX: ATD.a and ATD.b) reports its financial results in USD. Its stock, however, is traded on the TSX. Investors willing to purchase US shares over the counter should look at ANCUF. These shares, however, are very thinly traded.

ATD has Class A multiple-voting shares which are primarily held by insiders and which are very thinly traded. This article will deal with the more commonly traded Class B subordinated voting shares.

ATD uses USD as its reporting currency since it provides more relevant information given the predominance of its operations in the United States. This article, therefore, reflects all figures in USD unless otherwise noted.

Introduction

Readers unfamiliar with Alimentation Couche-Tard Inc. (TSX: ATD.a and ATD.b) might recognize the company’s Circle K, Mac’s, and Ingo brands.

In my March 22, 2018 Alimentation Couche-Tard – Attractive After Recent Pullback article I touched upon the fragmented nature of the convenience store industry and how ATD is rapidly expanding its presence on a global basis.

If you are interested in reading about people who have succeeded in the business world you may enjoy reading How Alain Bouchard built the Couche-Tard & Circle K convenience store empire. As I read the book I couldn’t help but think I may have unknowingly very briefly crossed paths with him when I frequented Perrette stores in the Montreal area when I was in my teens. I wonder if Bouchard ever envisioned heading up a company which is now the largest company on the basis of revenue of any Canadian based company ($51.4B Total Revenue in FY2018)!

In my March 22nd article I indicated that I viewed the pullback in the ATD’s share price as presenting an opportunity to acquire shares in a well run company at a reasonable valuation. On the basis of my analysis I acquired additional non-voting class B shares for the FFJ Portfolio bringing the total number of shares held to 553.

The shares pulled back a bit further subsequent to my article which presented investors with an even better opportunity to acquire reasonably valued shares in this high quality company.

At the close of business on July 9th, ATD released its Q4 and FY2018 results. On July 10th it held its analyst call to review its performance and the stock price popped thus prompting this review to determine whether ATD is still attractively valued for investors willing to initiate / increase their position in the company.

Business Overview

ATD is currently the leader in the Canadian convenience store industry and it is the largest independent convenience store operator in terms of the number of company-operated stores in the US. In Europe, it is a leader in convenience store and road transportation fuel retail in the Scandinavian countries (Norway, Sweden and Denmark), in the Baltic countries (Estonia, Latvia, and Lithuania), as well as in Ireland and it also has an important presence in Poland and has recently expanded into Russia.

As at April 29, 2018 (fiscal year end), ATD’s network comprised 10,015 convenience stores throughout North America, including 8,705 stores with road transportation fuel dispensing. The North American network consists of 19 business units, including 15 in the United States covering 48 states and 4 in Canada covering all 10 provinces.

Approximately 105,000 people are employed throughout the ATD network and at service offices in North America. In addition, through CrossAmerica Partners LP, ATD supplies road transportation fuel under various brands to approximately 1,300 locations in the United States.

In Europe, ATD operates a broad retail network across Scandinavia, Ireland, Poland, the Baltics and Russia through ten business units. As of April 29, the network comprised 2,725 stores, the majority of which offer road transportation fuel and convenience products while the others are unmanned automated fuel stations which only offer road transportation fuel. ATD offers other products, including stationary energy, marine fuel and aviation fuel. Including employees at branded franchise stores, ~25,000 people work in the retail network, terminals and service offices across Europe.

Under licensing agreements, more than 2,000 stores are operated under the Circle K banner in 14 other countries and territories (China, Costa Rica, Egypt, Guam, Honduras, Hong Kong, Indonesia, Macau, Malaysia, Mexico, the Philippines, Saudi Arabia, the United Arab Emirates and Vietnam), which brings the worldwide total network to more than 16,000 stores.

The following table sets out the number of stores in operation by geographic location and type of store as of April 29, 2018.

")

")

Source: ATD – Annual Information Form for FY2018

Q4 and FY2018 Results

ATD’s Q4 and FY2018 results can be found here and here.

Based on merchandise and service revenue information, ATD estimates FY2017 and FY2018 revenue for traditional convenience store items such as tobacco products, fresh food and foodservice, beer/wine/liquor, frozen beverages, candy and snacks, coffee, and dairy products and also for the following services featured in many of its stores (car wash, automatic teller machines, lottery ticket sales, cell phones, prepaid phone cards and financial services) amounted to:

Source: ATD – Annual Information Form for FY2018

Revenue derived from the road transportation fuel operations for FY2018 and FY2017 amounted to $37.1B and $ 26.1B, respectively. Road transportation fuel is sold at 8,914 company-operated stores, which represent 91% of total company-operated stores.

Road transportation fuel sales represented about 70% of ATD’s total revenues in Canada compared to ~72% of revenues in the U.S. and 74% in Europe. Road transportation fuel gross profits, however, represented only ~ 42% of overall gross profits.

ATD sells road transportation fuel either under its own brands (Couche-Tard® and Mac’s® in Canada and Circle K® in the United States) or under the name of major oil companies such as Esso, Shell, Mobil, Exxon, BP, Irving and Phillips 66.

In Europe, ATD’s retail sales of road transportation fuel are mainly generated through two different categories of sites: (i) full-service sites and (ii) automated fuel sites. Non-retail sales of transportation fuel are normally generated in bulk to customers with their own storage facilities. Sales in Europe are under the Circle K®, Ingo®, Topaz®, Shell and Esso brands.

ATD also has a global non-retail fuel business and it also has a Stationary Energy and Marine Fuel in Scandinavia and Ireland and an Aviation Fuel business in Ireland.

Credit Ratings

Moody’s and S&P Global continue to rate ATD’s long-term debt Baa2 and BBB, respectively. Both ratings are the middle tier of the lower medium grade ratings tier. One study by Moody’s claimed that over a “5-year time horizon” bonds to which is assigned a Baa2 had a “cumulative default rate” of ~2%.

Moody’s rating of ATD’s long-term debt is the 9th highest of 21 ratings. The Baa rating is considered to be medium-grade and is subject to moderate credit risk and as such may possess certain speculative characteristics

The S&P BBB rating is the 9th highest of 22 ratings. It indicates ATD has adequate capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

These ratings have been stable for several years and I am comfortable with the credit risk I have assumed through my investment in the company.

Valuation

Fiscal diluted net EPS (in USD) was (2018: $2.95, 2017: $2.12 and 2016: $2.09) with fiscal adjusted diluted net EPS (2018: $2.60, 2017: $2.21 and 2016: $2.08). Consensus estimates call for FY2019 adjusted diluted net EPS of ~$3.05.

ATD is currently trading at CDN ~ $60.80 or USD $46.41 which results in a PE ratio based on diluted net EPS of ~15.7 ($46.41 / $2.95) or a PE ratio based on adjusted diluted net EPS of ~17.85 ($46.41 / $2.60). ATD’s forward PE based on consensus estimates is ~15.2 ($46.41 / $3.05).

I view these valuation levels as reasonable given ATD’s growth potential.

Dividend, Dividend Yield and Dividend Payout Ratio

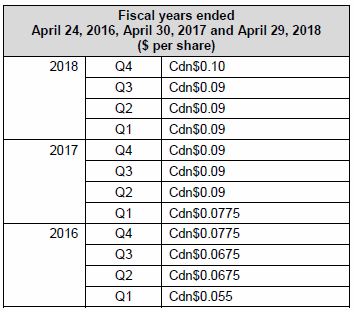

The following table reflects the dividends ATD has declared to all holders of Multiple Voting Shares and Subordinate Voting Shares for the three most recent fiscal years.

On July 9th, ATD announced a quarterly increase of CDN $0.01 in its quarterly dividend representing an 11.1% growth from its $0.09/quarter dividend. The CDN $0.40 annual dividend provides investors with a 0.066% dividend yield based on the current CDN ~$60.80 stock price.

If we convert the projected adjusted earnings of USD $3.05 to CDN using a conversion rate of 1.31, we arrive at projected adjusted earnings of ~$4. The $0.40 annual dividend is a very conservative 10% payout ratio based on adjusted earnings estimates.

Given ATB’s opportunity for growth and success to date with its growth strategy I do not envision any significant increase in the annual dividend in the foreseeable future. I suspect management will continue to stick with its strategy of reinvesting earnings to grow the business with the growth in the dividend being of secondary importance.

Final Thoughts

As I indicated in my March 22nd article, I am impressed with:

- management’s philosophy and level of discipline;

- the company’s ability to acquire companies and to consistently generate synergies that result in cost reductions which exceed projections;

- the ability to deleverage relatively quickly;

- the strong record of FCF generation.

I am confident we can expect to see top line growth that will outpace higher costs brought about by higher wage inflation (ie. regulated minimum wage increases).

I think ATD will focus on reducing its adjusted leverage ratio from 3.13:1 as at FYE2018 and will continue to make bolt-on acquisitions versus making a large transformational acquisition. Another major acquisition such as the CST Brands and Holiday Stationstores acquisitions is more likely to occur after FY2019 by which time ATD’s leverage ratio should have evidenced a reduction to well below the 3:1 level.

I would acquire additional shares at current prices but am satisfied with my current exposure of 553 shares, and therefore, do not intend to acquire any additional shares at this juncture.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: Long ATD.b

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.