Summary

Summary

- This company has increased its dividend for 35 consecutive years.

- An investor who acquired 100 shares for $1,110 when the company was founded in 1955 and never sold them you would now have 375,960 shares.

- The company’s total return to shareholders over the 10 year period ending December 31, 2017, including reinvested dividends, was 80.2%.

- The company is currently under investigation by the SEC but an independent investigation undertaken at the behest of the Board of Directors and completed in September 2017 found no evidence of wrongdoing.

- The company is currently undervalued and the pullback in the stock price in 2018 is less pronounced than that of its peers.

Introduction

I recently wrote about a great company which has rewarded long-term shareholders but which currently appears to be somewhat overvalued. In today’s article I cover a company which has rewarded long-term shareholders (it was founded in 1955 but was listed on the NYSE on June 14, 1974), is experiencing some headwinds, and is undervalued which could lead to reasonable returns for patient investors.

In my opinion, the company has been undervalued for the last several years and valuation levels were slowly trending upward toward historical levels. A few months ago, however, allegations were made by a small number of employees that the company had been misleading about the company’s sales and revenue. These employees accused the company of inflating a sales metric and of changing its timeline for recording revenue to improve its earnings reports.

The Securities and Exchange Commission (SEC) is currently investigating but an investigation by external lawyers hired by a special litigation committee constructed by the company’s board found no evidence of wrongdoing; a link to the ‘Report of the Special Litigation Committee of the Board of Directors’ for this company is provided in the full version of this article which is accessible to subscribers of this site.

Should the SEC find no wrongdoing, an inquiry is still expensive and the magnitude of the expense depends on what the SEC investigates.

As a result of the ongoing investigation, the company’s shares have traded in a fairly tight range for the last several months. As I compose the article, the company is trading at the low end of this range.

Sometimes attractive investment returns can be generated when negative news has resulted in a company being out of favor with many investors. In addition, this company’s peers have experienced a significant pullback in their stock price since the beginning of 2018; this company’s pullback is less extreme than its peers.

Another point I want to make is that the company reviewed in this article operates in an industry where the stock price is unlikely to be ‘knocked out of the park’. When creating a portfolio, however, I don’t think it is prudent to load up exclusively on companies in which you think they will consistently generate outsized returns. My reasoning for this comes down to the fundamental law of supply and demand. If everyone thinks a company will consistently generate outsized returns and they flock to a particular stock, the stock price will be driven up to the point where the value of the company becomes disconnected from the underlying fundamentals.

In my opinion, it is far better to create a well balanced portfolio consisting of companies within the 5 main economic sectors – Manufacturing & Industry; Resources & Commodities; Consumer; Finance; and Utilities.

If you create a balanced portfolio, several of your holdings will end up being ‘singles’. You will likely also end up with some holdings that may eventually become ‘doubles’ and, to a lesser extent, ‘triples’ and ‘home runs’. There is nothing wrong with a portfolio of companies that are spread over these classifications.

The company being analyzed in this article has managed to make disciplined long-term investors a lot of money. It has:

- Relatively strong credit ratings (upper medium grade) so you don’t have to worry about waking up one morning to read that the company has filed for bankruptcy protection;

- Increased its dividend for 35 consecutive years;

- Rewarded investors with numerous stock dividends and stock splits. Had you acquired 100 shares for $1,110 when the company was founded in 1955 and never sold them you would now have…..375,960 shares. NOTE: The company became a holding company and was listed on the NYSE on June 14, 1974 by which time those 100 shares had become 3140 shares.

Should the company in question appeal to you but you are reluctant to invest in it until such time as the SEC investigation is closed, there are various option strategies you may wish to employ; I present one ‘plain vanilla’ option strategy in this article.

Business Overview

Aflac Incorporated (NYSE: AFL) historical timeline can be found here.

The following are recent high level investor facts.

Source: AFL – 2017 Annual Report

AFL is a general business holding company which acts as a management company, overseeing the operations of its subsidiaries by providing management services and making capital available.

Its principal business is voluntary supplemental and life insurance, which is marketed and administered through its subsidiary, American Family Life Assurance Company of Columbus (Aflac), which operates in the United States (Aflac U.S.) and as a branch in Japan (Aflac Japan).

Most of AFL’s policies are individually underwritten and marketed through independent agents. Aflac U.S. markets and administers group products through Continental American Insurance Company (CAIC), branded as Aflac Group Insurance. The insurance operations in the U.S. and its subsidiary in Japan service the two markets for the insurance business.

The voluntary insurance policies offered in Japan and the U.S. provide a layer of financial protection against income and asset loss. In Japan it sells voluntary supplemental insurance products, including cancer plans, general medical indemnity plans, medical/sickness riders, care plans, living benefit life plans, ordinary life insurance plans and annuities. In the U.S. it conducts insurance business in all 50 states, the District of Columbia, and several U.S. territories where it sells voluntary supplemental insurance products including products designed to protect individuals from depletion of assets (accident, cancer, critical illness/care, hospital indemnity, fixed-benefit dental, and vision care plans) and loss-of-income products (life and short-term disability plans).

In FY 2017, the Japanese operations accounted for 70% of AFL’s total revenues versus 71% and 70% in FY 2016 and FY 2015, respectively. The percentage of AFL’s FY2017 total assets that were attributable to AFL Japan was 83% at both FYE 2016 and 2017.

The following tables provide a high level overview of the magnitude of the business conducted in Japan and the U.S..

Source: AFL – 2017 Annual Report

Source: AFL – 2017 Annual Report

Recent News

Additional details surrounding the allegations made against AFL can be found here, here, and this lengthy article.

The company’s January 2018 response to the allegations can be found in this Press Release.

In addition, there is a September 2017 ‘Report of the Special Litigation Committee of the Board of Directors of Aflac Incorporated’ which can be found here. Based on the findings of the Special Committee I am reasonably confident AFL will prevail in this legal matter.

Historical Shareholder Returns

AFL has outperformed the S&P500 over the long-term but has underperformed the index over the last several years.

Source: AFL – 2017 Annual Report

Given the conservative nature of this company and the industry in general, I was not expecting AFL to outperform the S&P500 where the largest 10 companies by market cap are currently Apple, Microsoft, Amazon, Facebook, Berkshire Hathaway, JP Morgan, Alphabet, Exxon Mobil, and Johnson & Johnson. Most of these 10 largest companies have been on a tear in recent years and together they make up over 21% of the S&P500 index. AFL, meanwhile is the 181st largest company in the S&P500 and its weighting is only ~0.14%.

Prior to analyzing AFL and comparing it with other members of the Life Insurance and Accident & Health Insurance industry within the Financial sector, I had no idea how its historical performance would have fared against its largest publicly traded U.S. listed competitors. Looking at the recent AFL stock chart and those of its largest U.S. peers I see that all stock prices have taken a hit in recent months.

Source: Finviz

Despite AFL’s current challenges, it is very difficult to overlook the following total returns.

Source: AFL – Investor Facts

I encourage you to check out AFL’s website where you can plug in various initial investment dates to determine the total investment return you would have achieved had you initiated a position based on your selected date(s). Here are the results I generated on the basis of $10,000 having been invested 10 and 20 years ago and with all dividends reinvested.

Source: AFL Investment Calculator

Q1 2018 Results and 2018 Guidance

AFL is scheduled to release its Q2 2018 results within 2 weeks (on July 26, 2018), and therefore, I will dispense with any comments regarding Q1 results. In the interim I provide a link to AFL’s Q1 earnings release and 2018 guidance.

As you can see, AFL still intends to continue to reward its shareholders regardless of the accusations levied against it.

Source: AFL – 2018 Morgan Stanley Financials Conference June 12, 2018

Credit Ratings

AFL’s credit ratings can be found here. The Issuer Credit Ratings are the lowest tier of the upper medium grade investment grade category. These ratings are acceptable and give me comfort that an investment in AFL would not be speculative in nature.

Valuation

In FY2017, AFL generated $3.405 in operating earnings per diluted share. The low, high, and closing stock prices in FY2017 were $44.91, $33.25, and $44.12 respectively. On the basis of the closing stock price for FY2017, AFL was trading at a ~12.96 adjusted PE.

Using management’s projected FY2018 adjusted diluted EPS of $3.72 – $3.88 and the July 13, 2018 $42.60 closing stock price we get an adjusted diluted PE ratio of ~10.98 – ~11.45 (~11.22 using the mid-point).

AFL’s PE in 2008 – 2017 was 17.5, 14.5, 11.4, 11, 8.7, 10.2, 9.6, 10.5, 11, 12.8 with the most recent 5 year PE being ~10.82.

In my opinion, AFL has been attractively valued for a few years and the current valuation is still attractive.

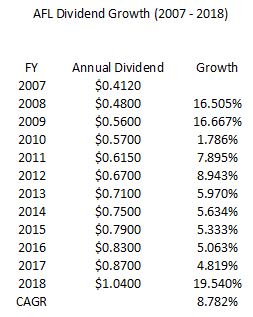

Dividend, Dividend Yield, Dividend Growth Rate, and Dividend Payout Ratio

AFL’s dividend history can be found here and its stock dividend split history can be found here.

The current $1.04 annual dividend offers a 2.44% yield on the basis of the $42.60 closing stock price on July 13, 2018.

AFL’s dividend compound annual growth rate is ~8.8% over 2007 – 2018.

On January 31, 2018, AFL significantly increased its quarterly dividend. This was partially attributed to the benefits AFL derived from the U.S. tax reforms enacted in December 2017. I do not envision dividend increases of the magnitude evidenced in 2017 going forward. I think you should temper your expectation for dividend increases from AFL and factor annual dividend increases between 5% – 8% into your investment decision making process.

On the basis of $3.405 in operating earnings per diluted share and a $0.87 annual dividend in FY2017, the dividend payout ratio was ~25.6%. Using management’s projected FY2018 adjusted diluted EPS of $3.72 – $3.88 ($3.80 mid-point), the new $1.04 annual dividend represents a ~27.4% dividend payout. This dividend payout ratio range gives me comfort that AFL’s dividend is sustainable.

Option Strategy – Sell PUT

If you are interested in investing in AFL you can certainly acquire a partial position, versus a full position, until such time as the SEC releases the findings of its investigation. Alternatively, you could employ various option strategies for which I provide the following possible strategy.

Sell a November 2018 PUT with a $40.00 strike price; I have selected a November 2018 expiry because I think this allows sufficient time for the SEC to render its decision before this option expiry date. You would collect ~$0.91/share so your breakeven cost would be reduced from $40/share to $39.10/share.

Keep in mind that by selling a PUT, your broker needs to ensure sufficient funds are on hand in the event the buyer of the PUT exercises their option and you have to purchase AFL shares. This means that you would most likely have to have funds or margin availability of $20,000 if you wrote 5 contracts.

If AFL exceeds the $40 strike price at expiry, nobody will sell their shares to you for $40 so you would end up with no AFL shares but you would have at least collected the option premium. If AFL closes below the $40 strike price at expiry you will end up with AFL shares being put to you at $40…even if AFL is trading at less than $40/share. Keep in mind that if AFL were to plunge to $25/share before expiry, for example, it is possible the buyer of a $40 PUT could exercise their option before expiry.

Options are a wonderful tool if you know how to use them. They can, however, be weapons of financial destruction if you don’t know what you’re doing. I do not profess to be an options expert, and therefore, any options I use are of the ‘plain vanilla’ variety.

Final Thoughts

I do not disagree there is short-term risk with AFL given that there is an ongoing SEC investigation. I suspect, however, that SEC’s findings will not lead to significant penalties and AFL’s shares will jump in value once the legal issue is out of the way. If anything, I think the allegations will either prove to be unfounded or at worst, the SEC will order the company to pay a fine that will pale in comparison to the company’s annual profit.

Interestingly, AFL’s stock price appears to have taken less of a hit in recent months than many of its peers. This would suggest to me that the investment community has placed a higher probability that AFL will be absolved of any wrongdoing as opposed to being found to have perpetrated any fraud for the purpose of misleading investors.

When I see AFL’s current attractive valuation I am reminded of Warren Buffett’s profound words of wisdom ‘Price is what you pay. Value is what you get’. In the case of AFL you might have to be prepared to wait before you notice a significant appreciation in the value of your investment. If history is any indication of what lies in store for the future, however, I think long-term AFL investors will be aptly rewarded.

It certainly is hard to imagine how a company which has generated the returns it has generated since going public in 1973 will suddenly fail its shareholders. The company is growing and is conservatively managed. This is far more than can be said about many other companies in which you can invest.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I do not currently hold a position in AFL but I intend to initiate a position within the next 72 hours.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.