Summary

Summary

- This MasterCard (NYSE: MA) stock analysis is based on Q4 and FY 2016 results reported January 31, 2017.

- MA continues to perform well but lofty expectations resulted in a small pullback in the stock price.

- While MA’s PE is just shy of 30, I am willing to pay up for high growth and will acquire additional shares.

- Should MA’s stock price experience a significant correction at a later date (not due to the deterioration of the business), I would buy more shares to lower my average cost.

Introduction

I recently reviewed Visa Inc. (NYSE:V) in my Visa – I Will Never Sell This Holding post. Secondly, on January 31, 2017, MasterCard Inc. (NYSE:MA) reported its Q1 2017 results. I thought, therefore, now would be an opportune time to review MA’s performance and to ascertain whether to increase our exposure to this name.

Before I go any further, some readers of my Visa post raised the issue of bitcoin and blockchain bringing V and MA to their knees. To avoid similar comments on this post, I encourage you to read my VISA – Will Bitcoin Or Blockchain Technology Displace It? post. While my comments were focused solely on what V is doing to address this risk, MA is not sitting idly waiting for new technology to disrupt its business. It is also looking into how it can use this technology to grow its business.

Business Overview

For those of us old enough to remember, MasterCard was once called Master Charge. Did you know, however, that the company’s history goes back even further than 1969 when the interlocking circles trademark became synonymous with the Master Charge name?

MA has clearly evolved over the past 50 years and today it is essentially a technology company in the global payments industry. It operates a global payments processing network which connects consumers, financial institutions, merchants, governments and businesses in more than 210 countries and territories. It also deals in 150 currencies, meaning a strong US dollar constrains revenue and earnings growth.

Next to V, MA is the second largest global payment solutions company. It manages a family of payment card brands, including MasterCard, Maestro and Cirrus, which it licenses to its customers. It also provides a variety of services in support of the credit, debit and related payment programs of about 22,000 financial institutions and other types of entities.

MA’s strategy to drive profitable growth is reflected below and was obtained from the September 7, 2016 Investment Community Meeting presentation.

MasterCard – Strategy to Drive Profitable Growth

MA’s business model is three-tiered:

- Franchisor – develops and markets payment solutions.

- Processor – processes payment transactions.

- Adviser – provides consulting services to customers and merchants.

Revenue is generated from fees (domestic assessments, cross-border volume fees, transaction processing fees, and other service fees).

As with V, MA follows a “four-party” payment system, which typically involves:

- The cardholder

- The merchant

- The issuer (the cardholder’s bank) – typically pays operation fees and assessments

- The acquirer (the merchant’s bank) – principally pays assessments on gross dollar volume of cards and, to a lesser extent, certain operation fees

In addition, it charges operation fees to its customers for providing transaction processing and other payment-related services. These include core authorization, clearing and settlement fees, cross-border and currency conversion fees, switch fees, connectivity fees, acceptance development fees, warning bulletins, holograms, fees for compliance programs, and user-pay fees for a variety of transaction enhancement services.

Q4 and FY2016 Financial Results

Full details can be found in MA’s January 31, 2017 earnings release. Highlights are provided below.

Q4 Results

MA reported:

- Net income of $0.933B, including a special item, or $0.86 per diluted share.

- Net income of $0.940B, excluding a special item, or $0.86 per diluted share.

- Gross dollar volume up 9% and purchase volume up 8%, both adjusting for the impact of recent EU regulatory changes.

- Net revenue of $2.76B, an increase of 9%, or 10% on a currency-neutral basis, vs. same period in 2015.

- An increase in switched transactions of 17%, to $15.2B. A 9% increase in gross dollar volume, on a local currency basis and adjusting for the impact of recent EU regulatory changes, to $1.2T.

- An increase in cross-border volumes of 13%.

- MA repurchased approximately 11 million shares at a cost of $1.1B. Between December 31, 2016 and January 26, 2017, MA repurchased an additional 2.3 million shares at a cost of $0.247B.

MA is renaming “processed transactions” to “switched transactions.” The methodology for calculating this metric has not changed and reflects the transaction counts that MA has authorized, cleared or settled.

FY2016 Consolidated Results

- Net income of $4.1B, an increase of 7%, or 8% on a currency-neutral basis, and diluted EPS of $3.69, up 10%, or 11% on a currency-neutral basis, vs. 2015.

- Net income, excluding special items, of $4.1B, up 6%, or 7% on a currency-neutral basis and diluted EPS of $3.77, up 10%, or 11% on a currency-neutral basis, vs. 2015.

- Net revenue of $10.8B, an increase of 11%, or 13% on a currency-neutral basis, vs. 2015.

- Operating income of $5.8B, an increase of 13%, or 15% on a currency-neutral basis, vs. 2015.

- Operating income, excluding special items, of $5.9B, an increase of 13%, or 14% on a currency-neutral basis, vs. 2015.

- Operating margin of 53.5%, or 54.5% excluding special items.

Strong FCF continues to be generated which will support share repurchases. $4.7B remains to be repurchased under current repurchase program authorizations.

MA recently announced a $0.03 increase in its quarterly dividend from $0.19 to $0.22 effective with the February 9, 2017 payment date.

Outlook for Fiscal 2017

In the January 31, 2017 conference call, MA indicated that revenue growth in the first half of 2017 is likely to be lower than in the second half due to higher incentives.

The strong US dollar, already near a 14-year high against the euro, is expected to negatively impact revenue growth by about 2% and net earnings by about 3%. MA expects further appreciation if the U.S. economy picks up speed and inflation rises under the Trump administration.

Low double-digit percentage revenue growth and EPS growth in the mid-teens is expected.

Full-year operating expenses are expected to increase by a high single-digit percentage on a currency-neutral basis.

Valuation

MA’s shares are never inexpensive and its current PE is just under 29.50 (current price as I compose this post is roughly $106.33). Personally, this is far greater than I like, but if I had waited for MA to have a sub 20 PE, I would still be sitting on the sidelines.

Even though the dividend has been increased to $0.88 for FY2017, the dividend yield is sub 1%. Clearly, the dividend yield on MA will not be the primary metric that will sway your decision to buy the stock.

Given the high growth nature of the business, I am prepared to pay up to acquire MA shares. Should a major market correction occur that sends MA’s stock price spiraling downward, I would just acquire more shares to lower my average cost.

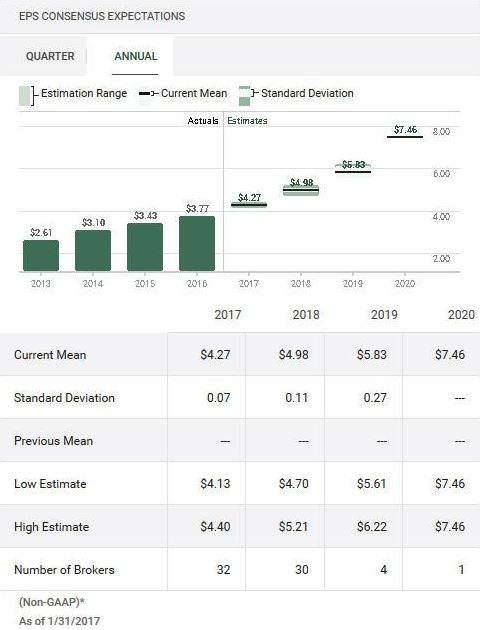

If I use the current mean 2017 EPS estimate of $4.27 which is based on input from 32 brokers and the current PE of 29.50 (approx.), I get a stock price of almost $126; the current price compares favorably with this figure.

Source: TD Bank WebBroker – MA EPS Concensus Expectations

MasterCard Stock Analysis – Final Thoughts

I recognize some readers may view MA as being too rich and would prefer that some major market correction occur before pulling the trigger. No problem. That is your prerogative.

I also recognize that MA’s minuscule dividend yield (sub 1%) will turn off other investors. For those readers, I encourage you to read my Low or No Dividend Yield Companies Belong in Your Portfolio post.

Despite MA’s lofty valuation, I intend to acquire more shares within the next 72 hours.

I will most likely do this through one, or more, of our Tax Free Savings Accounts (TFSA) versus our FFJ Portfolio. While I will get hit with a 15% withholding tax on all MA dividends, the dividend is not what is driving this additional purchase. The purchase of MA is primarily for the anticipated future capital gains. By holding MA in TFSA accounts, I will incur no capital gains tax should we ever sell at a later date. (NOTE: A sale at a later date is doubtful as we intend to pass on these shares to the next generation. I, however, like to keep my options open).

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long MA, V.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.