![]()

In my December 15, 2025 post I disclose initiating a 300 share position in Thomson Reuters (TRI) in one of the ‘Core’ accounts in the FFJ Portfolio. On January 20, 2026, I acquired an additional 200 shares in the same account.

When I reviewed TRI in this February 6, 2026 post, the most current financial information was for Q4 and FY2025. This is an opportune time to revisit this existing holding given the May 5, 2026 release of Q1 results.

NOTE: TRI is a Canadian company that reports in USD. Shares are listed on the New York Stock Exchange (NYSE) and the Toronto Stock Exchange (TSX) in Canada. I own the US shares.

Industry Overview

I provide a very high level industry overview in my December 15, 2025 post.

Business Overview

A good overview of the company is found:

- in Part 1 Item 1 in the FY2025 Form 40-F accessible through the SEC Filings section of the company’s website; and

- the company’s website.

I also recommend reviewing TRI’s 2024 Investor Day presentation.

NOTE: TRI changed the names of its Tax & Accounting Professionals segment to Tax, Audit & Accounting Professionals and its Reuters News segment to Reuters to reflect the broader scope of the activities in each of the respective segments. These name changes did not change the segments’ composition or the measurement of the segments’ results as previously or currently reported.

Current Negative Sentiment Presents A Buying Opportunity

TRI’s share price weakness appears to be primarily driven by investors who fear that large language models will commoditize professional expertise and bypass expensive research platforms. I think artificial intelligence (AI) will actually accelerate TRI’s competitive advantages. Given this, I think the current negative sentiment presents a significant buying opportunity.

Widening Data Moat

Judges have increasingly admonished, sanctioned, and fined lawyers for using artificial intelligence (such as ChatGPT) to generate legal submissions containing fabricated ‘hallucinated’ cases and quotations. These incidents have occurred in Canada and the US (2024-2026), with courts emphasizing that lawyers have a professional duty to verify the accuracy of their filings.

The following are examples in which Judicial Reprimands have been handed down because of the use of standard AI tools.

- Canada (B.C. Supreme Court, 2024): Justice David Masuhara reprimanded Vancouver lawyer Chong Ke for including two fake cases generated by ChatGPT in a high-conflict family dispute, ordering her to pay the opposing party’s costs. The judge noted that generative AI is ‘no substitute for the professional expertise’ of lawyers.

- Canada (Ontario Superior Court, 2025): Judge Fred Myers ordered Toronto lawyer Jisuh Lee to appear for a show cause hearing to explain why she should not be cited for contempt in the face of the court after she submitted a document containing non-existent case citations, which the judge suspected were ‘possibly AI hallucinations’.

- USA (New York, 2023): Judge P. Kevin Castel sanctioned lawyers Steven Schwartz and Peter LoDuca after they filed a brief written by ChatGPT containing fake court opinions, highlighting that ‘a lawyer’s ethical duty to ensure the accuracy of their filings’ was breached.

- USA (Alabama, 2025): Federal judge Terry Moore fined a lawyer $5,000 for submitting AI-generated false citations to court and ordered him to report the sanctions to all other courts where he practices.

- USA (Maine, 2026): Judge Stacey D. Neumann ordered attorney Kelly Guagenty to attend continuing legal education (CLE) on AI, following the submission of unverified AI-generated citations.

Just recently, Magistrate Judge Peter H. Kang of the US District Court for the Northern District of California sanctioned Lenden Webb who practices in Fresno, California primarily for failing in his professional responsibility to sufficiently supervise another lawyer at his firm who submitted court filings that contained AI-fabricated citations A California attorney failed, a federal judge ruled.

Justice Kang ordered Webb to pay $1,001 as a personal sanction, and to circulate the order to all attorneys and paralegals in Webb’s firm. Webb also must complete four hours of continuing legal education from the State Bar of California, including two hours on supervision of junior attorneys/staff, and at least another two in the area of “ethical/professional use” of AI in legal practice.

Lenden Webb, however, is merely the latest in a fast-growing string of lawyers to be fined over misusing AI through court filings with fabricated citations.

We see from these examples that standard AI tools do not replace expertise. AI must be used in conjunction with accurate data which is why TRI’s ‘Data Moat’ is widening.

Investors often mistake general-purpose AI (like standard ChatGPT) for professional-grade AI. In the legal and tax sectors, AI is only as valuable as the authoritative data it can access.

TRI’s proprietary content is viewed as the ‘gold standard’ datasets (Westlaw, Practical Law, and Checkpoint). General AI models are unlikely to be of any benefit when dealing with niche case law or complex tax codes.

TRI’s CoCounsel platform combines generative AI with these verified datasets, ensuring professional-grade accuracy that generic competitors cannot replicate.

As the risk of AI hallucinations becomes a liability for law firms, the value of TRI’s 1,500 attorney-editors, who manually verify and tag content, increases. They provide what is necessary for AI to function safely.

Evolution Into A Workflow Automation Company

The market appears to currently be pricing TRI as a potentially replaceable search engine. TRI, however, is evolving into a workflow automation company.

- TRI’s 2026 AI in Professional Services Report shows that organization-wide AI usage in professional services doubled to 40% this year.

- TRI is not just selling data anymore. It is selling time. Its agentic AI tools can now reason, plan, and execute multi-step tasks (like drafting a complex legal brief or an audit report). This shifts their value proposition from a ‘per-user license’ to a ‘value-delivered’ model, allowing for significant margin expansion.

TRI’s Financial Strength vs. Valuation Gap

Despite a drop in TRI’s share price, the company’s underlying fundamentals are strong.

- In Q1 2026, TRI beat its own guidance and reported 9% organic growth in its core segments (Legal, Corporate, Tax & Accounting).

- The company has ~$10B in acquisition capacity through 2027. It is aggressively buying AI startups such as the January 2025 acquisition of SafeSend for ~$0.6B to consolidate the market while valuations are depressed.

- TRI employs share consolidations to return capital to its shareholders. By reducing the share count while AI-driven margins expand, EPS should experience a significant melt-up once sentiment normalizes.

The Sentiment Buying Opportunity

The current issue with TRI does not appear to be with its financial results but rather with its share price behavior.

While history is not indicative of future performance it can, however, serve as a guide. When investors feared the internet would kill traditional professional publishing in the late 1990s, TRI pivoted and became more profitable by digitizing. This AI pivot is the same playbook, but with higher stakes and faster execution.

Financials

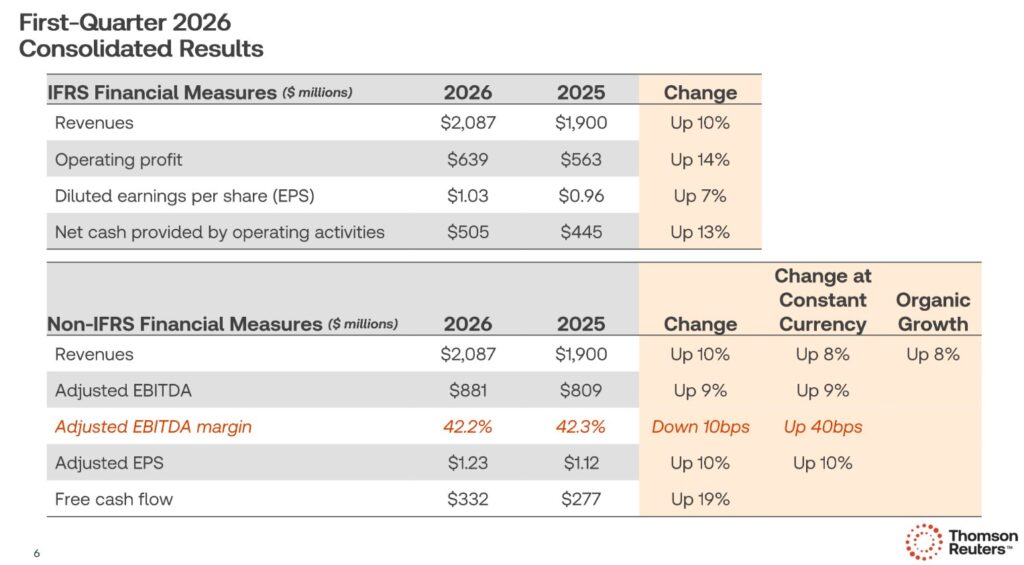

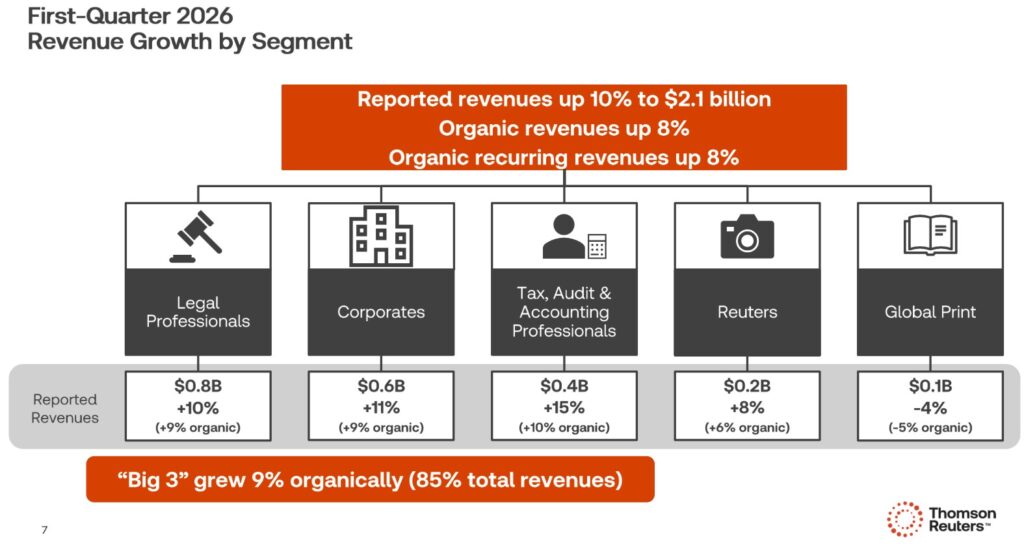

Q1 2026 Results

I strongly recommend reading the Form 6-K issued on May 6, 2026 that is accessible through the SEC Filings section of the company’s website. Further material is accessible through the Quarterly Results section of the company’s website.

The following, extracted from the Q1 2026 earnings presentation, provide a snapshot of TRI’s performance in Q1 2026.

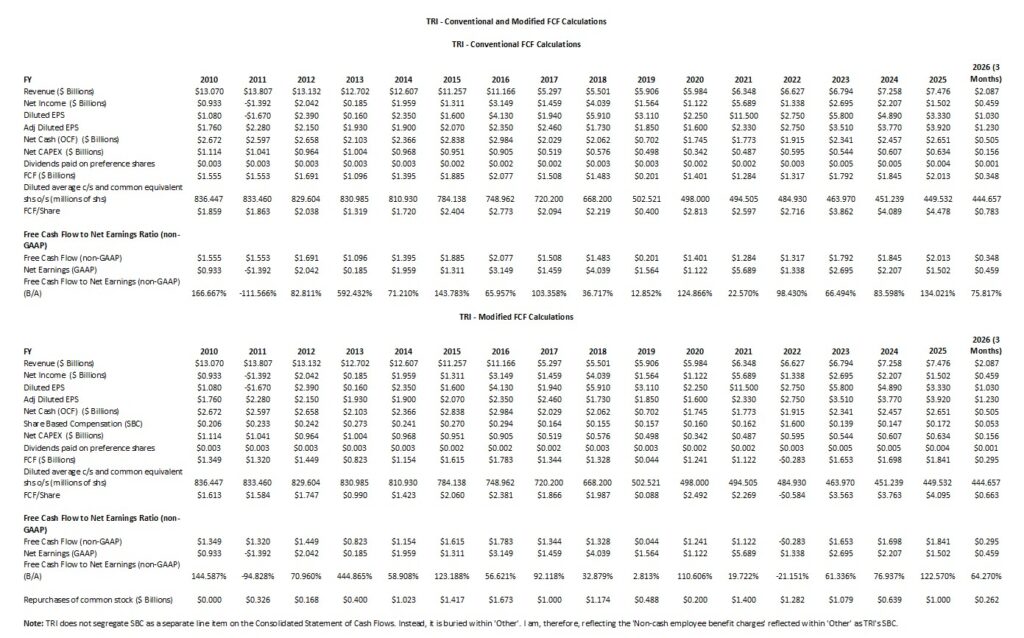

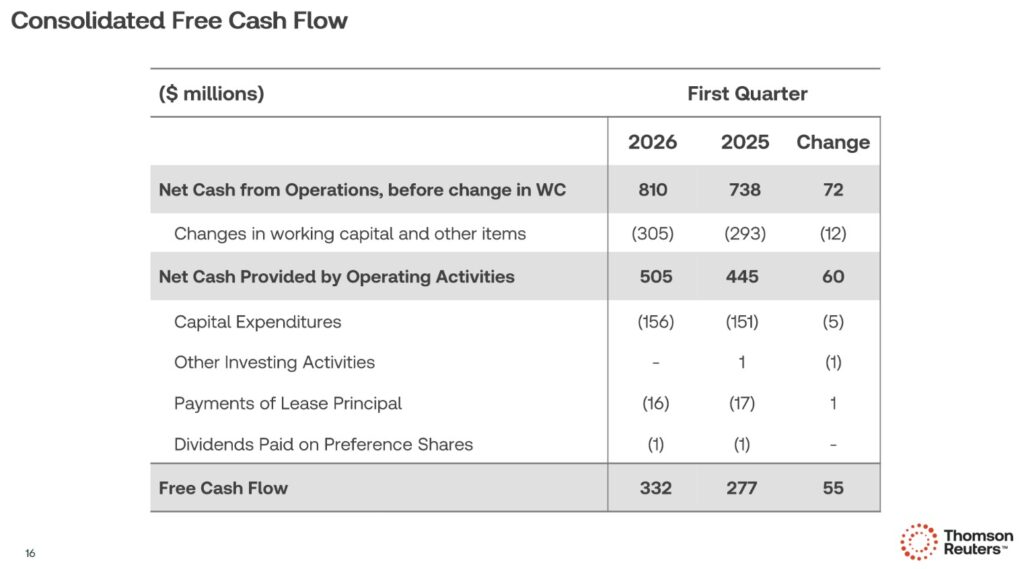

Operating Cash Flow (OCF), Free Cash Flow (FCF), and CAPEX

In prior posts I touch upon my rationale for deducting stock-based compensation (SBC) to calculate FCF. I, therefore, dispense with explaining this again.

The sale of the majority stake in the Financial & Risk (F&R) business (renamed Refinitiv) in 2018 resulted in a massive decline in TRI’s reported consolidated revenue. Prior to the sale, the F&R business was TRI’s largest division by revenue.

The sale reflected TRI’s strategic pivot to focus on high-growth, recurring-revenue businesses. The revenue reduction was not a complete loss of revenue from the F&R business because TRI retained a 45% equity stake in the new Refinitiv business and it entered into a 30-year agreement for Reuters News to supply news and editorial content to Refinitiv. This created a new revenue stream for the News segment.

TRI sold its remaining 45% stake in Refinitiv to the London Stock Exchange Group (LSEG) in an all-share transaction that closed in January 2021, further completing the strategic separation from the financial data business.

The following compares TRI’s FCF using the ‘conventional’ and ‘modified’ calculation methods.

TRI does not segregate SBC as a separate line item on the Consolidated Statement of Cash Flows but buries it within ‘Other’. I, therefore, reflect the ‘Non-cash employee benefit charges’ reflected within ‘Other’ as TRI’s SBC.

My FCF calculations differ slightly from those calculated by TRI. This is because TRI includes the ‘Other Investing Activities’ and ‘Payments of Lease Principal’ line items in its calculations. The values of these line items are relatively insignificant. They, therefore, have no meaningful impact on my analysis. My ‘modified’ FCF calculations, however, reflect lower FCF because the value of annual SBC is in excess of ‘Other Investing Activities’ and ‘Payments of Lease Principal’.

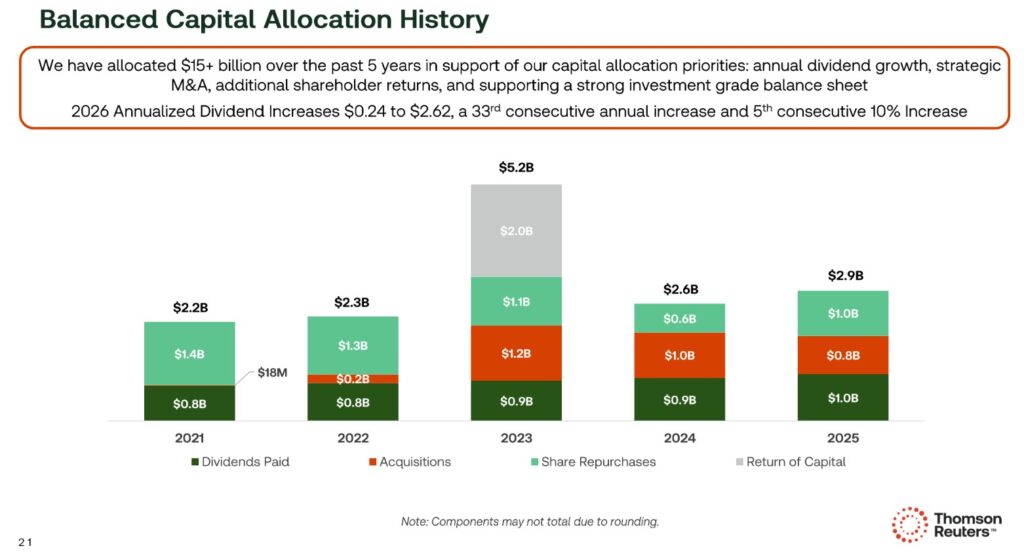

Capital Allocation

TRI has historically maintained a disciplined capital strategy that balances growth, long-term financial leverage, credit ratings, and returns to shareholders.

A key focus is to have the investment capacity to drive revenue growth, both organically and through acquisitions, while also maintaining long-term financial leverage and credit ratings and continuing to provide returns to shareholders. The firm’s principal sources of liquidity are cash and cash equivalents and cash provided by operating activities. From time to time, TRI will also issue commercial paper, issue debt securities and borrow under its credit facility. The principal uses of cash are for debt repayments, debt servicing costs, dividend payments, capital expenditures, share repurchases and acquisitions.

TRI’s capital strategy approach has provided it with a strong capital structure and liquidity position thus enabling it to pursue organic and inorganic opportunities in key growth segments to drive shareholder returns. Its disciplined approach and highly recurring cash generative business model have allowed it to weather economic volatility in recent years caused by macroeconomic and geopolitical factors, while continuing to invest in the business.

The company expects that the operating leverage of its business will increase FCF if revenues increase as contemplated by management’s outlook.

TRI’s maximum leverage ratio is 2.5x net debt to adjusted EBITDA and it continues to target:

- a payout of 50% – 60% of expected FCF as shareholder dividends;

- a return of at least 75% of annual FCF to shareholders in the form of dividends and share repurchases; and

- a return on invested capital (ROIC) that is double or more of the firm’s weighted-average cost of capital over time.

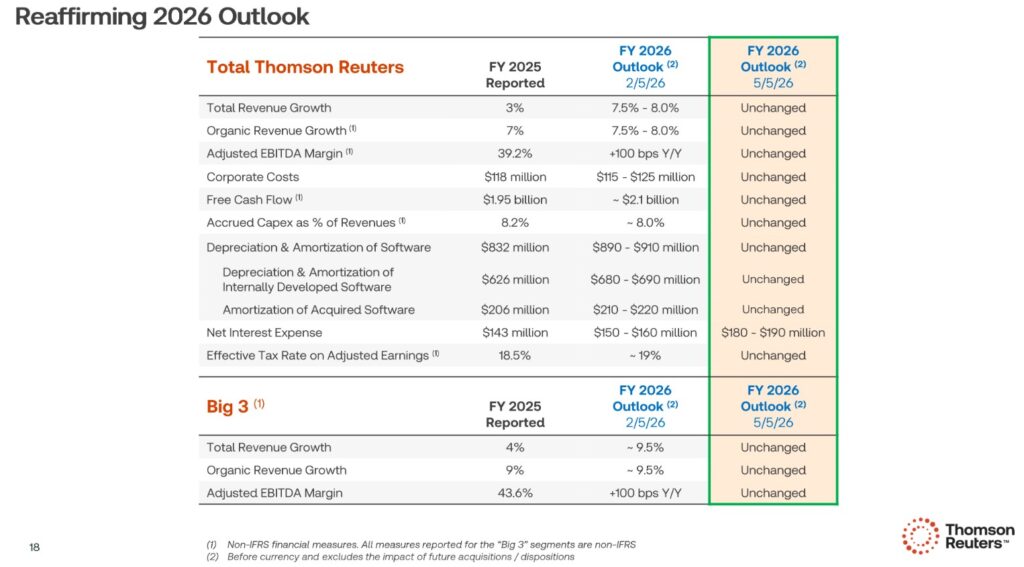

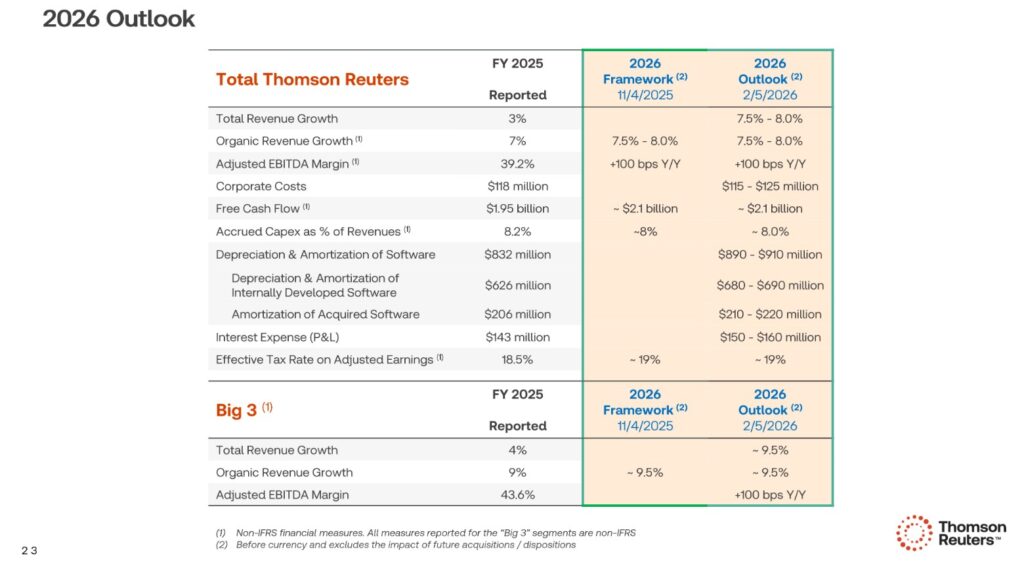

FY2026 Outlook

The following reflects TRI’s preliminary FY2026, current FY2026 outlook, and FY2025 results.

The following was provided with the release of Q4 and FY2025 results.

ROIC and WACC

Return on Invested Capital (ROIC) provides an indication of a company’s efficiency. In essence, is a company actually creating value or ‘burning’ cash for the sake of growth?

A company with a higher ROIC is mathematically worth more because it requires less reinvestment to achieve that growth.

A good indication of how well a company is performing is to compare ROIC to the Weighted Average Cost of Capital (WACC). TRI does not officially report the WACC metric. The company’s credit profile and market conditions, however, can help us roughly estimate it.

The generally accepted high-level formula used by Wall Street is:

ROIC = NOPAT/Average Invested Capital

with the Net Operating Profit After Tax (NOPAT) formula being Operating Income (EBIT) x (1-tax rate)

This shows how much profit the core business makes while ignoring how much debt the company has.

The Average Invested Capital is the total money tied up in the business.

- The Operating Approach formula is

- The Financing Approach is

One shortcoming with ROIC is that it is a non-GAAP metric meaning the input data plugged into the ROIC formula is inconsistent.

TRI has undergone a significant transformation between FY2020 and FY2025, and therefore, represents a significant transformation. The company evolved from a diversified holding company into a focused “Content-Led Technology” firm, which is reflected in the steady expansion of its ROIC.

TRI generally uses Adjusted ROIC (which it typically defines as Adjusted NOPAT divided by average invested capital).

The reasons for the dramatic rise in ROIC from ~8.4% in 2020 to ~18.4% in 2025 are:

- The launch in 2021 of an initiative focused on eliminating departmental silos and automating internal workflows. Management reports that this which significantly boosted operating margins.

- The sale of shares in the London Stock Exchange Group (LSEG). This removed a large, non-operating asset from TRI’s balance sheet, effectively lowering the ‘Invested Capital’ denominator while redeploying cash into higher-margin AI businesses.

- The shift from one-time ‘Print’ or ‘Desktop’ sales to high-margin, recurring cloud subscriptions (SaaS) improved the quality and predictability of TRI’s earnings.

TRI’s WACC was at its lowest in FY2020 – FY2021 due to near-zero interest rates and TRI’s massive cash position following the Refinitiv deal.

The WACC increased in FY2022 – FY2025 as central banks raised rates. TRI’s WACC, however, remained lower than many peers because of its credit ratings (see below), which allowed it to issue debt at more favorable spreads.

In finance, value is created when ROIC exceeds WACC. In 2020, In FY2020, the spread between ROIC and WACC was sub 2%. By FY2025, the spread has widened to the upper single digit range (~8% – 9.9%). This suggests TRI’s successful pivot to GenAI-integrated professional tools.

Risk Assessment

Many investors fixate on the potential return of an investment but overlook potential risks.

The risk aspect of an investment differs for every investor as our risk tolerance and circumstances differ. As a result, what I consider to be a ‘risky’ investment may satisfy another investor’s risk tolerance OR vice versa.

As part of my risk assessment process, I consider how the major credit rating agencies assess a company’s risk. Their risk ratings, however, are assigned to a company’s debt. My risk exposure is greater since I invest in a company’s equity. I rank ‘dead last’ should a company’ fall off the rails’. I, therefore, almost always restrict my investments to companies with reasonably strong investment grade credit ratings.

As I compose this post, the following are TRI’s domestic unsecured long-term debt credit ratings:

- Moody’s: Baa1 raised from Baa2 on November 27, 2023 and affirmed on November 13, 2025. This is the top tier of the lower-medium investment grade category.

- Morningstar DBRS:BBB (high) confirmed on June 27, 2025 with a stable outlook. This is the top tier of the lower-medium investment grade category.

- S&P Global: A- raised from BBB+ on May 30, 2025 with a stable outlook and last reviewed on April 14, 2026. This is the bottom tier of the upper-medium investment grade category.

- Fitch: A- raised from BBB+ on September 26, 2025 with a stable outlook and affirmed on February 12, 2026. This is the bottom tier of the upper-medium investment grade category.

The current ratings define TRI as having a strong capacity to meet its financial commitments. TRI, however, is somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

These ratings reaffirm my observation that TRI’s credit risk is acceptable for my relatively conservative risk profile.

Dividends, Return Of Capital, and Share Repurchases

Dividend

Details about TRI’s dividend are accessible here.

On May 5, 2026, TRI declared a USD$0.655/share dividend payable June 10, 2026.

Declaration and distribution of the quarterly dividend is in USD. Shareholders, however, can elect to have dividends paid in Canadian dollars or British Pounds Sterling.

Return Of Capital and Share Consolidation

On May 4, 2026, I received a $1.435518/share return of capital. This return of capital decision was primarily a mechanism to distribute the final tranches of significant excess cash following the company’s multi-year divestiture strategy.

There are 3 components behind the rationale for this return of capital.

Distribution of LSEG Sale Proceeds

The most direct driver was the liquidation of the company’s remaining stake in the London Stock Exchange Group (LSEG). TRI sold a large portion of its LSEG shares in May 2024.

The $0.605B special cash distribution (completed on May 4, 2026) was specifically earmarked as a return of the gross proceeds from that sale.

Management determined this cash was surplus to TRI’s immediate operational and M&A needs. The decision was made to return this surplus cash to shareholders rather than letting it sit on the balance sheet and potentially diluting ROIC.

Tax Efficiency for Canadian Shareholders

The combination of a specific structure of a return of capital with a share consolidation (reverse stock split) was chosen over a standard special dividend for tactical tax reasons.

For many Canadian residents, a return of capital is a reduction in the adjusted cost base (ACB) of their shares rather than immediate taxable income. It is, therefore, essentially a tax-free return.

Recognizing that this structure isn’t universally beneficial (especially for U.S. and other international investors), TRI provided an ‘opt-out’ mechanism. This allowed non-Canadian shareholders to avoid the immediate distribution and instead keep a higher proportional stake in the company.

Share Consolidation

To ensure the cash distribution did not result in a nominal drop in the share price that might affect index eligibility or financial ratios, TRI paired the payout with a share consolidation in which the share count was reduced by ~6.5 million shares; the number of outstanding common shares were reduced at a ratio of 1 pre-consolidated share for 0.984560 post-consolidated shares. This effectively neutralized the impact of the cash exit on the stock price, keeping the trading price relatively stable and ensuring that earnings-per-share (EPS) and dividend-per-share metrics remain robust.

Essentially, TRI’s Board signaled that while the company is aggressively investing in AI-powered ‘CoCounsel’ workflows, the business is generating more cash than those investments can currently absorb. This return of capital cleans up the balance sheet, leaving the company with a leaner, more focused capital structure as it moves deeper into its technology-first era.

Valuation

I have increased my TRI exposure with the purchase of 200 shares @ ~$92.237 on May 11. Using this purchase price and the currently available adjusted diluted EPS broker estimates, TRI’s forward adjusted diluted PE levels are:

- FY2026 – 15 brokers – ~20.8 using a mean of $4.43 and low/high of $4.13 – $4.60.

- FY2027 – 15 brokers – ~18.2 using a mean of $5.06 and low/high of $4.59 – $5.28.

- FY2028 – 5 brokers – ~16.3 using a mean of $5.65 and low/high of $5.09 – $5.94.

I place very little reliance on broker estimates since much can happen to make these estimates irrelevant. Furthermore, the disparity in estimates implies the brokers which cover TRI have very different outlooks.

My preference, however, is to analyze a company’s valuation using FCF.

TRI’s FY2026 FCF outlook is $2.1B and the diluted weighted-average number of common shares outstanding in Q1 2026 is 444.657 million. Subsequent to Q1, the share count was reduced by ~6.5 million shares thus lowering the diluted weighted-average number of common shares outstanding to 438.157 million. The company will undoubtedly issue additional shares over the remainder of FY2026 as part of its various compensation/incentive plans. It will, however, likely purchase additional shares. I, therefore, conservatively estimate the diluted weighted-average number of common shares outstanding in FY2026 will be ~437.5 million.

Conventional FCF Calculation

Using $2.1B of FCF and my ~437.5 million diluted weighted-average number of common shares outstanding estimate, TRI should generate ~ $4.80 FCF/share. Divide my ~$92.237 purchase price by ~$4.80 and the P/FCF is ~19.2.

Modified FCF Calculation

SBC in Q1 was ~$0.053B. If SBC is comparable in each of the next 3 quarters, SBC for FY2026 should be ~$0.212B. When I deduct this from the FY2026 $2.1B FCF outlook, the modified FCF is ~$1.888. Divide this by my ~437.5 million diluted weighted-average number of common shares outstanding estimate and TRI should generate ~$4.32 FCF/share. Divide my ~$92.237 purchase price by ~$4.80 and the P/FCF is ~19.2.

In my February 6 post I reflect the following:

Shares now trade at ~$88 as I compose this post on February 6, 2026.

In FY2025, TRI generated diluted EPS and adjusted diluted EPS from continuing operation of $3.33 and $3.92, respectively. Using the current share price, the diluted PE and adjusted diluted PE are ~26.3 and ~22.4.

Using this share price and the currently available adjusted diluted EPS broker estimates, TRI’s forward adjusted diluted PE levels are:

- FY2026 – 16 brokers – ~20 using a mean of $4.39 and low/high of $4.17 – $4.57.

- FY2027 – 14 brokers – ~17.6 using a mean of $5.01 and low/high of $4.70 – $5.26.

- FY2028 – 6 brokers – ~15.5 using a mean of $5.66 and low/high of $5.10 – $6.20.

I place very little reliance on broker estimates since much can happen to make these estimates irrelevant. Furthermore, the disparity in estimates implies the brokers which cover TRI have very different outlooks.

If TRI only manages to generate ~$4.17 in adjusted diluted EPS in FY2026, the forward adjusted diluted PE is ~21.1. This valuation is far more attractive than in recent years.

My preference, however, is to analyze a company’s valuation using FCF.

Conventional FCF Calculation

In FY2025, TRI generated $4.478 of FCF calculated using my conventional method of calculating FCF. Divide ~$88 by ~$4.478 and the P/FCF is ~19.7.

Modified FCF Calculation

In FY2025, TRI generated $4.095 of FCF calculated using my modified method of calculating FCF. Divide ~$88 by ~$4.095 and the P/FCF is ~21.5.

Final Thoughts

My final thoughts expressed in my prior post are unchanged.

I attribute TRI’s recent share price volatility and weakness to a deliberate corporate restructuring and broader market rotation rather than a signal of deteriorating business health. In essence, the recent selling pressure is likely the result of ‘risk-off’ sentiment rather than company-specific failures.

Investors have recently rotated capital out of premium-valuation Defensive Growth stocks into commodities and energy due to geopolitical tensions in the Middle East. Furthermore, some investors may have concerns about a higher expected net interest expense ($180M–$190M) for FY2026; the previous outlook was $150M – $160M. This higher interest expense, however, is a byproduct of the company’s aggressive capital return strategy and the broader rate environment. It is not a sign of credit instability.

TRI was not a top 30 holding when I completed my 2025 Year-End Investment Holdings Review. Following my May 11, 2026 purchase, I now hold a total of 700 shares in two different accounts included in the ‘Core’ component of the FFJ Portfolio. With shares currently trading at ~$92.237, my exposure is under USD $65,000. It is not, therefore, a top 30 holding. Nevertheless, I like the company’s long-term outlook which is why I have increased my exposure.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long TRI (the US listed shares).

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.