Summary

Summary

- This United Parcel Service stock analysis is based on Q4 and FY2016 results reported on January 31, 2017.

- UPS reported its results and the stock dropped roughly 8%.

- Results were impacted by a Mark-to-Market Pension Charge which resulted in EPS falling short of expectations.

- UPS continues to grow its business and FCF is still strong.

- UPS’ shares are now at the upper end of my “buy zone” and I acquired more shares on January 31, 2017.

Introduction

United Parcel Service, Inc. (NYSE: UPS) has been a wonderful investment for us over the years. I must admit, however, that 2012 was an extremely challenging year for UPS. Fortunately I approach investing with a long-term perspective and given the scale of the company and how it plays such an integral role in the movement of goods, I figured it would get back on track in short order. Sure enough, it did.

The purpose of this post is to review UPS’ results and its projections to determine whether we should increase our investment in UPS or just continue to automatically reinvest our quarterly dividends.

Business Overview

UPS was founded in 1907 as a private messenger and delivery service in Seattle, Washington. Today, UPS has 10 million customers in more than 220 countries and territories and operates in three segments (U.S. Domestic Package, International Package, and Supply Chain & Freight). It is:

- the world’s largest package delivery company

- a leader in the U.S. less-than-truckload industry

- the premier provider of global supply chain management solutions

A description of each of UPS’s 10 Reporting Segments, Products & Services, and Competitive Strengths can be found here.

Project ORION (On-Road Integrated Optimization and Navigation)

While drivers are the backbone of a logistics company, drivers with years of experience on the same route readily agree they are unable to compete with technology when it comes to finding the fastest, most fuel-efficient way to get packages to a customer’s door.

This is where UPS’s proprietary routing software (ORION) comes into play. This software uses package-level detail and customized online map data to provide drivers with optimized routing information. In essence, ORION can enhance customer service and reduce the numbers of miles driven by determining the most efficient delivery route.

While UPS has been extracting data on time of shipment and how it has matched delivery commitments for every package it delivers, ORION goes a step beyond. This software uses a combination of connected car-like telematics and a lot of data crunching of package information, user preferences and routes. It scans map data and historical GPS tracking of similar routes to come up with a solution.

In 2013, UPS began the first major deployment of ORION. Plans are to deploy ORION to all 55,000 North American routes by 2017. While UPS will not disclose the specific cost of the project, the information it has divulged suggests it takes up a good chunk of its $1B annual technology spend. Moreover, UPS has 500 staff working on its deployment.

Clearly, the magnitude of the amount spent on this project suggests UPS has huge expectations with respect to efficiency and cost savings once fully implemented.

Marken Acquisition (completed December 2016)

UPS completed its acquisition of Marken on December 22, 2016. The acquisition of Marken follows multiple UPS acquisitions that have expanded the company’s healthcare logistics services portfolio.

Marken is the only patient-centric supply chain organization 100% dedicated to the pharmaceutical and life sciences industries. It maintains the leading position for Direct to Patient services and biological sample shipments and offers a state-of-the-art Good Manufacturing Practices (GMP) compliant depot network and logistic hubs.

GMP, by the way, is a system for ensuring that products are consistently produced, controlled, and delivered according to quality standards. It is designed to minimize the risks involved in any pharmaceutical production that cannot be eliminated through testing the final product.

Marken has almost 700 staff members in 45 locations worldwide, including 10 depots that are compliant with GMP. It manages 50,000 drug and biological shipments every month at all temperature ranges to more than 150 countries. Additional services include biological kit production, ancillary material sourcing, storage and distribution, and shipment lane qualifications.

Pharmaceutical companies, clinical research organizations, and contract manufacturers rely on Marken for collection and transportation of clinical trial material and investigational medicinal products. In addition, they rely on Marken for the shipment of biological samples from these sites to central laboratories. These shipments are time- and temperature-sensitive, and their rapid, on-spec delivery is a key factor in the treatment of patients and the success of the clinical trial.

Q4 and FY2016 Financial Results

This UPS stock analysis is based on Q4 and FY2016 results reported on January 31, 2017.

Q4 Results

UPS reported:

- a 6.3% increase in US Domestic Revenue with Ecommerce being a driving force.

- Asia and Europe regions led the way with an 8.4% increase in International Export Shipments.

- EPS was ($0.27) as a result of a Mark-to-Market Pension Charge.

- The International Segment helped drive an adjusted EPS of $1.63 on $16.93B in revenue.

FY2016 Consolidated results

- 2016 diluted EPS: $3.87.

- Adjusted diluted EPS of $5.75 excludes the impact of the non-cash, Mark-to-Market pension charge.

- UPS generated $6.5B in cash from operations and $3.546B in FCF.

- CAPEX was roughly $3.0B.

- Dividends of $2.8B were paid which represents a 6.8% per share YoY increase.

- 5 million shares were repurchased for approximately $2.7B.

In my opinion, these are impressive results. Then why have UPS’ shares taken a hit just subsequent to the announcement of its results? Well, this is what happens when there are lofty expectations.

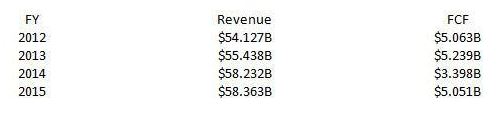

Here is a company which generated $60.906B in revenue and $3.546B in FCF in FY2016! That’s not bad.

How do these results compare with previous years’ results?

Source: Morningstar: UPS – Revenue and FCF 2012 – 2015

Sure, UPS’ revenue from overseas operations was pressured by the strong US dollar but this currency issue is plaguing most, if not all, US companies with international exposure. FCF also dropped $1.5B but FCF was still $3.546B!

Good grief! Volumes are up, UPS is controlling its pricing, and is investing heavily in project ORION to further improve efficiencies. What is not to like?

Outlook for Fiscal 2017

In its forecast for 2017, UPS provided guidance on an adjusted (non-GAAP) basis. UPS’ reasoning for this is that it is not possible to predict or provide a reconciliation reflecting the impact of future pension mark-to-market adjustments, which would be included in reported (GAAP) results and could be material.

UPS is already seeing tangible results from its investment in ORION. Bottom-line results, however, are being challenged by a shift in product mix and the continued softness in industrial production.

UPS expects 2017 adjusted diluted EPS to be $5.80 – $6.10, which includes $400 million of pre-tax currency headwinds. This currency drag is expected to lower the adjusted diluted EPS by $0.30 in 2017, and will decrease the EPS growth rates by approximately 500 bps.

Valuation

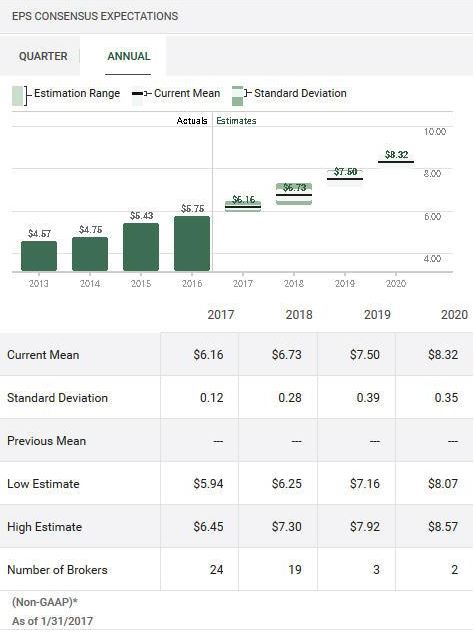

UPS’ diluted EPS and Adjusted diluted EPS in FY2016 were $3.87 and $5.75, respectively . While the FY2017 mean non-GAAP EPS derived from earnings estimates from 24 brokers is $6.16, I will go with the low side of UPS’ forecast and will use $5.80 to estimate at what value I would be prepared to acquire additional UPS shares.

Source: TD WebBroker – UPS Annual Earnings Estimates

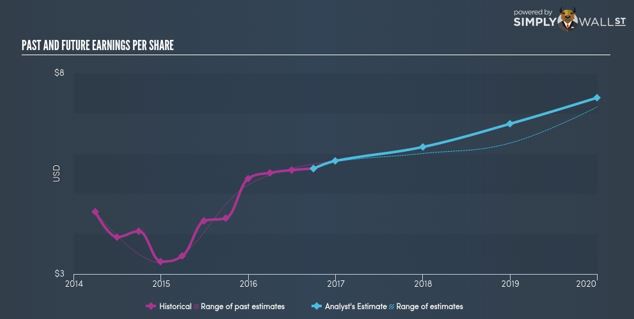

Source: Simply Wall Street – UPS Past and Future EPS

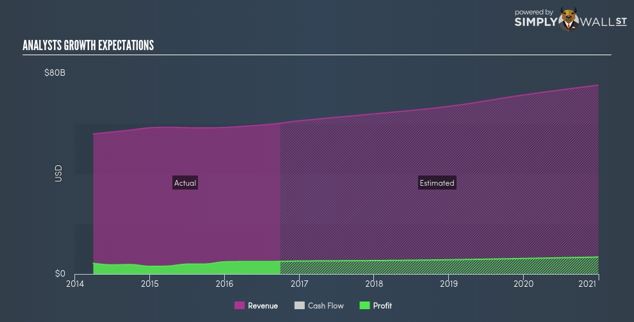

Source: Simply Wall Street – UPS Analyst Growth Expectations

As I compose this section of my post, UPS is trading at roughly $109.08 and its PE is now sub 20 (source: Google Finance).

If I use the forecast of $5.80 adjusted EPS and the current market price, I get a PE just under 19. I’m OK with that level for a company of the quality of UPS. I am not going to quibble about a couple of dollars here, a couple of dollars there. In the grand scheme of things, UPS will likely be worth a lot more 15 – 20 years from now.

UPS paid a quarterly dividend of $0.78 or $3.12/year in 2016. UPS has been consistently raising its quarterly dividend at least $0.05 for the last few years and I am of the opinion a $0.05/quarter dividend increase will be forthcoming very shortly.

If we use my quarterly/annual projected dividend of $0.83 and $3.32, we get a dividend yield of 3.04% based on the current market price. While this level is acceptable from my perspective, I recognize we all have different thresholds when it comes to the rate of return we want to achieve on our investments so this yield may be insufficient for some readers to initiate or increase their position in UPS.

United Parcel Service Stock Analysis – Final Thoughts

UPS is currently not a member of the FFJ Portfolio but it is held in one of our Registered Retirement Savings Plan accounts (RRSP); I am a Canadian resident. Fortunately I don’t get a 15% withholding tax haircut on dividends received from US listed stocks when they are held in such an account.

Yesterday I thought UPS was overvalued. With today’s roughly 8% pullback, however, it has come into my “buy zone”. I have, therefore, pulled the trigger and bought more UPS shares today.

I would have preferred to forewarn you of my decision to acquire additional UPS shares prior to the publication of this post since I do not want to come across as “pumping” a stock. The magnitude of my purchase relative to the January 31, 2017 trading volume of almost 9 million shares, however, has certainly not influenced the price; 2.17 million shares is the average daily volume according to Google Finance.

I look back at the dividends we have generated from UPS since the time we first acquired shares. The growth in our annual dividend income from UPS has been impressive. I am confident our UPS dividend income will be far greater in several years which will help finance our retirement lifestyle.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long UPS.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.