Summary

Summary

- VISA appears expensive at current levels but this is a result of several sizable one-time charges.

- The legal issue as it relates to interchange fees has still not been resolved.

- Even if VISA ends up having to pay a multi-billion dollar fine the interchange fee legal case should not dissuade investors from initiating / increasing a position in VISA with a long-term investment time horizon.

- VISA continues to operate on a business as usual basis and is investing heavily to address the ever evolving needs in the payment industry.

Note: All figures presented are expressed in USD unless otherwise stated.

VISA Inc. (NYSE: V) is one of the very few stocks on my list to hold in perpetuity. The reason I say this is because it is so intricately woven into our global payment system that any disruption to its business would be catastrophic. In my opinion, VISA is the equivalent of my veins and arteries through which my blood flows.

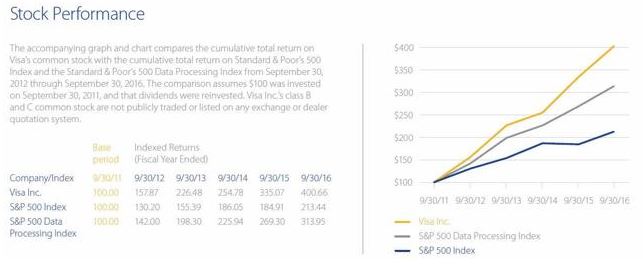

Thankfully, VISA became a publicly listed company in 2008, at which time I pulled the trigger and acquired 1000 shares. I say, thankfully, because the value of each VISA share is almost 6 times that of our average cost (as per data from my online brokerage trading platform). The following image only dates back to 2011.

VISA 5 Year Stock Performance

Source: VISA 2016 Annual Report, page 1

Business Overview

Most readers are familiar with VISA but many may not realize just how massive it is in scope!

This global payments technology company connects consumers, businesses, banks and governments in more than 200 countries and territories worldwide. It operates the world’s largest electronic payments network (based on payments volume, total volume, number of transactions, and number of cards in circulation) through which it processes credit, debit, prepaid and commercial transactions.

Here are some impressive key statistics taken from a somewhat outdated November 2015 Facts & Figures document VISA has posted on its website.

- 14,000+ financial institution clients and partners

- 36+ million merchant outlets

- 3+ billion VISA cards worldwide (Mastercard has roughly 1.6 billion cards in use) and in excess of US$5 trillion payments volume annually

- More than 2.4 million ATMs

- It processes over 83 billion total transactions annually (includes payments and cash transactions)

- VISA has the capacity to process 65,000 transaction messages per second

One of the attractive features of VISA’s business model is that it derives most of its revenue from fees it charges the card issuers and merchants who use its network; these fees are based on transaction volumes and other factors.

The business model is such that VISA has no responsibility for evaluating customer creditworthiness and collecting payments. This burden rests with the financial institutions which issue VISA cards and which provide merchant services.

Acquisition of VISA Europe

As part of the 2008 reorganization, VISA hived off its European operations (VISA Europe) as an independent firm owned by over 3,700 European banks. VISA Europe used VISA’s brand and payment networks under a licensing deal, and its volume accounted for about half of Europe’s card market.

Prior to December 2015, VISA had an impeccable balance sheet with essentially no long-term debt. In December 2015, however, it issued $16B of fixed-rate senior notes with maturities ranging between 2 and 30 years; interest on the notes ranges between 1.20% and 4.30% and is payable semi-annually on June 14 and December 14 of each year.

In June 2016, VISA completed the acquisition of 100% of the share capital of VISA Europe for €12.2 billion ($13.9 billion) and €5.3 billion ($6.1 billion) in preferred stock, with an additional €1.0 billion ($1.14 billion), plus 4% compound annual interest, to be paid on June 21, 2019.

While $16B is a staggering amount of money, you need to put this amount in perspective. VISA’s long-term debt of $15.882B as at VISA’s September 30, 2016 fiscal year-end was only roughly 9% of its market capitalization. Furthermore, VISA held $5.6B in cash and a little in excess of $3.3B in short-term investment securities.

2016 Annual Report

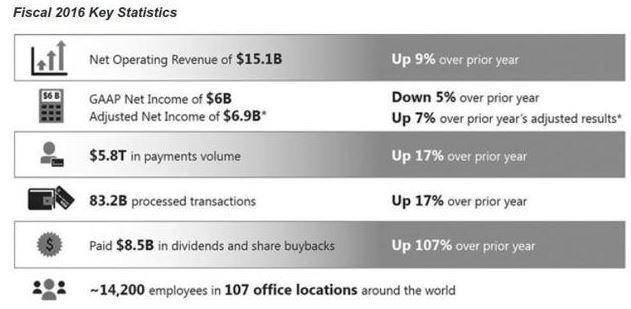

Thanks in part to the strategic acquisition of VISA Europe, VISA achieved the following impressive results in fiscal 2016:

VISA Fiscal 2016 Key Statistics

Source: VISA 2016 Annual Report, page 6

Legal Actions

VISA certainly is extremely busy on the legal front. The “Note 20 – Legal Matters” , where you can find a synopsis of the multiple legal actions in which VISA is engaged worldwide, commences on page 128 and ends on page 137 of the 2016 Annual Report.

One of the most controversial issues in recent years revolves around rates as they relate to interchange fees. These are paid between banks for the acceptance of card based transactions. They are set by credit card networks such as VISA, Mastercard (NYSE: MA), American Express (NYSE: AXP), and Discover (NYSE: DFS) and represent roughly 70% – 90% (less for large merchants such as Wal-Mart and Amazon) of the various fees most merchants pay for the privilege of accepting credit cards.

In the United States, a class action lawsuit was filed in 2006 by a class of 14 million merchants against VISA and Mastercard.

In 2012, VISA and Mastercard agreed to a $7.5B settlement in what was deemed to have been one of the largest-ever antitrust agreements in the US thus bringing to an end a lengthy period of uncertainty for the credit card networks. Several large merchants, however, opposed the settlement and filed an appeal.

In June 2016, the US Court of Appeals overturned the settlement in its entirety. As a result of this ruling, there is an element of uncertainty around interchange and future rules.

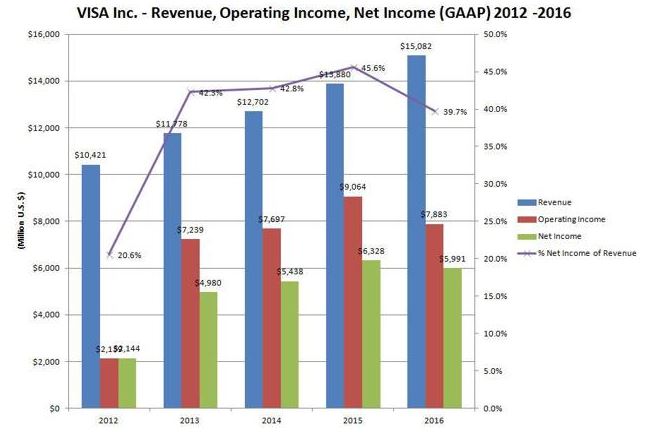

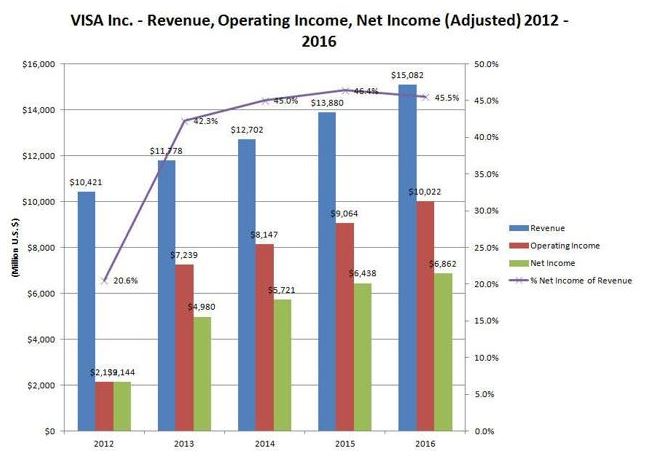

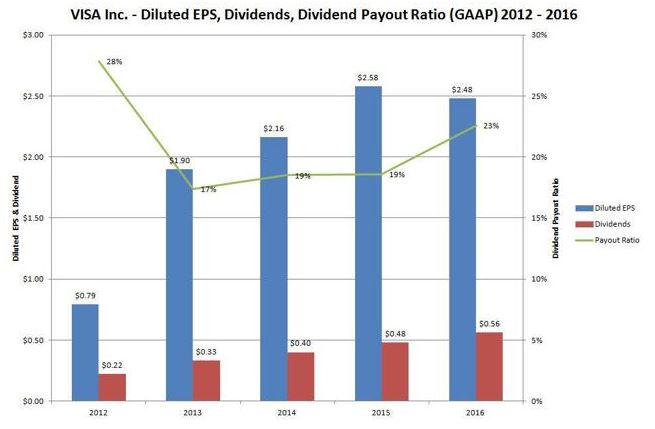

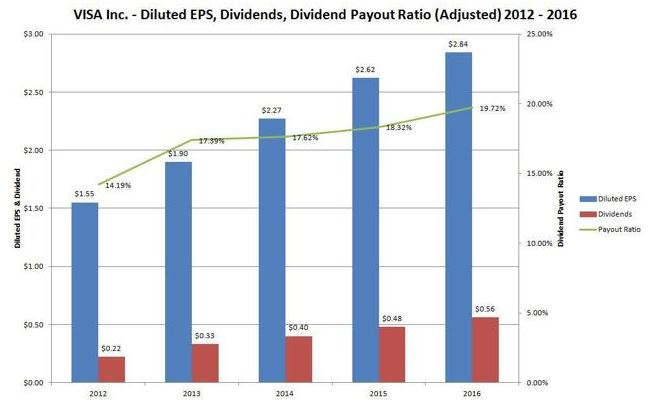

Financial Highlights (GAAP) and (Adjusted) FY 2012 – FY 2016

The following graphs show how VISA has performed fiscal 2012 – 2016 (all per-share amounts adjusted for a 4-for-1 stock split in March 2015) and were created using data extracted directly from VISA’s 2012 – 2016 Annual Reports.

While the Generally Accepted Accounting Principles (GAAP) results reflect a drop in Operating Income and Net Income relative to fiscal 2015, you need to take into consideration the costs associated with the VISA Europe acquisition were a one-time occurrence. Management backed out these one-time costs to arrive at the “Adjusted” results; both are provided below for comparison purposes.

The “Adjusted” results exclude almost $1.9B in VISA Europe Framework Agreement loss, a $693MM USD income tax provision related to said matter, and roughly $262MM in severance and acquisition related costs.

VISA Revenue, Operating Income, Net Income (GAAP) 2012 – 2016

VISA Revenue, Operating Income, Net Income (Adjusted) 2012 – 2016

Diluted EPS took a hit as a result of these one-time charges but continued to trend in the right direction on an adjusted basis.

The quarterly dividend continues to be increased annually and the payout ratio is very conservative at a level around 20% of EPS.

VISA Diluted EPS, Dividends, Dividend Payout Ratio (GAAP) 2012 – 2016

VISA Diluted EPS, Dividends, Dividend Payout Ratio (Adjusted) 2012 – 2016

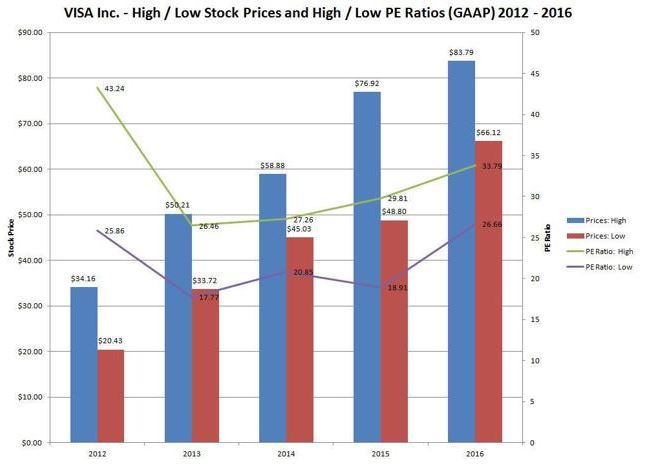

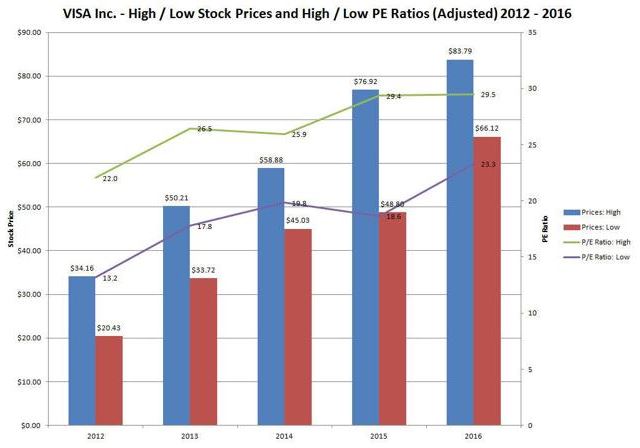

VISA’s PE ratio in 2016 has certainly experienced a run-up but is somewhat consistent with the market conditions over that past year.

VISA High/Low Stock Prices and High/Low PE Ratios (GAAP) 2012 – 2016

VISA High/Low Stock Prices and High/Low PE Ratios (Adjusted) 2012 – 2016

Outlook for Fiscal 2017

VISA generates just under half its revenue from outside of the U.S., and the high U.S. dollar has hurt the contribution from its overseas businesses. Even so, the addition of VISA Europe should increase EPS in fiscal 2017 by 15.5% (using the Adjusted 2016 EPS of $2.84) to $3.28.

As at the close of business January 11, 2017, VISA traded at almost 25 times the $3.28 EPS forecast. While this level is high from my perspective, this slightly elevated level is somewhat acceptable in light of VISA’s high market share, strong global growth prospects, and well-known brand.

VISA recently raised its quarterly dividend by 17.9%, to $0.165 a share from $0.14. The new annual rate of $0.66 yields just over 0.8% based on the January 11, 2017 closing price of $81.80.

In addition, VISA announced a new $5 billion share repurchase program, thus increasing the total available for share repurchases to $7.3 billion. VISA intends to continue to repurchase its shares until it has repurchased sufficient stock to offset the impact of preferred stock issued to VISA Europe members; management expects the buyback program to be completed by the end of fiscal Q1 2018.

VISA Stock Analysis – Final Thoughts

Despite renewed uncertainty as a result of the reversal of the settlement of claims related to the improper fixed credit-card swipe fees, it is business as usual for VISA.

The company continues to invest heavily in new technology, such as VISA Checkout, Digital Wallets, VISADirect, mVISA, Tokenization, Decision Manager Replay, and New VISA Consumer Authentication Service to address the ever evolving needs in the payment industry.

While VISA is certainly not a bargain at current levels, any investor with the intent of holding VISA for the long-term could do no wrong by purchasing VISA at these levels. I will continue to add to our VISA position in various tranches even though I think there is a possibility of a long overdue market correction at some stage in 2017. Should a correction materialize and VISA experience a nice correction in price, I will increase my level of purchases.

If an investment in VISA is of interest to you, note that it will be reporting its Q1 FY2017 financial results on Thursday, February 2, 2017. The results, along with accompanying financial information, will be released after market close and will be posted on the VISA Investor Relations website.

Finally, should you be a Canadian resident like me, you may wish to consider acquiring VISA within your Registered Retirement Savings Account (RRSP) or Registered Retirement Income Fund (RRIF) where you will avoid the 15% withholding tax on dividends received from US listed stocks. Having said this, if you have insufficient contribution availability within your RRSP, initiating or increasing a position in VISA within a Tax Free Savings Account (TFSA), a Registered Education Savings Plan (RESP), or a non-registered account would certainly be wise.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long V, MA.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.

Thanks for reading. I really don’t think you can go wrong owning VISA (nor Mastercard for that matter). Here’s hoping for a nice market correction in 2017!