The purpose of this post is to explain why I think low or no dividend yield companies belong in your portfolio.

I recently received an email from a reader in Brazil as a follow-up to my VISA post and on Seeking Alpha. Suddenly a new topic to research and write about.

Then, very late last night, I get an email from another blogger whose work impresses me (I swear this guy never sleeps!). I highly recommend you check out The Financial Canadian’s site. There is some great material there. In addition, he writes guest posts for Sure Dividend. We regularly exchange correspondence and run many of our posts by each other for honest feedback before publishing.

In his email he enclosed a draft version of his “Why Low Yield Dividend Stocks Belong in Your Portfolio” post; his guest post will be appearing on Sure Dividend within the next 24 hours and I urge you to check it out.

The topic of his post got me thinking. This would also be a good topic for me to cover. I certainly, however, don’t want to replicate his work. I am, therefore, approaching this subject from a “personal” perspective.

Lately, dividend investing appears to be the “flavor of the month”. When interest rates on term deposits, GICs, and bank accounts were in the mid – high teens in 1980 – 1981, investing in companies with dividend yields at a fraction of these rates was not in vogue. Now that relatively risk-free instruments offer negligible interest, people look for other investment opportunities to provide superior income.

Judging from some of the blogs I have read and some of the comments posted on Seeking Alpha, there clearly are investors out there who are reaching for yield. One comment I recently read on Seeking Alpha was from someone who indicated they don’t invest in anything with an annual dividend yield below 6 – 7%.

It is not my place to suggest what one should do with their money but when risk-free interest rates are at current rock-bottom levels, you know that an investment yielding 6 – 7% yield is taking someone a bit further out into the “risky” zone of the risk spectrum.

I won’t steal The Financial Canadian’s thunder (please just read his post which should appear on The Sure Dividend site within 24 hours). I do, however, want to provide some additional examples of how low dividend yield or no dividend yield companies can have a dramatically positive impact on your portfolio.

I provide the following graphs for stocks we own in the FFJ Portfolio or in accounts for which I am not prepared to disclose any details for confidentiality reasons. These graphs were all generated through Google Finance.

Each graph compares the stock’s performance relative to either the S&P 500 or NASDAQ index from the date of our initial “major” purchase.

Note that each stock has a minuscule dividend yield.

VISA (NYSE:V) – we acquired shares shortly after its IPO.

V vs S&P 500

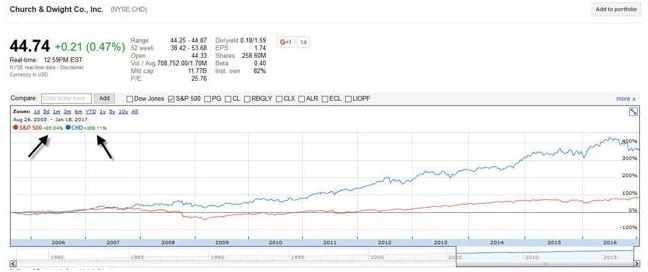

Church & Dwight (NYSE: CHD) – we acquired these shares because I was familiar with their Arm & Hammer and Trojan products.

CHD vs S&P 500

Broadridge (NYSE:BR) and CDK Global (NASDAQ: CDK) – we received shares when these entities were spun off from ADP.

BR vs S&P 500

CDK vs NASDAQ

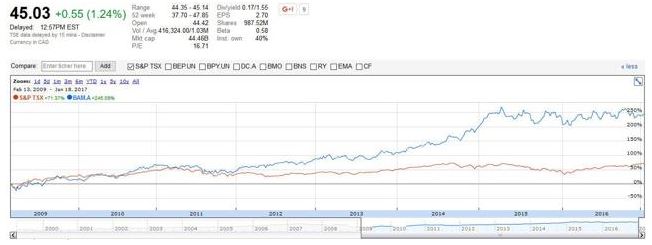

Brookfield Asset Management (TSX:BAM.a) – we own the Canadian listed shares. We also received Brookfield Business Partnership units (TSX:BBU.UN) and Brookfield Property Partners units (TSX: BPY.UN) when these entities were spun off from BAM.a, so our return on BAM.a is even better than what is reflected on the graph.

BAM.a vs TSX

Now I ask you, do you think I am upset because of the low dividend yield? I don’t think so. If I can triple or quadruple my investment, I’ll put up with a low dividend yield.

Not only have we benefited from the increase in the value of these companies over time, we have paid $0 tax on this growth!

In the case of the dividend income we receive annually, we have had a couple of levels of government stick their hands in our pocket every year. It is gratifying/satisfying to have something that increases in value where we don’t have to share the wealth….year after year after year after year!

I certainly would not invest 100% of our money in low and non dividend paying stocks. After all, the method to the madness I used when creating our investment portfolio was to generate a dividend and rental income stream to support our lifestyle. The liquidation of any investments would be solely if it was advantageous from a tax planning perspective.

Some of you are thinking “What goes up must come down”. That’s fine. I am not worried about the stock prices of these companies coming down. In fact, I want them to come down so I can purchase more shares; this assumes the drop in price is not because of some permanent impairment of the underlying business).

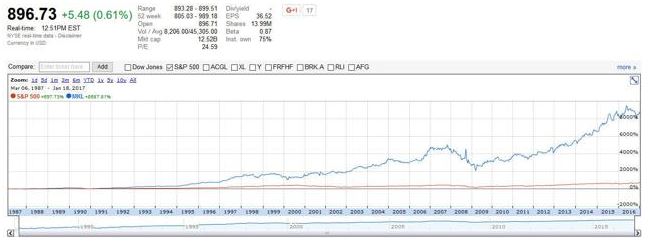

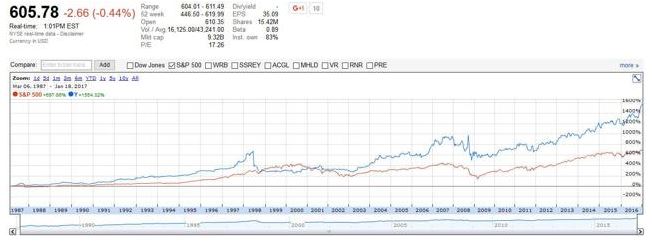

Here are graphs for some companies which pay NO dividend and on which I never pulled the trigger; Markel, White Mountain, and Alleghany.

I set the start date for March 1987 which is when I first heard of these companies. I think we have all experienced moments in our life where down the road you think “I Shoulda, I Woulda, I Coulda”. These are examples of some of my “I Shoulda, I Woulda, I Coulda” moments.

MKL vs S&P 500

WTM vs S&P 500

Y vs S&P 500

I recognize some readers are primarily focused on generating a dividend income stream to support their lifestyle during retirement, take time off work to raise a family, start a business that may not generate immediate income, or countless other reasons. In this case, low dividend or no dividend stocks may have absolutely no appeal to you. Not a problem. Perhaps just a small portion of your investment money can be placed in these types of stocks. You may be aptly rewarded in the long run.

CAVEAT: Speculative stocks, such as those for junior mining companies or high-tech companies with no proven track record of sustained profitability, are COMPLETELY excluded as possible low/no dividend yield investments.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence, and consulting your financial advisor about your specific situation.

Disclosure: I am long V, CHD, BR, CDK, BAM.a, BBU.un, BPY.un

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.