I crafted the following list of stock picking rules to follow because selecting companies in which to invest can be a daunting undertaking.

There are so many companies from which to choose which is why it is wise to pay heed to what Warren Buffett wrote in the 1977 Berkshire Hathaway annual report. Berkshire Hathaway wants a business:

- that we can understand;

- with favorable long-term prospects;

- operated by honest and competent people;

- available at a very attractive price.

These rules address the four conditions Buffett mentioned.

Rules

Rule 1 – Invest only in companies where the business model is easy to understand. Examples of such businesses would be McDonald’s (NYSE: MCD) and VISA (NYSE: V).

Rule 2 – Invest only in companies where management is ethical and acts in the best interests of shareholders.

Rule 3 – Before you invest in a company, learn about the industry in which it operates.

I worked in the Canadian banking industry my entire career. I understand how Royal Bank (TSX:RY), TD Bank (TSX: TD), Scotiabank (TSX:BNS), CIBC (TSX: CM), and Bank of Montreal (TSX:BMO) operate.

Rule 4 – Invest in companies that produce products or provide services with which you are familiar.

Church & Dwight (NYSE: CHD) produces Arm& Hammer baking soda and we have always had a box in our fridge. This prompted me to investigate the company several years ago. My due diligence revealed that it produces antiperspirant, toothpaste, air filters for vehicles, laundry detergent, Trojan condoms, and a host of other consumable products which are consumed regardless of economic conditions.

Rule 5 – Invest in companies across five broad industry sectors: financials, natural resources, utilities, consumer goods and services, industrial goods and services.

Rule 6 – A historical track record of increasing profitability is paramount. While it is important to look for companies with steadily growing Earnings per Share (EPS), earnings can be manipulated. Look for companies with strong positive Free Cash Flow (FCF). FCF determines the company’s ability to pay dividends.

Rule 7 – The old investing axiom, “past results do not guarantee future performance” is true. If a company has a strong past performance, however, there is a stronger probability of strong performance in the future versus a company with a spotty record.

Rule 8 – A manageable level of leverage can help a company build its business. Too much debt, particularly at high rates, can be detrimental.

Total Debt/Total Capital ratios vary by industry. Compare a company’s ratio relative to members of its peer group. Do not, for example, compare debt levels for a utility with a company in the consumer goods and services sector.

Rule 9 – Look for companies with a historical track record of a growing dividend. A good starting point is the Dividend Aristocrats. This is a select group of US listed companies with a track record of 25+ consecutive years of dividend increases.

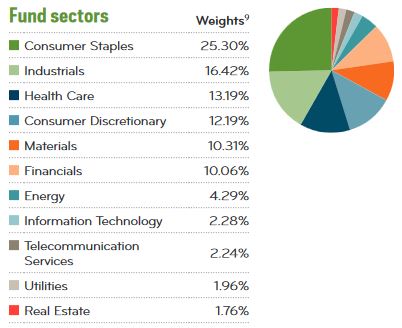

ProShares US Dividend Aristocrats Index ETF constituents as at March 17 2017

US Dividend Aristocrats Sector Exposure December 31 2016

There is also a similar list of Canadian Dividend Aristocrats. The criteria to belong are that securities:

- have consistently increased cash dividends for at least five consecutive years;

- have at least a C$300Million market capitalization;

- are from the S&P Broad Market Index

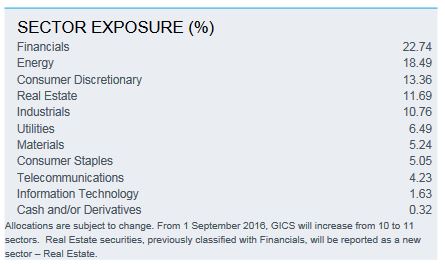

ishares S&PTSX Canadian Dividend Aristocrats Index ETF constituents as at March 17 2017

Canadian Dividend Aristocrats Sector Exposure February 28 2017

Do not, however, restrict your search solely to companies which are Dividend Aristocrats. Wonderful companies such as VISA (NYSE: V), MasterCard (NYSE: MA), Microsoft (NASDAQ: MSFT), and Apple (NASDAQ: AAPL) do not meet the Dividend Aristocrat requirements. This is because they only started paying dividends within the last few years. Furthermore, VISA and MasterCard have not been publicly traded entities for 25 years.

Rule 10 – Price and value are not always the same. This applies to all purchases including investments.

“Price is what you pay, value is what you get.” – Warren Buffett

Rule 11 – Focus on buying fairly valued wonderful companies. Wonderful companies allow you to compound your wealth. Making money from fair companies purchased at wonderful prices tends to only happen if you are able to sell your investment for a better price at a later date.

“It is far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” – Warren Buffett

Rule 12 – Wonderful businesses can be overvalued. You severely limit your ability to grow your wealth when you overpay for an investment.

“For the investor, a too-high purchase price for the stock of an excellent company can undo the effects of a subsequent decade of favorable business developments.” – Warren Buffett

The Price/Earnings (P/E) ratio for most of the Dividend Aristocrats currently exceeds their 5 year historical level. As at March 17, 2017, the 5 year historical P/E and current P/E ratios for 3M, for example, are 19.40 and 23.57 while those for ADP are 25.63 and 28.08.

Rule 13 – Avoid thinly traded stocks and small caps. Gravitate to “Best in Breed” companies in which several hundred thousand shares trade daily and whose market capitalization is in excess of $5B. These figures will be much greater for US listed entities since the universe of companies is far greater than in Canada.

Rule 14 – Include in your portfolio large multi-national companies with international operations listed on major US stock exchanges. This allows for a greater level of diversification.

Stock Picking Rules to Follow – Final Thoughts

We are often tempted to take advantage of every investment opportunity possible. Our opportunities, however, are actually incredibly finite. Narrow them down so you can focus on the successful ones with your limited resources as opposed to jumping at every opportunity presented.

Andrew Carnegie’s sage advice rings true to this day:

“The concerns which fail are those which have scattered their capital, which means that they have scattered their brains also. They have investments in this, or that, or the other, here, there and everywhere. “Don’t put all your eggs in one basket” is all wrong. I tell you “put all your eggs in one basket, and then watch that basket.”

Look round you and take notice; men who do that do not often fail. It is easy to watch and carry the one basket. It is trying to carry too many baskets that break most eggs in this country. He who carries three baskets must put one on his head, which is apt to tumble and trip him up. One fault of the American businessman is lack of concentration.”

The greater the number of investments the more unwieldy the portfolio becomes and the greater the challenge to truly understand each company and the industry in which it operates.

Very good list of rules. Helps me to appreciate your articles even more. 😉