Summary

Summary

- This Kellogg stock analysis is based Q4 and FY2016 results and forecast presented February 9, 2017 which reflects continued struggles.

- It does not have an enviable Revenue, FCF, Gross and Operating margins, and Debt/Equity track record.

- Kellogg has not had a wide economic moat for years.

- Kellogg does not satisfy several of my Stock Picking Rules to Follow.

Introduction

In reviewing my overall portfolio and my Stock Picking Rules to Follow, I realized our portfolio is underweighted in the Consumer Goods sector.

Given that Kellogg (NYSE:K) recently released its Q4 and FY2016 results and forecast, I thought it would be an opportune time to determine whether it would be a worthwhile addition to our holdings.

Business Overview

K products are manufactured and marketed globally.

It is the world’s leading producer of cereal, second largest producer of cookies and crackers, and a leading producer of savory snacks and frozen foods. Additional product offerings include toaster pastries, cereal bars, fruit-flavored snacks, and veggie foods.

Operations are managed through operating segments based on product category or geographic location. These operating segments are evaluated for similarity with regards to economic characteristics, products, production processes, types or classes of customers, distribution methods and regulatory environments to determine if they can be aggregated into reportable segments.

Results of operations are reported in the following reportable segments:

- U.S. Morning Foods – includes cereal, toaster pastries, health and wellness bars, and beverages;

- U.S. Snacks – includes cookies, crackers, cereal bars, savory snacks and fruit-flavored snacks;

- U.S. Specialty – represents food away from home channels, including food service, convenience, vending, Girl Scouts and food manufacturing;

- North America Other – includes the U.S. Frozen, Kashi and Canada operating segments;

- Europe – consists of European countries;

- Latin America – which consists of Central and South America and includes Mexico

- Asia Pacific – consists of Sub-Saharan Africa, Australia and other Asian and Pacific markets.

FY2016 Financial Results

K’s Q4 and FY2016 results and forecast presented February 9, 2017 can be found here.

Kellogg Summary of Q4 and FY2016 Financial Results Presentation –

February 9, 2017

K’s largest customer, Wal-Mart Stores, Inc. and its affiliates, accounted for approximately 20% of consolidated net sales during 2016, 21% in 2015, and 21% in 2014, comprised principally of sales within the United States.

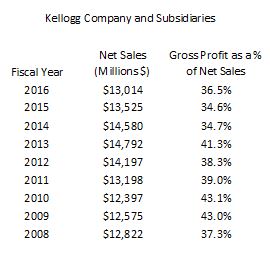

The following Net Sales and Gross Profit Margin chart does not reflect an enviable performance record. K has spent the last several years doing what it can to wring out every possible cost from its distribution network and the work is still not done. At some stage, K needs to grow its revenue.

K faces a huge challenge in this regard in that it needs to contend with General Mills (NYSE: GIS) and generic brands. It no longer has the economic moat it once had.

Kellogg – 2008 to 2016 Net Sales and GP Margin

Exit from the DSD

K historically used a Direct Store Delivery (“DSD”) selling and distribution system. It announced that it is shifting the affected portion (roughly 60%) of its U.S. Snacks segment to the warehouse distribution system through which it currently distributes the rest of U.S. Snacks and all of its other North America businesses.

Exiting DSD means K will no longer ship product directly to its retail customers’ stores but rather to their chain-wide warehouses. This will enable K to leverage the scale and technology of its, and its customers’, warehouse systems. This is expected to result in greater cost-efficiency and asset utilization while freeing up resources to invest in future growth.

Source: CAGNY February 21, 2017 Kellogg presentation

The transition from DSD will be primarily executed during Q2 and Q3 2017. It will encompass a transfer of inventory from K’s DSD distribution centers to retailers’ warehouses, a reduction in workforce, and the closing of DSD distribution centers.

K anticipates a reduction in net sales in U.S. Snacks during 2017 because of initial volume disruption and the impact of reducing stock-keeping units. In addition, it will include a reduction in list-prices reflecting the elimination of DSD services provided to retailers.

Overhead savings from the exit of the DSD system are expected to begin to accrue in Q4.

Project K

In November 2013, K announced Project K, a global efficiency and effectiveness program. The purpose of this four-year efficiency and effectiveness program is to drive the creation of new and improved capabilities in various parts of the company. In addition, it is also creating the supply chain of the future and a global business services structure. The global business services structure is streamlining some functional areas within the company.

When launched, Project K was expected to generate $425 – $475 million of annual cost-savings by 2018. The transition from DSD will contribute to an expanded Project K program whose savings will extend through 2019. Savings for Project K are now projected to reach $600 – 700 million through 2019.

Cumulative up-front costs for Project K are now expected to be $1.5 – $1.6B through 2019, up from previous estimates of $1.2 – $1.4B through 2018. The cash impact of these up-front costs is now expected to be at the high end of the previously estimated range of $0.9 – $1.1B.

These savings, in addition to those generated by K’s zero-based budgeting efforts, will provide K with the opportunity to make significant investments in the business while improving margins.

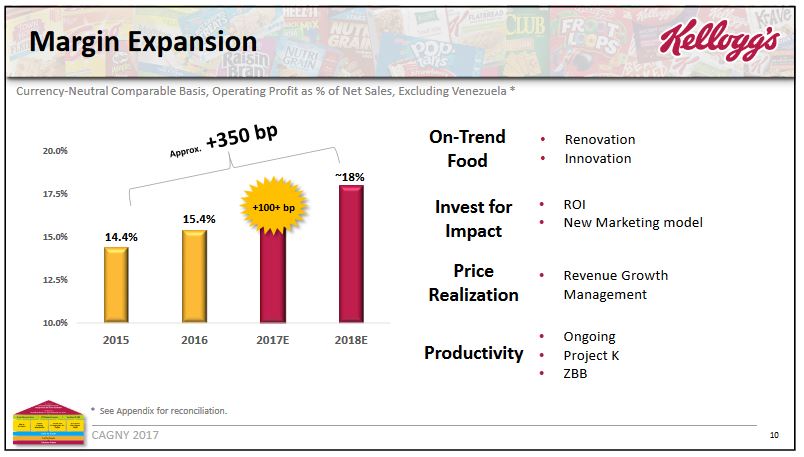

Operating Margin Expansion for 2018

K is working to stabilize net sales with an aim to return to growth. Its volume and price impact of exiting DSD, the elasticity impact of certain pricing actions, and the effect of portfolio optimization, in conjunction with current industry dynamics, is likely to result in a decline in currency-neutral comparable net sales (excluding Venezuela) by approximately 2% in 2017.

In 2016, K announced a plan to expand its currency-neutral comparable operating margin (excluding Venezuela) by 350 bps during 2016 through 2018. This is an increase and acceleration from its previous guidance, which targeted a 17-18% currency-neutral comparable operating margin excluding Venezuela by 2020.

Margin-expansion actions are expected to drive accelerated growth in currency-neutral comparable operating profit and currency neutral comparable earnings per share (excluding Venezuela) in 2017 and 2018.

Source: CAGNY February 21, 2017 Kellogg presentation

The four elements to this accelerated margin expansion plan are:

- Productivity and Savings – In addition to annual productivity savings to offset inflation, K will expand its zero-based budgeting initiative in the U.S. and international regions. It is working on additional Project K initiatives which should result in higher annual savings.

- Price Realization – A more formal global Revenue Growth Management discipline is being established.

- Investing for Impact – K’s investment model is being updated to align with current consumer and technology to optimize the return on investment in our brands.

- On-Trend Foods – K is adopting a more impactful approach to renovation and innovation of its products.

As K continues to implement zero-based budgeting, it may identify additional efficiency and effectiveness opportunities in advertising through 2017. K has indicated that it may choose to reinvest these savings back into advertising, or other areas such as food reformulation or capacity to drive revenue growth, or to achieve its 2018 Margin Expansion target.

2020 Growth Strategy

On February 21, 2017, K presented an update on its 2020 growth strategy at the Consumer Analyst Group of New York (CAGNY) Investor Conference.

Source: CAGNY February 21, 2017 Kellogg presentation

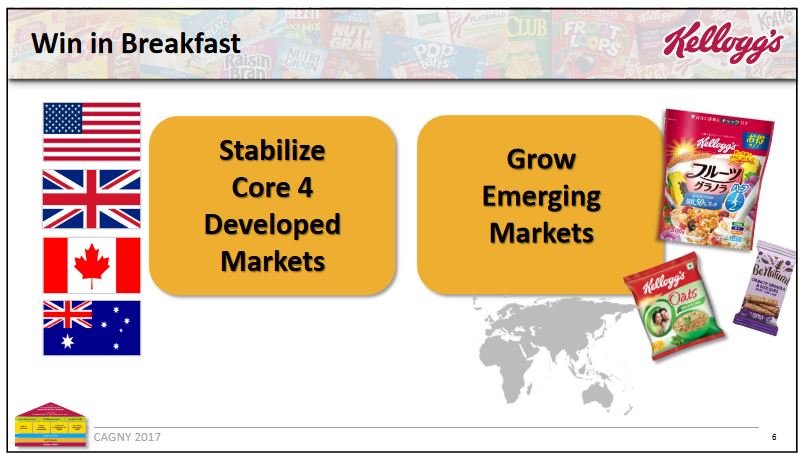

Win in Breakfast

- ~41% of current sales come from the breakfast occasion;

- four core cereal businesses have been somewhat challenged in recent years;

- U.S., Australia, and Canada are all largely stabilized and K is looking to grow again over time.

Source: CAGNY February 21, 2017 Kellogg presentation

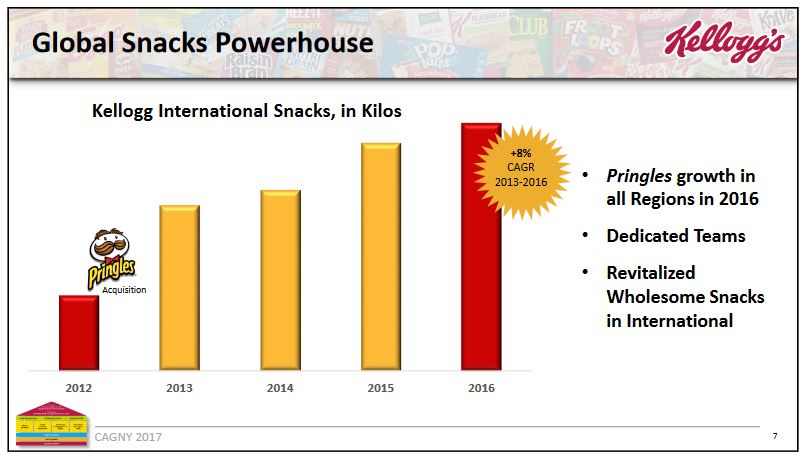

Be a Global Snacks Powerhouse

- Snacks generate $230B in annual total worldwide sales and represent almost 50% of K’s global sales;

- Wholesome Snacks is an area of focus for K;

- Pringles, acquired in 2012, revolutionized K’s international snacks business. It doubled or tripled the size of the business in certain key markets;

- Tonnage: 8% volume CAGR since 2013, the first full year with Pringles in the base figures;

- Prior to Pringles, K had one combined business unit trying to do cereal and snacks. It now has dedicated teams in Europe, Latin America, and Asia Pacific focused on snacking.

Source: CAGNY February 21, 2017 Kellogg presentation

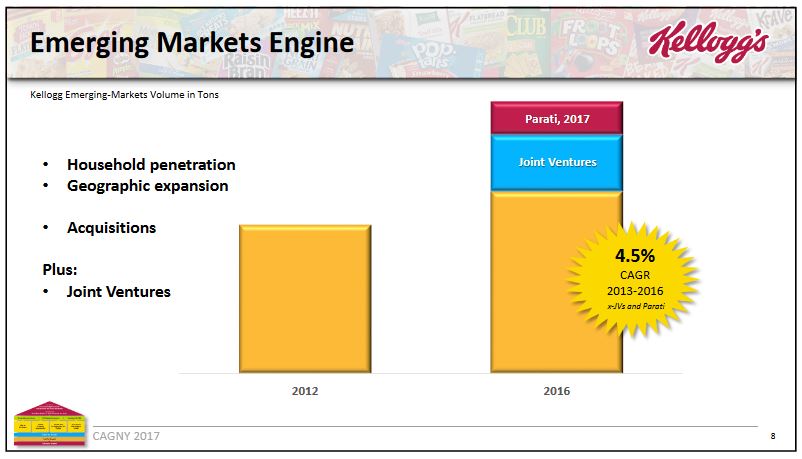

Double Emerging Market Footprint

- Potential exists because 80% of K’s current sales come from 20% of the global population;

- Progress made but much has yet to show up in reported results;

- 4% to 5% annual growth in volume from 2012 to 2016;

- Made the largest investment of any food company in Nigeria, and K is now one of the largest food companies in Nigeria;

- Acquisition of Parati in Brazil triples size of Brazilian business and changes the shape of K’s Latin American business. Around 25% of K’s sales in Latin America now come from snacks where in the past it was largely a cereal business.

Source: CAGNY February 21, 2017 Kellogg presentation

Win Where the Shopper Shops

- Become more of a snacking company;

- Invest in high frequency stores such as convenience stores in the U.S. or mom-and-pop stores in Mexico and around the world;

- Having the right portfolio is important. Examples include having Pringles in smaller cans, individual cereal bars, and small sachets of cereal, which all target key price points;

- eCommerce is going to be a major disruptive force. 1% or 2% of sales in the U.S. is currently conducted through eCommerce. As much as 10% of sales go through eCommerce in some European markets while roughly 30% of sales in China go through eCommerce.

Source: CAGNY February 21, 2017 Kellogg presentation

Build a $1 Billion Next-Generation Natural Business

- Create a sustainable, global next-generation natural foods business spanning both cereal and snacks;

- Leverage new and existing assets located primarily in the US-based Kashi business and to some extent K’s regional assets, such as its Be Natural brand in Australia.

Valuation

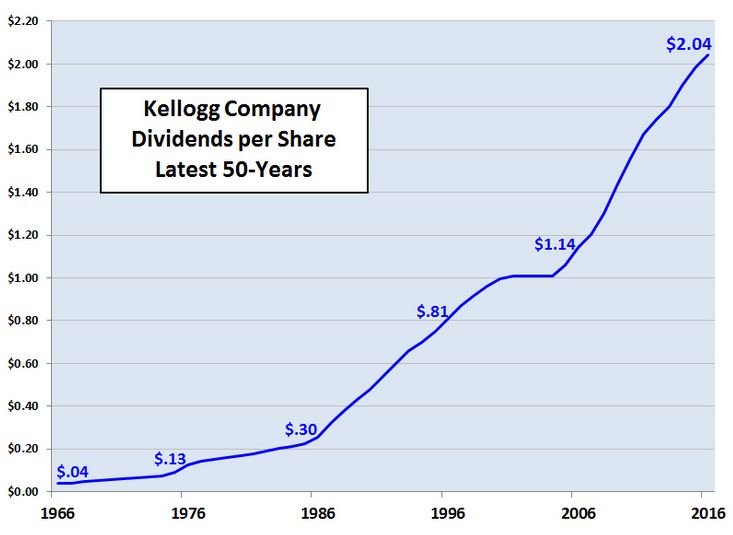

Kellogg is a Dividend Achiever having increased its dividend for 10+ consecutive years. In addition, based on its current $0.52/quarter dividend, K yields slightly in excess of 2.8%. Both these factors might lull some investors into purchasing K shares. I would caution investors to look beyond the dividend.

Kellogg Dividend History

As I compose this post, K is trading at $73.60 and its PE is in excess of 37.5. The 5 year average PE is just shy of 31. Not only does the PE grossly exceed the historical average, it is at a level where there is little margin for error.

It can take several years for you to generate a reasonable return on investment if you overpay. This caveat also applies to wonderful companies and, making matters worse, I do not deem K to be a wonderful company relative to the universe of companies in which you can invest.

Kellogg – Morningstar Valuation March 21 2017

The mean 2017 EPS estimate from several analysts is roughly $3.94. Considering K is not a high growth business, I would not be prepared to pay more than 15 – 16 times EPS. On this basis, I would not be prepared to pay more than $63.

Source: TD WebBroker – Kellogg Annual EPS Consensus

Source: ValueEngine – Kellogg Annual EPS Consensus

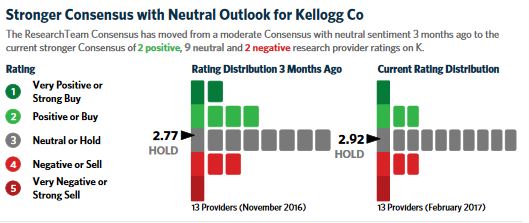

Looking at this graph, K is a weaker “HOLD” rating than 3 months ago. I agree will the consensus rating provided by 13 research providers.

Kellogg – Research Team Consensus Ratings

Warren Buffett has offered the suggestion that in order to improve your ultimate financial welfare think of having received a ticket with only 20 slots. These slots offer you 20 punches that represent all the investments you can make in a lifetime. Once you punch through the card, you can make no further investments. I know I would not want to use up one of my slots to acquire K.

Kellogg Stock Analysis – Final Thoughts

I undertook this analysis to determine whether K would be a suitable addition to our portfolio as we are somewhat underweight the Consumer Goods sector. After reviewing K, I have decided I will not initiate a position.

While K has a plan to improve business results, I think K is priced to perfection. Investors appear to already be pricing in the projected improvements.

Furthermore, my Stock Picking Rules to Follow includes buying best of breed. K does not strike me as a company that meets this criterion.

I am reminded of Andrew Carnegie’s adage that:

“The concerns which fail are those which have scattered their capital, which means that they have scattered their brains also. They have investments in this, or that, or the other, here, there and everywhere. “Don’t put all your eggs in one basket” is all wrong. I tell you “put all your eggs in one basket, and then watch that basket.”

Look round you and take notice; men who do that do not often fail. It is easy to watch and carry the one basket. It is trying to carry too many baskets that break most eggs in this country. He who carries three baskets must put one on his head, which is apt to tumble and trip him up. One fault of the American businessman is lack of concentration.”

K is not another basket I need to carry.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I do not own K and have no intention of acquiring K in the foreseeable future.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.