Summary

Summary

- This FedEx Stock Analysis is based on Q3 FY2016 financial results and outlook for the remainder of FY2017.

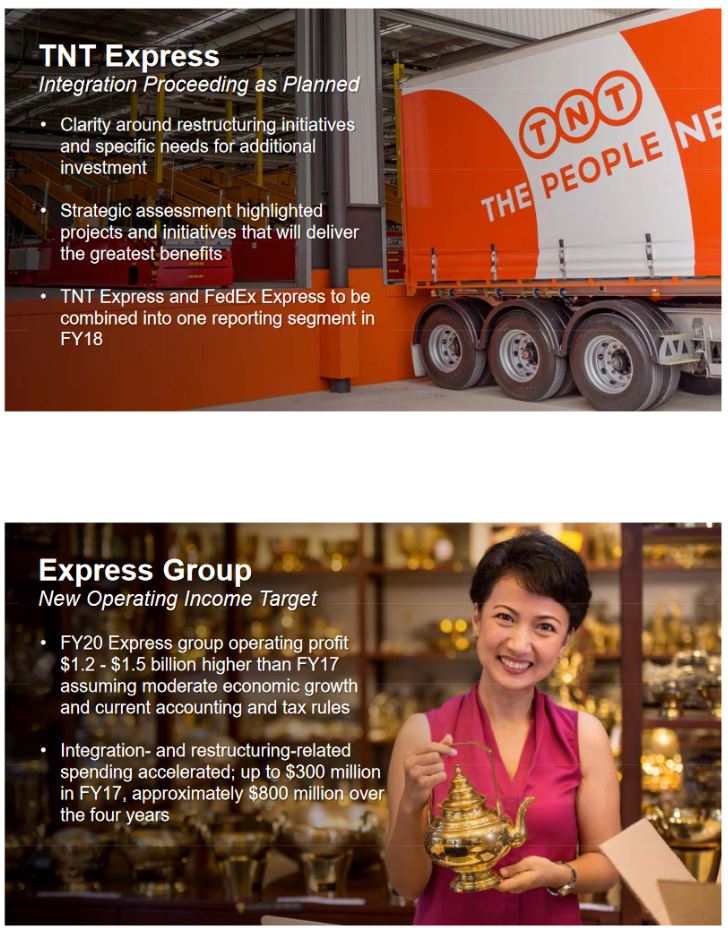

- The integration of TNT is proceeding as planned but management has accelerated the implementation of activities which were to have taken place later in the integration process.

- FedEx shares have increased dramatically in recent months but based on projected earnings they still offer some value.

- I foolishly had short-term thinking when I first owned FDX in 1999. I do not intend to repeat the same mistake.

Introduction

In early February 2017, a reader responded to my UPS – It Is Now In My “Buy Zone” post asking if I could provide my comments on FedEx (NYSE: FDX). Now is an opportune time to do so given the March 21, 2017 release of FDX’s Q3 2017 results, forecast for the remainder of the current fiscal year, and update on the TNT integration.

My Experience as a Short-Term FDX Investor

In late 1999, I acquired a few hundred shares of FDX. I do not recall the specific date of my purchase but I remember my purchase price was in the low $40s. My rationale for acquiring shares in FDX was based on the premise that somebody would have to ship all the goods being purchased online.

Shortly subsequent to my purchase, I exited my position when FDX climbed into the upper $40s. I thought I was an astute investor as I had generated a small profit!

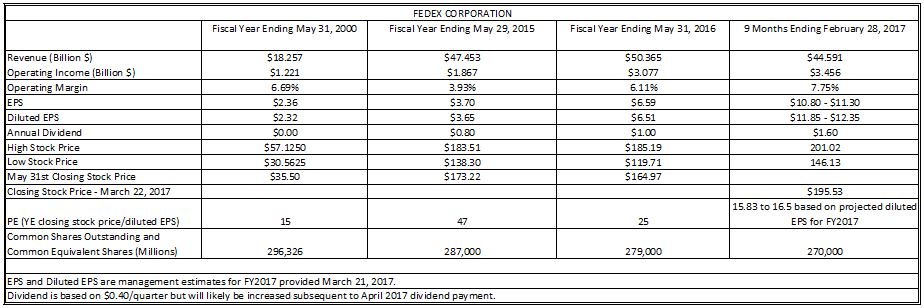

The following chart compares FDX’s results in FY2000, FY 2015, FY 2016, and Q3 2017.

FDX – Select Data for 2000 2015 2016 2017

Clearly, I left a lot of money on the table.

TNT Integration

FDX acquired TNT in May 2016. This integration is a massive undertaking and FDX expects to have it completed mid-2020, 4 years after the date of acquisition.

In the March 21, 2017 conference call which accompanied the Q3 2017 earnings release, management indicated that in the 9 months following the close of acquisition, it realized the TNT business it acquired was severely under-invested, particularly in IT and in operations. As a result, management has made strategic investment decisions which I touch upon in the next section of this post.

The combination of the TNT and FDX businesses is now more than just an integration of the two entities. FDX is taking measures to leverage the combined businesses to be transformative and fully expects significant synergies from the integration.

FDX – TNT Integration – March 21 2017 presentation

As the integration progresses, businesses are combined and countries are fully integrated. Discrete financial information about the legacy business, therefore, will no longer exist on a comparable basis. Beginning in FY2018, the TNT segment will be eliminated and will be reported under the FedEx Express segment.

FDX – TNT Integration Accomplishments to Date and Up Next

Q3 FY2016 Financial Results and Outlook for Remainder of FY2017

On March 21, 2017, FDX presented its Q3 2017 financial review and outlook along with an update on the TNT integration.

Management indicated it is targeting a $1.2B – $1.5B operating income improvement at the FedEx Express Group in fiscal 2020 versus the final FY2017 adjusted results. This assumes moderate income economic growth and current accounting and tax rules. FDX expects to lower the effective tax rate to around 33% to 34% with the completion of the integration.

The pace of the integration activities in FY2017 and preparations for FY2018 requires higher levels of dedicated integration personnel training, professional fees to support the integration, and investments in IT and operations.

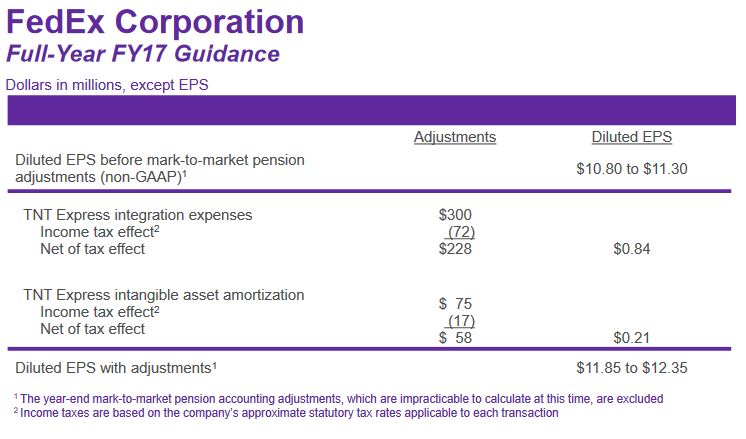

As a result, FDX is increasing FY2017’s forecast for integration and restructuring related spending by $50 – $300 million. This is a result of the acceleration of activities which were previously planned for later in the 4 year integration plan.

The aggregate integration expense over 4 years is now projected to be approximately $800 million. Management has cautioned that the actual timing and amounts of these integration-related estimates are subject to change as it implements and adjusts its integration plans.

Valuation

While earnings estimates are provided as far as 2020, I place little credence in earnings estimates several years into the future. I am, therefore, relying on estimates for FY2018 to determine what would be a reasonable price to pay for FDX; these estimates are less subjective.

I arrive at a trailing PE of 30 when I use FY2016’s diluted EPS of $6.51 and the current stock price of $195.53 as at close of business March 22, 2017.

If I use the current stock price, the $11.85 – $12.35 projected diluted EPS for FY2017 found on page 18 of management’s March 21, 2017 presentation, and the estimates from multiple analysts, I estimate a forward PE range of 15.8 – 16.5.

FDX – Q3 2017 Earnings Review – March 21 2017

FDX – TD WebBroker annual EPS estimates

FDX – ValuEngine annual EPS estimates

FDX – Thomson Reuters – annual EPS estimates

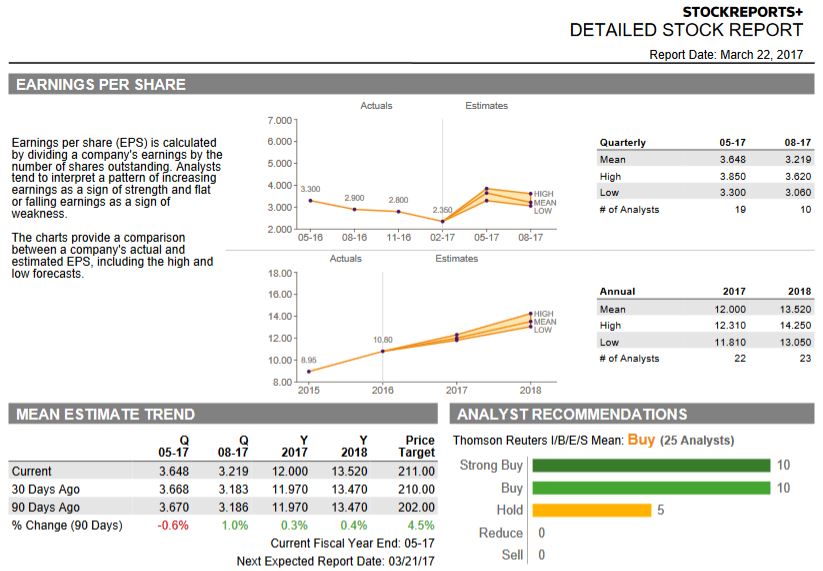

The current mean estimates reflect a 2018 EPS range of $13.05 – $14.25 with $13.65 being the midpoint.

If I use a mid-point PE of 16.15 and the projected mean FY2018 EPS of $13.65, I anticipate FDX will likely be trading around $220 at some stage of FY2018.

FDX’s dividend yield is a negligible sub 1% and is not a factor in my FDX analysis. While I do enjoy receiving an ongoing dividend income stream, there are reasons why Low or No Dividend Yield Companies Belong In Your Portfolio.

Final Thoughts

FDX meets all my Stock Picking Rules to Follow.

I am confident FDX will successfully integrate TNT in the 4 year timeframe it set for itself. Once the integration is complete I envision FDX will be significantly more expensive than current levels.

I intend to initiate a position shortly and subsequent purchases will also be likely. This time I am looking at FDX from a long-term perspective.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I currently have no position in FDX but may initiate a long position within the next 72 hours.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.