Summary

Summary

- This MasterCard stock analysis is based on Q2 2017 results released July 27, 2017.

- MA’s projected EPS for FY 2017 and FY 2018 from multiple analysts have been revised upward subsequent to my February 1, 2017 post.

- MA recently received a favorable ruling from the Competition Appeal Tribunal (CAT) and no longer faces the $18B British Class Action Suit filed against it.

- While MA’s dividend yield is currently sub 1% I expect dividend income and capital gains will yield a high single digit or a low double digit return over the long-term.

- MA and VISA are two stocks I will never sell.

Introduction

On February 1, 2017 I wrote that MasterCard (NYSE: MA) was expensive but worth the price and on January 12, 2017 I wrote that I would never sell my VISA (NYSE: V) holding. Some readers cautioned me that never is a very long time and that I should not get “married” to a stock. In general, I am in total agreement. In the case of V, and now M, I view these two stocks as being pretty darn close to the “marrying” kind. Sure, I strongly suspect both stocks will experience a drop in price from current levels at some stage of the game but in all likelihood, a drop in price will most likely present a buying opportunity.

While MA is certainly not on sale at current levels I recently decided to acquire shares for the FFJ Portfolio. Ultimately, I would like the investments in the portfolio to be transferred to the next generation. Hopefully I will remain in good health and this transfer will need not occur sooner than 20 years from now.

Recent Events

Subsequent to my previous MA post, MA:

- announced in late April 2017 the completion of its $0.92B acquisition of Vocalink, a leader in bank account-based payments;

- unveiled the next-generation biometric card in April 2017;

- announced on July 17, 2017 that it had entered into an agreement to acquire Brighterion, Inc., a leading software company specializing in artificial intelligence. This acquisition will further expand its suite of capabilities that deliver an enhanced customer experience and security.

- received a favorable ruling from the Competition Appeal Tribunal (CAT), a newly-empowered court that oversees Britain’s fledgling class action regime, ruled that it would not grant the necessary collective proceedings order for the $18B British Class Action Suit against MA to proceed to trial.

Q2 2017 Financial Results

Readers are encouraged to review the details of MA’s July 27, 2017 Q2 Earnings release. Highlights from the analyst conference call are provided below.

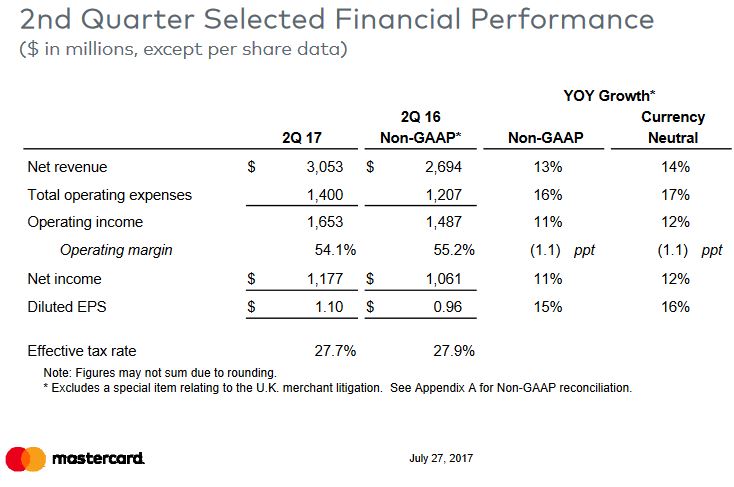

Q2 2017 Selected Financial Performance

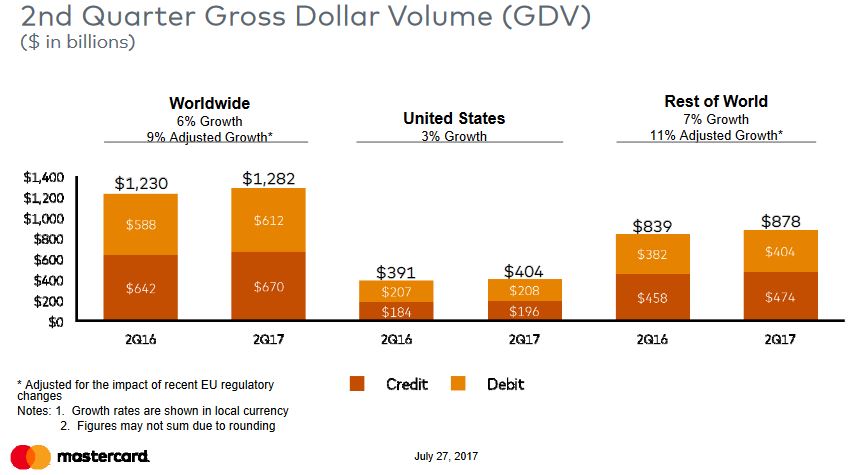

Q2 2017 Gross Dollar Volume

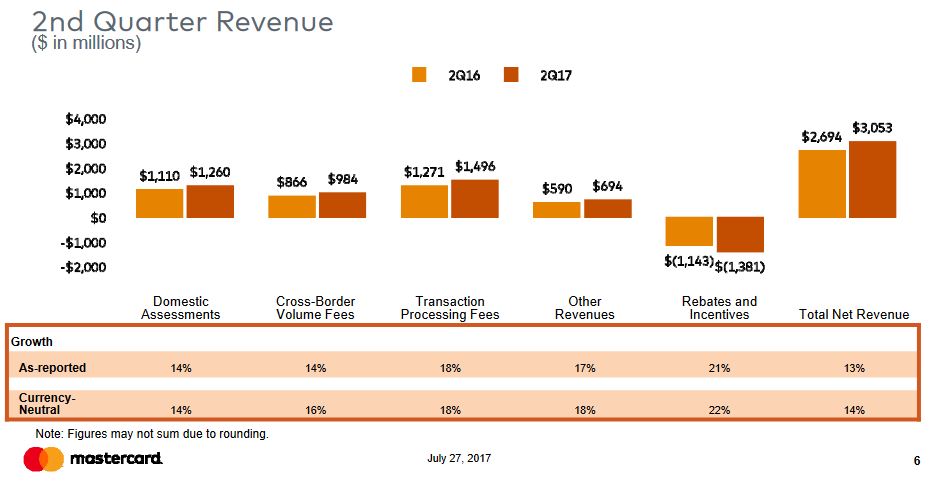

Q2 2017 Revenue

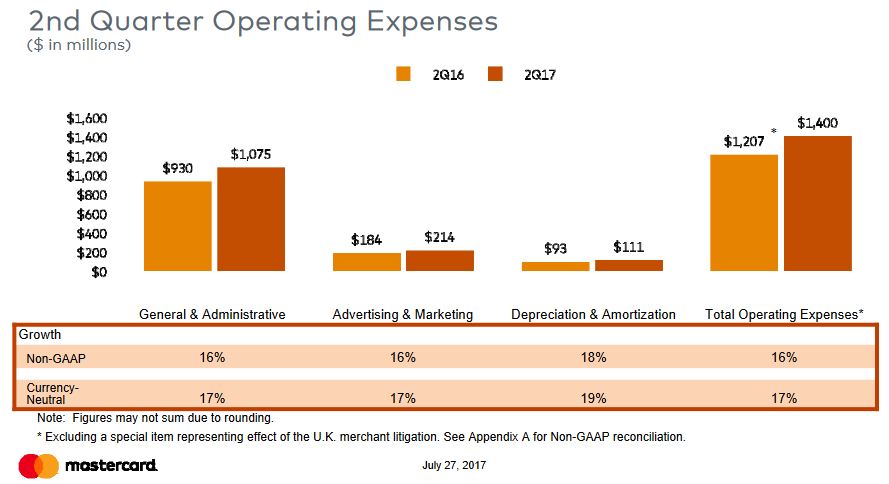

Q2 2017 Operating Expenses

While Great Britain’s decision to leave the European Union has hammered the British Pound, MA has benefited in that it has experienced higher transactions in the UK. The weaker currency helped drive customer spending as retail sales grew 5% in the three months ending June 30th; MA’s cards account for roughly 28% of all transactions.

In Q2, MA and Britain’s largest digital bank (TSB Bank plc which is part of the Banco de Sabadell Spanish banking group as of June 30, 2015), jointly announced a 7 year agreement commencing in 2018 wherein MA will replace V as TSB’s debit-card provider. In addition, TSB will continue to issue MA credit cards over the same term. This agreement is significant for MA in that TSB’s customers make up about 4% of all debit-card users in the UK.

Outlook for Remainder of Fiscal 2017

On the recent Q2 conference call, management indicated the underlying business fundamentals remain strong with growth expected to continue to come from a combination of new and renewed agreements as well as its expanded set of service offerings.

Progress has been made in the first 6 months of FY2017 in Europe and in Latin America and the forecast is for this momentum to continue.

FX headwinds are expected to subside primarily due to the weakening of the USD.

Net revenue for the year is expected to grow at a low double-digit YoY rate on a currency neutral basis excluding acquisitions.

YoY total operating expenses are expected to continue to grow in the high single digit range excluding acquisition and special items.

MA continues to see growth in its commercial business. This growth is driven by a combination of innovation and some new deals.

MA recently announced the launch of the MasterCard B2B Hub. This is an innovative solution that enables small and medium-size businesses in the US to automate their invoice and payment processes.

In the US, more than 50% of all B2B payments are still made via cheques. The intent is to integrate this with more than MA’s 130 accounting and back-office systems and also into inControl, MA’s virtual card platform. This solution would help buyers and suppliers become more efficient and would reduce the cost associated with manual payment processes.

Prior to retirement I was employed by a major Canadian financial institution and headed up a Corporate Cash Management sales team. One of the services we sold was VISA Payables Automation, V’s offering tailored for companies with significant annual spend. Spoken from experience, the volume of transactions and the dollar value processed through this offering is significant. As MA’s and V’s B2B solutions become more widely accepted by businesses, I foresee a dramatic increase in payment volumes through these networks which bodes well for both company’s shareholders.

MA is expanding its global partnership with Amadeus IT Group SA in the US with U.S. Bank as Amadeus’ exclusive issuer. This is part of MA’s strategy to pursue $300B+ in annual global payments that travel agencies make to airlines, hotels, and other travel providers; these payments are currently largely made via bank transfers and cheques.

Dividend

MA’s dividend history can be found here. On August 8, 2017, MA will distribute its third consecutive $0.22 quarterly dividend. If history is any indication of what can reasonably be expected in the future, I suspect MA will pay another $0.22 dividend in early November 2017 and the February 2018 dividend will probably be increased $0.03 – $0.05 per share. Using this projected increase and MA’s current stock price of $127.91 would still result in a sub 1% dividend yield.

Some investors will shy away from investing in MA because their primary focus is to generate dividend income and MA’s dividend yield will not meet their minimum dividend yield requirement. In my case, I am retired and have no intention of starting to collect a government pension for another 14 years. I also have absolutely no intention of EVER returning to the workforce, and therefore, I will be relying on dividend and rental income for several years. Despite this, I will not invest exclusively on the basis of dividend yield for the following reasons:

- I find that a company paying a juicy dividend yield generally carries an unacceptable level of risk.

- I have invested in a few companies whose stock has a very low dividend yield. Despite this, these companies have grown their dividends dramatically over the years. The steady dividend increases and dramatic rise in stock price has compensated us nicely for having had the intestinal fortitude not to chase yield but rather to look at the underlying long-term dividend AND capital gains growth potential.

In a nutshell, a well structured equities portfolio will consist of investments in companies with both low and moderate dividend yields. My suspicion is that MA will yield a high single digit or a low double digit return over my investment time horizon.

Share Repurchases

When I am prepared to sacrifice dividend yield, I look for a strong probability that I will be compensated from a capital gains perspective. I preferably like it when capital gains are generated through extraordinary results achieved through normal business operations. I do not complain, however, when management views its company’s shares to be undervalued and makes it a point to significantly and steadily reduce the number of outstanding shares.

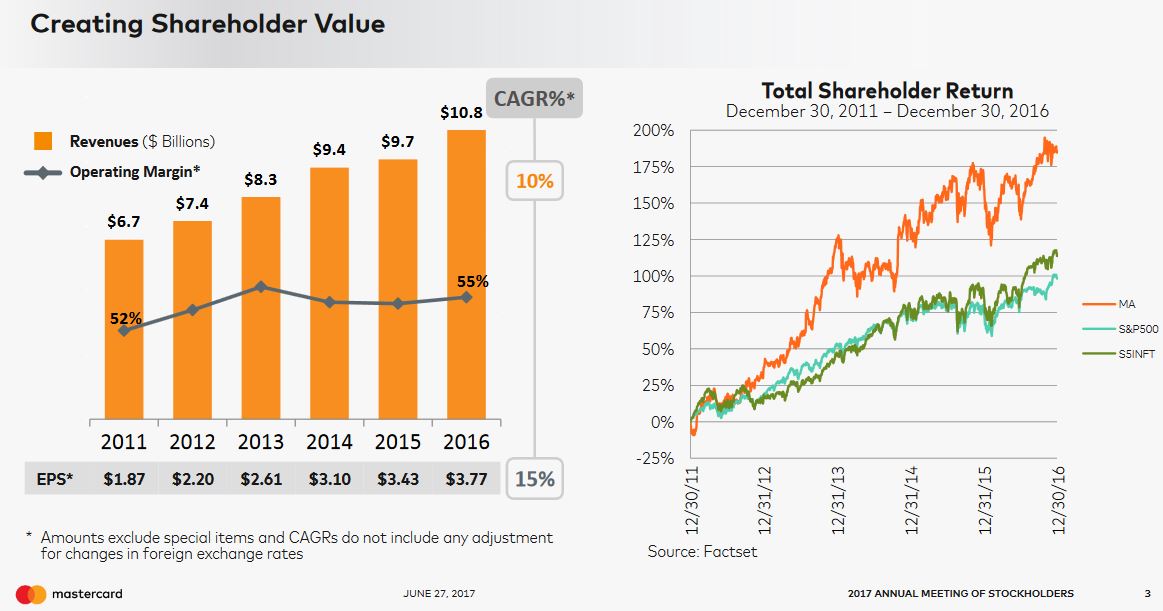

Creating Shareholder Value – June 27, 2017 Annual Meeting of Shareholders

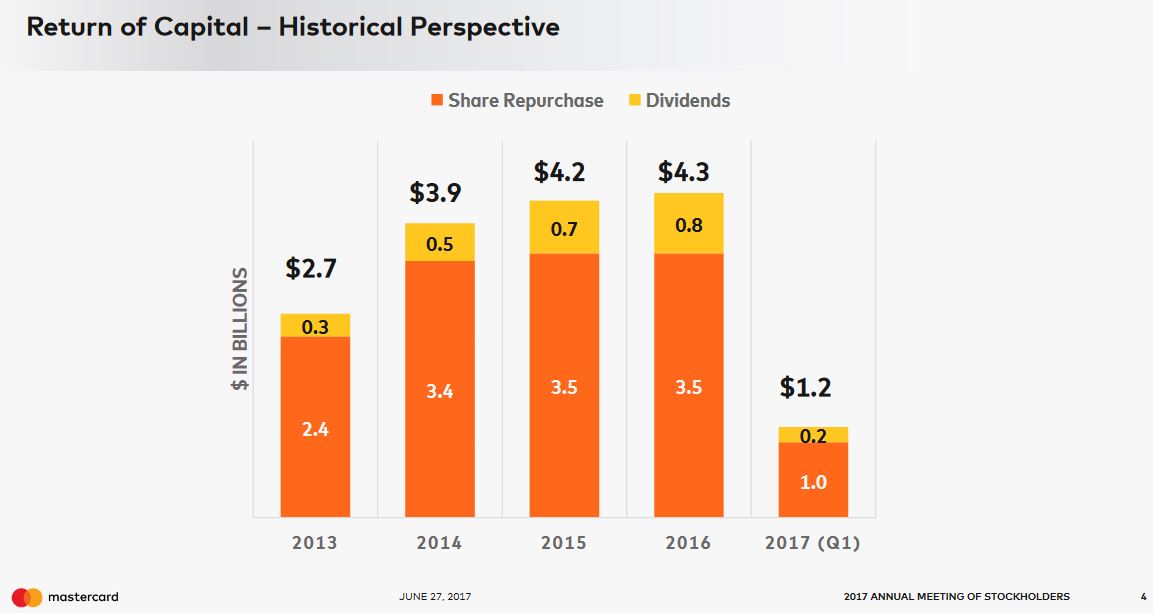

Return of Capital Historical Perspective – June 27, 2017 Annual Meeting of Shareholders

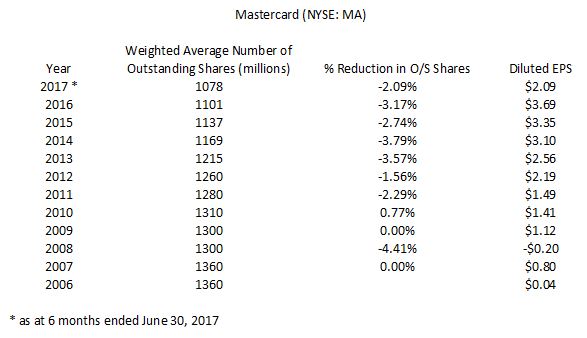

In MA’s case, the diluted weighted average number of shares outstanding has dropped considerably subsequent to its May 25, 2006 IPO; the following chart takes into consideration the January 22, 2014 10 for 1 stock split.

Weighted Avg No of OS Shares and Diluted EPS 2006 – 2017

I suspect MA may become more aggressive with its stock repurchase program given the Competition Appeal Tribunal’s recent ruling that it would not grant the necessary collective proceedings order for the $18B British Class Action Suit against MA to proceed to trial.

Valuation

If an investor has a hard and fast rule that an investment in a company will only be made when a company’s shares have a sub 20 PE ratio, I suspect this investor is highly unlikely to ever own MA shares. Even if we get a long overdue market correction, I suspect MA’s PE may only retrace to a level in the low 20s.

In my February 1, 2017 post I indicated I was prepared to pay up to acquire MA shares. When that post was written, the consensus 2017 EPS expectation from 32 brokers was $4.27 and 30 brokers projected EPS of $4.98 for FY2018. These estimates have subsequently been revised to $4.38 and $5.09.

Source: TD WebBroker – MA EPS Consensus Expectations July 28 2017

Using the July 28, 2017 closing price of $127.91 and the projected $4.38 EPS for FY2017, I get a forward PE of 29.20 which is a shade lower than when I wrote my February 1, 2017 post. MA is certainly not trading at a “bargain” level but if you have a long-term investment time horizon, I think you can do far worse than purchasing MA at current levels.

MasterCard Stock Analysis – Final Thoughts

I want to benefit from the ever increasing transition from cash to other methods of payment. Secondly, inflation will naturally result in most goods and services trading hands at higher price points which will benefit MA. Furthermore, I don’t want to miss out when merchants and consumers switch from MA to V or vice versa. This is why it is imperative that I own shares in both companies.

Given that MA and V are the two dominant publicly traded companies in their industry I feel no need to own shares in American Express Company (NYSE: AXP) or Discover Financial Services (NYSE: DFS). If China UnionPay were publicly traded, however, I would very likely acquire shares in this company because it is a dominant player in the Far East region of the globe.

MA is certainly not on sale at current levels but I am not concerned. This is why I recently acquired another 400 shares. Unlike the other MA shares we already own, these newly acquired shares will be held in the FFJ Portfolio.

Note: I sincerely appreciate the time you took to read this post. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long MA.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.