![]()

Hormel Foods Corporation (HRL) is a member of the exclusive group of Dividend Kings (dividend increases for at least 50 consecutive years). This article looks at valuation based on Q1 2019 results and FY2019 guidance.

Summary

- Hormel Foods has just released Q1 2019 results and has reaffirmed FY2019 guidance of $1.77 – $1.91 per share.

- Following a Goodwill write-down in Q4 2018 resulting from the deterioration in the CytoSport business which was acquired in FY2014, HRL has entered into a definitive agreement to sell this business to PepsiCo.

- HRL is seeing the benefits from its long-term strategy to move its portfolio away from low margin commodities to higher margin branded value added products.

- HRL will not appeal to growth inclined investors but may appeal to value investors.

Introduction

Investors seeking to invest in ‘Value’ companies may find Hormel Foods Corp. (HRL) to be an attractive long-term investment. Founded in 1891, this Consumer Goods company has a suite of well known brands; HRL’s brands have a #1 or #2 marketshare in over 40 categories which is an increase from 35 a year ago.

HRL is a member of the highly exclusive ‘Dividend King’ group of companies. These are companies which have increased their dividend for at least 50 consecutive years.

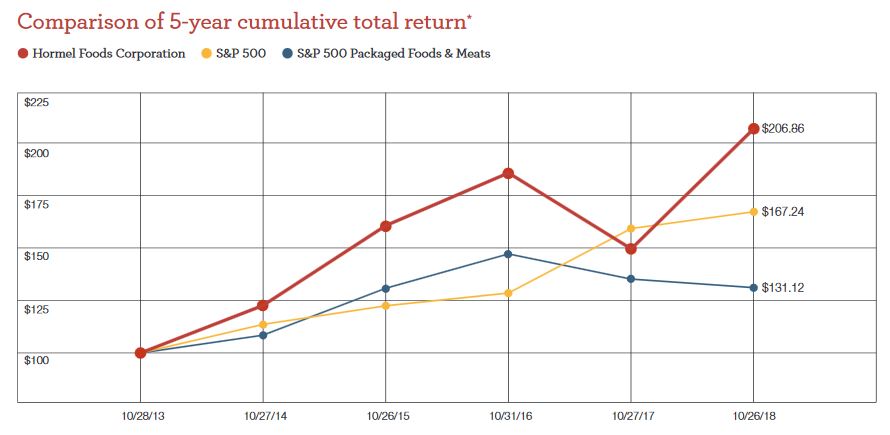

In addition to a steadily increasing dividend, we see that HRL’s 5 year cumulative return (October 2013 – October 2018) exceeds a couple of indices.

Source: HRL – 2018 Annual Report (page 12 of 99)

If you view a 5 year timeframe as too short in which to properly assess a company’s performance, let’s have a look at 10 years.

How about 15 years?

Source: TickerTech

HRL certainly has rewarded shareholders over the long-term. I still, however, like to see whether I am acquiring shares when they are fairly valued. Far too often I have seen investors acquire shares in a company when shares are trading at a lofty valuation because they look at a company’s historical track record and think what happened in the past will be replicated in the future.

I have provided examples on this matter in previous articles and once again suggest you look at how Cisco (CSCO) and Intel (INTC) shareholders have fared depending on when shares were acquired.

I acquired CSCO shares at an average cost of just under $20. Had I acquired CSCO shares in 1999 – early 2000 my investment experience with CSCO would be entirely different from that I have experienced.

When I acquired HRL shares in June 2017 I wrote that I viewed HRL as being attractively valued. I was of the same opinion when I wrote my November 2017, February 2018, and May 2018 articles.

My sentiment changed slightly when I wrote my August 28, 2018 article. In that article I indicated I was of the opinion HRL was fairly valued versus attractively valued.

By the time I wrote my November 20, 2018 article I was of the opinion HRL (trading at $44.50) did not warrant its current valuation. My ‘Final Thoughts’ in that article were:

‘My modus operandi is such that I buy and hold shares for the long-term and very rarely do I sell shares….even though they may be slightly overvalued.

I have sufficient exposure to HRL (shares are held in the FFJ Portfolio) but if this were not the case I still would not acquire shares at the current valuation. I would patiently wait for Mr. Market to sour on HRL to the point where shares retrace to sub $39.’

We now have Q1 2019 results released on February 21, 2019 and a reaffirmation of full-year diluted EPS guidance of $1.77 – $1.91 per share ($1.84 mid-point).

Interestingly, just a couple of days before the release of Q1 results, HRL announced that it had entered into a definitive agreement to sell its CytoSport business to PepsiCo, Inc. (PEP); PEP has been a long-standing distribution partner for CytoSport which puts them in a strong position to grow this business. Closing of this transaction is expected to occur in Q2.

In my November 20, 2018 article I indicated that HRL had recorded a $17.279 million non-cash impairment charge associated with the CytoSport business it acquired in August 2014 for $0.45B; CytoSport was generating annual sales of $0.37B.

This acquisition was to serve as a growth catalyst for HRL’s Specialty Foods segment and to help expand HRL’s offerings of portable, immediate, protein-rich foods.

Fast forward to FY2018, however, and with $0.3B in annual sales it is clear this acquisition did not go as planned. In my November 20, 2018 article I indicated ‘this goes to show how growth by acquisition can be risky.’

Fortunately, HRL will extricate itself from CytoSport with the business to be sold for $0.465B which is $15 million higher than the purchase price. When you factor in all the costs associated with this acquisition, the time value of money, and the opportunity cost of having had money tied up in this business for ~4.5 years, this acquisition has been a destruction of shareholder value.

With the release of HRL’s Q1 2019 results and a pull back in the share price from ~$46 reached in November 2018 to $41.86, let’s have a look at whether HRL presents an attractive buying opportunity for investors seeking steady dividend growth and, for the most part, relatively minor fluctuations in the stock price.

Q1 2019 Financial Results and FY2019 Guidance

HRL’s Q1 2019 Earnings release can be accessed here.

HRL delivered $0.44 EPS which is a 21% decline compared to Q1 2018. Last year’s results, however, included a large one-time benefit from the Tax Cuts and Jobs Act.

Management has indicated that its well-developed strategy of shifting its brand mix toward branded, value-added products in the domestic and international businesses more than offset significant declines in the commodity businesses; HRL continues to intentionally transition its portfolio away from commodity products and the associated earnings volatility.

Results are promising in the deli, foodservice and China businesses but the fundamentals in the turkey industry, while improving, will very likely result in Jennie-O Turkey Store falling short of full-year expectations due to a lower retail sales outlook.

Full-year net sales guidance is $9.7B – $10.2B (FY2018 was $9.546B) and full-year diluted EPS guidance is $1.77 – $1.91/share ($1.84 mid-point).

Credit Ratings

HRL’s credit ratings remain unchanged from those reflected in my previous articles. Moody’s rates HRL’s senior unsecured debt A1 (top tier in the upper medium grade category) and S&P Global Ratings continues to assign an A rating (middle tier in the upper medium grade category).

Both ratings should be satisfactory for a conservative investor.

Valuation

At the time of my August 28th article, HRL was trading at $37.94/share and its forward PE was ~19.4 – ~20.96 based on EPS guidance. This was higher than the ~18.2 – ~19.6 range at the time of my May 24th article and the ~16.9 – ~18.2 range at the time of my February 22nd article.

In my August 28th article I indicated that if we took the $1.88 mid-point of the EPS guidance of $1.81 – $1.95 and estimated a 6% growth in earnings for FY2019, we could expect HRL to generate EPS of ~$2. Using the $37.94 stock price at the time of that article we arrived at a forward PE of ~19.

By the time of my November 20th article, HRL was trading at ~$44.50 and it had just reported FY2018 diluted EPS of $1.86 thus resulting in a diluted PE of ~23.93. This valuation was well in excess of HRL’s valuation at the time of my previous article; Mr. Market had bid up HRL’s stock price by over $6.50/share within less than 3 months.

Guidance at the time of that article was $1.77 – $1.91 and using the $1.84 mid-point and HRL trading at ~$44.50, the forward diluted PE was ~24.18.

Now, with the release of Q1 2019 results, FY2019 guidance remaining at $1.77 – $1.91 ($1.84 mid-point), and a current stock price of ~$41.86 we get a forward diluted PE of ~22.75; this compares favorably with HRL’s 5 year average PE of ~23.6.

Dividend and Dividend Yield

HRL’s dividend and stock split histories can be found here.

On November 19th, HRL announced a 12% dividend increase ($0.1875/share/quarter increased to $0.21/share/quarter).

At the time of my August 28th article, HRL’s dividend yield was 1.98%. When I wrote my November 20th article and HRL was trading at ~$44.50, the new $0.84/share annual dividend yielded ~1.89%.

With HRL now trading at ~$41.86, the $0.84 annual dividend provides investors with a ~2% dividend yield. This is certainly not great but at least you know that with a ~45.7% dividend payout ratio ($0.84/$1.84 projected diluted EPS for FY2019) a dividend cut surprise is unlikely.

Options

At the time of my November 20, 2018 article I looked at the possibility of writing out of the money covered calls to generate additional income. I ended up passing because the potential option income was negligible.

This continues to be the case and I will not be entering into any conservative covered call option trade.

Final Thoughts

I acquired HRL shares because I:

- expected HRL to continue to increase its dividend on an annual basis;

- was optimistic the share price would remain low enough so the dividend income could acquire a few more shares quarterly via automatic dividend reinvestment;

- anticipate a very reasonable quarterly dividend in another 15+ years.

This certainly has not been my most rewarding investment from a total return perspective. I am, however, satisfied with my HRL exposure and intend to make no changes.

If you are an investor seeking steady dividend growth and a low probability of a significant drop in a company’s stock price (barring another Financial Crisis type event) then HRL could be a suitable investment for you.

I view shares as fairly valued but am of the opinion a broad market pullback within the next few months is a very real possibility. If I were interested in acquiring more HRL shares I would patiently wait for such a pullback. If you do, however, decide you want to acquire HRL shares at the current valuation I see no reason why you would not be well rewarded over the long-term.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long HRL.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.