Summary

- This post addresses YTD changes and changes expected to occur within the next 4 – 6 weeks in the FFJ Portfolio.

- We have been able to transfer shares to the FFJ Portfolio as a result of a recent review of our long-term cash flow requirements.

- I anticipate a significant inflow of funds within the next 4 – 6 weeks and have compiled a list of potential investments.

Introduction

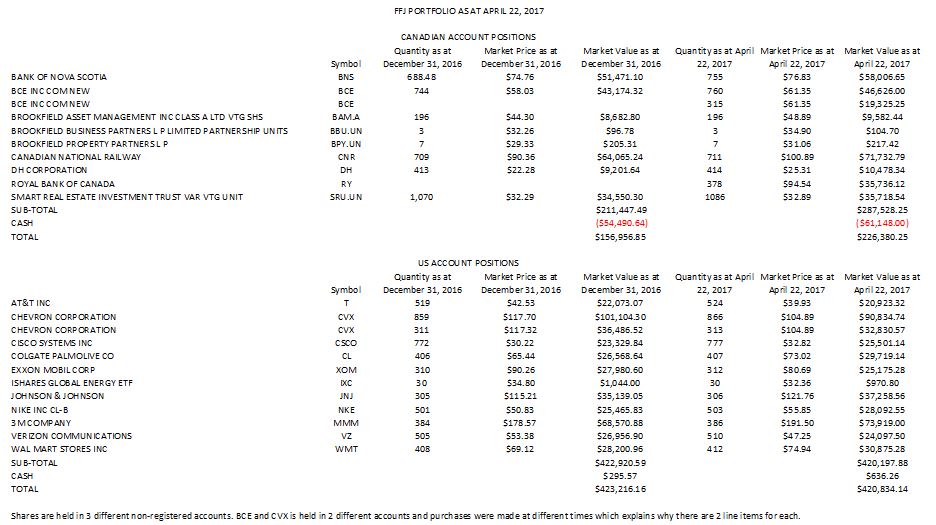

In early January 2017 I launched Financial Freedom is a Journey (FFJ) Portfolio. The following chart reflects our current holdings and our holdings as at inception on December 31, 2016.

FFJ Portfolio as at April 22 2017

Recently, we undertook a further review of our future cash flow requirements. Based on our forecast, we elected to transfer additional BCE Inc. (NYSE: BCE) shares to the FFJ Portfolio as well as Royal Bank of Canada (NYSE: RY) shares; we own the TSX listed shares. The reasoning for these transfers is that we do not foresee a need for the funds held in these shares at any stage in the future.

This was not meant to be an active portfolio. As a result, minimal activity has been evidenced subsequent to its inception. We have solely reinvested all dividends and we have acquired an additional CDN $590 in The Bank of Nova Scotia (NYSE: BNS) shares every 2 weeks. Within the past few days, we have terminated the acquisition of additional BNS shares since we have more than ample exposure to this bank on an overall portfolio basis.

While the level of activity has been minimal to date, the level of activity will increase marginally over the next couple of months.

Anticipated Inflows

DH Corp (TSX: DH)

On March 13, 2017, DH Corporation, a leading provider of technology solutions to financial institutions globally, and Vista Equity Partners (“Vista”) announced they had entered into a definitive arrangement agreement under which Vista will acquire all of the outstanding shares of DH Corporation for CDN $25.50/share in cash including the assumption of all debt obligations including the issued convertible debentures, for a total enterprise value of approximately $4.8 billion.

While the purchase price is less than the average cost of our DH shares held in the FFJ Portfolio, we hold another 1256 shares in another account at an average cost of CDN $18.892. As a result, we are coming out ahead overall on our DH investment.

No definitive date has been announced re: closing but on May 16, 2017, a Debenture holder meeting is to be held as well as a Special Meeting of Shareholders.

Once the acquisition has been completed, the FFJ Portfolio will receive $10,557 (414 shares x $25.50/share) for redeployment.

Commuted Value of Defined Benefit Pension Plan (DB)

Recently, my wife and I met with our investment adviser to review the material provided by my former employer regarding the DB. Based on our analysis, we have elected to take the commuted value of the DB and I will manage these funds. This decision has been made taking into consideration the income we expect to receive once our Registered Retirement Savings Plans (RRSPs) are converted to Registered Retirement Income Funds (RRIFs) plus the projected Canada Pension Plan (CPP) and Old Age Security (OAS) payments we will start collecting at age 71 (15 and 17 years from now).

While funds from the DB will form part of the FFJ Portfolio, they must be held in a separate locked-in RRSP; the current holdings are held in non-registered accounts.

A benefit of holding US shares in a registered account is that all dividends received are not subject to a 15% withholding tax. Currently, all US listed holdings in the FFJ Portfolio are held in non-registered accounts and are subject to this withholding tax.

In addition to the DB component which must be invested in a locked-in RRSP, I will receive a cash component (the Federal government will also receive its cut!). The cash component may be used to reduce the leverage exposure but I may elect to do otherwise.

Receipt of these DB funds is anticipated within the next 4 – 6 weeks.

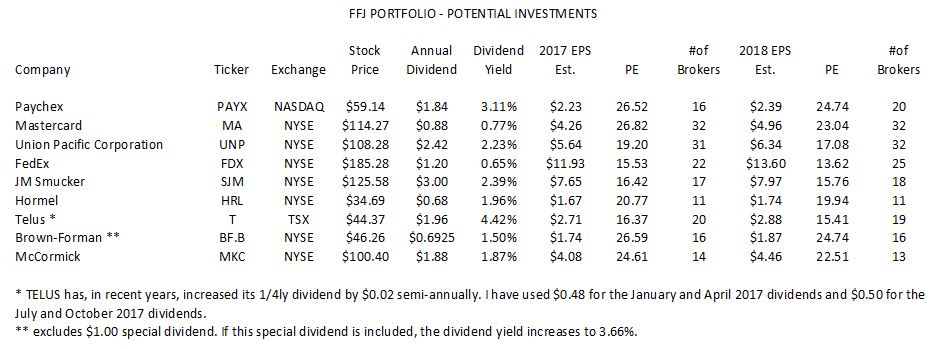

Potential Investments

The following is a small subset of the list of companies in which I would be interested in initiating a position and/or increasing our exposure.

FFJ Portfolio – Potential Investments

Paychex, Inc. (NASDAQ: PAYX)

Recently I had to liquidate our PAYX shares which were held in a Registered Education Savings Plan (RESP) established for the purpose of funding our daughter’s college education. I like PAYX and regret having had to liquidate these shares. There are, however, multiple conditions which must be satisfied regarding the use of funds held in a RESP. One of these conditions is that all funds must be used to fund education related expenses. Any funds remaining in an RESP would result in us having to return some grant money to the Federal Government.

Our experience in owning PAYX was positive. Our average cost per share, including all reinvested dividends, amounted to $31.406 and our selling price was $58.05.

I fully intend to re-acquire PAYX shares upon receipt of my DB proceeds.

PAYX’s historical PE ratios can be found here and its dividend track record can be found here.

Here is a link to a PAYX post I wrote in December 2016.

Mastercard Inc. (NYSE: MA)

MA and VISA (NYSE: V) are wonderful companies that definitely fall into my “hold forever” category. We already own a few thousand V shares but I definitely need to increase our MA exposure.

MA is rarely on sale (refer historical PE ratios here). Its dividend track record can be found here.

Here is a link to a MA post I wrote in February 2017.

Union Pacific Corporation (NYSE: UNP)

Warren Buffett explained the purchase of BNSF in an interview with Charlie Rose on April 1, 2011. Many of his comments are applicable to the rail industry in general. If the rail industry is good enough for Buffett and Munger, it is certainly good enough for me.

We currently own several hundred shares of Canadian National Railway (NYSE: CNI) within the FFJ Portfolio. I would like to expand our exposure to this industry hence the reason UNP is on my “wish” list.

Its historical PE ratios can be found here and its dividend track record can be found here.

I previously wrote a post about UNP in January 2017. I still think it is slightly expensive at current levels.

FedEx Corporation (NYSE: FDX)

In March 2017 I wrote a post about FDX and initiated a position. We now hold shares in FDX and United Parcel Service (NYSE: UPS). In hindsight, I should have never sold my FDX position several years ago simply because I wanted to capture a quick profit. If I gained anything from my early FDX experience, it was that short-term thinking is not the road to building long-term sustainable wealth.

The chart at the beginning of this post reflects a $1.20 annual dividend. I anticipate FDX’s dividend will increase with the dividend payable the beginning of July 2017.

FDX’s historical and current PE ratios can be found here.

Once again, FDX is not on sale but my investment time horizon is such that I am not going to quibble about a few dollars.

J. M. Smucker Company (NYSE: SJM)

I consume enough BICK’s pickles and Smucker’s jams that it is high time SJM start thanking me by way of quarterly dividend payments. I have no idea if/when there will be an economic downturn but when I look at SJM’s brands, they all strike me as brands that will continue to be purchased even if consumers have to reign in their spending to some extent.

Its historical PE ratios can be found here and its dividend track record can be found here.

Hormel Foods Corporation (NYSE: HRL)

HRL has never been on my radar screen until it was brought to my attention by The Financial Canadian. In hindsight, HRL would have been an extremely valuable addition to our investment holdings as it has outperformed the S&P500 by a wide margin over an extended period of time.

Some of you may associate HRL with SPAM. I certainly did and this is perhaps the reason why I never looked into HRL any further. From a very early age I always felt SPAM was not fit for human consumption. Over the years, however, their brand portfolio has expanded dramatically.

In conjunction with their consistent growth over the years, HRL has aptly rewarded its shareholders with a steadily increasing stream of dividends. In fact, HRL has increased its annual dividend for 51 consecutive years thus qualifying it to be a “Dividend Kings” member. This a group of 19 companies with 50+ years of consecutive dividend increases.

HRL is currently attractively valued from a PE perspective.

TELUS Corporation (TSX: T or NYSE: TU)

We have owned AT&T (NYSE: T), Verizon (NYSE: VZ), and BCE (TSX: BCE) for quite some time. I view the telecommunications industry to be reasonably attractive from a long-term investment perspective. I was looking to expand our exposure in this space and wrote a post explaining my rationale as to why I thought TELUS was attractively valued. Based on my analysis, I initiated a position earlier in April 2017 and I am looking to add to this position.

TELUS’ dividend history can be found here and its historical PE levels can be found here.

I plan to attend TELUS’ annual general meeting (AGM) on May 11th in Toronto.

Brown-Forman Corporation (NYSE: BF.B)

I previously wrote about BF.B. While I was not totally enamored with its recent results, I must admit I like the liquor business. We have owned Diageo plc (NYSE: DEO) for years and have been rewarded handsomely despite getting slammed with an onerous withholding tax…even when held within a Registered Retirement Savings Plan.

I would like to diversify our “distillers and wineries” holdings and Brown-Forman seems to be a logical candidate.

BF.B is going through a transformation as it has disposed of various brands and has acquired new brands. Further details can be found in Brown-Forman’s December 2016 Investor Conference presentation.

BF.B’s dividend history can be found here and its historical PE ratios can be found here. As you can see, Brown-Forman periodically issues a special dividend. The dividend yield reflected on various investment related websites, however, rarely reflects these special dividends.

In 2016, for example, Brown-Forman paid out $1.6925 in dividends of which $1.00 was a special dividend. Many websites exclude this special dividend, and therefore, reflect a sub 2% dividend yield. If I use a current price of $46.26 and the 2016 dividend of $1.6925, the dividend yield in 2016 was closer to 3.66%. All websites I have checked reflect a dividend yield closer to 1.58%.

I totally recognize these are “special” dividends, and therefore, I exclude them when analyzing Brown-Forman.

Should we elect to add Brown-Forman to our portfolio, I would acquire the class B shares versus the class A shares. The class B shares are non-voting but in the grand scheme of things, my voting privileges through the ownership of several hundred, or a few thousand, class A shares will be immaterial.

McCormick & Company (NYSE: MKC)

MKC has always had some appeal to me from an investment perspective. I can’t pinpoint the exact reason but maybe it has something to do with the fact that when I open a kitchen cupboard to retrieve spices, 99% of the time they happen to be MKC products.

I recognize MKC does not have a dividend yield to write home about but I don’t make investment decisions solely on the basis of dividend yield. I look for a long-term sustainable business that has a historical track record of moderate dividend growth and capital appreciation.

In March 2017 I wrote a post indicating I thought MKC was a bit rich. I still think it is but that doesn’t mean I don’t want to add it to our holdings. I just need to wait for it to be more attractively priced.

Final Thoughts

I have been practicing a great deal of patience for the past few months as the political and economic uncertainty in various areas of the world has me concerned that not all is well. I have restricted our YTD 2017 investment to $55,000 as I have been hoping for a market correction of significance so as to bring stock valuations to more reasonable levels.

Should we experience a market correction of significance, I would have no hesitation in using a prudent amount of leverage to acquire shares in wonderful companies. I recognize taking on debt during retirement is generally not prudent but I am willing to take on the risk.

I have compiled the list of companies reflected in this post while taking into consideration all our equity holdings. As a result there are many attractive companies that have been excluded from my list of potential investments.

While I certainly intend to acquire shares in UNP, PAYX, SJM, MA, FDX, HRL, and TU in the not too distant future, it is entirely possible I may defer any investment in BF.B and MKC.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long BCE, BNS, CNI, DEO, DH, FDX, MA, RY, T (AT&T), T(Telus), UPS, V, VZ.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.