Summary

Summary

- This Enbridge stock analysis is based on Q2 2017 results and management’s forecast for the remainder of fiscal 2017 which was presented August 3, 2017.

- Enbridge has excellent long-term growth opportunities and currently has one of the strongest portfolios of in-service and future growth pipeline projects.

- It currently has $31B of diversified low-risk projects in various stages of development of which $7B are to be placed in service in the 2nd half of 2017.

- Enbridge has a track record of rewarding dividend conscious investors with steadily increasing dividends over the past 22 years.

- I recently acquired Enbridge shares for the FFJ Portfolio after completing my analysis.

All figures are expressed in Canadian dollars unless otherwise noted.

Introduction

I am in the process of deploying cash to acquire additional shares for my FFJ Portfolio. While I may want to use the dividends generated from this portfolio to service some of my living expenses during retirement, my ultimate goal is to have a well diversified portfolio which can be willed to the next generation.

I am investing in companies where I can put my head on the pillow at night knowing there is a possibility they may get bruised but will likely survive if/when we do experience market turmoil. In this regard, I am not seeking speculative investments. Instead, I am restricting my investments to high-quality companies with a track record of dividend growth and I am spreading my investments over the five main economic sectors (Resources, Manufacturing, Finance, Utilities, and Consumer).

The subject company of this post appears to fit the bill and this is a company which has been almost under my nose for years!

Today I saw Enbridge Inc. (NYSE: ENB) and Union Gas vehicles in our neighborhood; ENB owns Union Gas as a result of its acquisition of Spectra Energy Corp. on February 27, 2017. I regularly see these companies’ vehicles but I have never given it any thought to check out ENB as a potential investment until fellow blogger The Financial Canadian asked me for my take on the company. I decided to act on his request and coincidentally noticed ENB had released its Q2 results ending June 30, 2017 on August 3, 2017!

Business Overview

ENB has been in business for over 65 years. It lines of business are energy transportation, generation, and distribution. It is a Canada’s largest natural gas distribution provider with about 3.5 million retail customers in Ontario, Quebec, New Brunswick and New York State. It has interests in nearly 3,000 megawatts of net renewable generation and power transmission capacity, based on projects in operation or under construction, and continues to expand into renewable energy sources of power.

1. Energy Transportation

ENB’s 17,511 miles (28,181 km) of active pipe makes it the operator of the world’s longest, most sophisticated crude oil and liquids transportation system. It delivers an average of 2.8 million barrels of crude oil each day through its Mainline and Express pipelines, and transports 28% of the crude oil produced in North America. It is also a North American leader in the gathering, transportation, processing and storage of natural gas, with 34,410 miles (55,377 km) of gas pipelines. Approximately 23% of all natural gas consumed in the U.S., serving key supply basins and demand markets, is moved by ENB. In addition it has 11.4 billion cubic feet per day (Bcf/d) of processing capacity, 307 thousand barrels per day (Mbpd) of NGL production, and 437 billion cubic feet (Bcf) of net natural gas storage capacity.

2. Energy Generation

ENB is actively expanding its interests in renewable and green energy technologies. This includes wind, solar energy, and geothermal, with nearly 3,000 megawatts (MW) of net renewable generation and power transmission capacity, based on projects in operation or under construction.

3. Energy Distribution

ENB is Canada’s largest natural gas distribution provider, with about 3.5 million retail customers in Ontario, Quebec, New Brunswick and New York State.

ENB also manages several investment options that trade on the NYSE and/or the TSX:

- 9% economic interest in Enbridge Energy Partners, L.P. (NYSE: EEP);

- 7% economic interest in Enbridge Energy Management, L.L.C. (NYSE: EEQ);

- 75% equity interest in Spectra Energy Partners, LP (NYSE: SEP);

- 6% economic interest in Enbridge Income Fund (TSX: ENF).

While I endeavor to provide a high level overview of ENB, I strongly suggest you look at the following to get a more comprehensive overview of ENB’s operations.

- Enbridge Energy Dashboards so you can see the magnitude of ENB’s operations;

- ENB’s highly informative June 27, 2017 presentation made at JP Morgan’s Energy Conference;

- ENB’s 2017 Mid-Year Investor Update Meeting presentation held June 8, 2017.

There is just no possible way this post can cover all the material presented in the company prepared material.

Here are some statistics for those interested in more than just the financials:

- ENB has been ranked on the Global 100 Most Sustainable Corporations index for 8 straight years;

- It was ranked # 12 worldwide on the 2016 Newsweek Green Rankings corporate sustainability index;

- On 15 occasions ENB has been named to the Canada’s Top 100 Employers list;

- ENB has been selected as one of Canada’s Top Diversity Employers 3 years running.

Q2 2017 Financial Results

On August 3, 2017, ENB released its Q2 results ending June 30, 2017. The Q2 2017 Financial Results and Strategic Update which includes details related to the publicly traded investment options ENB manages can be found here.

Q2 profitability was negatively impacted by outages and production disruptions in ENB’s liquids pipeline business. ENB, however, expects improved business as production and throughput ramps back up on its mainline system.

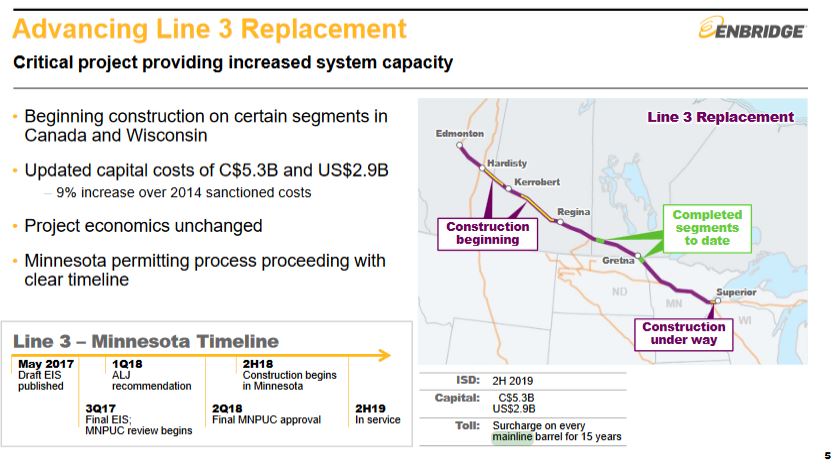

Very recently ENB confirmed it had obtained permits in Canada, North Dakota, and Wisconsin for its Line 3 pipeline replacement project which will run from Hardisty, Alberta, to Superior, Wisconsin. It, however, still requires regulatory approval from Minnesota but is cautiously optimistic it will receive this in Q3, and therefore, has very recently commenced construction.

The downside is that regulatory delays and route modifications are expected to increase the cost to C$8.2 billion ($6.52 billion) which is 9% more than previously projected.

On a positive note:

- this increased cost is now expected to be offset by lower operating costs and a stronger U.S. dollar;

- despite regulatory delays, the project remains on track for service in the second half of 2019.

ENB, is of the opinion it will be extremely competitive in terms of attracting spot barrels as refiners in the U.S. Midwest and Gulf Coast area like the product ENB transports. It is not, however, the only company in the business of moving liquids through pipelines. It competes against TransCanada and Kinder Morgan; TransCanada’s (NYSE: TRP) Keystone XL and Kinder Morgan’s (NYSE: KMI) Trans Mountain pipeline projects have also experienced considerable delays but are cautiously expected to proceed after years of political wrangling.

Strategic Update

The combined ENB/Spectra entity adds significant scale, improves the balance sheet, and is accretive to dividend growth. I really like that Spectra’s gas pipelines diversify ENB’s risk profile and I foresee growth in demand for natural gas over the coming years as being as huge plus for ENB.

The completed merger between ENB and Spectra Energy now means that:

- ENB has an industry-leading $28B in secured expansion projects in execution which are scheduled to come online between 2017 and 2019 plus $48 billion of development projects;

- ENB has a more balanced platform of crude and natural gas;

- ENB’s growth program has more than doubled;

- ENB’s dividend growth outlook is enhanced.

ENB’s “Mainline” is well positioned to benefit from Western Canadian crude volume growth. It has been operating at close to full capacity and the replacement of “Line 3” in 2019 will add an incremental 375,000 barrels/day of new capacity.

I think it would be a real shame for ENB to just focus on the pipeline business so I am pleased to see that ENB is growing its renewable energy business.

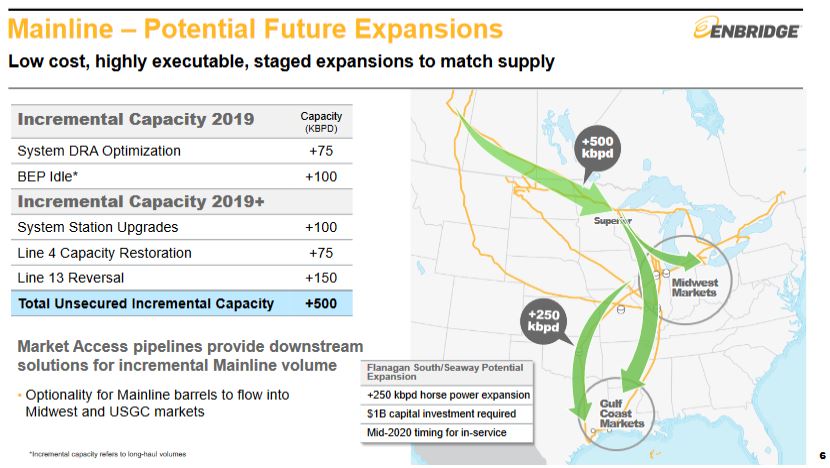

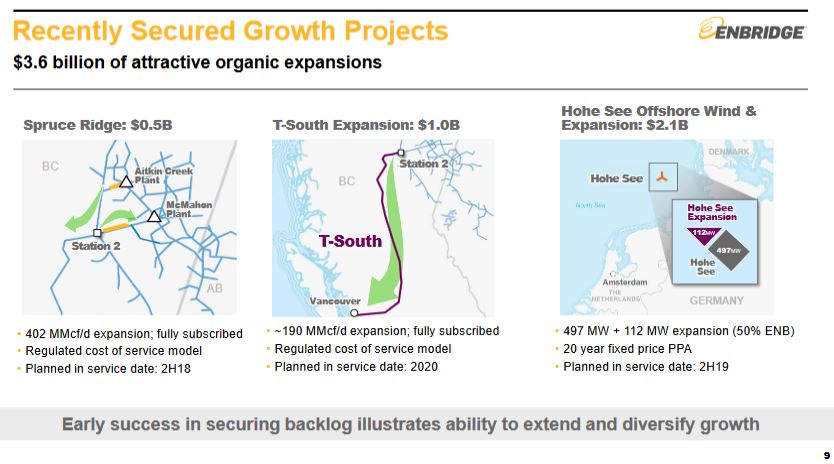

You can get a high level overview of ENB’s multiple projects here and also in the following screenshots extracted from the Q2 2017 Financial Results and Strategic Update.

ENB Strategic Update August 3 2017 page 5

ENB Strategic Update August 3 2017 page 6

ENB Strategic Update August 3 2017 page 7

ENB Strategic Update August 3 2017 page 8

ENB Strategic Update August 3 2017 page 9

I also like that ENB has a relatively low-risk business model with limited direct commodity exposure since ~96% of its cash flow is linked to long-term commercial agreements (e.g. take or pay contracts). In addition, less than 5% of EBITDA is exposed to commodity prices.

Dividend

ENB has a track record of paying dividends for over 64 years to shareholders and with annual dividend increases dating back to 1996.

ENB currently pays a CDN$0.61 or a USD$0.49 quarterly dividend thus resulting in a dividend yield north of 4.6% based on the August 4, 2017 closing price of CDN$52.57 or USD$41.53.

Over the past 20 years, ENB’s dividend has grown at an average compound annual growth rate of 11.2% and ENB is projecting annual dividend growth of 10% – 12% during the 2018 – 2024 timeframe. This historical dividend growth has not come at the expense of ENB’s financial strength as Adjusted Cash Flow from Operations (‘ACFFO’) coverage of the dividend remained very strong in 2016 (approximately two times).

In 2017 alone, ENB has increased its dividend twice. In January 2017, ENB announced a 10% increase to its dividend per share, increasing the quarterly dividend to $0.583 from $0.53; this increase represented the 22nd consecutive year of increased dividends.

On May 4, 2017, ENB declared a quarterly common share dividend of $0.61/share payable on June 1, 2017 to shareholders of record on May 15, 2017. The declared dividend represented an increase of approximately 5%. That incremental dividend increase was consistent with ENB’s previously announced intention to consider an additional increase to its quarterly dividend upon completion of the Spectra Energy Corp acquisition which closed February 27, 2017.

ENB – 3 and 6 month Dividends

ENB targets a 50% – 60% dividend payout of ACFFO, thus providing a healthy balance between returning income to shareholders and retaining income for reinvestment in new growth opportunities.

I view ENB’s dividend track record and its projected dividend growth as attractive features for my purposes.

Share Dilution

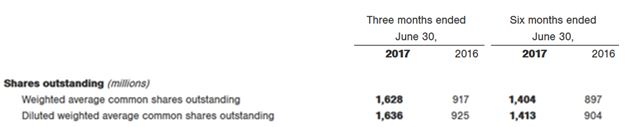

As part of the Spectra Energy acquisition, ENB issued a considerable number of new shares.

ENB – 3 and 6 month Shares Outstanding

ENB does not have a history of redeeming shares. In fact, during the 2009 – 2016 time frame, ENB had the following number of diluted weighted average shares outstanding (expressed in millions): 732, 748, 761, 785, 817, 840, 847, and 918. I generally prefer to acquire shares in companies that are reducing their share count but have made an exception in the case of my recent acquisition of ENB shares since there is a positive trend on an adjusted earnings per share basis.

Valuation

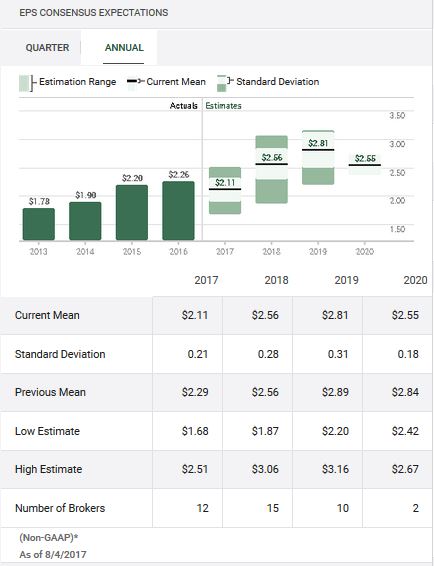

The consensus 2017 and 2018 EPS expectations from multiple brokers are $2.11 and $2.56 respectively.

ENB – EPS Consensus Expectations as at Aug 4, 2017

Source: TD Bank WebBroker

The TSX listed ENB shares closed at $52.57 on August 4, 2017. Based on this closing price and the projected $2.11 EPS for FY2017, I get a forward PE of 24.92. While a PE at this level might appear to be a tad rich, I am prepared to pay up for the type of quality I see in the combined ENB/Spectra entity.

Enbridge Inc. Stock Analysis – Final Thoughts

I like ENB’s relatively recent acquisition of Spectra Energy and the business model. I take comfort that ENB has the wherewithal to weather the storms that will inevitably arise over the course of time. Furthermore, I am confident ENB will generate a reasonable return for me over the foreseeable future with the probability being very low that I will experience a major permanent impairment to my invested capital.

Based on my analysis I very recently initiated a position of 400 shares in the TSX listed ENB shares for my FFJ Portfolio; I am a Canadian resident and want to minimize my foreign exchange risk and do not want to incur withholding tax on the ENB dividends hence the reason why I did not purchase the NYSE listed shares.

Note: I sincerely appreciate the time you took to read this post. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long ENB.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.