I last reviewed Broadridge Financial Solutions (BR) in this November 29, 2022 post at which time it had recently released its Q1 2022 results. With the release of the Q4 and FY2023 results and FY2024 guidance, I take this opportunity to revisit this existing holding.

Business Overview

BR operates in two reportable segments, Investor Communication Solutions and Global Technology and Operations, which are both highly competitive.

The majority of BR’s clients operate in the financial services industry. Its largest single client in FY2021, FY2022, and FY2023 accounted for ~6%, ~7%, and 7% of consolidated revenues.

Part 1 Item 1 in the FY2023 Form 10-K is a good source of information to learn about the company.

In BR’s December 10, 2020 Investor Day Presentation, it set out its new 3-year growth objectives for FY2020 – FY2023.

In FY2020, BR reported recurring revenues of $2.9B and adjusted diluted EPS of just over $5. Three years later, BR has grown its recurring revenues by ~40% to $4B and reported adjusted EPS of $7.01.

Financials

Q4 and FY2023 Results

Material related to BR’s Q4 and FY2023 financial results is accessible here. The FY2023 Form 10-K is available here.

In 2023, recurring revenue and adjusted EPS both rose 9%, and free cash flow conversion improved to 90%.

The very nature of BR’s business is such that it is extremely difficult to compare BR’s financial condition, results of operations, and cash flows every quarter.

The processing and distribution of proxy materials and annual reports to investors comprise a large portion of BR’s Investor Communication Solutions business. It processes and distributes the greatest number of proxy materials and annual reports during its Q3 and Q4 (its fiscal YE is the end of June); the recurring periodic activity of this business is linked to significant filing deadlines imposed by law on public reporting companies. As a result, BR’s revenues, operating income, net earnings, and cash flows from operating activities are typically higher in Q3 and Q4.

On the Q4 earnings call, management states that its financial services clients are reducing headcount and delaying purchasing decisions as they deal with the fallout from:

- the steepest rate increases in decades;

- a sharp slowdown in investment banking activity;

- fund outflows;

- banking crises; and

- increased regulation.

These pressures are impacting BR’s sales. After 11 years of record sales, closed sales of $0.246B were down 12% vs FY2022.

While U.S. sales were largely on track, there were many delayed decisions in Europe. Management thinks that these are delays and that they will have little impact on BR’s long-term growth trajectory. It has not witnessed projects being dropped or losses to competitors and the sales pipeline is at a record.

With a new UBS contract in place, BR has moved to marketing and generating $20 – $30 million in sales from the new wealth management platform components.

Now that the UBS project has gone ‘live’, ~$0.6B of software investment from the ‘Deferred Client Conversion’ line item on the Balance Sheet is being reassigned to ‘Intangible Assets’. This is consistent with the Balance Sheet classification of platform technology that will be marketed to multiple clients. Additional information regarding the ‘Deferred Client Conversion and Start-Up Costs’ is in BR’s Form 10-K.

Source: BR – FY2023 Form 10-K

BR expects to recognize $57 million of annualized amortization expense in FY2024 resulting from its wealth platform investment. This change will have no impact on FCF or the income statement.

Capital Allocation

The following reflects BR’s capital allocation in FY2023.

Source: BR – Q4 and FY2023 Earnings Presentation – August 8, 2023

In contracts, BR’s capital allocation in the form of CAPEX and Software, Client Platform Investments, M&A, and Debt Paydown in prior recent years was:

- FY2022: $0.073B, $0.447B, $0.037B, $0

- FY2021: $0.101B, $0.298B, $2.6B, $0 (Press Release regarding Itiviti acquisition)

- FY2020: $0.99B,$0.157B, $0.339B, and $0

Given management’s expectation for a strong FY2024 that includes continued top and bottom line growth, record close sales, and higher free cash flow conversion, the plan is to return to a more balanced capital allocation. Management expects to make further progress in raising the firm’s Return on Invested Capital (ROIC) to the mid-to-high teens over the next three years which would be relatively similar to historical levels.

Free Cash Flow (FCF)

BR’s FCF (in billions of $ rounded) in FY2012 – FY2023 is $0.220, $0.334, $0.365, $0.362, $0.312, $0.556, $0.544, $0.500, $0.539, $0.370, and $0.748. The YoY improvement in FY2022 to – FY2023 FCF is attributed to a reduction in client platform spend and payments from UBS as the UBS project goes live, along with strong working capital management.

Over the last 12 months, BR generated a 90% Free cash flow conversion rate. BR expects an FCF conversion rate of ~100% in FY2024.

As a result of our strong free cash flow, we expect to resume share repurchases in fiscal 2024 and to also have the flexibility to fund tuck-in M&A if the right opportunity arises.

Source: BR – Q4 and FY2023 Earnings Presentation – August 8, 2023

FY2024 Guidance

BR typically generates a little less than 25% of its earnings in the first half of the fiscal year. In the first half of the year, earnings are slightly more weighted toward Q1 versus Q2. This is driven by higher event-driven revenue in Q1. The revenue flow is likely to be no different in FY2024.

BR will host its Investor Day on December 7, 2023 at which time it will likely lay out a new set of 3-year objectives. Until such time, however, we have BR’s FY2024 guidance.

Source: BR – Q4 and FY2023 Earnings Presentation – August 8, 2023

I include BR’s FY2023 guidance from the time of my last review for comparison.

BR is undergoing a modest restructuring to realign some of the businesses and streamline the management structure. Expectations are that ~2% of BR’s 14,700 associates will be impacted.

As a result of this restructuring, BR incurred a $20 million restructuring charge in Q4 2023. Management anticipates this restructuring will generate ~$50 million in annualized savings.

The forecast calls for another ~$15 – ~$30 million charge in Q3 2024 as BR completes this restructuring initiative. Guidance excludes these additional charges.

Credit Ratings

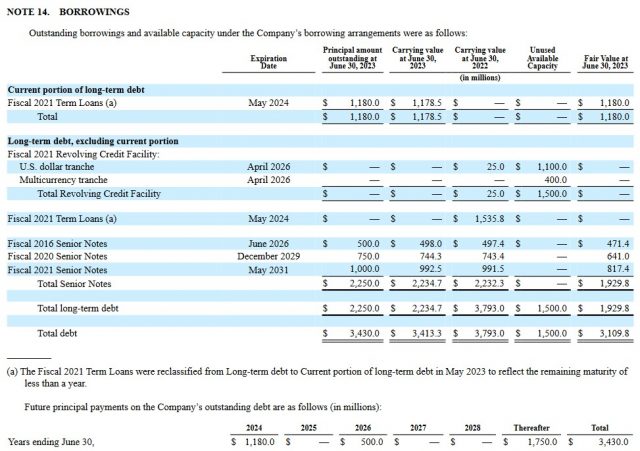

Details of BR’s credit facilities are found in Note 14 within the FY2023 Form 10-K (page 77 of 406).

I provide the debt schedule found on page 44 of 130 in the FY2022 Form 10-K for comparison purposes.

Source: BR – FY2022 Form 10-K

BR’s leverage is higher than historical levels and the plan is to reduce the debt to a more sustainable level.

All BR’s domestic senior unsecured debt ratings are at the top tier of the lower-medium grade investment-grade category. There is no change from the time of my last review.

- Moody’s: Baa2 with a stable outlook. This rating was downgraded from Baa1 on May 15, 2023;

- S&P Global: BBB with a stable outlook. This rating was downgraded from BBB+ on June 13, 2023;

- Fitch: BBB+ and a stable outlook and affirmed on June 28, 2023. This rating is unchanged from the time of my prior reviews.

These ratings define BR as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

Surprisingly, these ratings were not downgraded sooner.

Despite the rating downgrades, BR’s credit risk remains acceptable for my purposes.

Dividends and Share Repurchases

Dividend and Dividend Yield

As I compose this post, BR’s dividend history does not reflect the recent announcement about the 10% increase in the annual dividend to $3.20 ($0.80/quarter) from $2.90 ($0.725/quarter); the first $0.80/share dividend payable in early October.

BR has increased its dividend every year (17 years) after its spin-off from Automatic Data Processing (ADP) on March 30, 2007. This includes double-digit increases in 11 of the past 12 years.

Shares now trade at $176.86 and the forward dividend yield is ~1.8%.

When I reviewed BR in my November 29, 2022 post, shares were trading at ~$143, the dividend yield was ~2%.

Share Repurchases

The weighted average shares outstanding in FY2012 – FY2023 (in millions rounded) are 128, 125, 124, 124, 122, 121, 120, 119, 117, 118, 119, and 119.

In FY2022, BR repurchased $22.8 of outstanding shares. At the end of Q3, BR had only repurchased $3.7 million shares YTD. By the end of FY2023, it had repurchased $24.3 million. No shares repurchased in FY2021 – FY2023, however, were made under the company’s share repurchase program.

BR still has ~9.6 million shares available for repurchase under its share repurchase program.

Valuation

BR’s diluted PE in FY2012 – FY2022 is 21.58, 20.69, 22.86, 22.96, 26.21, 31.89, 25.46, 31.68, 38.01, 39.2, and 30.48.

BR has now reported $5.30 in diluted EPS for FY2023. The current share price is $176.86 thus resulting in a diluted PE of ~33.4.

My November 29, 2022 post reflects BR’s valuation using adjusted earnings estimates at the time of prior posts. However, I provide BR’s valuation at the time of my November 29, 2022 post for ease of comparison.

Management’s adjusted diluted EPS guidance was ~$6.91 – ~$7.17. Using a ~$143 share price, the FY2023 adjusted diluted PE range was ~20 – ~20.7.

BR’s valuation using current broker guidance was:

- FY2023 – 5 brokers – mean of $6.97 and low/high of $6.88 – $7.02. Using the mean, the forward adjusted diluted PE is ~20.5.

- FY2024 – 4 brokers – mean of $7.52 and low/high of $7.39 – $7.65. Using the mean, the forward adjusted diluted PE was ~19.

- FY2025 – 2 brokers – mean of $8.27 and low/high of $8.25 – $8.29. Using the mean, the forward adjusted diluted PE was ~17.3.

With the release of FY2023 results, we see that BR’s FY2023 adjusted diluted EPS is $7.01. Using management’s FY2024 adjusted diluted EPS growth guidance of 8% – 12%, we get a range of ~$7.57 – ~$7.85. With shares currently trading at ~$176.86, the forward adjusted diluted PE range is ~22.5 – ~23.4.

BR’s valuation using the current broker guidance is:

- FY2024 – 8 brokers – mean of $7.57 and low/high of $7.36 – $7.80. Using the mean, the forward adjusted diluted PE is ~23.4.

- FY2025 – 7 brokers – mean of $8.38 and low/high of $8.02 – $8.68. Using the mean, the forward adjusted diluted PE was ~21.

- FY2026 – 2 brokers – mean of $9.27 and low/high of $9.05 – $9.49. Using the mean, the forward adjusted diluted PE was ~19.1.

If we look at the Condensed Consolidated Statements of Cash Flows for FY2020, FY2021, FY2022 and FY2023, we see that:

- Depreciation and amortization;

- Amortization of acquired intangibles and purchased intellectual property; and

- Amortization of other assets

total ~$0.300B, ~$0.335B, ~$0.464B and ~$0.425B. These significant non-cash items reduce EPS but have no impact on cash flow. I, therefore, look at BR’s valuation using FCF. BR’s Price/FCF per share is:

($748.2 million of FY2023 FCF/119 million diluted share O/S in FY2023) = $6.29 FCF/share

~$176.86 share price/$6.29 = ~28.1 P/FCF

BR’s valuation using P/FCF is higher than on an adjusted diluted PE basis.

Final Thoughts

On December 7, BR will host its Investor Day at which time I expect the presentation of new 3-year growth objectives. As a risk-averse investor, I hope BR plans to restore the credit ratings to the levels before the recent downgrades.

I am a BR shareholder since the spin-off from ADP; the average cost of those shares which I hold in a retirement account is below $30.

I also hold 285 shares in a ‘Core’ account and 545 shares in a ‘Side’ account within the FFJ Portfolio.

In my Mid-2023 Investment Holdings Review, BR was my 17th largest holding at which time its share price on June 30th (date of review) was ~$166.

I am looking to add to exposure in high-quality companies that appear to have temporarily fallen out of favour. Since BR is currently not such a company, I do not intend to acquire additional shares. Furthermore, I think BR is overvalued. I deem a price of ~$165 or lower to be reasonable ($7.71 midpoint of management’s FY2024 guidance x a ~21 forward adjusted diluted PE).

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BR and ADP.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.