Summary

Summary

- This Bank of Montreal Stock Analysis is based on Q2 2017 results and is the first of a 6 part series covering the Big 6 Canadian Banks.

- BMO US results have raised concerns about a slowing in its US growth.

- BMO’s Capital Measure Ratios continue to improve thus providing investors with assurances that BMO remains a safe bank.

- Pockets of the Canadian real estate market are wildly overheated but BMO’s results indicate its real estate related loan portfolio is of sound quality.

- The Home Capital Group implosion is unlikely to have a significant effect on BMO’s residential mortgage portfolio.

- BMO has paid a dividend for 188 years and it announced a $0.02 increase to CDN $0.90 effective with its August 2017 dividend payment.

All figures are expressed in Canadian dollars unless otherwise noted.

Introduction

Bank of Montreal (TSX: BMO), Canada’s 4th largest bank by market cap, reported Q2 2017 results on May 24th. Despite reporting relatively decent results, the market has not taken kindly to the less than stellar results from BMO’s US Personal and Commercial Banking operations.

While I touch upon various topics that impact the Canadian Banking Sector and the top 6 Schedule I Canadian Banks, I strongly encourage you to listen to the BMO segment of the March 29 and 30, 2017 National Bank Financial Markets – 15th Annual Financial Services Conference. There is far too much information covered in this ~30 minute segment for me to give the content justice in this post.

The Canadian Banking Sector

The Canadian banking sector is pretty close to an oligopoly. You essential have 6 large (by Canadian standards) Schedule I banks, some smaller Schedule I banks, and even smaller Schedule II and Schedule III banks.

In most cases, if a personal banking client elects to make a change in their banking relationship, the change will be from one of the Big 6 to another one of the Big 6. Naturally this is not always the case but odds are this is more common than not.

The same will apply with respect to Commercial Banking relationships. In many cases, Commercial Banking clients require cash management services which the smaller banks are unable to offer. In addition, as a business grows in size, credit facilities typically increase in size. It is not uncommon for multiple banks to participate in credit facilities for large Commercial Banking clients since banks tend to mitigate their risk by inviting other lenders into the picture to share the risk.

At the Corporate level, you typically see multi-nationals or large publicly traded Canadian entities dealing with multiple banks in a lending syndicate. In some cases, major Canadian financial institutions may only be a participant and not the lead when dealing with large Canadian corporate entities with extensive international operations. If a large multi-national has Canadian operations, there is a very strong probability that no major Canadian financial institution is participating in the lending syndicate. The reasoning for this is that the largest Canadian financial institutions are not relatively small on a global scale and their banking operations are extremely limited or non-existent in other parts of the world.

Another trend in the Corporate Banking world is the streamlining in the number of banks providing cash management services. Historically it was not uncommon for large corporations with extensive international operations to have dealings with dozens of banks. This is grossly inefficient and the trend in the last couple of decades has been toward the consolidation of cash management services with fewer service providers as large multi-national banks develop their cash management services.

At the Corporate Banking level, ancillary services (eg. foreign exchange, cash management, trade finance) are allocated to the financial institutions which extend their balance sheet to the company. Same is generally done on the basis of where a bank ranks in the lending syndicate. Furthermore, at the Corporate level, the major Canadian banks are no longer competing amongst themselves and in many cases, the terms and conditions of a company’s credit facilities are dictated by a large foreign bank.

Fortunately, the Canadian financial institutions have a diversified book of business. A huge focus is placed on growing the personal banking, small business, and the wealth side of the banking operations. The rationale for this is that the profit margins are higher and this business is less susceptible to being lost to much larger foreign-based financial institutions.

Technological Innovation

The banking industry has experienced dramatic technological changes in recent years. This has been brought about by reason of such factors as, but not restricted to, increasingly stringent reporting requirements, increasingly sophisticated clients, the need for instantaneous information, the rapidly escalating human resource related costs (eg. pension and benefits), and lower spreads resulting from a prolonged low interest rate environment.

The rapid technological changes are also introducing new competitors. You now have non-bank lenders using technology to encroach in areas of business where banks essentially had a stranglehold (ie. wealth, personal lending, foreign exchange, mortgage lending).

In addition, advances in technology will continue to provide opportunities for banks to consolidate operations. While much of the consolidation to date has occurred within specific countries, it is not unreasonable to foresee a future where, for example, one or two data centres could process on behalf of a bank’s operations in multiple countries.

The Canadian banks also recognize they need to partner with Financial Technology firms (FinTechs) in order to become more competitive; FinTech is an industry composed of companies that use new technology and innovation in order to compete in the marketplace of traditional financial institutions and intermediaries in the delivery of financial services.

FinTechs bring to the table very client friendly and simple to use systems. The Canadian financial institutions bring to the table their massive client base. By joining forces, the banks are able to turn off their clunky legacy systems which have limited functionality and flexibility and which cost a fortune to upgrade.

BMO Overview

You can access BMO’s Q2 2017 Corporate Fact Sheet here if you are totally unfamiliar with this Canadian financial institution.

BMO’s medium term financial objectives can be found here.

Q2 2017 Financial Results

Readers are encouraged to review BMO’s May 24, 2017 Earnings Release and to listen to the Conference Call.

Capital Measure Ratios

The following table reflects BMO’s various Capital Measure Ratios for the last 9 quarters. While all are trending in the right direction I recognize that Capital Measure Ratios can vary slightly from quarter to quarter. I do not, therefore, get overly concerned with slight variations from quarter to quarter. I do, however, monitor these ratios to determine whether there has been any significant variance or whether there is an identifiable trend.

BMO – Capital Measure Ratios

A high level overview of the various ratios referenced above can be found here.

The financial stability of a financial institution is of paramount importance. In an effort to avoid a repeat of the Financial Crisis, a comprehensive set of reform measures (Basel III) was developed by the Basel Committee on Banking Supervision. While the Basel Committee undertook a program of far-reaching reforms to the international standards for bank capital requirements and reached an agreement in 2009, the agreement left some significant unfinished business. Until recently, the Committee had been working to complete the reform agenda, but those negotiations have stalled, and it is not clear when they will resume.

As a result, The Office of the Superintendent of Financial Institutions (OSFI) in Canada is moving ahead with a Canada-specific plan for improving the capital regime. Should OSFI conclude that the Basel process is unlikely to restart in the near future, it will put that plan into action in a measured way. Moreover, that plan will recognize that an effective capital regime includes much more than the minimum requirements that have been the primary focus of attention at Basel in recent years.

Risk Management

Readers are encouraged to review the 26 page “Quarterly Presentation” found here as there are multiple pages that provide details addressing the quality of BMO’s loan portfolio. There are also multiple pages in BMO’s 2016 Annual Report addressing BMO’s Risk Management. Page 26 of the Annual Report lists the locations of the disclosures within the report.

Recent Events in the Canadian Banking Sector

Improper Retail Sales Practices

BMO shares, along with shares in its major counterparts (Royal Bank of Canada (TSX: RY), The Toronto-Dominion Bank (TSX: TD), The Bank of Nova Scotia (TSX: BNS), Canadian Imperial Bank of Commerce (TSX: CM) and National Bank (TSX: NA) were on a steady upward trajectory subsequent to the US Presidential election until mid/late February 2017. In early March 2017, however, allegations of improper retail sales practices at TD (see here, here) and deceptive employee titles at RY (see here) took the wind out of their sails.

While reports of improper sales practices are no longer receiving heavy media exposure, it is highly likely the allegations of abusive sales practices will be back in the spotlight before long. The Parliamentary Finance Committee has announced it wants to hear from top bank executives as to whether their sales team are pressured to push products on customers which those customers do not need or want.

Home Capital Corporation Implosion

In addition to the recent allegations of improper retail sales practices, we then experienced the implosion of alternative mortgage lender Home Capital Group Inc. (TSX: HCG).

HCG recently had to raise $2B in financing from Healthcare of Ontario Pension Plan at usury rates (try 22.5%) in order to temporarily remain in operation. It is extremely difficult for a financial institution to be profitable when its cost of borrowing is at this level!

We are now a few weeks after this financing arrangement was announced and no major Canadian financial institution has stepped up to the plate to try and acquire HCG’s book of business. I strongly suspect this will never happen! The major Canadian financial institutions are far more stringent when it comes to assessing the background of borrowers and I strongly suspect a huge percentage of the mortgages approved by HCG would have never met the major Canadian financial institutions’ mortgage requirements.

Secondly, HCG’s primary source of mortgage business is through the broker channel. Sourcing mortgage business from brokers is not the modus operandi of the major Canadian financial institutions as they don’t just want a client’s mortgage. They want the opportunity to develop a relationship with their clients so they can offer a suite of products and services. Have you ever attempted to transfer all your banking arrangements to another financial institution if you have multiple products and services? It is a hugely time-consuming and disruptive undertaking.

In fact, several years ago most of the major Canadian financial institutions made it less attractive for mortgage brokers to bring them business; BMO is one of the banks that discontinued sourcing mortgage business from brokers several years ago.

In addition to concern as to the quality of HCG’s mortgage book, there is concern about its deposit book. HCG sources the vast majority of its deposits through the broker channel. These types of deposits are not “sticky”, and therefore, are of little value from a Basel III perspective as they are highly susceptible to “run off”. This “run off” is exactly what has transpired. Deposits in HCG’s high-interest savings accounts dropped ~94% from March 28 (the day the company terminated the employment of former Chief Executive Martin Reid) and May 11 and continue to drop.

While some of the remaining high-interest savings deposits are covered by the Canada Deposit Insurance Corporation (CDIC), there are some limitations as to the extent of the coverage. In my opinion, this insurance coverage may be insufficient or unsatisfactory to warrant the risk of holding deposits with HCG for the sake of a few extra basis points.

The true test of depositor confidence will come shortly when $12.6B in 30, 60 fixed term instruments mature. I strongly suspect HCG will experience a huge outflow of these funds which will put further pressure on this bank.

As with most runs on a bank, the HCG crisis has been driven by sentiment and many have been wondering:

- whether the problems at HCG is a “canary in the coal mine”

- what will be the spillover effects if HCG were to go under?

In my opinion, HCG is not the “canary in the coal mine” nor will the spillover effects dramatically impact the major Canadian financial institutions; this sentiment is shared by RY’s CEO.

First and foremost, HCG is a minuscule player with a relatively tiny book of business in the overall picture. The Canadian financial industry is strong and has weathered far worse storms with the most recent example being the Financial Crisis. During this period the banks took a hit and even had to freeze their quarterly dividends. Their financial strength, however, allowed them to capitalize on growth opportunities. In fact, BMO was one of the Canadian financial institutions which made an opportunistic acquisition.

I think it is unlikely HCG will fail completely and in a worst case scenario, I suspect opportunistic venture capitalists would likely swoop in for pennies on the dollar and would recapitalize HCG.

Inflated Real Estate Values

I would expect the rapid rise in real estate values in various regions within Canada to be a bigger risk to the Canadian banks. I distinctly recollect what happened in the early 1980s and early 1990s when inflated real estate values came crashing down. The banks certainly took a hit but because they were well capitalized and well managed they were able to weather the storm.

In an effort to bring the real estate market under control, various measures have been introduced. The British Columbia government introduced measures in late 2016 to cool the real estate market in the Vancouver area but that just shifted the demand from Chinese residents to real estate in Toronto, Montreal, and Calgary. Measures are also being taken by the Ontario provincial government as Toronto real estate values have soared dramatically within the past year. Interestingly, an ad in Hong Kong by a local broker offers to cover the 15% foreign buyers’ tax for the first 30 buyers of units in a downtown Toronto condo building!

In my opinion, we will undoubtedly have a correction in the residential real estate market within the next 12 months. The dramatic rise in real estate values is simply unsustainable and in a recent survey, 52% of Canadians have indicated they lack the financial flexibility to quickly adjust to a change in costs.

Having said this, the Canadian banks have managed their mortgage book very well. While the statistics vary for each bank, a significant proportion of each bank’s mortgage book is insured, borrowers with uninsured mortgages typically have reasonable FICO scores, the loan to value ratios are acceptable, and delinquency rates are currently negligible.

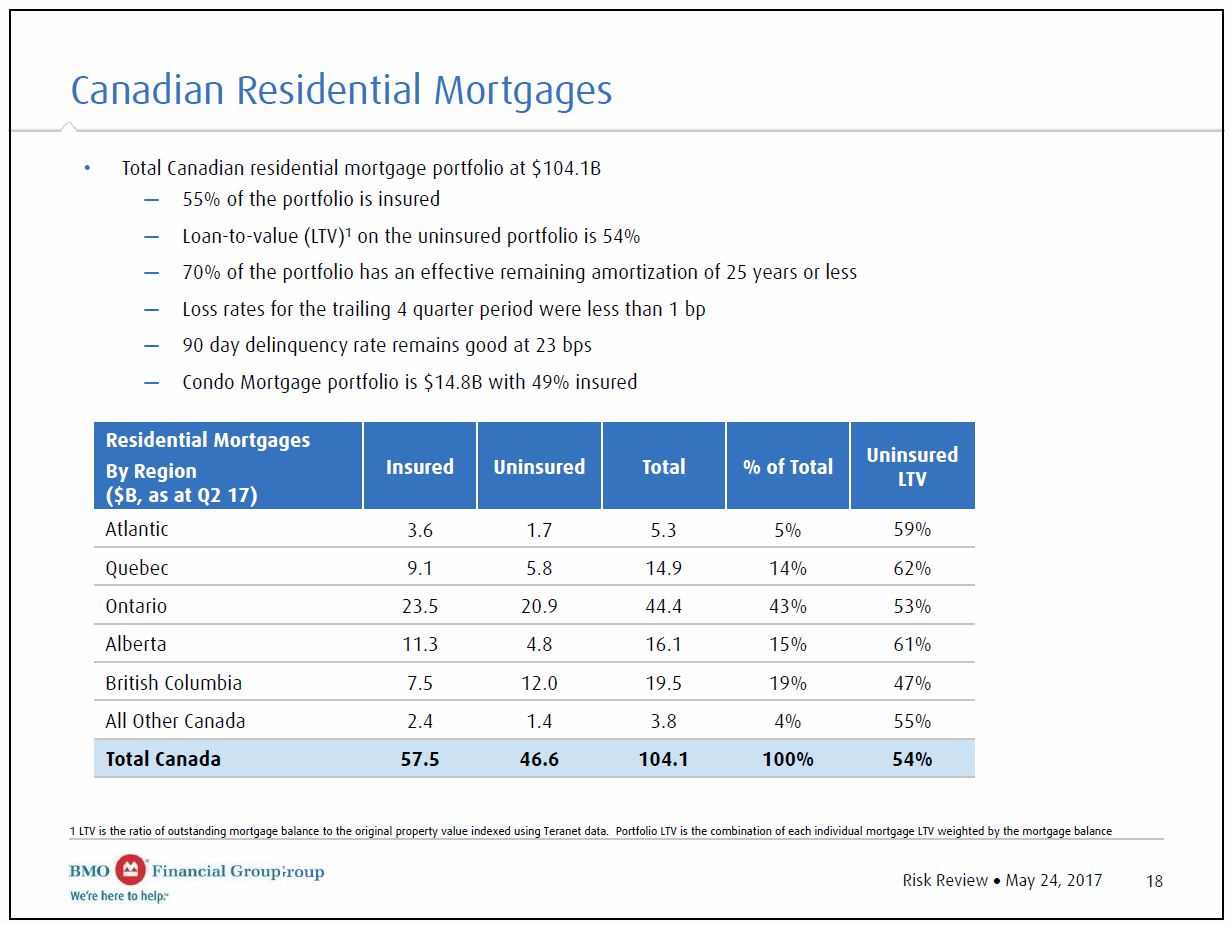

BMO’s Canadian Real Estate Secured Lending and Personal Banking Portfolios

With all the concerns about the average Canadian consumer being stretched financially and the inflated real estate values in specific geographic pockets within Canada, the major Canadian financial institutions have provided more information regarding the composition of their respective real estate related loan portfolio.

The following data was included in BMO’s Q2 2017 Earnings report.

BMO – CDN Residential Mortgages Q2 2017

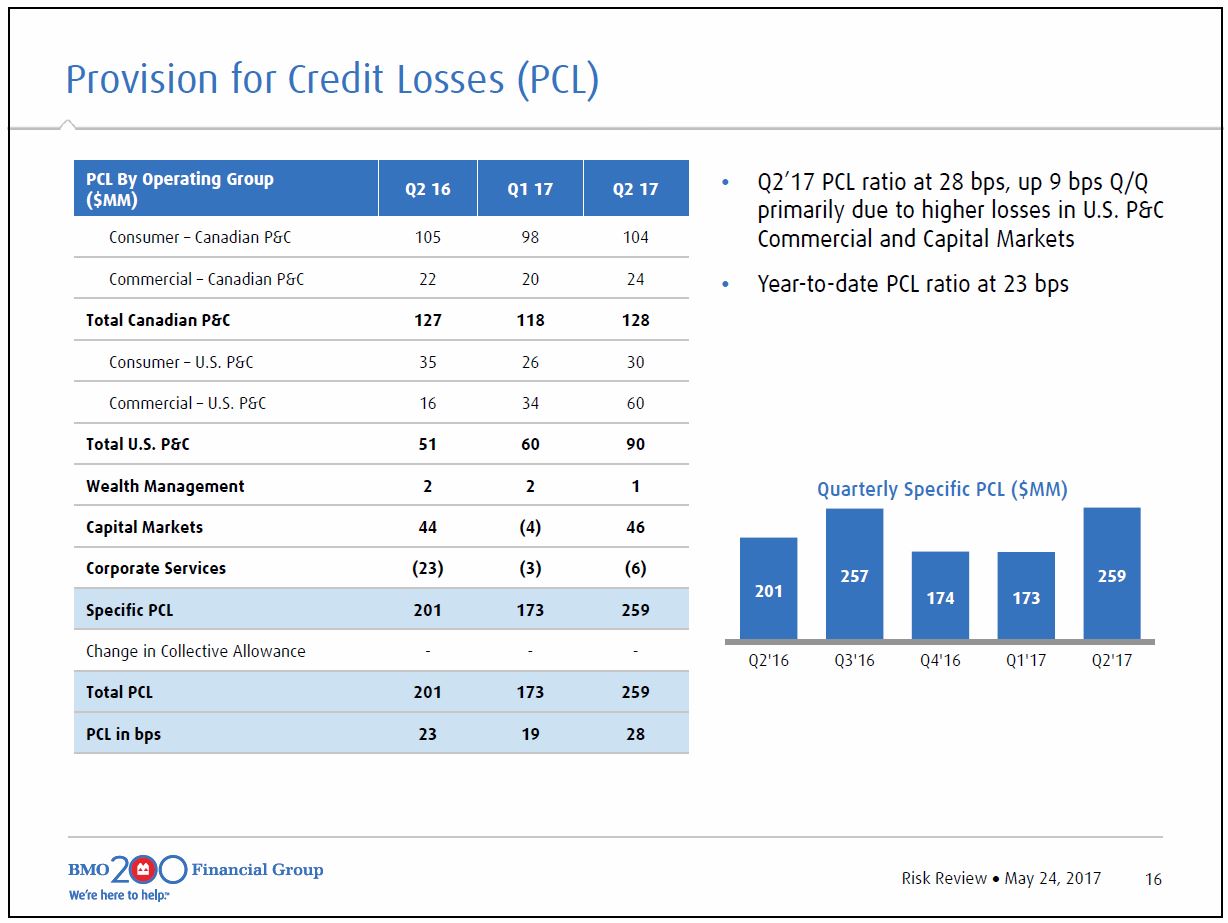

BMO – Provision for Credit Losses Q2 2017

While 45% of BMO’s real estate portfolio consists of uninsured mortgages, the Loan to Value ratio of these mortgages averages 54%.

BMO’s Provision for Credit Losses and Loans 90+ days past due appear to be well controlled. Naturally, if we enter an economic downturn we can certainly expect to see an increase from current levels. At the moment, however, there is no cause for alarm.

Other Risks

There are a host of other risks the Canadian financial institutions face. Global uncertainty, Brexit, Oil & Gas, Cyber risk, anti-money laundering, renegotiation of NAFTA, and the increasing complexity of regulation are just a few of these other risks.

If you want to see how each Canadian financial institution is addressing each identifiable risk I suggest you access the most recent annual report. There are countless pages where the banks discuss their approach to managing the key risks.

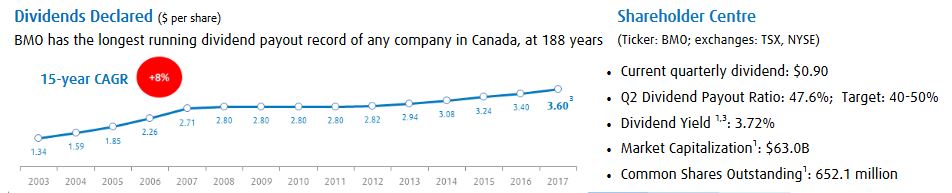

Dividend

Unlike many foreign banks which were forced to dramatically reduce or suspend their dividend during the Financial Crisis, BMO and its Canadian counterparts froze their quarterly dividend.

In 2012, BMO reinstated dividend increases albeit with some modification. In lieu of a one-time dividend increase on an annual basis, BMO opted to go with a lower dividend increase at the outset of the year followed by a second dividend increase mid-way through the year.

BMO’s recent dividend distribution history can be found here. On May 24th, BMO announced an increase in its quarterly dividend from $0.88 to $0.90 with the next dividend payable August 28th.

BMO Common Stock Dividend History

BMO has a 188 year dividend payout record and the likelihood of a dividend cut or elimination is remote. In this regard, investors seeking a safe dividend and a respectable dividend yield (~4% as I compose this) would be well served acquiring BMO shares at current levels.

Valuation

The market has not taken kindly to BMO’s Q2 results as it reported softer than expected results from its US operations. This has further helped BMO’s stock price retreat from its February 2017 highs.

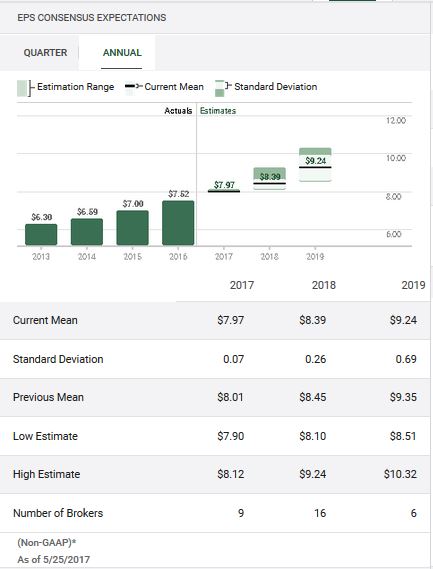

The current mean FY2017 adjusted EPS estimates from various brokers for fiscal 2017 is $7.97.

BMO EPS Earnings estimates May 2017

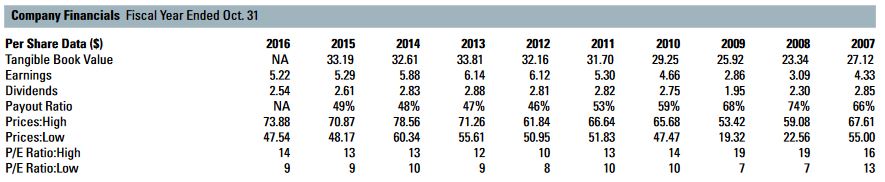

BMO Historical PE levels

As I compose this post, BMO is trading at ~$91 on the TSX thus giving us a forward PE of ~11.42. When I look at the high/low PE ratio levels for the past several years I view the current level as acceptable and would consider adding to our existing position. In fact, we DRIP all our BMO dividends and have just acquired several more shares by reason of the May 26th dividend payment.

Bank of Montreal Stock Analysis – Final Thoughts

I do not view BMO as the most attractive of Canadian banks from an investment perspective. In fact, we own shares in 5 major Canadian financial institutions (we hold no shares in National Bank) and our exposure to BMO is the least of all 5.

Based on my analysis, there is nothing wrong with having some exposure to BMO and the ~$13 drop in price since mid-March 2017 has now brought BMO to a level which I think represents reasonable, but not extremely attractive, value.

The risks posed by the cooling of BMO’s US growth and the overheated real estate market in major Canadian centres are not things investors should merely brush aside as immaterial risks, but I think BMO is prudently managing these challenges. I do suspect, however, there will be a correction in the Canadian real estate market and I also fall in the camp of those who suspect a major market pullback (also see here and here) will come about within the next 12 months.

I urge caution and suggest that if you intend to initiate or increase a position in BMO that your purchases be made in small tranches.

Note: I appreciate the time you took to read this article and hope you got something out of it. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long a few thousand shares of BMO, RY, TD, BNS, and CM. These holdings represent ~13.5% of our overall holdings and not just the FFJ Portfolio.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.

Well thought out & written article. Thank you. The banking sector (and utility sector) should be boring and profitable (buy & forget blue chip stocks). Dividend “laying” stocks 🙂

A quick question about portfolio construction. Which other sectors in your portfolio account for over 10%. I fear I’m over weighted in consumer staples and international at 18% each

Lovemydividends,

I did not convert the USD to CDN. I just took everything at par so the following %s are not ENTIRELY accurate but it will give you some idea as to the composition of our overall holdings. in addition, I have not broken out the holdings by registered vs non-registered.

CDN FI 20%, CDN Insurance 3.3%, CDN Real Estate 1.1%, CDN Services 0.6%, CDN Tech 1%, CDN Telecom 9.8%, CDN Transportation 2.4%, US FI 10.5%, US Healthcare 7.2%, US Industrial 11.3%, US O&G 9%, US Services 6%, US Technology 4.4%, US Telecom 3.2%, and US Consumer Goods 17%.

Hope this helps.