Summary

Summary

- This Royal Bank of Canada Stock Analysis is the second of a 6 part series covering the Big 6 Canadian Banks.

- RY reported strong Q2 2017 results May 25th with earnings by business segment and by geography reflecting a marginally greater % from Wealth and the US relative to FYE2016.

- RY’s Capital Measure Ratios are strong and the bank continues to be very well managed.

- Pockets of the Canadian real estate market are wildly overheated but RY’s results indicate its real estate related loan portfolio is of sound quality.

- RY is an attractive long-term investment but I suspect we will experience a major market correction within the next 12 months and urge caution.

All figures are expressed in Canadian dollars unless otherwise noted.

Introduction

The Royal Bank of Canada (NYSE: RY), Canada’s largest bank by market cap, reported Q2 2017 results on May 25th.

A high level overview of RY can be found here.

RY had a strong Q2 with earnings of ~$2.8B and solid growth across most of its lines of business as well as prudent risk management. Despite the uncertain operating environment, RY’s strong capital position enabled it to repurchase over 30 million common shares within the first 6 months of the current fiscal year.

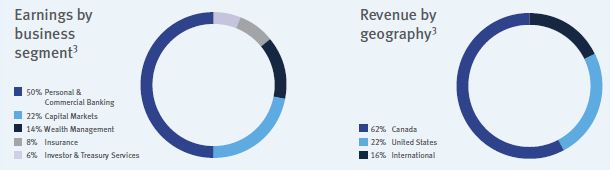

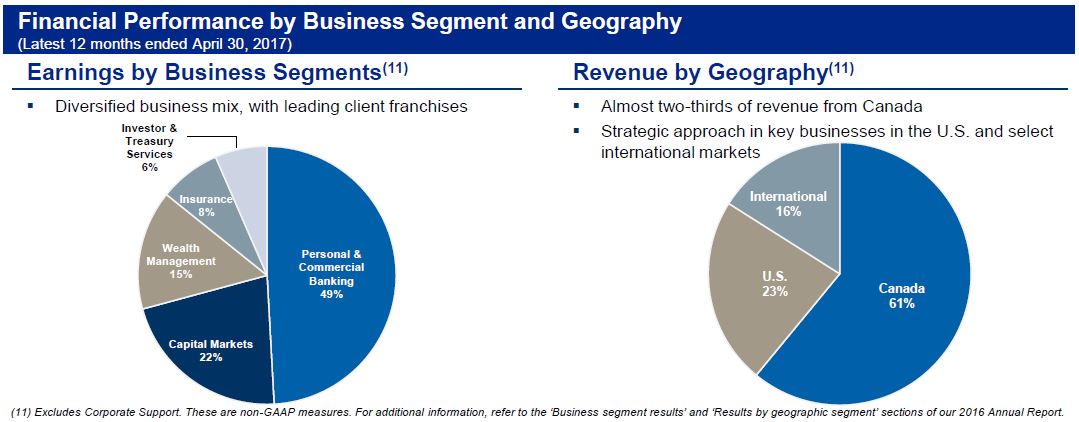

RY is making efforts to diversify its income by business segment and by geographical region. The following reflect results as at FYE2016 (October 31, 2016) and the most recent 12 months ending April 30, 2017.

RY – Earnings Breakdown as at FYE2016

RY – Earnings Breakdown as at Q2 2017

While I touch upon various topics that impact the Canadian Banking Sector and the top 6 Schedule I Canadian Banks, I strongly encourage you to listen to the RY segment of the March 29 and 30, 2017 National Bank Financial Markets – 15th Annual Financial Services Conference. There is far too much information covered in this ~30 minute segment for me to give the content justice in this post.

The Canadian Banking Sector

Details on the Canadian Banking Sector can be found here.

Technological Innovation

Details about the Technological Innovation the Canadian banks are undertaking can be found here.

RY Overview

A very high level overview is available on RY’s Q2 2017 Corporate Fact Sheet which can be found here. In addition, information about RY’s multiple acquisitions and divestitures over the years can be found here.

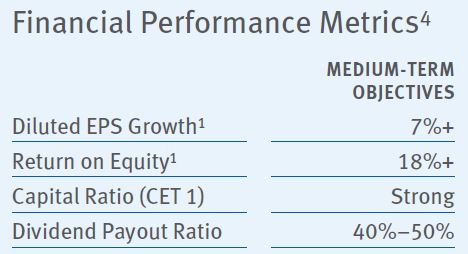

RY’s medium term financial objectives extracted from the 2016 Annual Report are reflected below.

RY Medium-Term Objectives

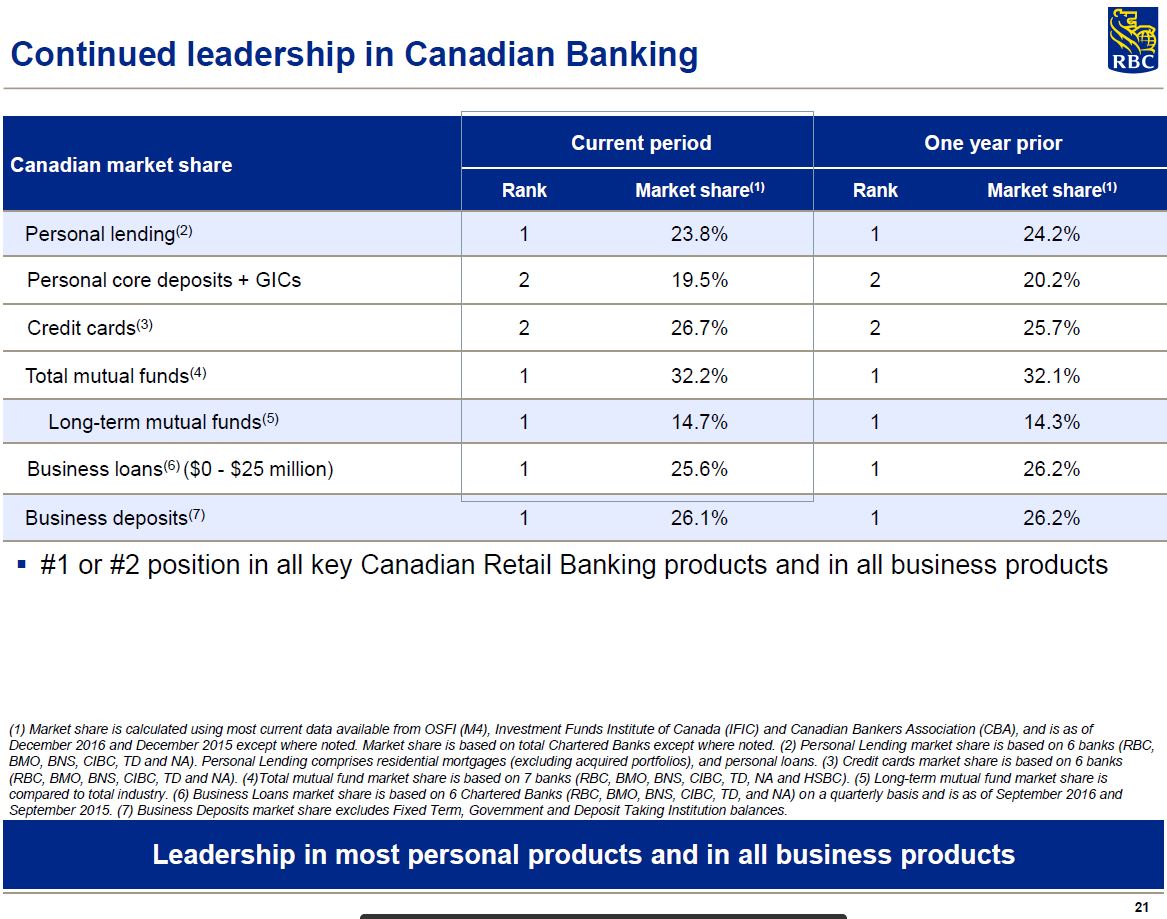

RY’s franchise includes a leading position in personal/commercial banking, wealth management, capital markets, and wealth management.

RY – Continued Leadership in Canadian Banking

It has a strong record of organic growth and, for the most part, has made well-timed strategic acquisitions in the US and internationally although its acquisition of Centura Bank in 2001 did not produce the desired results.

A strategic area of growth is in wealth management. In November 2015, RBC acquired City National in its efforts to create a leader in private and commercial banking and wealth management in the U.S..

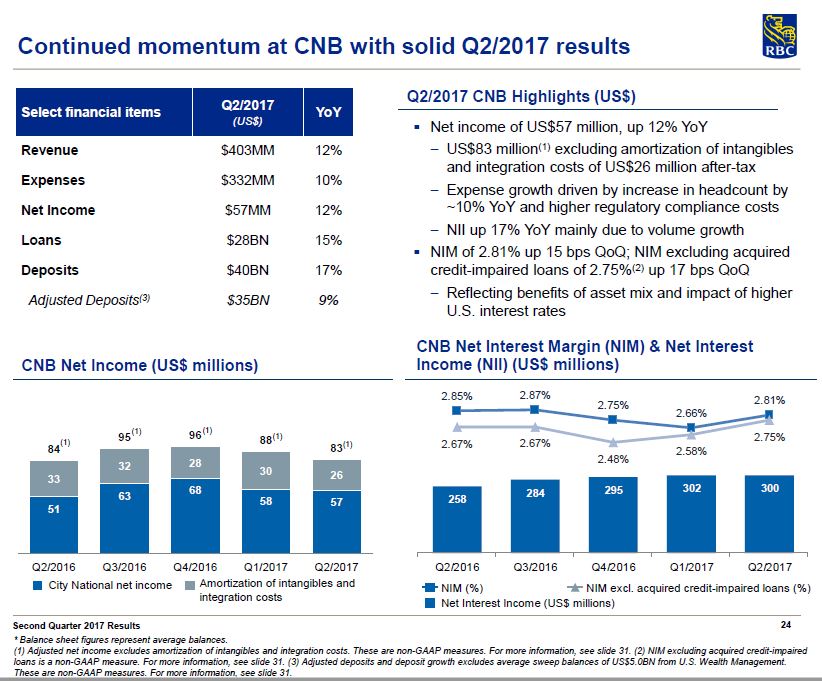

City National’s results for Q2 2017 and YoY are reflected below.

RY – Q2 2017 CNB results

RY has decided to focus on the highest-margin areas of wealth management rather than on traditional banking. An example of a recent divestiture because the line of business did not fit into RY’s long-term plans is the recent sale of a 50% interest in Moneris Solutions USA.

Q2 2017 Financial Results

Readers are encouraged to review RY’s May 25, 2017 Earnings Release and to listen to the conference call.

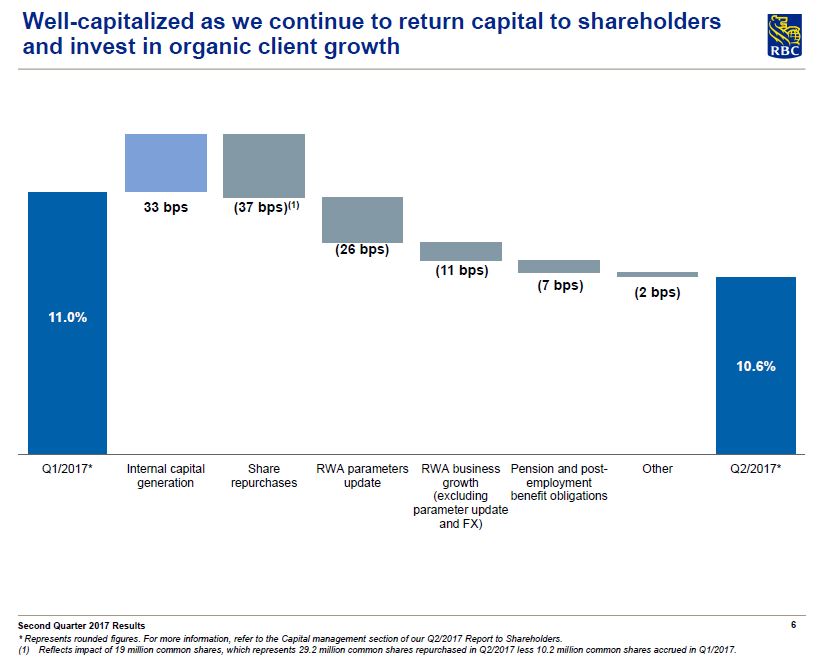

Capital Measure Ratios

In addition to touching upon the Capital Measure Ratios for RY, you can find more information here.

RY – Capital Measure Ratios

RY – Well Capitalized

Recent Events in the Canadian Banking Sector

A brief overview about a few major Recent Events in the Canadian Banking Sector can be here.

Inflated Real Estate Values

Given the impact the US real estate bubble had on the US Banking sector, it is only fair that people should be wondering what would happen to the Canadian financial institutions if the grossly inflated real estate values in various major centres in Canada were to experience a correction.

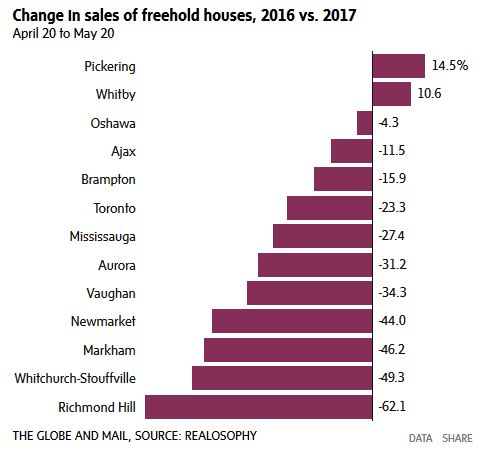

Multiple articles have been published about the state of certain pockets of the Canadian real estate market and how consumers are stretched financially. Recently, more articles have appeared about the sudden cooling of the real estate market.

Change in Sales of Freehold Houses 2016 vs 2017

In addition to my opinion on this topic which can be found here, I have very recently attended Open Houses (a community on the outskirts of Toronto) so I could speak with various real estate agents and brokers. All have indicated they have noticed a marked change in the last couple of months. Buyers appear to be less aggressive and in all cases, Open Houses are getting much less foot traffic. They have also commented that there is concern that some buyers may be willing to risk the loss of their deposit and will just walk away from their offers.

RY’s Canadian Real Estate Secured Lending and Personal Banking Portfolios

With all the concerns about the average Canadian consumer being stretched financially and the inflated real estate values in specific geographic pockets within Canada, the major Canadian financial institutions have provided more information regarding the composition of their respective real estate related loan portfolio.

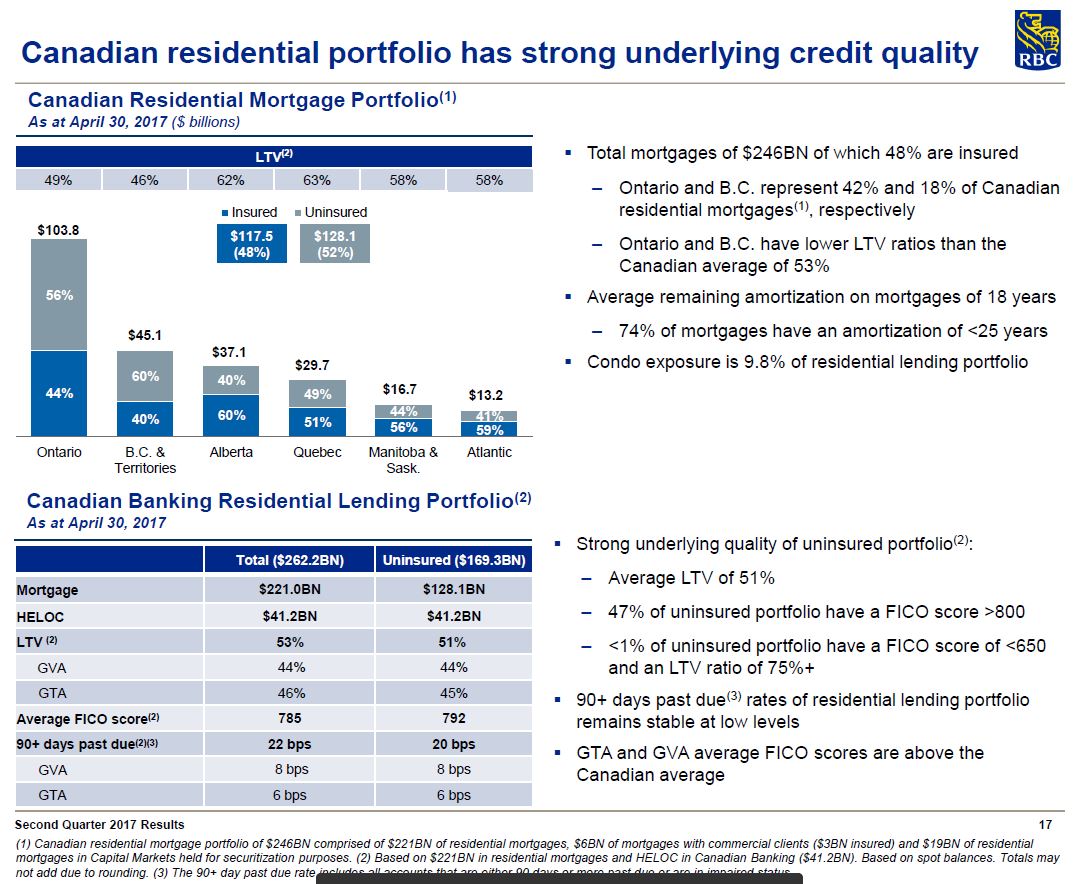

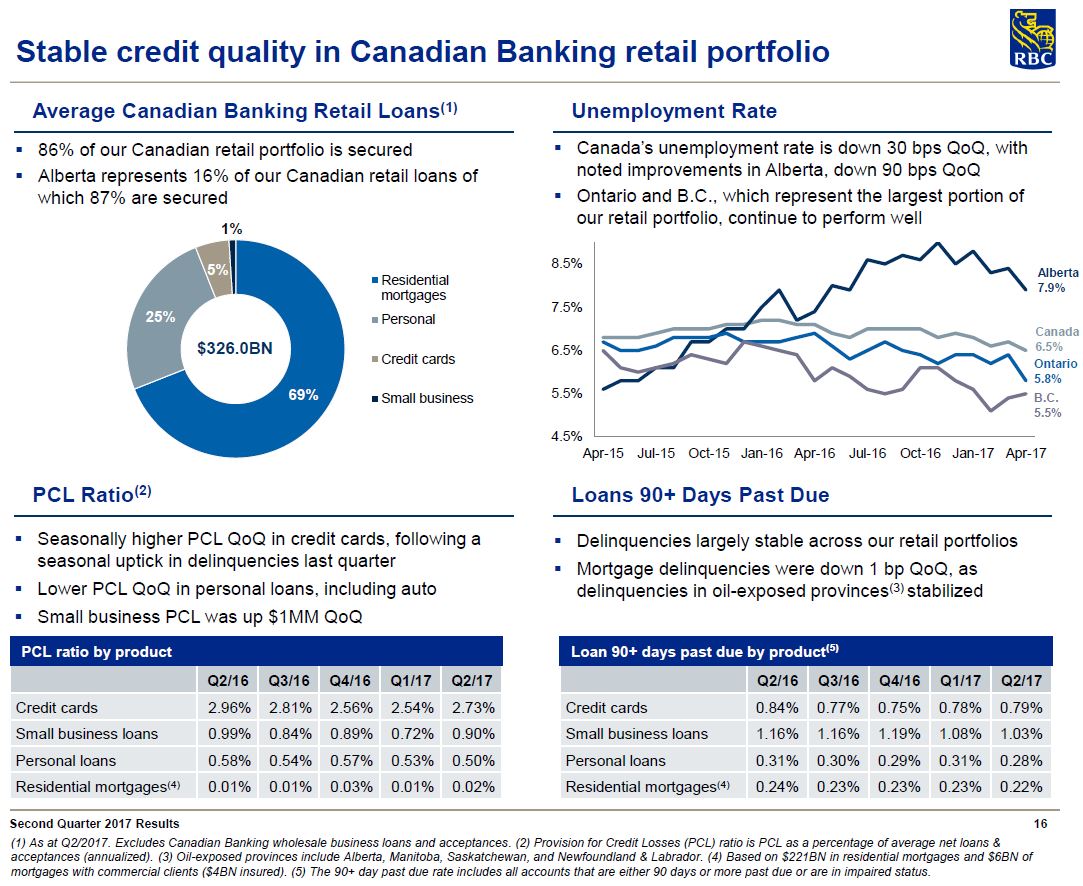

The following data was included in RY’s Q2 2017 Earnings report.

RY – CDN Residential Portfolio Q2 2017

RY – Stable Credit Quality Q2 2017

While 52% of RY’s real estate portfolio consists of uninsured mortgages, the Loan to Value ratio averages 51% and 47% of borrowers with uninsured mortgages have FICO scores in excess of 800. In Canada, credit scores range from 300 (just getting started) up to 900 points, which is the best score. According to TransUnion, 650 is the magic middle number; a score above 650 will likely qualify you for a standard loan while a score under 650 will likely bring difficulty in receiving new credit.

RY’s Provision for Credit Losses and Loans 90+ days past due appear to be well controlled. Naturally, if we enter an economic downturn we can certainly expect to see an increase from current levels. At the moment, however, there is no cause for alarm but caution is definitely warranted.

Risk Management

There are a host of risks the Canadian financial institutions face. Global uncertainty, Brexit, Oil & Gas, Cyber risk, anti-money laundering, renegotiation of NAFTA, and the increasing complexity of regulation are just a few of these other risks.

I recommend you review the 32 page “Quarterly Slides” presentation found here as there are multiple pages that provide details addressing the quality of RY’s loan portfolio. In addition, there are multiple pages in RY’s 2016 Annual Report addressing RY’s Risk Management. Page 8 of the Annual Report lists the locations of the disclosures within the report.

Dividend

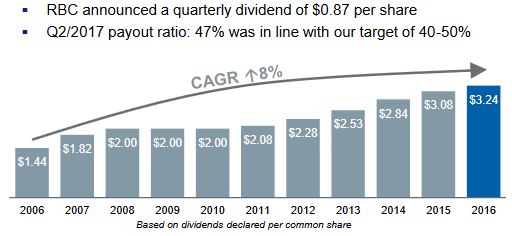

Unlike many foreign banks which were forced to dramatically reduce or suspend their dividend during the Financial Crisis, RY and its Canadian counterparts froze their quarterly dividend.

In mid-2011, RY reinstated dividend increases albeit with some modification. In lieu of a one-time dividend increase on an annual basis, RY opted to go with a lower dividend increase at the outset of the year followed by a second dividend increase mid-way through the year.

RY’s dividend distribution history dating back to the beginning of 2000 can be found here. RY’s next quarterly $0.87 will be distributed August 24th.

RY – Dividend History

RY is another Canadian financial institution with a lengthy history of uninterrupted quarterly dividend payments. The likelihood of a dividend cut or elimination is remote so investors seeking a safe dividend and a respectable dividend yield (~3.7% as I compose this) would be well served acquiring RY shares at current levels.

Valuation

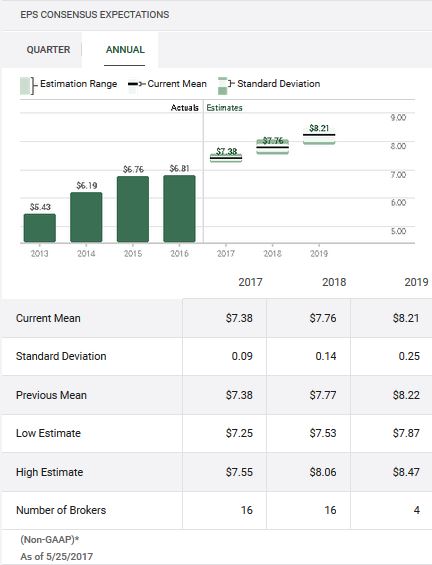

The current mean FY2017 adjusted EPS estimates from various brokers for fiscal 2017 is $7.38.

RY – TD WebBroker EPS Estimates

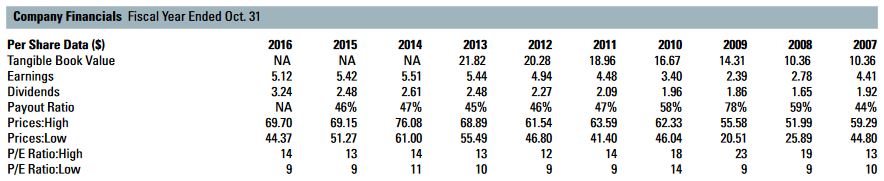

RY – High Low PE Ratios

As I compose this post, RY is trading at ~$93.75 on the TSX thus giving us a forward PE of ~12.70. When I look at the high/low PE ratio levels for the past several years I view the current level as acceptable and would consider adding to our existing position. In fact, we DRIP all our RY dividends and have just acquired several more shares by reason of the May 24th dividend payment.

Royal Bank of Canada Stock Analysis – Final Thoughts

In my opinion, RY is an ideal holding within a well-balanced and well-diversified portfolio if you are an investor with a long-term perspective. While RY is prudently managing its loan portfolio, has a strong capital base, and is reasonably valued at current levels, my major concern at this stage is that I suspect a major market pullback (also see here and here) will come about within the next 12 months. I, therefore, urge caution and suggest if you intend to acquire RY shares in the near-term that your purchases be made in small tranches. In the event a major market correction materializes, I would back up the truck and load up on RY.

Note: I appreciate the time you took to read this article and hope you got something out of it. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long a few thousand shares of BMO, RY, TD, BNS, and CM. These holdings represent ~13.5% of our overall holdings and not just the FFJ Portfolio.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.