Summary

Summary

- This Brookfield Asset Management Stock Analysis is based on Q1 2017 financial results reported May 11, 2017.

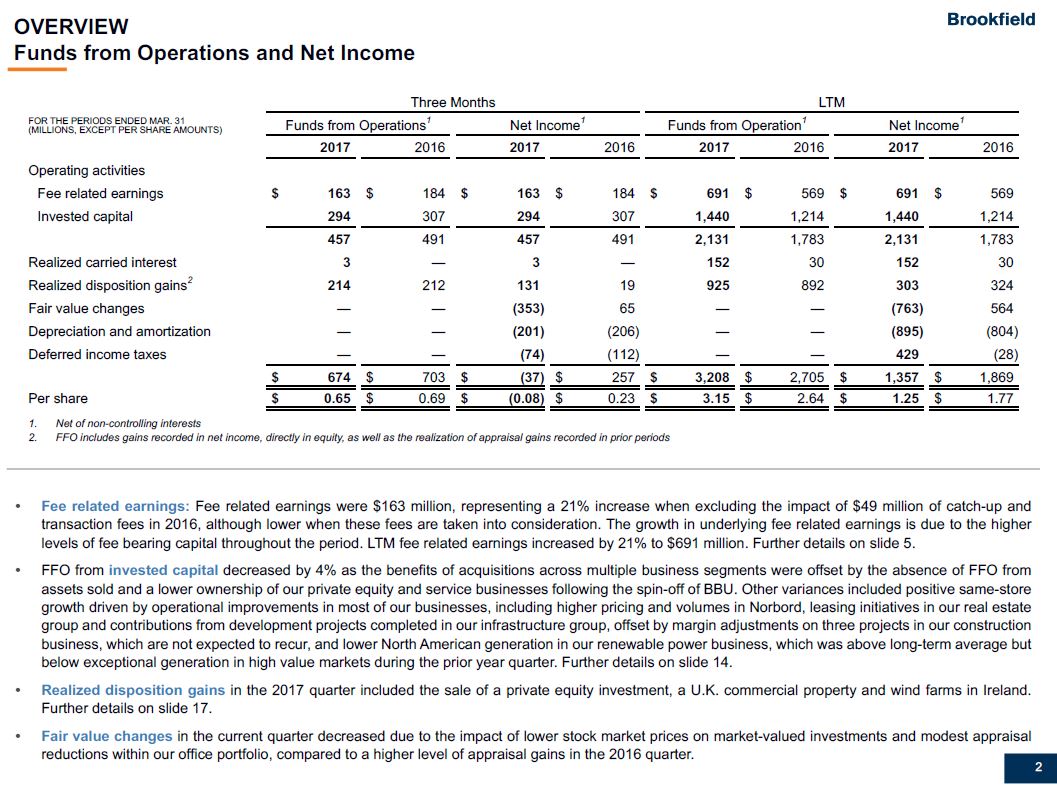

- Brookfield reported FFO of $0.674B for Q1 2017 and $3.2B on a last 12 month basis.

- On May 19, BAM received approval from the TSX for its proposed normal course issuer bid to purchase up to ~83 million Class A Limited Voting Shares, representing 10% of the public float.

- Brookfield is not inexpensive but is worth acquiring at current levels when you look at its long-term growth potential.

Introduction

This post is a follow-up to my February 10, 2017 Brookfield Asset Management (NYSE: BAM) post wherein I expressed an opinion that BAM represents a solid investment for investors with a focus on long-term wealth creation.

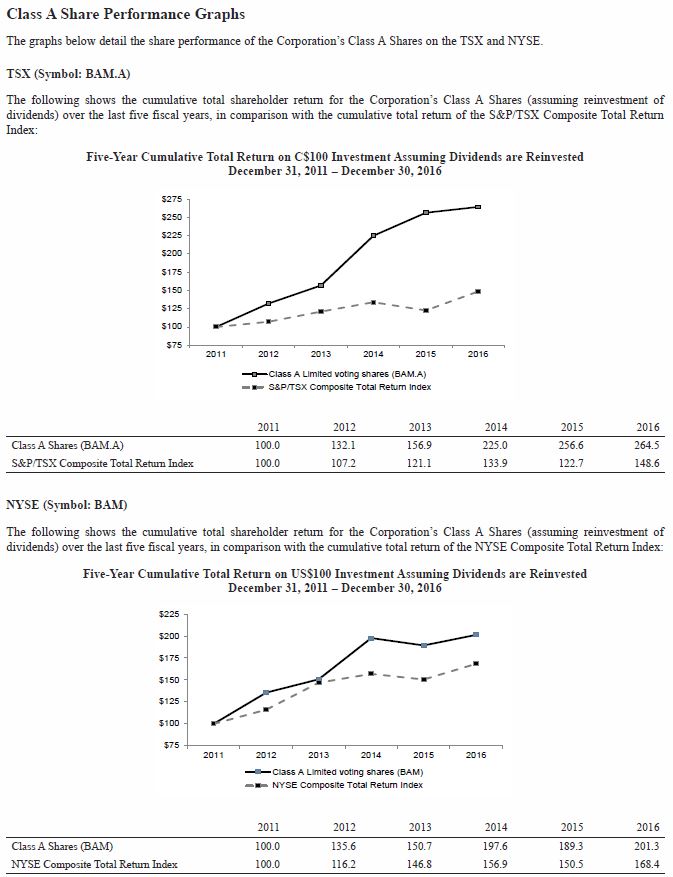

We initially acquired shares in TSX: BAM.a in February 2009, and therefore, have first-hand experience of BAM’s success. I also provide the following two graphs from BAM’s recently released Management Information Circular which attests to BAM’s impressive returns over the recent years.

BAM – Class A Share Performace Graphs

I recognize that while the past does not predict the future, it certainly lends some comfort knowing that BAM has a proven successful track record.

Overview

Over the last ~8-9 years, BAM has gradually transitioned from actually owning assets directly for its own portfolio to becoming a fee generating advisor. As part of this transition, the following divisions were taken public beginning in 2008.

- Brookfield Property Partners (NYSE: BPY) (TSX: BPY.UN) – Ownership Interest: 63% (fully diluted)

- Brookfield Renewable Partners (NYSE: BEP) (TSX: BEP.UN) – Ownership Interest: 61%

- Brook field Business Partners (NYSE: BBU) (TSX: BBU.UN) – Ownership Interest: 75%

- Brookfield Infrastructure Partners (NYSE: BIP) (TSX: BIP.UN) – Ownership Interest: 30%

Collectively, the 5 public entities have a market value in excess of $56B.

BAM’s stakes in the four entities feed BAM with a perpetual and growing stream of cash. It generates fixed fees plus a 1.25% annual management fee based on the value of its listed partnerships and performance fees of 15% to 25% based on the level of the dividends. Add in dozens of private funds in which BAM is usually a 20% investor and BAM is generating ~$1.1B annually in fee revenues. This is a 31% YoY increase and a 160+% gain from 2012; BAM expects it will generate $2.4B in annual fees by 2021.

In addition to the annuity of fees generated from the management of third party funds, the BAM structure is such that funding never has to be returned to investors. Because permanent capital is built into its public vehicles, roughly half of BAM’s funding never has to be returned to investors. This allows investments to grow on a compounded basis.

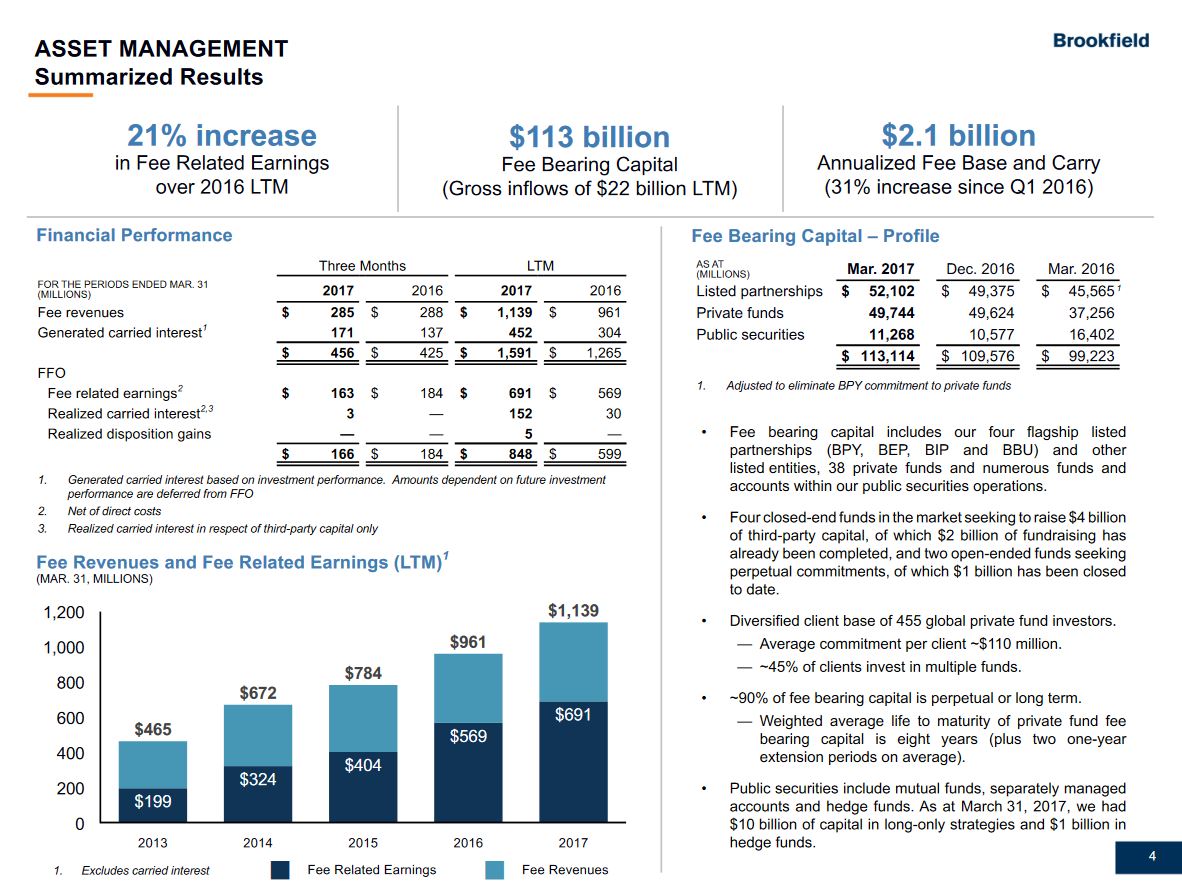

Q1 2017 Financial Results

Readers are encouraged to review BAM’s results reported in its May 11, 2017 Earnings Release, the Q1 2017 Supplemental Information document, and the Q1 2017 May 11, 2017 Conference Call Transcript.

BAM – Q1 2017 Summarized Results

- In addition to the free cash flow generated, BAM and its permanent capital partnerships have ~$10B of liquid financial assets and term bank lines. Coupled with ~$20B of commitments to its private funds, BAM has ~$30B for future investments.

- BAM continues to allocate capital disproportionately to the emerging economies where it feels it can still acquire assets of very good value in slowly recovering economies.

- BAM manages the business for the long-term, and therefore, places greater focus on long-term metrics; its goal is to generate 12% to 15% long-term compound returns.

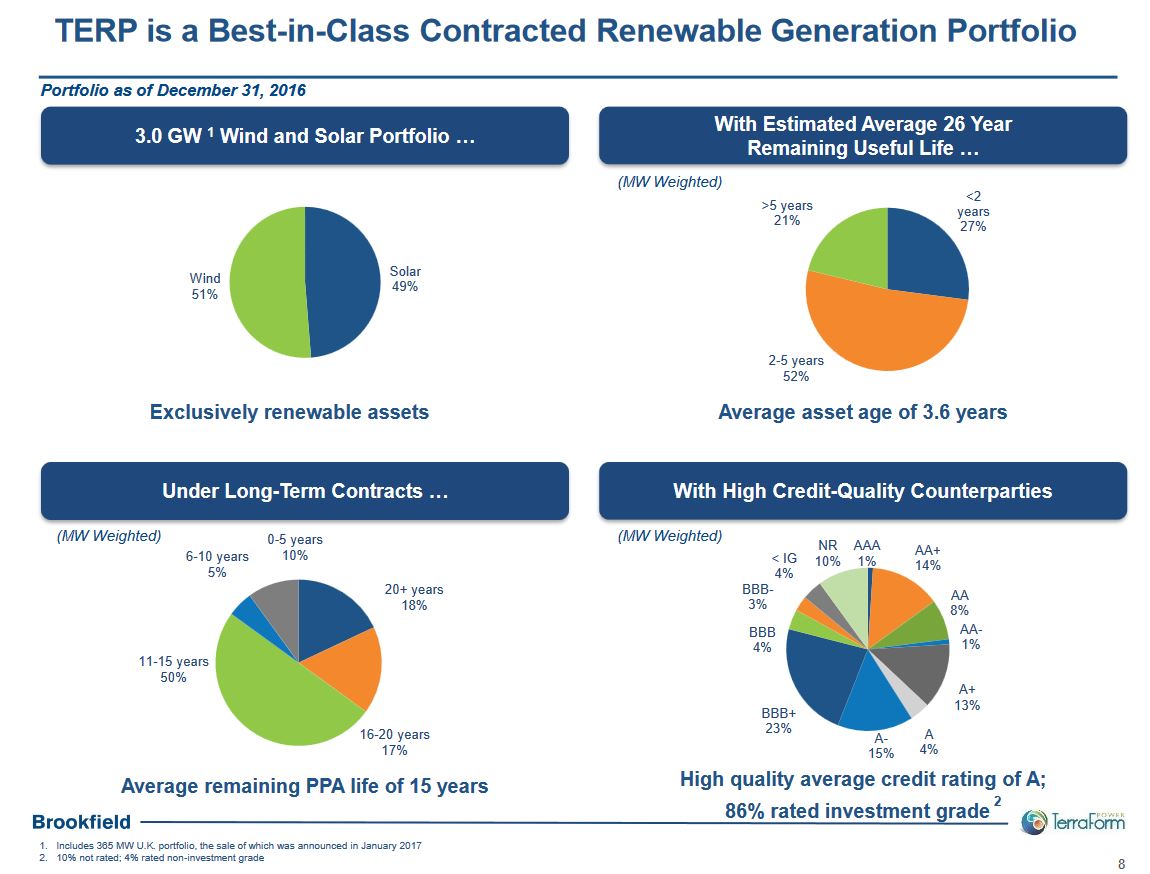

TerraForm Acquisition

In Q1, BAM successfully closed a number of transactions totaling ~ $10B of investments and it advanced the $1.4B acquisition of TerraForm Companies (NASDAQ: TERP) for its renewable power business which it hopes to close later in 2017. Details of the TerraForm investment can be found in this March 7, 2017 Press Release.

BAM – TERP Renewable Generation Portfolio

Trisura Guarantee Insurance Company

BAM has owned Trisura Guarantee Insurance Company, a property and casualty insurance business, for ~10 years. This entity is in the business of writing specialty insurance policies and it has consistently and profitably grown its operations over the years. It also specializes in providing surety bonding for smaller contractors. The business is regulated, stands on its own, has been run very conservatively, and it reinsures most of the exposures and only assumes underwriting risk in a measured way.

BAM deemed this business to no longer be strategic given the focus on its asset management operations. Since the sale of Trisura was viewed as being too disruptive and unlikely to generate an offer that would fairly value the business, BAM has decided to combine this business with the rest of its small specialty insurance operations and will spin them off from BAM under the brand name Trisura Group.

Details of the spin-off can be found here.

Normal Course Issuer Bid

On May 19th BAM announced it had received approval of the renewal of its Normal Course Issuer Bid in which it can purchase up to 82,965,721 Class A Limited Voting Shares between May 24, 2017 – May 23, 2018 or an earlier date should BAM complete its purchases; this represents 10% of the public float of BAM’s outstanding Class A Shares.

As a long-term BAM investor, I am fully in favor in the reduction in the number of shares outstanding. I suspect, however, that BAM is unlikely to repurchase in excess of $3.1B of Class A Limited Voting Shares (82,965,721 x $37.50) over the upcoming 12 month period!

Dividend

BAM’s recent dividend distribution history can be found here.

BAM’s Board declared a dividend of $0.14/share/quarter or $0.56/share/year payable at the end of June 2017. This represents an annual dividend yield of ~1.5%.

Many readers prefer to invest in securities having a far better yield. In this case, an investment in one of BAM’s 4 divisions referenced in the Introduction section of this post may be more attractive than an investment in BAM.

While there is absolutely nothing wrong with a direct investment in the divisions, I prefer to invest at the “top of the house” for the following reasons:

- I need to ensure our portfolio holds a balance between income and growth holdings and I suspect that over the long-term BAM will have greater potential for capital appreciation than the 4 divisions.

- BAM’s revenue income stream is far more diversified than each division on a stand-alone basis.

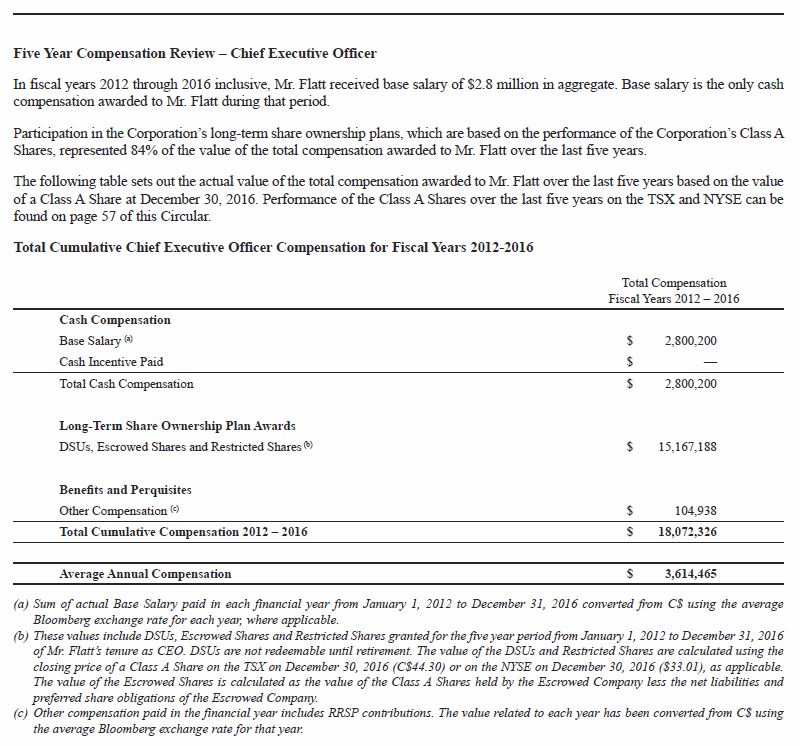

- A significant proportion of BAM’s CEO’s (Bruce Flatt) compensation for the fiscal 2012 – 2016 period consisted of Deferred Share Units, Escrowed Shares, and Restricted Shares in BAM. The following 5 year compensation review extracted from the 2017 Management Information Circular disseminated to all shareholders confirms a significant proportion of his compensation is dependent on BAM’s future success.

BAM – Bruce Flatt (CEO) compensation

Valuation

As at the date of this post, the FFO/Stock Price ratio is ~12 (~$37.50 May 19, 2017 closing stock price/BAM’s last 12 months FFO of $3.15/share) – refer page 3 of BAM’s Q1 2017 Supplemental Information document.

BAM – FFO Q1 2017

This level is comparable to the FFO/Avg. Stock Price for 2012 – 2016 with the exception of fiscal 2013.

BAM – FFO to Avg Stock Price

While BAM is not inexpensive by any stretch of the imagination, it is not currently unreasonably priced when you look at BAM’s long-term growth potential.

Brookfield Asset Management Stock Analysis – Final Thoughts

BAM is certainly not an easy to understand entity and this post provides no justice in trying to explain the shrewdness and sophistication of BAM’s long-term strategy and overall operations.

If you happen to be a reader who has come away disappointed that I did not go into any “technical” analysis, please accept my apologies. I, however, view technical analysis as something more relevant to short-term investors. I happen to be focused on investing for the next generation. This time frame, coincidentally, is similar to that of BAM as evidenced by Bruce Flatt’s comment on the eve of the Financial Crisis in 2007:

“Forget the gloom. Pipelines, wireless towers, power generation, ports and toll roads–the backbone of the global economy–would soon become the holy grail investment product for trillions of dollars stagnating in pension funds and savings. “David [Rosenberg’s] presentation is probably about the next six months,” Flatt told the doomsday-obsessed audience. “Mine is more relevant to the next 25 to 60 years.”

The following are factors I have also taken into consideration in my ultimate decision to periodically add to our BAM holdings:

The following are factors I have also taken into consideration in my ultimate decision to periodically add to our BAM holdings:

- Members of BAM’s senior management team have a significant vested interest in BAM’s success.

- Historically, BAM had to actively seek out investors. In recent years, however, BAM’s successful track record now means investors seek out BAM for its “best in class” management expertise; BAM has a diversified client base of ~455 global private fund investors.

- BAM has a reputation of being an opportunistic investor. It has the skill set to seek out longer dated infrastructure, renewable power, and real estate assets in geographic regions where other investors are reluctant to venture.

Finally, it is entirely possible the following observations made in an article in the May 16, 2017 issue of Forbes magazine may not resonate with you. They do, however, resonate with me as I have grown tired of stories about senior executives leading an extravagant lifestyle at the expense of company shareholders.

“Bruce Flatt is an accountant from Manitoba who lives in a quiet Toronto neighborhood and often commutes by subway.” Note: I have personally seen Mr. Flatt commuting to work on the Toronto subway (TTC).

“Modest home? He lives in a two-story brick townhouse barely set back from the sidewalk. Humble office? A drab gray cubicle, positioned against a window looking onto a courtyard of an office complex that Brookfield owns. Contrarian outlook? The only piece of art visible from Flatt’s desk is a framed cartoon depicting a herd of white sheep moving toward a cliff as a single black sheep heads in the opposite direction.”

I would like to think I am not the only “average small time investor” who wishes more CEOs would lead less extravagant lifestyles that are ultimately financed by shareholders of the companies they oversee!

Note: I appreciate the time you took to read this article and hope you got something out of it. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long a few hundred shares of BAM.a, BPY.un, BBU.un. These holdings represent ~0.5% of our overall holdings and not just the FFJ Portfolio.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.

Great article. Very Insightful! I bought BAM when it was trading slightly below book value (I should have bought more). I need to increase my position.

The investment team at BAM have an excellent track record of investing during distressed markets. They scored several home runs during the last financial crisis. They purchased premium assets from highly motivated “desperate” (institutional) sellers. These transactions were made at significant discounts to the assets historic value. Similar value oriented approach Mr Buffet used to acquire the companies in Berkshire’s portfolio. But the guys at BAM keep a much lower profile.

Glad you liked it.

I am currently working on a series of posts about the 6 largest Canadian financial institutions (RY, TD, BNS, BMO, CM, NA). Each post is in order of the date they release their Q2 results.

NA is the last of the group to release their results (May 31st). The posts will come out probably June 2nd.

Do you have a site I can look at?

Cheers.