Summary

Summary

- This VF Corporation stock analysis is based on Q4 and FY 2016 results and the outlook for fiscal 2017 which were released February 17, 2017.

- Market conditions continue to be extremely challenging.

- VFC is unlikely to hit many of its 17X17 key targets which it introduced to shareholders in June 2013.

- VFC continues to reward shareholders with attractive annual dividend increases but this is small consolation for investors who acquired shares 2014 – 2016.

- I do not view VFC as a company I will be acquiring any time soon.

Introduction

I have never owned shares in VF Corporation (NYSE: VFC) nor has it ever been on my radar screen although I wish it had been many, many years ago.

Recently I was shopping for a new ski jacket and winter boots for my upcoming ski trip in British Columbia and noticed several of VF’s brands. This prompted me to look into VFC more carefully and it was certainly fortuitous that it released its Q4 and FY2016 financial results on February 17, 2017.

In this post I will examine whether VFC would be a worthwhile addition to the FFJ Portfolio.

Who is VF Corporation?

VFC was formed in 1899. It designs, manufactures, markets and distributes branded lifestyle apparel, footwear and related products. Over the course of time, VFC has grown to become a global leader in branded lifestyle apparel, footwear and accessories, global iconic brands, 62,000 associates and $12B in revenue.

The Company’s segments include Outdoor & Action Sports, Jeanswear, Imagewear, Sportswear, Contemporary Brands and Other. It owns a portfolio of brands in the outerwear, footwear, denim, backpack, luggage, accessory, sportswear, occupational and performance apparel categories.

The following image reflects VFC’s brands and has been updated to reflect those which have been SOLD or in which it took a Pre-Tax Goodwill and Intangible Assets Impairment Charge.

VFC Brands

On June 11, 2013, VFC introduced its 17X17 strategy wherein senior management provided details on how it intended to attain global sales of $17B by 2017.

VFC 17X17 Strategy

VFC 2017 Revenues

VFC 2017 Gross Margin

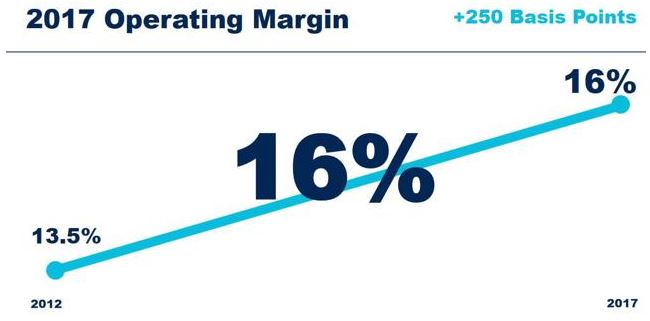

VFC 2017 Operating Margin

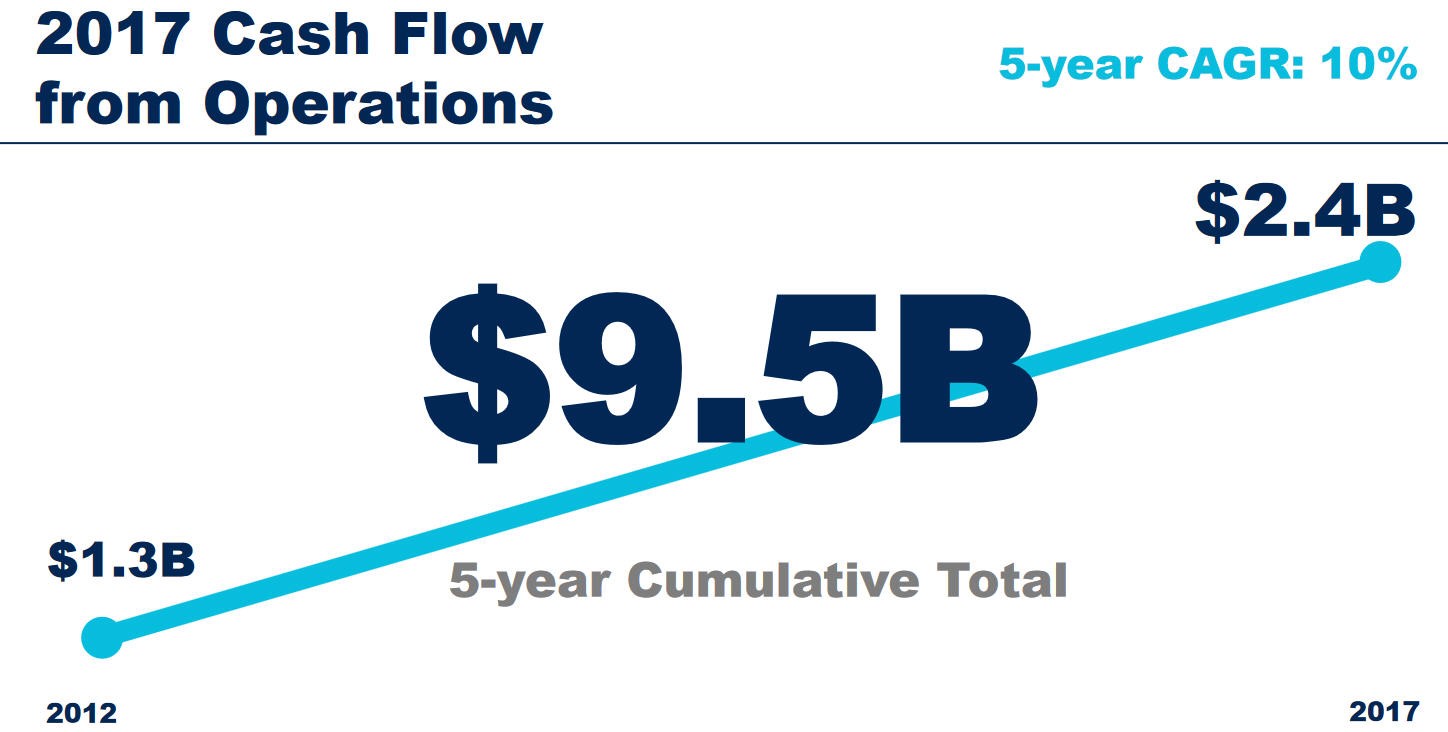

VFC 2017 Cash Flow from Operations

VFC 2017 EPS

Growth was expected to come from four key growth drivers.

- Innovation: a constant stream of new and better products, new and better store environments, new and better digital experiences.

- Connect with Consumers: invest more in developing and refining consumer insights and do it better than anybody else in the industry.

- Serve Consumers Directly: serve consumers in the manner in which they which to engage with VFC’s brands. Recognize consumers are completely in charge of their relationship with the company. Ensure total effectiveness in stores, through ecommerce, at partner stores and through social media.

- Expand Geographically: growth potential remains in the more mature US and European markets, however, there is abundant opportunity in emerging market. Double international business over the next 5 years.

When I read the transcript of the President and CEO’s presentation, I see that in 2011 management announced the 5 year plan which was simply to grow VFC by $5B and $5 in EPS by 2015. The acquisition of Timberland and SmartWool certainly helped at the time of the announcement but now that this is 2017, let’s see how VFC has executed relative to various metrics under its 17X17 plan that were presented June 11, 2013.

Q4 and FY2016 Results

Highlights of VFC’s results can be found in its February 17, 2017 Earnings release. A few are reflected below for ease of reference.

- FY revenue from continuing operations comparable to 2015 at $12B while FY international revenue increased 4% percent but up 6% currency neutral.

- FY Gross Margin improved 20bps to 48.4% and 40bps to 48.6% on an adjusted basis with changes in FX negatively affecting reported and adjusted gross margin by almost 80bps.

- FY EPS from continuing operations down 9% to $2.78 while adjusted EPS was up 2% to $3.11 – up 7% when impact of foreign currency changes are excluded.

- FY cash flow from operations reached almost $1.5B and more than $1.6B returned to shareholders through dividends and share repurchases.

When I compare these results to the screen shots reflected in the previous section, VFC definitely has some challenges if it intends to hit the targets it set out for itself.

Outlook for Fiscal 2017

Before the February 17, 2017 Earnings release, one of the concerns I had with VFC’s business was the extent to which technology would be impacting its business. Sure enough, this area of concern is definitely on VFC’s radar screen as it grapples with changes in the industry and the ever increasing changes in the consumer landscape.

As noted by VFC’s President and CEO, “The proliferation of technology and innovation across all aspects of our lives has shifted consumers’ shopping behaviors and elevated their expectations when engaging with our brands. We are pivoting to become more agile and consumer centric to compete and win in this changing global marketplace.”

Highlights of VFC’s outlook for the current fiscal year are:

- Overall revenue for FY2017 is expected to increase at a low single-digit % rate which includes about a 2% negative impact from changes in foreign currency.

- Gross margin is expected to be about 48.6% and is consistent with 2016 gross margin on an adjusted basis and includes about a 70bps negative impact from changes in FX.

- Operating margin is expected to approximate 14% including about a 70bps negative impact from changes in FX.

- EPS is expected to be down at a low single-digit % rate compared to 2016’s $3.11 adjusted EPS (up at a mid-single-digit percentage rate on a currency neutral basis).

- Cash flow from operations is expected to reach $1.5B and VF expects to once again return more than $1.6B to shareholders through share repurchases and dividends.

- An effective tax rate in the low 20% range is once again expected and capital expenditures are forecast to be $225 Million.

Well….those projections certainly do not give me any comfort that VFC is going to hit several key 17X17 targets.

Dividend History

VFC investors who stepped into the VFC party in 2014 – 2016 certainly do not have too many reasons to rejoice. Many investors are likely underwater at this stage but I recognize that if you are a disciplined investor with a long-term investment time horizon, 2 – 3 years is immaterial.

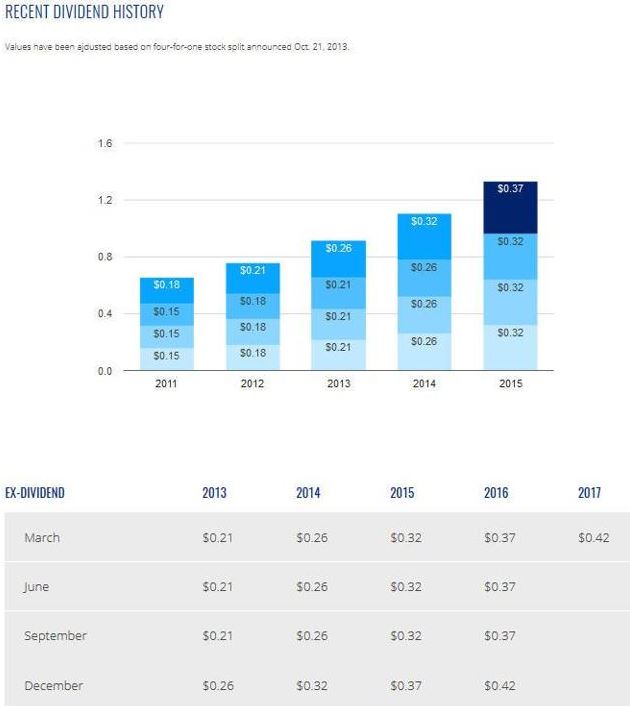

If there is any consolation, at least VFC has rewarded investors with a consistent increase in its quarterly dividend of $0.05/share. Your annual $0.89 dividend in 2013 jumped to $1.53 in 2016 and if history is any indication of what to expect on the dividend front in 2017, investors will likely receive a total of $1.73 ($0.42 x 3 quarters plus $0.47 in the last quarter).

VFC Dividend History

Valuation

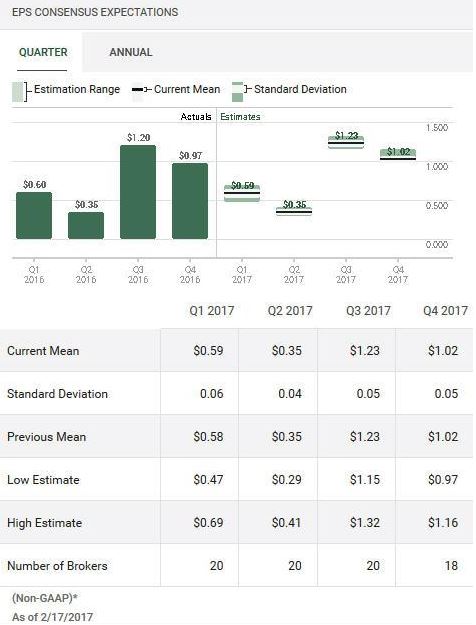

The Mean EPS from 23 analysts which I generated from TD Bank WebBroker reflects $3.19 as the projected 2017 adjusted EPS. The Mean EPS derived from ValuEngine which is based on input from 22 analysts reflects $3.36. This $3.36 appears high given that management has given guidance that suggests 2017’s adjusted EPS will be a mid-single-digit increase from the 2016 level of $3.11.

Source: TD WebBroker – VFC Quarterly EPS estimates

Source: TD WebBroker – VFC Annual EPS estimates

Source: ValuEngine – VFC Quarterly EPS estimates

Source: ValuEngine – VFC Annual EPS estimates

If I take $3.11 and increase this by 5% – 6%, I get a projected adjusted EPS range of $3.27 – $3.30. I will use $3.27 to be conservative (so much for that $4.50 EPS projection for FY2017!).

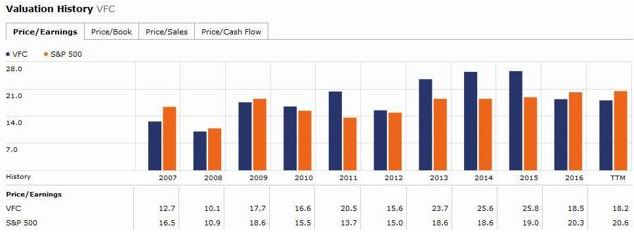

As I compose this, VFC’S shares are trading around $52.68 so I get a forward PE of 16.11.

Source: Morningstar – VFC PE ratios vs S&P500

Given that VFC’s top line is not growing as in the past and it is highly unlikely it will hit many of the key targets it set for itself a few years ago, I think a forward PE of 16.11 is too rich. I certainly have no intention of purchasing VFC but if you still intend to do so, I would be inclined to wait for VFC’s stock price to pull back to the upper $40s. If I use a stock price target of $48 and the adjusted EPS of $3.27, the forward PE drops to 14.67 which, in my opinion, is more reasonable.

As noted in the Dividend History section of this post, I project a dividend of $1.73 for 2017. Using a stock price of $48, that would lead to a dividend yield of 3.60% versus 3.28% based on the current price of $52.68.

If, after my analysis, I had decided I was going to go through with a VFC purchase, I would have had to adjust these calculations to take into consideration a 15% withholding tax I will incur as a Canadian citizen. If you are a Canadian citizen and want to avoid this withholding tax, you could purchase VFC in your Registered Retirement Savings Plan (RRSP) or Registered Retirement Income Fund.

In our circumstance, our Financial Advisor has suggested that for tax planning reasons we should stop contributing to our RRSPs. Any investments going forward should continue to be transacted through our Tax Free Savings Accounts (TFSA) or non-registered accounts. If we were to hold VFC in either of these accounts, our net annual dividend would end up being $1.47 or 85% of $1.73. So, if we were to acquire VFC at $48, our dividend yield would be 3.06% versus 3.60%.

I would also need to take into consideration that the US Dollar relative to our Canadian dollar is not nearly as favorable as when we acquired a significant percentage of our US holdings several years ago. Back then, our Canadian dollar was either stronger than or close to par with the US dollar. As I compose this, it takes roughly CDN$1.32 to acquire USD$1.

Given that I think the US Dollar is overvalued and my thought appears to be supported by a recent Bank of America Merrill Lynch Global Fund Manager Survey, I do not view this as a time to be buying US shares of any magnitude. I must confess, however, that I have made a couple of small purchases with surplus money which has accumulated in some of our RRSPs to increase some of our US holdings.

VF Corporation Stock Analysis – Final Thoughts

I have no intention of acquiring VFC after analyzing this company. I recognize many readers may have a different take on VFC but it is certainly much easier to be stoked about this company if you acquired your shares pre-2011.

I do not see the challenges VFC is currently experiencing as going away in the near future. Some readers may be willing to live with VFC’s “headwinds” and will focus primarily on VFC’s dividend. If this happens to be you, I would wait for the price to drop to at least $48; VFC was $48ish earlier February 2017. I am more confident it will revisit this low far sooner than it will revisit its 12-month high in the mid $60s.

I am also of the opinion a market correction is long overdue. If interest rates start to tick upwards in 2017, I think stocks acquired primarily on the basis of an attractive dividend yield will take a hit.

As for the ski jacket and winter boots I purchased….they were NOT VFC brands.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I do not own VFC and have no intention of acquiring VFC in the foreseeable future.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.

IH,

I see a line item in the middle of your stock portfolio which reflects 495 shares, a MV of $32.5M, a weighting of 14.82%, and an overall cost basis of $0. What’s that?

I see you were born in the SF area. Not sure if you still live there. If you do, it appears it is a “little wet” there at the moment. Hope all the rain ends soon.

Appreciate your take on VFC and analysis. No doubt the company is facing issues in the near term but I will continue to hold. I first started buying this stock in late 2007 and plan to keep it for the foreseeable future in my portfolio as long as those dividends continue to roll in.

DH,

If you have held on to the shares you started buying in late 2007 you should do just fine. Those who jumped on the VFC bandwagon in 2014 – 2016 don’t have the same luxury as you.