![]()

This article analyses SmartCentres REIT (SRU.un), a high quality REIT listed on the TSX.

Summary

- SmartCentres’ purpose is to develop, lease, construct, own and manage conveniently located and well designed shopping centres and office buildings.

- The Trust is diversifying its portfolio and continues to work on opportunities to provide various forms of residential housing, seniors housing and also self storage facilities at many of its shopping centre properties across Canada.

- Management continues to seek opportunities to fix interest rates, secure longer-term financing when appropriate, and increase the REIT’s unencumbered asset pool with the ultimate goal of enhancing its current BBB (mid) credit rating.

- There are various methods of valuing a company. The dividend yield theory works well under certain conditions.

- SRU.un has an attractive distribution which is well covered by FFO and ACFO but units appear to be overvalued.

Introduction

I typically shy away from REITs in favor of companies with greater growth potential. In fact, SmartCentres Real Estate Investment Trust (TSX: SRU.un) is the only REIT in which I have invested.

SRU.un may appeal to investors seeking an attractive income stream. Since the monthly distribution consists of Other Income, Capital Gains, and Return of Capital I encourage you to look at the historical tax aspect of SRU.un’s distributions.

My initial exposure to SRU.un was several years ago when the CFO from a REIT with which I had dealings from a work related perspective assumed the role of CFO at SRU.un (the company was known as Calloway REIT at the time). I held this individual in high regard and knew that he would not move from one good REIT to another unless there was a very good reason.

I delved into SRU.un a bit further and attended the Q2 2015 investor meeting at which time it was announced that following a long-standing and highly successful alliance Calloway would be joining forces with SmartCentres to become Smart Real Estate Investment Trust. As a fully integrated real estate provider, this new entity would have the expertise in acquisition, asset management, planning, development, construction, leasing, operations and property management all under one roof.

In this meeting, the investment community was informed that following the closing of this transaction, the new entity would benefit from the addition of 22 retail properties located primarily in Ontario and Quebec with Walmart (WMT) as anchor or shadow anchor. This resulted in an additional 3.4 million square feet of retail space, for a combined total of 30.8 million square feet in the portfolio.

Following this meeting I initiated a position in SRU.un and have closely watched its transformation; units are held in the FFJ Portfolio.

History

In 2017, the Trust changed its name from Smart Real Estate Investment Trust to SmartCentres Real Estate Investment Trust in order to further streamline the recognition, branding and goodwill associated with the SmartCentres’ brand among investors, retailers, municipal officials and consumers.

The following is a very high level overview of SRU.un’s history.

Source: SmartCentres Real Estate Investment Trust Investor Presentation

Source: SmartCentres Real Estate Investment Trust Investor Presentation

Business Overview

SRU.un develops, leases, constructs, owns and manages shopping centres and office buildings that provide retailers with a platform to reach their customers through convenient locations and to provide high-quality office space for tenants to locate effective workspaces.

In addition, SRU.un is working on opportunities to provide various forms of residential housing, seniors housing, and self storage facilities. It is also developing certain of its urban properties to provide a mix of retail, residential, office and self-storage space.

Shopping centres owned by the Trust focus on value-oriented retailers and include strong national and regional names as well as strong neighbourhood merchants. Walmart is the dominant anchor tenant in the portfolio and this is expected to continue.

As at the end of FY2018 (December 31, 2018) SRU.un held an ownership interest in 152 shopping centres with total income producing gross leasable area of 34.4 million square feet, one office property, seven development properties and four mixed-use properties, located in communities across Canada.

While many investors are scared of investing in retail REITs, the following are what make SRU.un strong:

- An exceptional pipeline of mixed-use growth initiatives;

- Outstanding quality of shopping centres and tenants;

- Healthy Balance Sheet and financial flexibility;

- Conservative property valuations and significant net asset value growth potential;

- The quality and depth of the development team and JV relationships.

For the most part, SRU.un’s tenants are of high quality. Reitmans (RET-a), which occupies 91 stores, is a very poor quality company from a credit perspective but only accounts for 2% of gross rental revenues.

Source: SmartCentres Real Estate Investment Trust Investor Presentation

Source: SmartCentres Real Estate Investment Trust 2018 Annual Report

Management has indicated the average age of its shopping centre portfolio is the youngest in the industry at 14.8 years, and therefore, capital expenditures will typically be lower than that of its industry counterparts which own older properties.

Average occupancy since 2005 has been 98.9% and all its major national and regional retailers continue to grow; the value segment of the retail industry is still growing. Keep in mind this high average occupancy rate includes the timeframe in which we experienced a Financial Crisis.

In addition to the quality of the tenants is the stability of the lease portfolio.

Source: SmartCentres Real Estate Investment Trust Investor Presentation

In addition to owning shopping centres which are located close to major highways, SRU.un owns the following Mixed-Use Developments.

- Vaughan Metropolitan Centre (“VMC”) in Vaughan, Ontario;

- Laval high-rise residential project in Laval, Quebec;

- Leaside self storage in Toronto (Leaside), Ontario

- Oshawa South self storage in Oshawa, Ontario.

SRU.un has several strategic relationships and initiatives in progress.

Toronto Studio Centre(“Studio Centre”) in Toronto, Ontario;

- townhouses with Fieldgate;

- seniors residence towers with Revera;

- self-storage with SmartStop at the Vaughan North West (“Vaughan NW”) shopping centre in Vaughan, Ontario;

- the development of up to 1.5 million square feet of residential space, in various forms, in Pointe-Claire, Quebec;

- the development of up to 2.5 million square feet of residential space, in various forms, at Westside Mall in Toronto, Ontario;

- the development of residential apartments, seniors residences and self-storage facilities, several of which were recently announced, at various shopping centres in the portfolio.

I have personally viewed almost all of SRU.un’s assets in the Greater Toronto Area. They are strategically located attractive properties.

The Vaughan Metropolitan Centre located on the north end of Toronto is a 10 – 15 year project which is a 50/50 joint venture between SmartCentres and Penguin Properties. Mitchell Goldhar (Executive Chairman of SRU.un’s Board) is intimately involved in all aspects of the project.

Potential density of this project is 18 –19 million sf. of residential, office and retail development for the whole 100-acre site.

Transit infrastructure, including TTC subway and VIVA bus opened in December 2017, and a York regional bus station is slated to open early in 2019.

The Toronto Premium Outlet located within a 10 minute drive from where I live opened in August 2013. It has recently undergone a major expansion and traffic flow is high and steady.

I have exchanged correspondence with subscribers of this site who reside in Montreal and Chilliwack. Feedback from them indicate that SRU.un’s projects in those cities are centrally located and attractive suggesting that maintaining high occupancy levels should not be an issue.

I view SRU.un as having the following competitive advantages at the centre of its long-term investment thesis.

- An exceptional management team led by Mitchell Goldhar (Executive Chairman of the Board) and Peter Forde (President & CEO);

- SRU.un has 151 employees in development & leasing related functions where the number of years experience with SRU.un averages 7 years (a total of 1,092 years) and the number of years experience in real estate averages 16 years (a total of 2400 years);

- A high percentage of cash flow being derived from investment-grade tenants;

- A diversified portfolio (premium outlet centres, apartment rentals, condominiums, townhouses, self-storage, office, seniors residences);

- Strong cash flow;

- A conservative (and improving) use of leverage.

Key Financial Highlights

SRU.un’s Q4 and FY2018 Earnings Release can be found here.

In this uncertain interest rate environment, SRU.un is continuing to seek opportunities to fix interest rates and secure longer-term financing when appropriate.

It is continuing to repay most maturing mortgages by using its line of credit on an interim basis, and then terming out selectively with unsecured debentures or similar unsecured facilities.

SRU.un’s current debt maturity/leverage levels are within its targeted ranges with the exception of the unencumbered asset pool. The plan, however, is to continue to increase this pool (valued in excess of $4.3B) so as to provide SRU.un with increased flexibility.

Source: SmartCentres Real Estate Investment Trust Investor Presentation

As at December 31, 2018, SRU.un’s overall debt levels continued to decline from prior years.

Debt to Aggregate Assets ratio was 43.9% (2017 – 45.4%), Debt to Adjusted EBITDA was 8.2x (2017 – 8.2x), and Interest Coverage was 3.3x (2017 – 3.2x).

In keeping with SRU.un’s goal to fortify its balance sheet, it raised $0.23B in equity in January 2019. Including this recent equity issuance, the metrics reflected above improved to 41.5%, 8.0x, and 3.5x, respectively.

As at December 31, 2018, SRU.un’s weighted average cost of secured and unsecured debt was 3.93% (2017 – 3.87%) and 3.51% (2017 – 3.42%), respectively.

SRU.un has also recently redeemed debentures with an unsecured 7 year, 3.59% fixed rate bank facility which bears a lower interest rate than the 4.05% redeemed debentures.

This accretive financing provides certainty on interest rate for the next 7 years and mitigates any potential dilutive impact from possible interest rate increases that could have occurred between now and the July 2020 maturity date of the recently redeemed Series H debentures.

SRU’s Balance Sheet would benefit from lower leverage and to this end, SRU.un has recently completed financing arrangements thus strengthening its debt ladder and extending the weighted average term on unsecured debt.

Source: SmartCentres Real Estate Investment Trust Investor Presentation

Credit Ratings

On September 21, 2018, DBRS Limited (DBRS) confirmed the Senior Unsecured Debentures rating at BBB (mid) with a Stable trend. This confirmation reflects continued growth in the value-focused shopping centres portfolio and the active development pipeline.

The rating is supported by SRU.un’s roster of high quality tenants and its strong market position in the value-focused retail segment nationally.

SRU.un has stated that the recent raising of additional equity and the refinancing of debt at lower rates are part of the REITs ultimate goal of enhancing the current BBB (mid) credit rating.

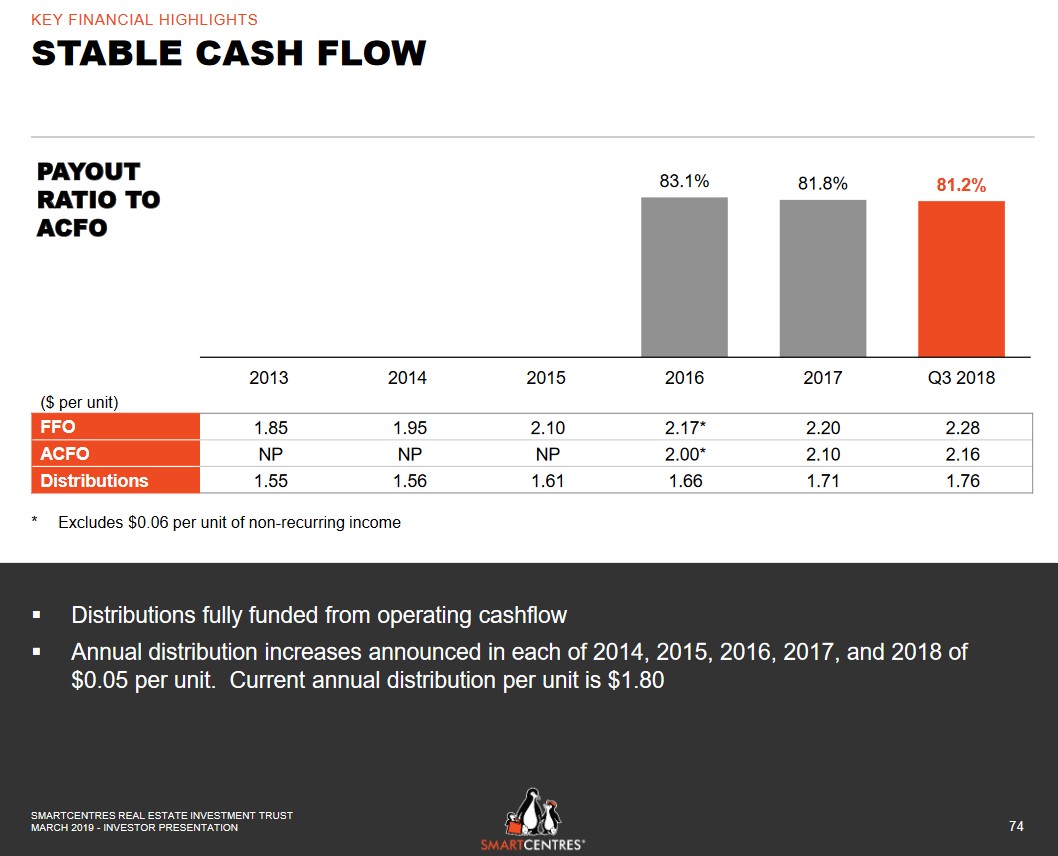

Distribution and Payout Ratio

SRU.un’s monthly distribution history can be found here. At $0.15/month, the annual $1.80 distribution provides investors with a ~5.17% annual yield.

The typical REIT investor seeking a monthly income stream will view a generous, safe, and steadily growing dividend as key factors. I view SRU.un’s monthly distribution as very safe thanks to a modest payout ratio backed by highly stable, recurring and recession-resistant cash flow.

Source: SmartCentres Real Estate Investment Trust Investor Presentation

Valuation

In all my years of investing I have yet to find a perfect valuation model. There are numerous ways to value a company: discounted cash flow models, PE ratios, price to book value, etc. but they all have their limitations.

One of the lesser-known valuation methods proven to be reasonably effective for stable income producing stocks is the dividend yield theory. This theory has been around for decades and readers interested in learning more may wish to read Dividends Don’t Lie: Finding Value in Blue-Chip Stocks published in 1990 and Dividends Still Don’t Lie: The Truth About Investing in Blue Chip Stocks and Winning in the Stock Market published in 2010.

The theory is reasonably simple and intuitive in that it basically says that for blue-chip dividend stocks, dividend yields tend to revert to the mean; a stock’s dividend yield fluctuates around a relatively fixed level over the years that approximate fair value.

Once again, no valuation model is perfect all the time and based on the findings in the books reflected above, this valuation model works best under long-term conditions (5+ year time frames) where high quality dividend stocks possess:

- A stable business model;

- Secure dividends;

- Generous payouts.

This valuation model states that if a stock’s current yield is far enough above its historical yield then the stock is likely undervalued. Alternatively, if its yield is well below the historical norm, then the stock could be overvalued.

The reason I compare a company’s current dividend yield versus its historical dividend yield in every article is because I am of the opinion that if stock prices follow earnings and the high quality companies distribute a reasonably consistent percentage of their earnings as dividends then there could be a connection with stock prices tracking dividends.

I have found that dividends are typically much less volatile than earnings which leads me to the conclusion that dividend yield can be a less noisy indicator of value.

The findings from the dividend yield theory study indicate this valuation model is most appropriately applied to companies with consistent and predictable business models (REITs (eg. SRU.un), most utilities, and companies with a long-term dividend track record).

The stability of their business models do not change much over time which leads to a relatively stable trading range for the stock’s dividend yield.

So, given the above, let’s look at SRU.un’s current dividend yield compared to that over the past few fiscal years. I will only go back to FY2015 because this REIT underwent a significant transformation that year as noted in the Introduction of this article.

SRU.un is currently distributing $0.15/month ($1.80/year) and the stock price as at April 2, 2019 is $34.92 giving is a distribution yield of ~5.15%. When compared to the low/high yields in recent years we see that the current distribution yield is at the low end of the range which suggests SRU.un is somewhat expensive at current levels.

Final Thoughts

I have mentioned in several previous articles that I view investors to be behaving somewhat irrationally and a broad pullback in the North American markets of some magnitude should not be unexpected.

Based on my Valuation analysis I would expect a 5.6% distribution yield to be more in line with that evidenced in recent years. With the current $1.80/year distribution this would imply a unit price of ~$32.14 is more reasonable ($1.80/5.6%).

While SRU.un’s long-term prospects are attractive I do not intend to increase my exposure. If SRU.un is of interest to you I suggest you keep in mind Buffett’s observation that ‘the stock market is designed to transfer money from the active to the patient.’

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long SRU.un.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.