Summary

Summary

- This National Bank of Canada Stock Analysis is the sixth of a 6 part series covering the Big 6 Canadian Banks.

- National Bank of Canada reported Q2 2017 results May 31st that were positively received by the market.

- Liquidity Ratios continue to be strong thus providing investors with assurances that an investment in the bank is relatively safe.

- Pockets of the Canadian real estate market are wildly overheated but NA’s real estate portfolio is significantly less exposed to these areas than its larger peers.

- NA is not nearly as diversified as its largest competitors and I am not enamored with some of the regions in which it has expanded in the past few years.

- A recap is provided in which I have ranked my take on the 6 Canadian Banks from a long-term investment perspective.

All figures are expressed in Canadian dollars unless otherwise noted.

Introduction

National Bank of Canada (TSX: NA), Canada’s 6th largest bank by market cap, reported Q2 2017 results on May 31st. A link to the Earnings release can be found below in the Q2 2017 Financial Results section of this post.

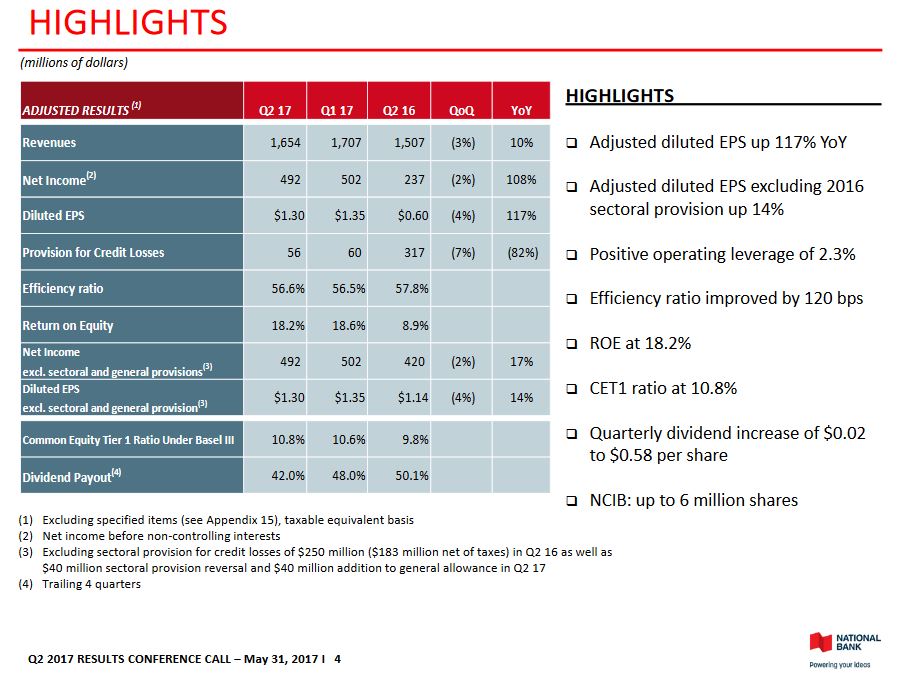

NA – Q2 2017 Financial Highlights

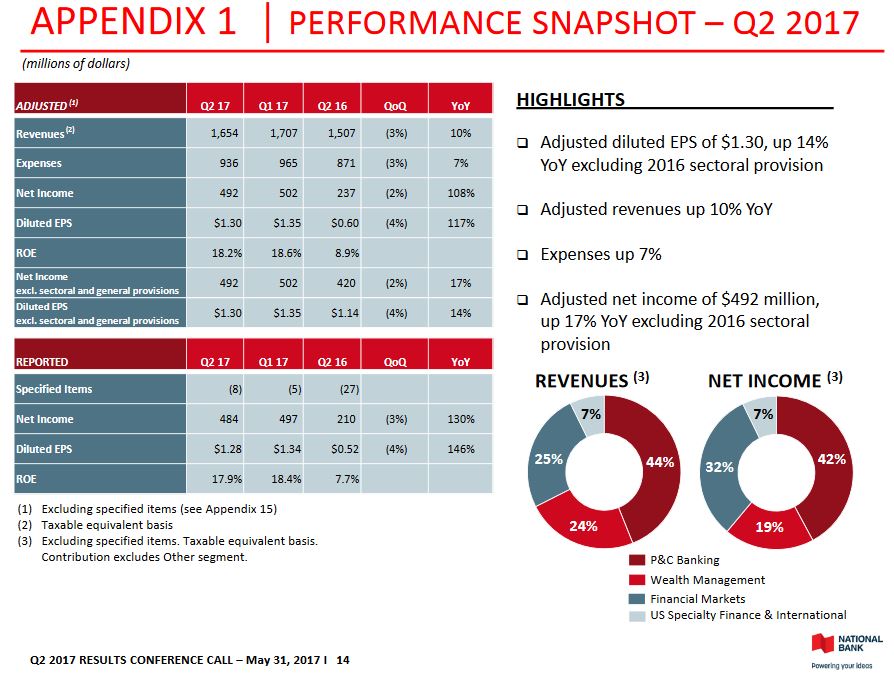

NA – Q2 2017 Performance Snapshot

While I touch upon various topics that impact the Canadian Banking Sector and the top 6 Schedule I Canadian Banks, I strongly encourage you to listen to the NA segment of the March 29 and 30, 2017 National Bank Financial Markets – 15th Annual Financial Services Conference where Louis Vachon (President & CEO) discusses a wide range of topics. There is far too much information covered in this ~35 minute segment for me to give the content justice in this post.

In his presentation he touches upon:

- the Quebec economy which is where NA has a huge presence.

- the shrinking of Canada’s manufacturing sector which is 20% smaller than 10 years ago.

- the record tourist industry results in 2016 and strong expectations for this industry in 2017. This is attributed to the weak Canadian dollar and the fact Canada will be celebrating its 150th anniversary and Montreal will be celebrating its 375th anniversary in 2017.

- the Montreal real estate market is experiencing a “spillover effect” as Asian and European buyers view Montreal real estate values as far more attractive than Greater Vancouver Area (GVA) and Greater Toronto Area (GTA).

- the bank’s focus on efficiency improvements.

In addition, he discusses NA’s 3 priorities with respect to the deployment of capital. In order of priority, they are:

- Fund organic growth.

- Domestic Wealth Management or International strategic acquisitions. Having said this, domestic wealth management opportunities at attractive valuations are extremely hard to come by.

- A mix of dividend increases or share buybacks when the bank views its share price as undervalued.

The Canadian Banking Sector

Details on the Canadian Banking Sector can be found here.

Technological Innovation

Details about the Technological Innovation the Canadian banks are undertaking can be found here.

NA Overview

Many readers may not be entirely familiar with NA given that it is small relative to its peers and its North American geographic presence is somewhat limited. In addition, it is not listed on a US exchange so it very likely flies under the radar of many US investors. I, therefore, provide a link to NA website which shows some of its strategic milestones.

In part 5 of this series I discussed The Bank of Nova Scotia’s (TSX: BNS) preferred regions for strategic growth. NA’s international expansion in recent years has been in Cambodia and in a financial group headquartered in Abidjan, Côte d’Ivoire (French speaking Africa), with operations in 12 countries across West and Central Africa.

Further details can found in the first few pages of NA’s 2016 Annual Report.

Q2 2017 Financial Results

Readers are encouraged to review NA’s May 30, 2017 Earnings Release, Earnings Presentation, and to listen to the conference call.

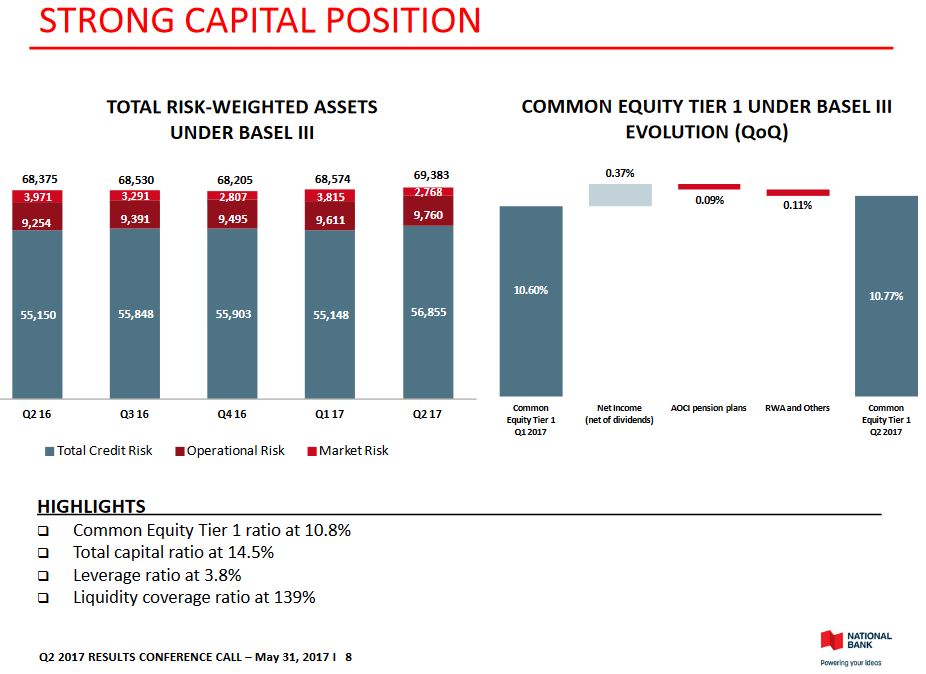

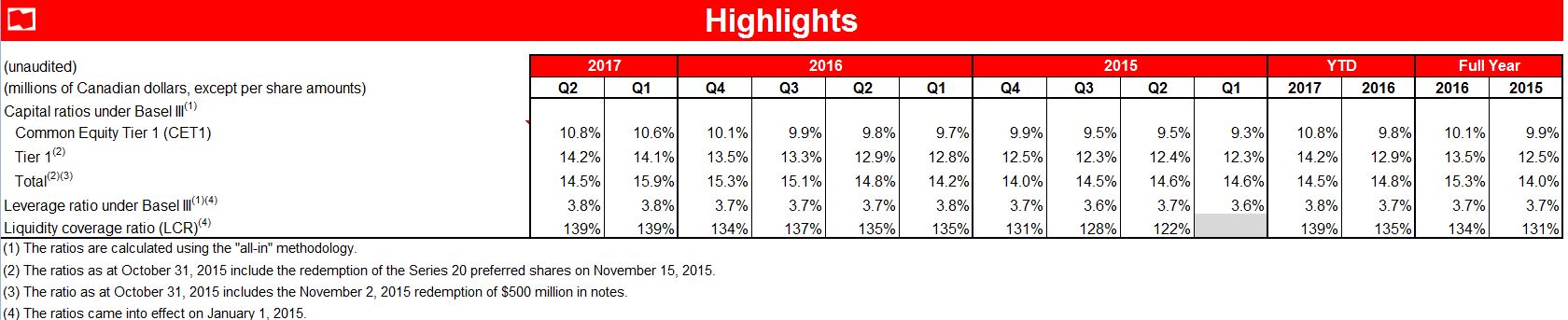

Capital Measure Ratios

In addition to touching upon the Capital Measure Ratios for NA, you can find more information here.

NA – Strong Capital Position

NA – Comparative Performance Capital Ratios

NA – Capital Ratios

You like numbers? A host of numbers can be found in Excel files right here! Knock yourself out.

Recent Events in the Canadian Banking Sector

A brief overview about a few major Recent Events in the Canadian Banking Sector can be found here.

As to whether the Home Capital problems in Canada will spillover to the Big 6 banks, here is a recent article which supports my opinion that the Big 6 will be just fine.

Inflated Real Estate Values

Given the impact the US real estate bubble had on the US Banking sector, it is only fair that people should be wondering what would happen to the Canadian financial institutions if the grossly inflated real estate values in various major centres in Canada were to experience a correction.

Multiple articles have been published about the state of certain pockets of the Canadian real estate market and how consumers are stretched financially. Recently, more articles have appeared about the sudden cooling of the real estate market and the concern about the reliance on real estate that has fueled a growth surge in GDP.

Change in Sales of Freehold Houses 2016 vs 2017

In addition to my opinion on this topic which can be found here, I have very recently attended Open Houses (a community on the outskirts of Toronto) so I could speak with various real estate agents and brokers. All have indicated they have noticed a marked change in the last couple of months. Buyers appear to be less aggressive and in all cases, Open Houses are getting much less foot traffic. They have also commented that there is concern that some buyers may be willing to risk the loss of their deposit and will just walk away from their offers.

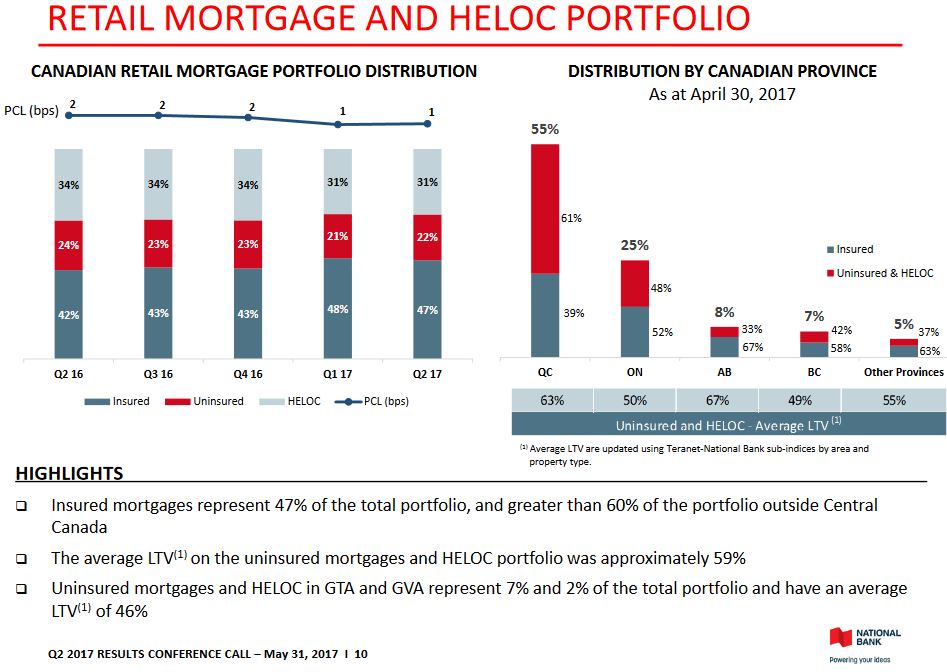

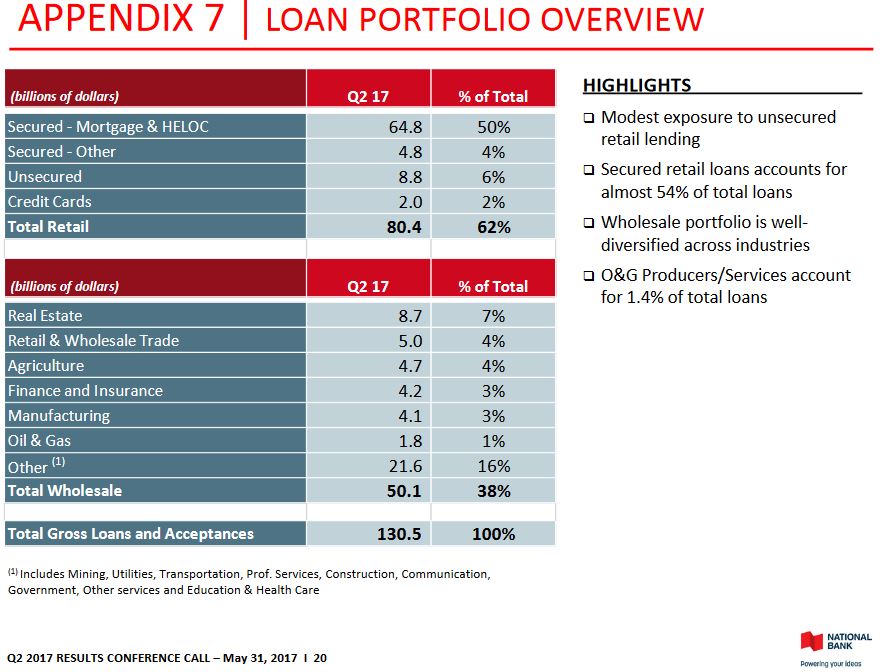

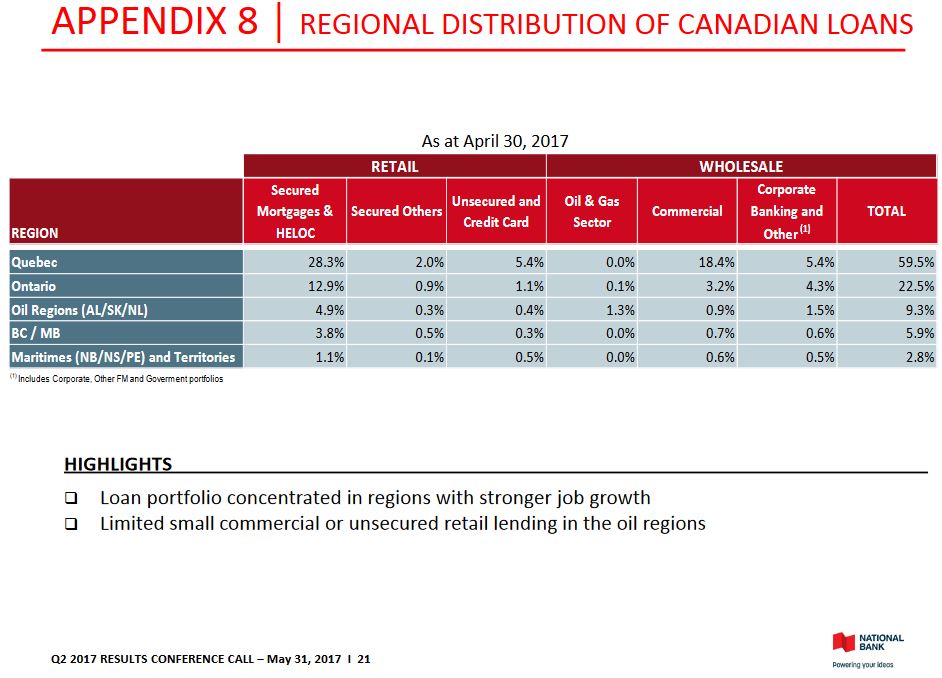

Fortunately, NA’s exposure to real estate in the GVA and GTA markets is far lower than its peers. While real estate values have certainly increased in the Greater Montreal Area (GMA), housing is generally more affordable. Another comforting fact is that NA’s average LTV on its uninsured mortgages and HELOC portfolio in the GVA and GTA is 46% and they only represent 7% and 2% of the total portfolio.

NA – Retail Mtgs and HELOC Portfolio

NA – Loan Portfolio Overview

NA – Regional Distribution of Canadian Loans

Risk Management

There are a host of risks the Canadian financial institutions face. Global uncertainty, Brexit, Oil & Gas, Cyber risk, anti-money laundering, renegotiation of NAFTA, and the increasing complexity of regulation are just a few of these other risks.

Readers are encouraged to review the 29 page “Quarterly Slides” presentation found here as there are multiple pages that provide details addressing the quality of NA’s loan portfolio. There are also multiple pages in NA’s 2016 Annual Report addressing NA’s Risk Management. Page 9 of 202 pages of the Annual Report lists the locations of the disclosures within the report.

Dividend

NA’s dividend distribution and stock split history can be found here.

Unlike many foreign banks which were forced to dramatically reduce or suspend their dividend during the Financial Crisis, NA and its Canadian counterparts froze their quarterly dividend. In early-2011, NA reinstated dividend increases.

Readers should note that the quarterly dividend paid on NA’s common shares have been adjusted to account for 2 for 1 stock splits on February 12, 1987 and February 13, 2014.

I suggest readers look at NA’s dividend history going back to 1980. It appears NA was not so kind to investors in 1981 – 1983 and about half of the 1990s.

In addition to a spotty dividend history, NA’s dividend increases are somewhat lower than its larger Canadian peers.

On May 31, 2017, NA announced that its Board of Directors declared a quarterly dividend increase of $0.02/share from $0.56 to $0.58. The next dividend is payable August 1, 2017 to shareholders of record at the close of business on June 26, 2017.

As I compose this post, NA’s dividend yield is ~4.2%. This is ~50 basis points higher than peer levels with the exception of Bank of Montreal (TSX: BMO) (~4%) and Canadian Imperial Bank of Commerce (TSX: CM) (~4.8%). I do not view NA’s positive yield variance relative to The Royal Bank of Canada (TSX: RY), The Toronto-Dominion Bank (TSX: TD), and BNS as sufficient to warrant NA’s weaker dividend history.

Valuation

On May 31, 2017, NA announced that its Board had authorized a normal course issuer bid to purchase for cancellation up to 6,000,000 of its issued and outstanding common shares which represents approximately 1.76% of its 341,517,603 issued and outstanding common shares as at May 23, 2017. This normal course issuer bid is subject to the approval of the Office of the Superintendent of Financial Institutions Canada (OSFI) and the Toronto Stock Exchange (TSX).

The current mean FY2017 adjusted EPS estimates from various brokers for fiscal 2017 is $5.22.

NA – Projected EPS

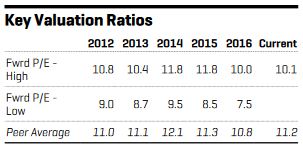

NA – Historical Valuation Ratios

As I compose this post, NA is trading at ~$53.3 on the TSX thus giving us a forward PE of ~10.2. When I look at the high/low PE ratio levels for the past few years I view the current level as slightly elevated but not totally unreasonable.

National Bank of Canada Stock Analysis – Final Thoughts

I can see how NA would be an appealing investment for some investors. It:

- is currently trading at a reasonable valuation and its dividend yield is attractive.

- has rewarded some investors handsomely (see comparative stock chart below).

- has a retail business with a heavy geographic concentration in Quebec. Readers might deem this to be a huge strike against NA but in the current environment, Quebec’s financial picture is better than that of other provinces; Quebec has actually balanced its books for 3 years in a row. The same can’t be said for Ontario, BC, and Alberta where one has to question whether the provincial governments have the foggiest idea on what it means to be fiscally responsible.

NA – Stock Chart for 6 banks

I, however, have no desire initiate a position in NA any time soon and my reasoning is as follows:

- I am already overweight the banking sector with positions in the largest 5 Canadian banks.

- NA is not nearly as well diversified as its largest Canadian peers.

- NA’s recent international expansion has been in regions which I deem to be of higher risk. NA’s ~21% investment in an entity in Côte d’Ivoire may end up generating a decent return at some stage but, personally, this is not a region I deem to be low risk.

- It is far smaller (market cap of ~$18.2B) than CM which is Canada’s 5th largest bank (market cap of ~$42B).

- NA has previously cut or suspended its dividend. While both happened several years ago, the mere fact its dividend history is not as exemplary as that of its peers is, in my opinion, a strike against NA.

- NA is not listed on a US exchange. While not necessarily a terrible thing, all its larger peers are listed on the NYSE. This means they attract more interest/coverage from the investment community.

Conclusion – Ranking of the Big 6 Banks

After completing my analysis of the Big 6 Schedule I Canadian Banks, my opinion on each is as follows (ranked in order of personal preference):

#1 – RY has a well diversified book of business and has historically been the premiere Canadian bank. It represents a great long-term investment.

#2 – TD has done an amazing job in growing its Wealth business and in becoming a solid bank in the NE part of the US. It certainly is a very different bank from when I started working there in 1987; I moved to BNS in early 2004. This bank represents a great long-term investment.

# 3- BNS is my 3rd rated stock. I like its geographic footprint in that it is focused on markets where the demographics are right and the middle class is growing (Mexico, Chile, Peru, and Colombia). In my opinion, the Caribbean region is definitely not where I would want to be a premiere bank but since BNS has been entrenched in that region so long and it already has a solid footprint, I think senior management has no intention of pulling up stakes. I am also encouraged that the bank is becoming more focused on the geographic regions in which it wants to operate as opposed to stretching itself too thin. BNS also represents a great long-term investment.

As for #4 – Bank of Montreal (NYSE: BMO) and #5 – Canadian Imperial Bank of Commerce (NYSE: CM), you will likely do well long-term by owning shares in these two banks. Based on my qualitative analysis, however, they are not nearly attractive as RY, TD, and BNS.

I started my career with BMO in 1980 and for the last ~37 years, BMO just seems to have plodded along. It acquired Harris Bank in the US in the early 1980s and Marshall & Ilsley in 2011 and, in my opinion, BMO’s success in the US pales in comparison to that of TD.

As for CM, this is another Canadian bank that just seems to plod along. It certainly provides investors with an attractive dividend yield but as far as the growth of its share price since 1999, results have fallen short relative to its larger peers.

I am hopeful CM’s acquisition of PrivateBancorp (NASDAQ: PVTB) will help it in the long-term but am concerned CM has overpaid for this bank. I think the US market is “overbanked” and CM is going to find it a really tough slog integrating this bank into its existing operations.

As for #6- NA, it is not a terrible bank. I just don’t recommend it as a core investment since I do not view it as being strategically positioned for future growth to the same extent as RY, TD, and BNS.

Some of you may be wondering “OK, if you don’t think BMO and CM are decent investment opportunities why do you own shares in these two banks?”

Good question. The reason my wife and I still own shares in these two banks is that a sizable component of our equity portfolio was acquired many years ago and we are being rewarded handsomely from a quarterly dividend income perspective. Secondly, we significantly increased our equities exposure at the height of the Financial Crisis. Valuations when we acquired our shares were far, far different from current levels. Back then, fear gripped the markets. Today, too many investors are euphoric and think values can only go in one direction.

If you are hell bent on initiating or increasing positions in any of the banks I have analyzed in this series, I suggest your purchases be gradual. I certainly do not have a crystal ball but I suspect a major market pullback (also see here and here and here and here) will come about within the next 12 months. As if that isn’t enough, the International Monetary Fund has recently expressed concern about the Canadian economic outlook.

There you go…my take on the Canadian banking sector.

Note: I hope you enjoyed this series and sincerely appreciate the time you took to read these posts. Hopefully you came away with some new information to help you in your decision making process.

As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long CM, RY, BMO, TD, and BNS.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.