On October 25, 2018, I initiated a position in S&P Global (SPGI) within one of the ‘Side’ accounts in the FFJ Portfolio. I subsequently initiated a position in Moody’s (MCO) in the same account on October 26, 2018.

My rationale for having a position in both companies is:

- they are leading global integrated risk assessment firms;

- their respective valuation was reasonable;

- they are not capital intensive companies;

- they generate strong Free Cash Flow (FCF); and

- the outlook for both firms is promising.

Furthermore, just like my decision to invest in Visa (V) and Mastercard (MA), I have no idea which of the 2 companies will perform best over the long term. Rather than pick the wrong company in which to invest, I decided to invest in both.

My purchase price in 2018 was $143.61 and the quarterly dividend at the time was $0.44 resulting in a ~1.2% dividend yield or a ~1% dividend yield when I account for the 15% dividend withholding tax.

On March 16, 2021, I transferred the SPGI and MCO shares between investment accounts for tax planning purposes. MCO’s share price at the time of transfer was ~$297 and that of SPGI was ~$349. These transfers triggered a capital gain but future capital gains will be taxed at a more favourable rate.

The share price has appreciated rapidly since the beginning of 2021. Since we can not rule out a pullback, we must be careful not to grossly overpay to acquire shares or we may find ourselves in a predicament where the potential for capital appreciation is limited. Ask any investor who invested in Intel (INTC) or Cisco (CSCO) at the height of the .com craze. Twenty years later and their respective share price has still not reached the peak share price!

Moody’s – Stock Analysis – Business Overview

Moody’s (MCO) is a globally integrated risk assessment firm that empowers organizations and investors to make better decisions.

Moody’s reports in two segments:

- Moody’s Investor Services;

- Moody’s Analytics.

It provides customer solutions through a family of companies, affiliates, and joint ventures. Additional information about each wholly-owned, majority-owned, and minority-owned entity is accessible here.

MCO’s August 10, 2021, Q2 Investor Presentation provides a wealth of information.

MCO was founded in 1909 and has grown significantly as borne out by the following statistics.

A high-level overview of MCO’s journey over the most recent 5 decades is accessible here.

Part 1, Item 1 in the FY2020 10-K provides a good overview of the company.

Item 1A discloses and addresses key identifiable risks.

Short videos that address such topics as Priorities and Strategy provide additional information about the company.

Moody’s – Stock Analysis – Acquisition of RMS

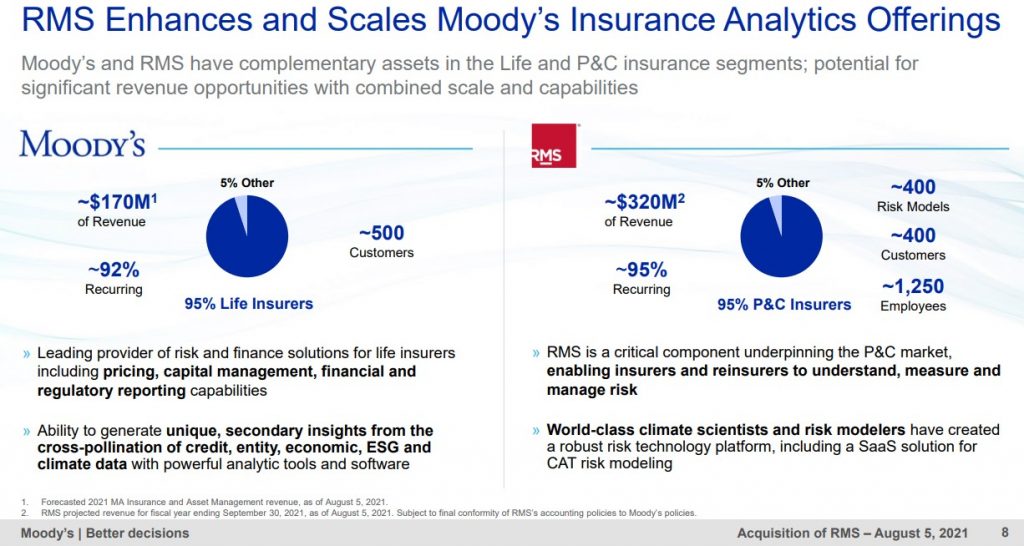

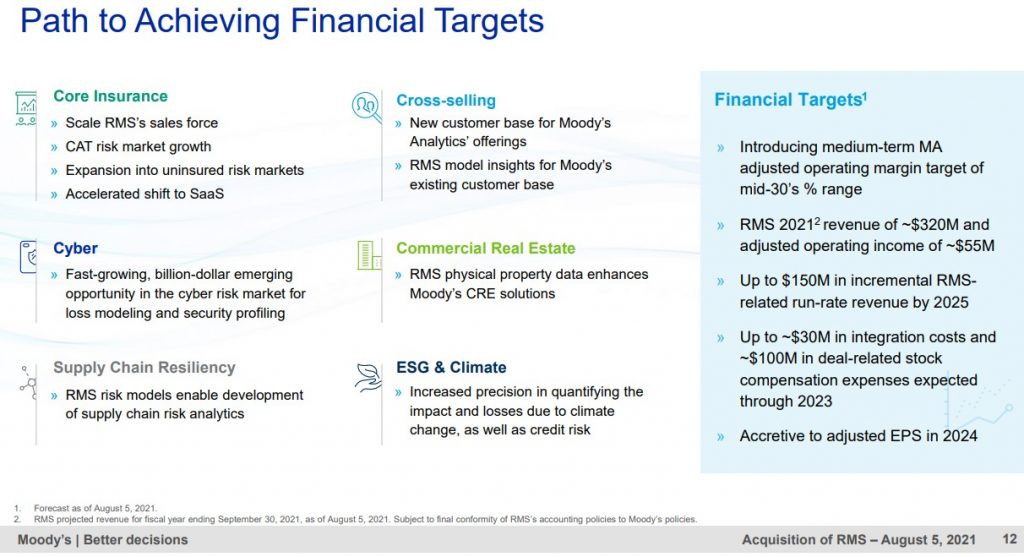

On August 5, 2021, MCO and Risk Management Solutions, inc. (RMS) announced that they entered into a definitive agreement for MCO to acquire RMS for ~$2B from Daily Mail and General Trust plc; RMS is a leading global provider of climate and natural disaster risk modelling and analytics.

The acquisition will immediately increase MCO’s insurance data and analytics business to ~$0.5B in revenue and will accelerate the development of MCO’s global integrated risk capabilities to address the next generation of risk assessment.

RMS has over 400 risk models covering 120 countries and is the world’s leading provider of climate and natural disaster risk modelling serving the global property and casualty (P&C) insurance and reinsurance industries.

Moody’s – Stock Analysis – Financials

Q2 2021 and YTD Results

MCO released Q2 and YTD results on July 28, 2021. The accompanying Investor Presentation is accessible here.

FY2021 Guidance

- February 12, 2021 – MCO released FY2020 results and FY 2021 diluted EPS and adjusted diluted EPS guidance ranges of $9.70 – $10.10 and $10.30 – $10.70.

- April 28, 2021 – MCO released Q1 2021 results at which time it raised FY 2021 diluted EPS and adjusted diluted EPS guidance ranges to $10.40 – $10.70 and $11.00 – $11.30, respectively.

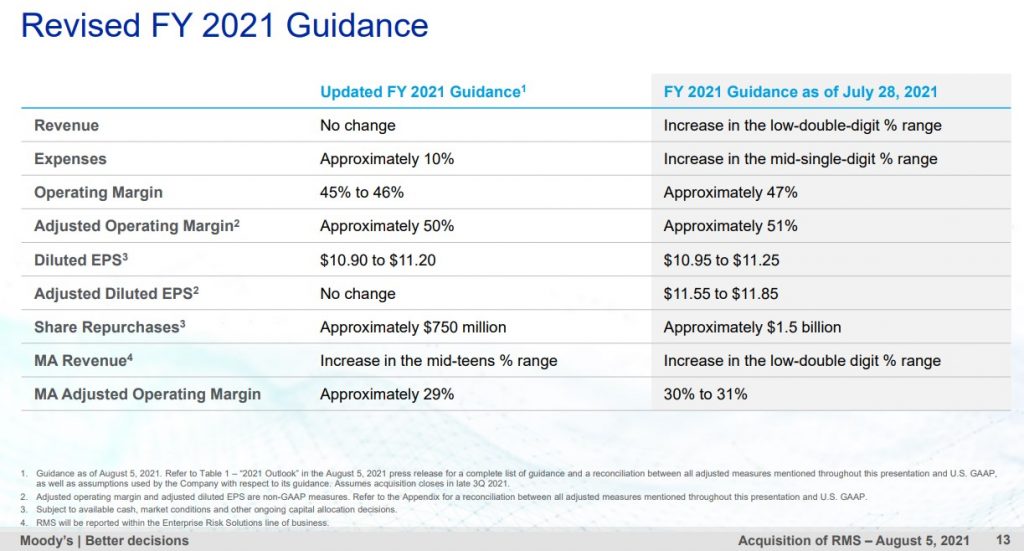

- July 28, 2021 – MCO released Q2 results and once again raised FY2021 diluted EPS and adjusted diluted EPS guidance to $10.95 – $11.25 and $11.55 – $11.85, respectively. This revised guidance accounts for the accretion in revenue and earnings from the RMS acquisition that was announced on August 5, 2021.

Moody’s – Stock Analysis – Credit Ratings

Given that MCO is one of the two leading credit rating agencies, it would not bode well if MCO’s credit ratings were non-investment grade.

The senior unsecured domestic long-term debt ratings assigned by S&P Global and Fitch are:

- S&P Global – BBB+ long-term unsecured debt credit rating with a stable outlook; and

- Fitch – BBB+ long-term unsecured debt credit rating with a stable outlook;

Both ratings are the top tier of the lower medium-grade investment-grade tier.

These ratings define MCO as having an ADEQUATE capacity to meet its financial commitments. However, adverse economic conditions or changing circumstances are more likely to lead to MCO having a weakened capacity to meet its financial commitments.

The Summary of Outstanding Debt and Debt Maturity Profile as of June 30, 2021, reflects a well-balanced maturity schedule.

I view MCO’s credit risk to be acceptable.

Moody’s – Stock Analysis – Dividends and Share Repurchases

Dividend and Dividend Yield

MCO’s dividend history reflects annual dividend increases starting 2011 following a dividend freeze that was precipitated by challenging business conditions during The Financial Crisis.

MCO’s current ~$382 share price and $0.62 quarterly dividend yields ~0.65%. As with SPGI, I hold my MCO shares in a taxable account and I am a Canadian resident. I, therefore, incur a 15% dividend withholding tax. My dividend yield is ~0.55% which is reasonably similar to that of SPGI.

Investors seeking income from their investments will likely shy away from investing in MCO.

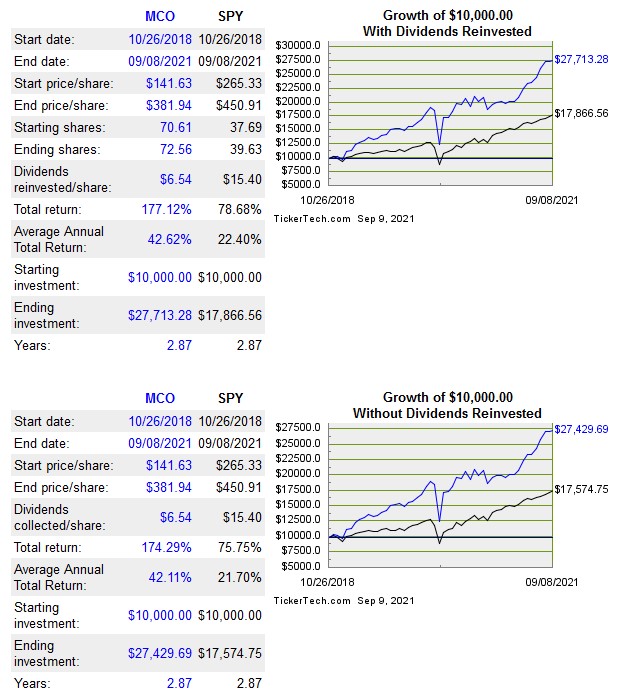

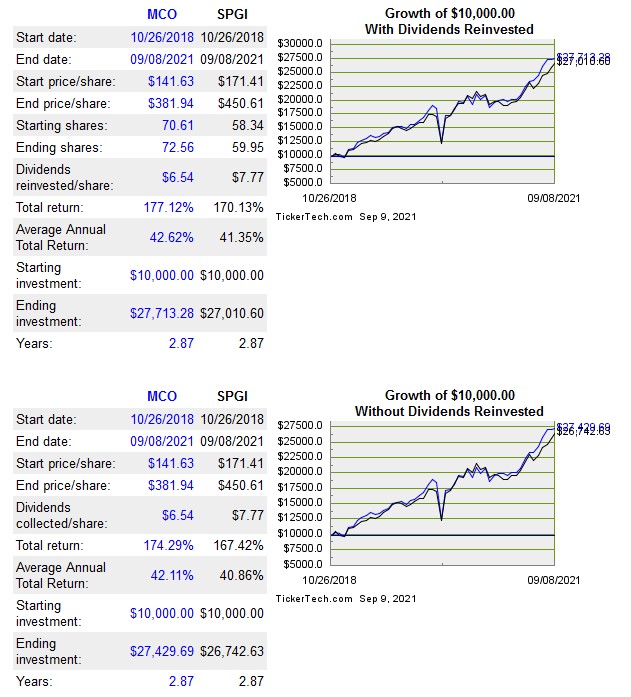

Although the dividend yield is unattractive, MCO has generated an impressive total return relative to the S&P500 over the timeframe in which I have been a shareholder.

We also see that the total investment return for MCO and SPGI over the same timeframe is almost identical.

There is no assurance the share price of either company will appreciate to the same extent as in the past ~2.87 years. Earnings and FCF growth coupled with share buybacks make it likely, however, that their respective share price will appreciate significantly in value over the next decade.

I am not a MCO shareholder for the dividend. I invest in MCO from a total return perspective and envision long-term capital gains will form the bulk of my investment return.

Share Repurchases

On December 16, 2019, MCO’s Board authorized $1B in share repurchase authority.

On February 9, 2021, the Board approved an additional $1B in share repurchase authority.

On June 30, 2021, there was approximately $1.327B of combined share repurchase authority remaining. There is no established expiration date for the remaining authorization.

In Q4 2020, Q1 2021 and Q2 2021, Moody’s issued a net 0.2 million shares, 0.6 million shares, and 0.2 million shares under employee stock-based compensation plans. Despite the issuance of these shares, MCO’s Diluted Weighted-Average Shares of Common Stock Outstanding has steadily declined as evidenced from the FY2011 – FY2020 figures of 229, 227, 224, 215, 203, 195, 194, 194, 192, and 189 (millions of shares).

Moody’s – Stock Analysis – Valuation

Management’s most recent adjusted diluted EPS guidance is $11.55 – $11.85. Using the current ~$382 share price and the $11.70 mid-point of guidance we get a forward adjusted diluted PE of ~32.7.

The current FY2021 – FY2023 adjusted diluted EPS analyst estimates are fairly wide-ranging:

- FY2021 – 16 brokers – mean of $11.87 and low/high of $11.69 – $12.52. Using the mean estimate, the forward adjusted diluted PE is ~32.2.

- FY2022 – 17 brokers – mean of $12.40 and low/high of $11.54 – $13.50. Using the mean estimate, the forward adjusted diluted PE is ~30.8.

- FY2023 – 12 brokers – mean of $14.01 and low/high of $13.05 – $15.25. Using the mean estimate, the forward adjusted diluted PE is ~27.3.

While I like MCO as a long-term investment, I think the current valuation is somewhat rich.

Moody’s – Stock Analysis – Final Thoughts

I like MCO’s and SPGI’s long-term outlook and plan to increase my exposure to both companies. However, I think it will be challenging to generate a decent rate of return if shares are purchased at the current valuation. Furthermore, I think the broad market is poised for a pullback and the share price of both companies will likely be caught in the downdraft.

Given the above, I am not prepared to add to my MCO position at this point and will patiently wait on the sideline.

Stay safe. Stay focused.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long MCO, SPGI, V, MA, and CSCO.

Disclaimer: I do not know your individual circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.

[…] NOTE: My most recent MCO analysis is accessible here. […]