Summary

Summary

- This Hershey stock analysis is based on Q4 and FY2016 results and outlook for fiscal 2017 which were released February 3, 2017.

- For the 3rd time this century, The Hershey Company spurned a takeover offer in 2016. Don’t expect The Hershey Trust Company to ever sell.

- While FY2016 results were acceptable, the Chinese need to step up and buy more HSY chocolate; sales in China were down 4% in Q4 (same rate as Q2 and Q3).

- I am reluctant to acquire any more HSY shares unless the price retraces to $95 or below.

- I encourage readers to purchase HSY chocolates for Valentine’s Day (February 14th).

Introduction

We have owned shares in Hershey Company (NYSE:HSY) for several years. With the release of its Q4 and FY2016 results on February 3, 2017, I am taking this opportunity to assess the company’s performance and outlook.

Industry Overview

A key ingredient in HSY’s product is cocoa. You can click on this link if you wish to see cocoa’s price action over time.

While HSY does not buy their chocolate on a spot basis, I am certain they are taking advantage of the downturn in cocoa prices. I recognize prices do not always go up, nor do they always go down. I do, however, certainly expect HSY to be sufficiently astute to take advantage of depressed cocoa prices whenever possible.

The industry in which HSY competes is relatively mature in the U.S. and Western Europe. There have been indications of food industry volume softness in the U.S. over the past few years which is likely partially attributable to the cumulative impact from price increases and lackluster economic growth.

Opportunities for faster longer-term growth, however, exist in China and Latin America as the standards of living in developing international markets rise. Unfortunately, HSY’s recent results out of China have been less than stellar.

In 2014, Nielsen conducted a study to determine what consumers around the world are looking for.

30,000 consumers in 60 countries participated in the study about popular snacks. At the time, snack sales across the globe hit $374B, which was a 2 percent increase from the previous year. Keep in mind that HSY’s annual sales are only the $7.44B range so you would think there is ample growth opportunity for HSY.

One caveat about international sales in emerging international markets is the additional risks from factors such as currency fluctuation and regulation. The strong US dollar is certainly not helping HSY.

While growth opportunities do exist, most industry participants have been undertaking cost reduction programs to improve efficiency and productivity to bolster the bottom line. This trend is likely to continue.

Business Overview

Mondelez International Inc. (NYSE: MDLZ), one of the companies within HSY’s peer group, made a run for HSY in 2016 by offering $107/share for a total of $23B. For the third time in this millennium, The Hershey Trust voted against any takeover.

Some investors were disappointed the MDLZ offer was not accepted. With the retirement announcement of HSY’s CEO, effective the end of February 2017, there was cautious optimism another takeover offer could be presented subsequent to his departure.

The incoming President and CEO, however, has been HSY’s EVP and COO for the past 11 years. I suspect the likelihood of another takeover offer being successful is unlikely.

Investors can likely expect HSY to continue with its strategy which is to:

- develop new products.

- make bolt-on acquisitions.

In April 2016, HSY completed its acquisition of Ripple Brand Collective, LLC, whose annual net sales are in the $65 – $75 million range.

Q4 and FY2016 Financial Results

This Hershey stock analysis is based on Q4 and FY2016 results and outlook for fiscal 2017 which were released February 3, 2017 Earnings.

Q4 Results

- Consolidated net sales were $1.9702B vs. $1.9092B Q4 2015. This 3.2% increase includes the impact of acquisitions and foreign currency exchange rates.

- Reported gross margin was 37.7% vs. 46.0% in Q4 2015.

- Adjusted gross margin was 44.5% vs. 45.0% in Q4 2015. The 50 bps decline was primarily driven by unfavorable supply chain costs and trade, partially offset by supply chain productivity and costs savings initiatives.

- Operating profit and margin was $0.2295B or 11.6% vs. $0.32B or 19.2% in Q4 2015.

- Adjusted operating profit was $0.3784B, a 0.5% decline vs. Q4 2015.

- Reported net income $0.1169B or $0.55 diluted EPS vs. $0.2279B or $1.04 diluted EPS for Q4 2015.

- Adjusted net income was $0.9485B vs. $0.9097B in FY2015, a 7% increase.

- Net margin was 5.9% vs. 11.9% in Q4 2015.

- Adjusted diluted EPS of $1.17 vs. $1.08 in Q4 2015.

- 5 bps unfavorable foreign currency exchange rate.

- Acquisitions provided a 9 bps benefit.

FY2016 Results

- Consolidated net sales were $7.4402B compared with $7.3866B for Q4 2015. This 0.7% increase includes the impact of acquisitions and foreign currency exchange rates.

- Operating profit and margin was $1.2058B or 16.2% vs. $1.0378B or 14% FY2015.

- Reported net income $0.72B or $3.34 diluted EPS vs. $0.513B or $2.32 diluted EPS for FY2015.

- Adjusted net income was $0.2497B vs. $0.237B in FY2015, a 5.4% increase.

- Net margin was 9.7% vs. 6.9% in FY2015.

- Adjusted diluted EPS of $4.41 vs. $4.12 in FY2015.

- Acquisitions provided a 6 bps benefit.

- Cash flow generation remains strong. Operating cash flow of nearly $1B in 2016 enabled HSY to return about $0.920B to shareholders via dividends and share repurchases.

- HSY repurchased $0.420B outstanding shares, resulting in diluted shares outstanding of 215.3 million at the end of 2016 vs. 220.7 million at the end of 2015.

Outlook for Fiscal 2017

- Continued rollout of Hershey’s Cookie Layer Crunch bars, barkTHINS chocolate and other new products such as Reese’s Crunchers candy and Krave meat bars and sticks, is expected to accelerate North America sales growth.

- International macroeconomic challenges expected to persist, especially in China.

- Full-year net sales expected to increase 2% to 3% including a net benefit from acquisitions of about 50 bps and unfavorable foreign currency exchange rates of about 25 bps.

- Reported diluted EPS expected to be $4.54 – $4.65.

- Adjusted EPS expected to increase 7% to 9% and be $4.72 – $4.81.

HSY implemented various efficiency initiatives mid last fiscal year which are expected to translate into a 40 bps expansion in adjusted operating profit margin (20% increasing to 20.4%). The program, dubbed “Margin for Growth”, will be a multi-year program designed to improve overall operating profit margin through supply chain optimization, a streamlined operating model and reduced administrative expenses, with savings primarily achieved in 2018 and 2019. Details of this program are to be provided March 1, 2017.

Valuation

HSY is definitely not a high growth company. If you take a look at its top line for the last few years, results have hovered in the $7B – $7.5B range. The bottom line certainly does not exhibit a nice upward trajectory but HSY does continue to generate positive cash flow.

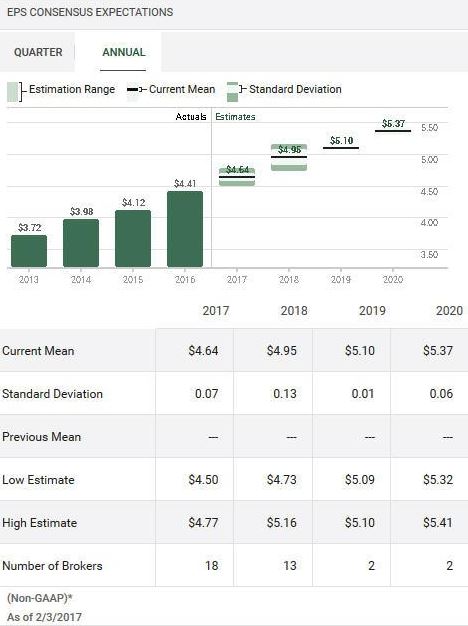

Let’s look at what analysts are projecting.

Multiple analysts have provided their estimates and it appears $4.65 is their EPS consensus for FY2017. This is at the upper end of HSY’s diluted EPS projections but let’s go with that number for the exercise.

Source: TD WebBroker – HSY Quarterly EPS estimates

Source: TD WebBroker – HSY Annual EPS estimates

Source: ValuEngine – HSY Quarterly EPS estimates

Source: ValuEngine – HSY Annual EPS estimates

Google Finance currently reflects a PE just under 34 but it uses an EPS of $3.16. HSY reported $3.34 so if we use the current stock price of $106.79 at the time I compose this post and a $3.34 EPS, the PE drops to 31. If I use $106.79 and the $4.41 adjusted diluted EPS for FY 2016 I get a PE of 24.22.

Now let’s use the projected diluted EPS and projected adjusted EPS figures reflected in the Outlook for Fiscal 2017 section of this post to come up with forward looking PE ratios.

$106.79/$4.65 = 23

$106.79/$4.765 (mid-point of $4.72 – $4.81 range) = 22.41

I generally like to acquire shares in companies when the PE is sub 20 so using the current stock price and estimated FY2017 EPS, I view HSY as too expensive at this stage.

Let’s look at HSY from a dividend yield perspective. HSY currently pays a quarterly dividend of $0.618. If it sticks with a once a year dividend increase, we can expect two more dividends of this amount. Looking at the historical dividend increases, I would expect HSY to perhaps increase its quarterly dividend later this year by $0.035 – $0.04. To be conservative, I will go with a $0.035/quarter increase thus giving us a new dividend of $0.653/quarter or $2.612/year.

So, the current dividend yield is 2.31% (($0.618*4)/$106.79 and if I use my $2.612 annual dividend forecast and the current price of $106.79, I get a dividend yield of 2.45%.

When looking at HSY from a dividend yield perspective, I still can’t justify paying the current price.

Since I generally like to acquire shares in companies when the PE is sub 20, if I use the projected EPS I used above, HSY’s price would have to come down to a level below $95.

$4.65 *20 = $93

$4.765 * 20 = $95.30

Using these values, the dividend yield would be $2.612/93 = 2.8% and $2.612/$95.30 = 2.74%. While these are slightly better yields than currently, they are nothing to write home about.

Option Strategy

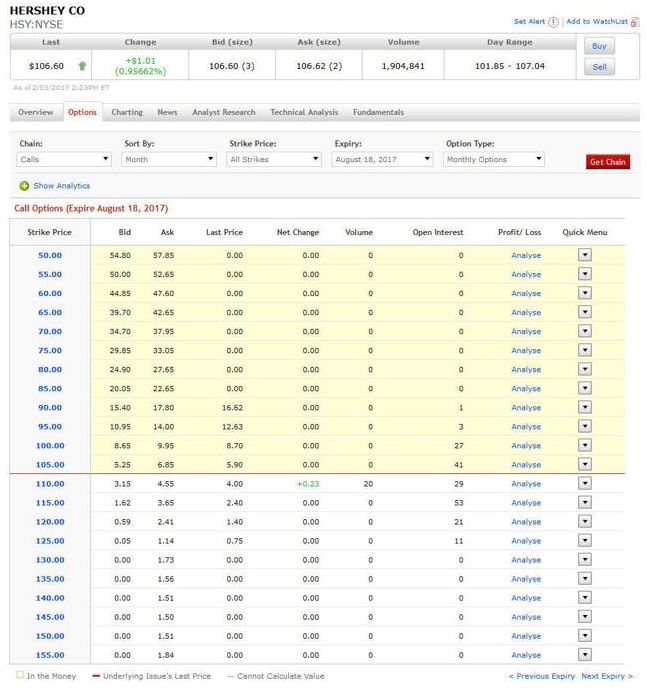

If you happen to already own HSY, you may wish to employ a covered call option strategy. This could be one way to extract a little bit more juice from HSY.

If you write an out of the money $115 call with an August 18, 2017 expiry, you would receive roughly $2.40/share. If the stock price stays below $115 you get to keep your shares and the premium (minus commission of course). If the stock price rises above $115, you would be obligated to sell your shares for $115 OR you could close out your position and sell another call for a higher strike price and further out on the calendar.

Here is a snapshot of the Call Options using the parameters noted above. Clearly, this is not the only options strategy you could deploy but this post is already long enough.

Source: Scotiabank – HSY Call Option Strategy

Hershey Stock Analysis – Final Thoughts

HSY is not a company where I envision a huge run-up in the stock price. While there might be the occasional uptick every time a takeover offer comes along, I really don’t see The Hershey Trust Company, which holds the lion’s share of the voting rights, ever agreeing to sell. In essence I don’t see HSY’s stock price going through the roof any time soon.

In addition, I do not view the current dividend yield as being attractive.

If you intend to purchase HSY, or to continue to hold it as we will (our average cost is $47.43), you should probably just accept that HSY will continue to plod along. The stock price will likely continue to tick up over the long term and the dividend will increase consistently over time. That is probably the most you can expect but sometimes, “boring” can be “sexy”….especially when markets correct.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long HSY.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.