![]()

Summary

- Cisco has shifted to more of a software and subscription-based offerings is resulting in more revenue predictability.

- It has an extremely strong balance sheet and generates significant FCF on an annual basis.

- An investment in Cisco offers investors the opportunity to have exposure to the technology sector without having to assume the potential of significant volatility.

Introduction

In the vast majority of the companies in which I have invested, long-term investors have been greatly rewarded. Within the past 10 years many of my investment holdings have increased threefold to tenfold; I can assure you these companies are not speculative in nature.

Cisco Systems, Inc. (NADAQ: CSCO), however, is a completely different story as it has only increased about 2.5Xs in value. I did not, however, make this investment in the hopes of possibly generating significant capital gains. This investment was made because I recognized a need to generate income from our investments to service our ongoing obligations. This is because:

- My wife and I are retired with absolutely no intent of ever returning to the workforce because we need to generate income;

- I generally just acquire shares in high quality publicly traded companies and very rarely sell.

Given the above, we hold investments in various companies where the reliability of a growing stream of dividend income (keeping in mind I am not a yield chaser) was more of a deciding factor than the potential for the investment to generate significant capital gains.

You may recal that CSCO rocketed to stratospheric valuation levels during the ‘dot.com’ craze. I recollect co-workers who were ‘day trading’ in this company in late 1999/early 2000.

While many companies in the ‘Technology’ sector founded in the 1980s and 1990s were ‘flame outs’, CSCO continues to thrive; it was founded in 1984 and today it now generates ~$49.3B in annual revenue.

I never had the intestinal fortitude to initiate a position in CSCO until November 2010. By then, the stock price was roughly 28% of that evidenced at the height of the ‘dot.com’ craze.

When I initiated my position, CSCO had not yet initiated a dividend. Given its ongoing profitability and the billions of dollars of cash and short-term investments it had on its balance sheet, however, I strongly suspected a dividend policy would be put in place and that it would start paying a dividend in short order; within a few months of initiating a position, it announced (March 2011) its first quarterly dividend.

Over the next several months I continued to acquire shares at a relatively depressed stock price fully anticipating that CSCO would continue to reward shareholders with anual dividend increases.

Where does CSCO stand on the dividend front today?

Well…what started off as a $0.06/quarter dividend is now a $0.33/quarter dividend. Based on the stock price as at the time this article is being composed, the dividend yield is ~3%. Not super generous but the dividend payout ratio is conservative to the extent where the probability of a dividend cut is remote.

Another positive aspect about CSCO is that the CSCO of today and CSCO of yesteryear are different. It has been transforming itself toward more of a software-style focused company with recurring revenue. This transition has negatively impacted revenue growth results in the past couple of years but it now appears to be entering a period of solid and predictable growth rates.

Under new accounting standards, the timing of CSCO’s revenue is changing. Under the old accounting standard, a product sold for $100 would result in ~$75 of this revenue being recognized up front; the remaining $25 would be recognized over a period of 3 years.

Under the new accounting standard, more revenue will be recognized upfront thus boosting sales numbers. There will, however, still be ~10% – 11% of deferred revenue. This revenue recognition change will help make CSCO’s revenue slightly more predictable.

Business Overview

CSCO’s business overview can be found in my May 19, 2018 article.

Subsequent to that article, CSCO announced its intent to acquire Duo Security for ~$2.35B with closing scheduled for Q1 2019. In the August 2nd Press Release, CSCO indicated that:

‘Duo Security is the leading provider of unified access security and multi-factor authentication delivered through the cloud. Duo Security’s solution verifies the identity of users and the health of their devices before granting them access to applications – helping prevent cybersecurity breaches. Integration of Cisco’s network, device and cloud security platforms with Duo Security’s zero-trust authentication and access products will enable Cisco customers to easily and securely connect users to any application on any networked device.’

The presentation provided at the time of CSCO’s August 2nd announcement of its intent to acquire Duo Security can be found here.

On August 15th Q4 and FY2018 Earnings Release conference call with analysts, CSCO indicated that Duo’s SaaS delivered solution will expand CSCO’s cloud security capabilities so as to help enable any user on any device to securely connect to any application on any network. By combining CSCO’s network, end point, and cloud security platform with Duo’s zero trust authentication and access solutions, CSCO will broaden the industry’s most effective security architecture in the market.

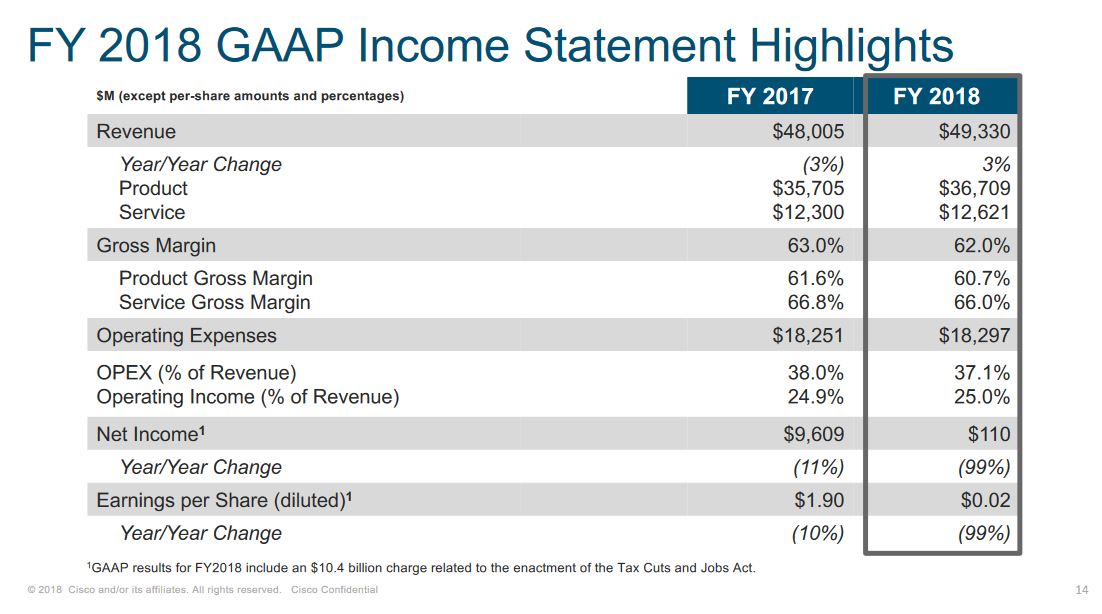

Q4 and FY2018 Financial Results

On August 15, 2018, CSCO reported Q4 and FY2018 results.

CSCO’s revenue grew for the third consecutive quarter. It reported revenue of $12.84B versus consensus expectations of $12.77B with full-year revenue growth of ~2.7% to $49.3B; in FY2017, CSCO reported full year revenue of ~$48B.

FY2018 marks CSCO’s first full fiscal year of appreciable revenue growth since FY2015. This growth was propelled partly by the Catalyst 9000, a software-centric switch introduced in 2017 that moves Cisco toward more recurring revenue.

The transitioning toward more of a software-style focus with recurring revenue has negatively impacted CSCO’s revenue growth results in the past couple of years but CSCO appears to be entering a period of solid and predictable growth rates.

Another noticeable change has to do with the timing of revenue recognition. CSCO’s CFO has indicated that under the old accounting standard, if CSCO sold a product for $100, it would recognize approximately $75 up front. The remaining $25 would be recognized over a period of three years. Under the new accounting standard, more revenue will be recognized upfront thus boosting sales numbers. There will, however, still be ~10% – 11% of deferred revenue. This will certainly help make CSCO’s revenue slightly more predictable.

Source: CSCO – Q4 FY2018 Earnings Presentation – August 15, 2018

Q1 2019 Guidance

On the August 15th analyst call, CSCO provided Q1 guidance. It expects 5% – 7% revenue growth; the new accounting standard that requires CSCO to recognize more of its contracted revenue up front will provide slight boost (roughly 1%).

CSCO anticipates the:

- non-GAAP gross margin rate to be in the range of 63% – 64%;

- non-GAAP operating margin rate to be in the range of 30% – 31%;

- non-GAAP tax provision rate of 19%;

- non-GAAP EPS from $0.70 – $0.72;

- GAAP EPS $0.69 to $0.74.

This guidance includes CSCO’s service provider video software solutions business it has recently agreed to sell. CSCO recently announced the sale of its Service Provider Video Software Solutions (SPVSS) business for ~$5B. This transaction is expected to close in the first half of fiscal 2019 subject to customary closing conditions and regulatory approvals.

Guidance also excludes the Duo Security acquisition.

Credit Ratings

There has been no change to CSCO’s credit ratings subsequent to my last article. Moody’s rates CSCO’s long-term debt A1 (top tier of the upper medium grade range) and S&P Global rates it AA- (top tier of the high grade range).

These credit ratings give me comfort that CSCO can adequately service its obligations.

Dividend, Dividend Yield, Dividend Payout Ratio and Share Repurchases

CSCO’s dividend and stock split history can be found here. I envision a $0.03 – $0.04 dividend increase will be announced within the first couple weeks of December.

Currently, the $1.32 annual dividend provides a yield of ~2.9% on the basis of the current $45.38 stock price (August 16, 2018).

The following reflects the extent to which CSCO has repurchased shares and distributed dividends in FY2018.

Source: CSCO Q3 2018 Earnings Conference Call – May 16, 2018

In my May 19, 2018 article I indicated that CSCO had announced a $25B increase to the share repurchase program authorization to $31B and that it expected to utilize this authorization over the next 18 to 24 months. A significant proportion of the funds for this share repurchase program will come from CSCO’s repatriation of $67B of offshore funds to the U.S. which was previously ‘trapped’ prior to the implementation of the Tax Cut and Jobs Act.

Valuation

CSCO reported $0.02 in GAAP EPS for FY2018 versus $1.90 in FY2017. FY2018 GAAP results, however, include a $10.4B charge related to the enactment of the Tax Cuts and Jobs Act comprised of $8.1B for the U.S. transition tax, $1.2B for foreign withholding tax, and $1.1B for the re-measurement of net deferred tax assets.

If we adjust for these one-time charges, CSCO’s non-GAAP EPS amounted to $2.60/share versus $2.39/share in FY2017.

CSCO has only provided guidance for Q1 but 29 analysts have provide a full year mean adjusted EPS estimate of $2.97. On the basis of the current $45.38 stock price I arrive at a forward adjusted PE of ~15.3.

I am of the opinion that the current valuation level is fair and CSCO should be able to reward long-term investors with a low double digit return over the next several years.

Final Thoughts

One of the nice things about investing in a cash rich company such as CSCO (~$46.5B in cash and short-term investments as at FYE2018) is that it can make a methodical and calculated transition to more of a software-style focused company without having to be worried how a change of this magnitude will impact its financial stability. A heavily leveraged company with a poor credit rating would definitely be facing an uphill battle if it tried to make changes to the extent of those made by CSCO over the past couple of years.

Technology companies can experience significant volatility in their stock prices. While I had virtually no exposure to the Technology sector during the ‘dot.com’ era, I witnessed co-workers losing several hundred thousand dollars of their investments. As a result, I am satisfied with being exposed to a ‘plodder’ like CSCO for a portion of my exposure to the Technology sector.

I view CSCO as currently being fairly valued. I will not be acquiring additional shares as I view my 807 shares as being a reasonable position; the dividends (net of the 15% withholding tax) are being automatically reinvested thus resulting in our position in CSCO increasing by ~5 shares/quarter.

I hope you enjoyed this post and I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long CSCO.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.