![]()

Summary

- CSCO continues to shift toward the development and sale of more software and subscription-based offerings so as to improve the predictability of its revenue.

- It has an extremely strong balance sheet and generates significant FCF on an annual basis.

- I expect investors will continue to be rewarded with double digit percentage annual dividend growth.

- CSCO has a $31B share repurchase program authorization which is expected to be utilized over the next 18 to 24 months.

- CSCO is not as attractively valued as at the time of my February 15, 2017 article. I am, however, of the opinion investors with a 10+ years investment time horizon will be aptly rewarded through an investment in CSCO at current levels.

Introduction

I have mentioned in previous articles that many investors rely almost exclusively on stock screeners to identify investment opportunities. I do not dispute that stock screeners can assist in distilling the universe of companies into a smaller subset of companies that warrant further analysis. Investors, however, should be cognizant that the output based on certain search parameters can eliminate truly wonderful companies.

In some cases, these ‘eliminated’ companies have truly superior balance sheets. They also have competitive advantages which enable them to quickly increase their earnings power in ways that a cursory analysis of certain metrics does not make apparent.

Examples of such companies include Berkshire Hathaway (NYSE: BRK-a and BRK-b), Microsoft (NASDAQ: MSFT), Johnson & Johnson (NYSE: JNJ), Visa (NYSE: V), MasterCard (NYSE: MA), and Cisco (NASDAQ: CSCO). For the sake of full disclosure, shares in all aforementioned companies are held in the FFJ Portfolio (details disclosed to Financial Freedom is a Journey subscribers) or in accounts that are kept confidential.

This article addresses my rationale for holding CSCO and why I am of the opinion it is extremely important to pay attention to valuation levels in your investment decision making process.

In my February 15, 2017 CSCO article I concluded with:

‘I see it more as a company that will continue to plod along, will generate strong cash flow, and will continue to reward shareholders with steady dividend increases. There is absolutely nothing wrong with a company of this nature and if CSCO’s profile now fits your investment criteria, I would not hesitate to acquire some shares over the course of a few months.’

My sentiment has not changed even though CSCO is no longer as attractively valued as at the time of my previous article.

At the time of that article, CSCO was trading at ~$33, non-GAAP diluted EPS for FY2017 was projected to come in at $2.34 (~14.1% forward adjusted PE), diluted GAAP EPS was expected to come in at ~ $1.90 (~17.4% forward PE), and the FY2017 dividend of $1.10 yielded ~3.3%.These metrics alone, were sufficiently attractive to warrant further analysis by a potential investor.

If such an investor had undertaken a review of the Q2 2017 10-Q, they would have noticed CSCO had ~$72B in cash and short-term investments versus ~$62.4B in TOTAL liabilities.

CSCO has since reduced its cash and short-term investments to ~$54.4B and its total liabilities amount to ~$67.4B as at Q3 2018. A significant proportion of this reduction in cash and short-term investments relates to $11.1B charge resulting from the enactment of the Tax Cuts and Jobs Act ($8.9 billion related to the U.S. transition tax, $1.2 billion related to foreign withholding tax and $1.0 billion related to the re-measurement of net deferred tax assets. The remaining $0.2 billion was related to other significant tax matters).

Despite this significant change in cash and short-term investments relative to TOTAL liabilities, a company with such a high quality balance sheet should certainly pique an investor’s attention.

Business Overview

CSCO has been designing and selling a broad range of technologies that have been powering the Internet since 1984.

CSCO competes in a highly competitive space and technological change is rapid. In addition, CSCO’s customers / prospects are adding billions of new connections to their enterprises and are looking for intelligent networks that provide meaningful business value through automation, security, and analytics. Given this, CSCO’s vision is to deliver a highly secure, intelligent, platform for digital businesses and its strategic priorities include accelerating the pace of innovation, increasing the value of the network, and delivering technology the way its customers want to consume it.

In order to remain competitive in the rapidly evolving world of technology, CSCO announced a significant transformation in its reporting structure. The rationale for this change was so as to better align CSCO’s product categories with its evolving business model. The segments, however, continue to be based on geographies which consist of the Americas, EMEA, and APJC.

Effective Q1 FY 2018, CSCO reports its product and service revenue in the following categories:

- Infrastructure Platforms

- Applications

- Security

- Other Products

- Services

The following is a mapping of CSCO’s prior to new categories.

Source: CSCO – Change in Product Categories Presentation October 23, 2017

Remaining competitive has also meant partnering with Google and multiple acquisitions.

As part of CSCO’s evolution, CSCO announced in June 2017 the initial development of new network product offerings that feature “intuitive” networking technology. This is an intent-based networking platform designed to be intelligent, highly secure, powered by “intent” and informed by “context”. This technology aims to constantly learn, adapt, automate and protect in order to optimize network operations and defend against an evolving cyberthreat landscape. CSCO is applying the latest technologies such as machine learning and advanced analytics to operate and define the network. These new product network offerings are designed to enable customers to detect threats in encrypted traffic.

The new Catalyst 9000 series of switches represent the initial foundation of CSCO’s intent-based networking capabilities. They provide highly differentiated advancements in security, programmability, and performance, while lowering operating costs by innovating at the hardware and software layer.

CSCO has experienced very strong adoption by customers with over 5,800 customers on this series of switches despite shipments only having started June 21, 2017; it is the fastest ramping product introduction of CSCO’s history.

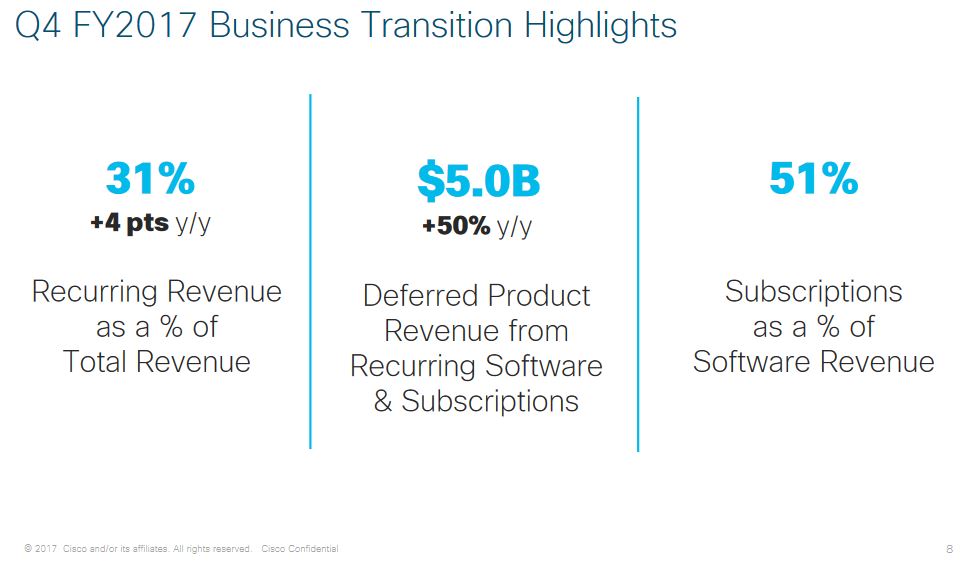

In order to meet evolving customer needs, CSCO is shifting to develop and sell more software, subscription-based offerings, and perpetual licenses. This is expected to increase the level of CSCO’s recurring revenue.

CSCO’s progress to reduce the lumpiness of its revenue through ongoing efforts to improve the level of recurring revenue is borne out from the following images extracted from the 4 most recent quarterly results presentations.

Source: CSCO – Q4 FY2017 Earnings Presentation – August 16, 2017

Source: CSCO – Q1 FY2018 Earnings Presentation – November 15, 2017

Source: CSCO – Q2 FY2018 Earnings Presentation – February 14, 2018

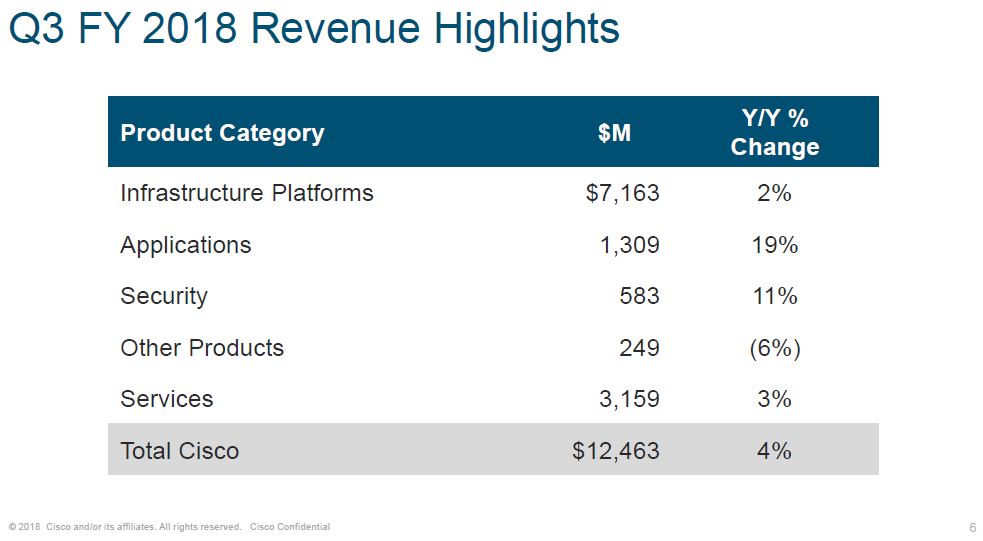

Source: CSCO – Q3 FY2018 Earnings Presentation – May 16, 2018

Source: CSCO – Q3 FY2018 Earnings Presentation – May 16, 2018

Q3 2018 Financial Results

On May 16, 2018, CSCO reported Q3 2018 results.

Source: CSCO – Q3 FY2018 Earnings Presentation – May 16 2018

In Q1, CSCO reported a 2% year over year (YoY) contraction in overall revenue, and 3% YoY growth in Q2. In Q3, CSCO reported 4% YoY revenue growth with Q4 revenue projected to grow 4% – 6% YoY.

YTD gross margin has dipped to ~62.2% versus ~63.2% for the same period FY2017. This was the result of softer pricing and higher component costs on both the product and service sides.

Management has forecast Q4 gross margin of 63% – 64%. A full year gross margin of 63% would exceed CSCO’s FY 2011 – 2015 gross margin and would be comparable to that in FY2016 and 2017.

Credit Ratings

Moody’s rates CSCO’s long-term debt A1 (top tier of the upper medium grade range) and S&P Global rates it AA- (top tier of the high grade range).

These credit ratings give me comfort that CSCO can adequately service its obligations.

Free Cash Flow (FCF)

CSCO consistently generates a considerable amount of FCF on an annual basis which it can then deploy to enhance shareholder value. In FY2016 it generated ~$12.4B and in FY2017 it generated ~$12.9B. Management projects FY2018 will be another strong year of FCF.

Dividend, Dividend Yield, Dividend Payout Ratio and Share Repurchases

CSCO’s dividend and stock split history can be found here. While CSCO only initiated its quarterly dividend in 2011 at $0.06/share, the dividend has been increased at least annually to the point where the quarterly dividend is now $0.33/share.

On the basis of a $1.32 annual dividend and the $43.21 closing stock price on May 18, 2018, the dividend yield is ~3.05%.

The following images reflect the extent to which CSCO has repurchased shares and distributed dividends in FY2017 and the first 3 quarters of FY2018.

Source: CSCO Q4 2017 Earnings Conference Call – August 16, 2017

Source: CSCO Q4 2017 Earnings Conference Call – August 16, 2017

Source: CSCO Q3 2018 Earnings Conference Call – May 16, 2018

Source: CSCO Q3 2018 Earnings Conference Call – May 16, 2018

In Q2 2018, CSCO announced a $25B increase to the share repurchase program authorization to $31B and that it expected to utilize this authorization over the next 18 to 24 months. A significant proportion of the funds for this share repurchase program will come from CSCO’s repatriation of $67B of offshore funds to the U.S. which was previously ‘trapped’ prior to the implementation of the Tax Cut and Jobs Act.

CSCO needs to repurchase a sizable amount of shares annually as it issues a significant number of shares under its Employee Stock Purchase Plan and its share-based compensation arrangements. Please refer to the #14 – Employee Benefit Plans section in the FY2017 10-K which starts on page 110 of 275. CSCO employees, and executives to a greater extent, really stand to benefit from the appreciation in CSCO’s stock price subsequent to the beginning of 2016!

Valuation

CSCO is a classic example of why it is imperative you pay particularly close attention to valuation in your investment decision making process. If you access the Investment Calculator on CSCO’s site and plug in different investment start dates you will see a huge disparity in investment returns depending on the investment start date.

I distinctly remember co-workers investing in ‘high tech’ companies during the dot.com era. Those investments were certainly not made on the basis of sound investment analysis!

A $10,000 investment in CSCO on June 19, 2000, for example, would only be worth $7,753.21 (with dividends reinvested) or $7,103.91 (without dividend reinvestment) 17.92 years later.

$10,000 invested on November 16, 2010 (the date of my initial CSCO investment), however, would have resulted in a current value of $27,249.12 (with dividends reinvested) or $25,179.12 (without dividend reinvestment) 7.5 years later.

The investment returns are remarkably different depending on when you invested in CSCO. The reasoning for this is that CSCO’s valuation during the dot.com craze was totally detached from reality. The same rationale explains why I am highly reluctant to invest in Amazon (NASDAQ: AMZN) even though it is a great company. A great company does not necessarily represent a great investment and a great investment does not necessarily represent a great company!

While CSCO has reported a GAAP EPS loss of $0.76 for the first 3 quarters of FY2018 this is primarily attributed to the previously mentioned $11.1B charge related to the enactment of the Tax Cuts and Jobs Act. If we adjust for non-recurring charges, CSCO has generated $1.90 in non-GAAP earnings for the first 9 months of FY2018. It has also projected GAAP EPS of $0.55 – $0.60 for Q4. Using the mid-point of this range we can expect CSCO to generate ~$2.48 in non-GAAP EPS for FY2018.

CSCO closed at $43.21 on May 18, 2018. On this basis, CSCO’s forward PE on the basis of adjusted EPS is ~17.4. While this level is slightly higher than the ~14 – ~15.7 levels when I wrote my February 15, 2017 article, I am of the opinion that the current valuation level is sufficiently reasonable where long-term investors can expect to realistically generate a low double digit return.

Final Thoughts

I recognize CSCO is not of the same quality as the other companies referenced in the Introduction of this article; those are the companies in which you should feel reasonably comfortable in taking outsized positions.

While CSCO is no longer as attractively valued as when I reviewed it February 15, 2017, I am of the opinion it has a reasonably good chance of generating a double digit investment return over the next 10+ years. It has a strong core business and the decision to increase the recurring revenue component is, in my opinion, a sound decision in that the revenue stream will be more predictable.

I expect CSCO will continue to generate significant positive cash flow. This should enable it to repurchase a significant number of shares annually going forward and to continue to reward shareholders with annual dividend increases. I, therefore, recommend CSCO as a long-term investment.

For the sake of full disclosure, I currently hold 802 CSCO shares in the FFJ Portfolio and I increase my exposure quarterly by 5 shares through the automatic reinvestment of the quarterly dividend (shares are held in a non-registered account which means I incur a 15% withholding tax on the quarterly dividends).

I hope you enjoyed this post and I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long CSCO, BRK-b, MSFT, JNJ, V, and MA.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.