This company may appeal to investors seeking exposure to the Technology sector who also want to generate an increasing stream of dividend income.

Summary

- This company’s shift to more of a software and subscription-based offerings is resulting in more revenue predictability.

- The company has an extremely strong balance sheet and generates significant FCF on an annual basis.

- An investment in this company offers investors the opportunity to have exposure to the technology sector without having to assume the potential of significant volatility.

Introduction

In the vast majority of the companies in which I have invested, long-term investors have been greatly rewarded. Within the past 10 years many of my investment holdings have increased threefold to tenfold; I can assure you these companies are not speculative in nature.

The company covered in today’s article, however, is a completely different story as it has only increased about 2.5Xs in value. I did not, however, make this investment in the hopes of possibly generating significant capital gains. This investment was made because I recognized a need to generate income from our investments to service our ongoing obligations. This is because:

- My wife and I are retired with absolutely no intent of ever returning to the workforce because we need to generate income;

- I generally just acquire shares in high quality publicly traded companies and very rarely sell.

Given the above, we hold investments in various companies where the reliability of a growing stream of dividend income (keeping in mind I am not a yield chaser) was more of a deciding factor than the potential for the investment to generate significant capital gains.

The company analyzed in this article rocketed to stratospheric valuation levels during the ‘dot.com’ craze. In fact, I recollect co-workers who were ‘day trading’ in this company in late 1999/early 2000.

While many companies in the ‘Technology’ sector founded in the 1980s and 1990s were ‘flame outs’, this company continues to thrive; it was founded in 1984 and today it now generates ~$49.3B in annual revenue.

I never had the intestinal fortitude to initiate a position in this company until November 2010. By then, this company’s stock price was roughly 28% of that evidenced at the height of the ‘dot.com’ craze.

When I initiated my position, this company had not yet initiated a dividend. Given its ongoing profitability and the billions of dollars of cash and short-term investments it had on its balance sheet, however, I strongly suspected a dividend policy would be put in place and that the company would start paying a dividend in short order; within a few months of initiating a position, this company announced (March 2011) its first quarterly dividend.

Over the next several months I continued to acquire shares in this company at a relatively depressed stock price fully anticipating that this company would continue to reward shareholders with anual dividend increases.

Where does this company stand on the dividend front today?

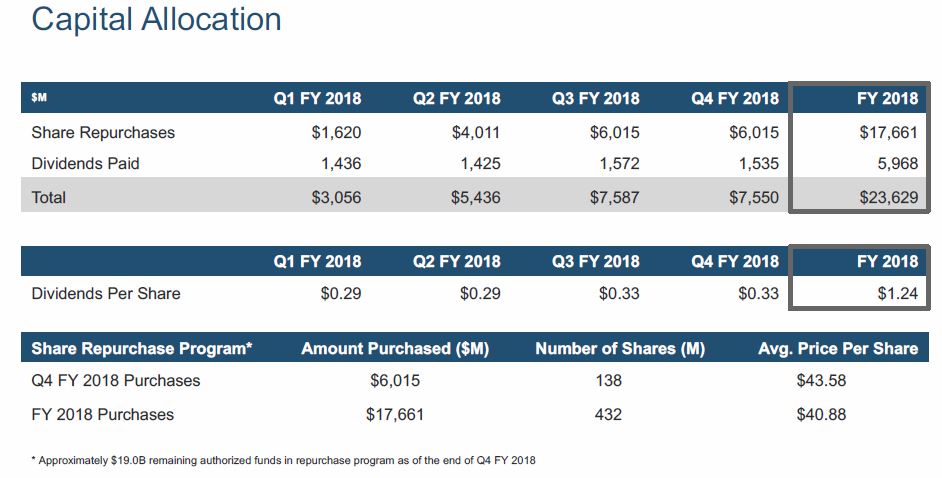

Well…what started off as a $0.06/quarter dividend is now a $0.33/quarter dividend. Based on the stock price as at the time this article is being composed, the dividend yield is ~3%. Not super generous but the dividend payout ratio is conservative to the extent where the probability of a dividend cut is remote.

Another positive aspect about this company is that the company of today and the company of yesteryear are different. This company has been transforming itself toward more of a software-style focused company with recurring revenue. This transition has negatively impacted revenue growth results in the past couple of years but the company now appears to be entering a period of solid and predictable growth rates.

Under new accounting standards, the timing of this company’s revenue is changing. Under the old accounting standard, a product sold for $100 would result in ~$75 of this revenue being recognized up front; the remaining $25 would be recognized over a period of 3 years.

Under the new accounting standard, more revenue will be recognized upfront thus boosting sales numbers. There will, however, still be ~10% – 11% of deferred revenue. This revenue recognition change will help make this company’s revenue slightly more predictable.

Please click here to read the complete version of this article.

Members of the FFJ community can access reports I generate on high quality companies which add long-term shareholder value. In an effort to help you determine whether my offering is of any value to you I am pleased to offer 30 days’ free access to all sections of my site. No commitments. No obligations. That’s 30 days from the time you register at absolutely no cost to you!