This company has transformed itself radically over the past few years having gone from a predominantly Canadian exposure to one where the majority of revenue is derived from the US.

Based on current metrics, investors can earn a ~6% dividend yield if they participate in the company’s dividend reinvestment program.

Summary

- This company has more than doubled its annual revenue since FY2015.

- Growth is being generated primarily from the US, as opposed to Canada, subsequent to the completion of a very significant acquisition in 2016.

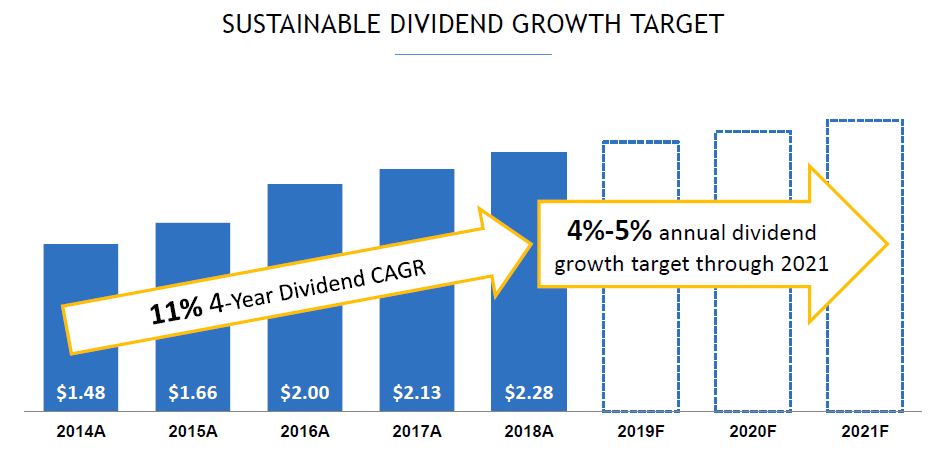

- The company will be incurring significant CAPEX over the next few years. As a prudent measure, the historical dividend growth has been scaled back so as to incorporate a higher component of internally generated funds in the capital plans to fund these accretive investments.

- The company’s dividend is attractive and deemed safe which will make this stock appealing to investors seeking dividend income.

All figures are reported in CDN $ unless otherwise noted.

Introduction

My most recent article covered a company that would appeal to investors seeking long-term capital growth as opposed to a steadily increasing source of dividend income. The company covered in today’s article will most likely appeal to investors seeking a safe stream of quarterly dividend income.

This company recently announced a ~4% dividend increase. Based on the stock price as at the time this article is being written, the dividend yield is ~5.85%. This yield is further enhanced if you elect to enrol in the company’s DRIP (dividend reinvestment program); the company’s DRIP stipulates that ‘there may be a discount of up to 5% from the average market price for shares purchased in connection with the reinvestment of cash dividends’.

Business was predominantly generated from within Canada but over the past couple of years the company has transitioned to one where a majority of its earnings comes from its US subsidiaries. The rationale for this company’s expansion into the US market is because that market:

- offers the ability to generate higher returns;

- there are superior growth opportunities.

Due to this company’s recent radical transformation, comparing the company of today and that of the past is ill-advised; the company’s revenue has more than doubled to over $6.2B (FYE2017) versus ~$2.8B as at FYE2015 (it generated ~$1.3B in annual revenue in FY2008).

This growth has come primarily by way of acquisition. Growth has been financed through the raising of additional equity and considerable additional debt. Moody’s and S&P Global, however, have not amended this company’s long-term unsecured debt ratings in several years.

Furthermore, Goodwill, that intangible asset that arises when a buyer acquires an existing business, has ballooned as a result of these acquisitions.

Nova Scotia Power generates allowed returns that are generally lower than in the US. It typically enjoys a lower cost of capital than U.S. counterparts and it is not subject to an annual general rate base review, which can increase regulatory uncertainty.

The Newfoundland and Labrador transmission projects and Brunswick pipeline offer strong efficient scale advantages. Capital costs for competing transmission systems would be too high to offer a sufficient return on capital for new entrants.

The Caribbean utility portfolio faces higher political risk when compared with Canadian and US utility portfolios. It is, however, granted meaningfully higher allowed returns to compensate for this additional risk.

Please click here to read the complete version of this article.

Members of the FFJ community can access reports I generate on high quality companies which add long-term shareholder value. In an effort to help you determine whether my offering is of any value to you I am pleased to offer 30 days’ free access to all sections of my site. No commitments. No obligations. That’s 30 days from the time you register at absolutely no cost to you!