Summary

Summary

- This Wal-Mart (NYSE: WMT) stock analysis is based on Q4 and FY2017 results released February 21, 2017.

- WMT reported $4.38 Diluted EPS from continuing operations.

- Total revenue of $485.9B increased 0.8% or 3.1% to $496.9B if currency adjustments are excluded.

- Operating income decreased 5.6% to $22.8B or decreased 2.9% to $23.4B when currency adjustments are excluded.

- $31.5B in operating cash flow and $6.2B in dividends and $8.3B in share repurchases.

- WMT generated just under $21B in FCF!!!

Introduction

I think it is only fair that I should preface this Wal-Mart Stores Inc. post with full disclosure of the following:

- I currently hold, and have held, WMT shares for years in my Registered Retirement Savings Plan (RRSP) and also since October 21, 2015 in the FFJ Portfolio.

- All dividends have been automatically reinvested.

- The average cost of all our WMT shares is substantially below the current market price of just below $72.

My take on how WMT has rewarded us is, therefore, significantly different from readers who have acquired shares during the 2012 – 2017 period with the exception of a brief period in late 2015 when WMT’s share price tanked.

If you access WMT’s Investment Calculator and enter various “Start” dates you will be able to see why so many investors view WMT to have been a poor investment relative to many other potential investments in the universe.

Wal-Mart and Technology

When investors think of technology in the retail environment, Amazon (NASDAQ: AMZN) will probably spring to mind before WMT. Don’t, however, rule out WMT completely. It is spending a ton of money on technology because it knows that if it does not it will have a huge detrimental impact to its business with each passing generation of consumers.

In Ancaster, an affluent suburb of Hamilton, Ontario, for example, WMT has a supercentre designed for the digital age. What it is doing is making big bets on product lines for which consumers tend to come into the store to purchase (eg. groceries, toys, childrens’ clothing, health and wellness products) and scaling back on other product lines where consumers are more inclined to shop online (eg. furniture, cribs, strollers).

At the store’s entrance, shoppers are given a scanning gun as part of WMT’s “Scan & Go” test program. Consumers can use these scanners to scan each purchase they decide to make as they move throughout the store. By the time consumers get back to the checkout counters, their bills are already tallied. Early indications are that consumers are, on average, purchasing 18 items when they use these scanners versus 13 on regular shopping trips.

Plans are to roll out these scanners to 20 more stores in Canada. In addition, plans are for consumers to be able to scan using their own mobile devices before the end of 2017!

Apparently, this is the first year since WMT arrived in Canada in 1994 that it will NOT be opening a new store. Money that would have normally been spent in this regard is being redeployed to help WMT adapt to the new ecommerce landscape and in revamping its 400+ stores, some of which look pretty dated.

In essence, WMT is looking to lure shoppers back to its stores. This includes widening aisles by a foot to help consumers navigate their way through the stores more easily. In addition, as previously noted, it is devoting more space to some departments and scaling back in others. The areas used for car seats, adult apparel, large furniture, paint, hardware are all shrinking in favor of more space for such departments as children’s toys and apparel.

On the fresh food front, WMT is introducing walk-in refrigerated rooms much like Costco’s (NASDAQ: COST) “cooler” rooms.

Bring consumers back to the stores? Of course! Even AMZN is experimenting with high-tech physical stores.

PHEW! This certainly is reassuring to read given that I also hold 1000+ shares in Smart REIT (TSX: SRU.UN) in the FFJ Portfolio. The fact WMT is spending a ton of money to upgrade its existing stores is a good sign for this landlord!

Clearly, WMT has to get it right. In the 2nd and 3rd quarters of 2016, same-store sales at outlets that had been opened for 1+ years only increased by 1.1% in each quarter. This is lower than in 2015 when WMT benefited from TGT’s exit from Canada.

Despite this miniscule increase in quarterly sales, WMT Canada is stealing market share from its competitors in the health and wellness, consumer products, and food categories. These 3 categories alone are estimated to make up more than 50% of all its sales in Canada; in 2013 these made up 43%.

And it is not just on the shopping front where WMT is rolling out new technology! Before I retired in May 2016, I was aware that WMT was already experimenting with the use of “G4S – CASH360” machines in some of its North American stores. My understanding is that pilot results were such that WMT was looking to expand the use of these machines. (Please note that while I have provided a link to G4S’s service, by no means am I suggesting that they are the only company which competes in this space or that their solutions are the best).

There are varying types of machines but the most sophisticated machines would permit the dumping of money in the cashiers’ tills into a repository. The machines would count and sort the money. Once a certain dollar value was reached in the machine, the “excess” money would be automatically moved into a safe and secure compartment without any human intervention; these funds would no longer be accessible to WMT employees. Only the armored car carrier employees would be able to open these compartments.

Once the money moved to this safe and secure compartment, WMT’s bank would give it immediate value for these funds even though the funds were still on WMT’s premises.

The money that had not been transferred to the safe and secure compartment could still be used by the store for normal business purposes.

Now pause for a moment and imagine millions of dollars in hundreds, and potentially thousands, of machines that no longer need to be picked up daily by armored car companies yet WMT is still getting immediate value for those funds. Instead of a daily armored car pick up you now go down to 2 – 3 times/week. You think WMT might save a buck or two?

In addition, can you imagine a higher interest rate environment where WMT is getting credit for billions of dollars 1 – 2 days sooner!

Sure, the cost of each machine and installation is significant but I am certain WMT is not going to introduce something of this magnitude if the payback period is lengthy. I am not privy to WMT’s decision making process on this front but I suspect a payback period in the form of several months or 1 – 2 years versus several years is the more likely scenario.

Furthermore, I am not privy to whatever WMT has negotiated with their bank to take advantage of immediate access to funds that are still on WMT’s premises. You have to figure WMT’s banker will want to get some form of compensation since it does not have these funds for its immediate use.

Wal-Mart and Jet.com

Most readers are probably well aware that in August 2016 WMT acquired Jet.com for $3.3B. At the time this was the largest purchase of an e-commerce startup in the U.S.. The rationale behind the acquisition was that WMT felt Jet.com would complement the significant foundation WMT already had in place to serve its customers across the WMT app, site, and stores. WMT made this strategic acquisition because it felt it would be better positioned for even faster e-commerce growth by expanding customer reach and adding new capabilities.

Additional information about WMT’s plans with Jet.com can be found here and here and here.

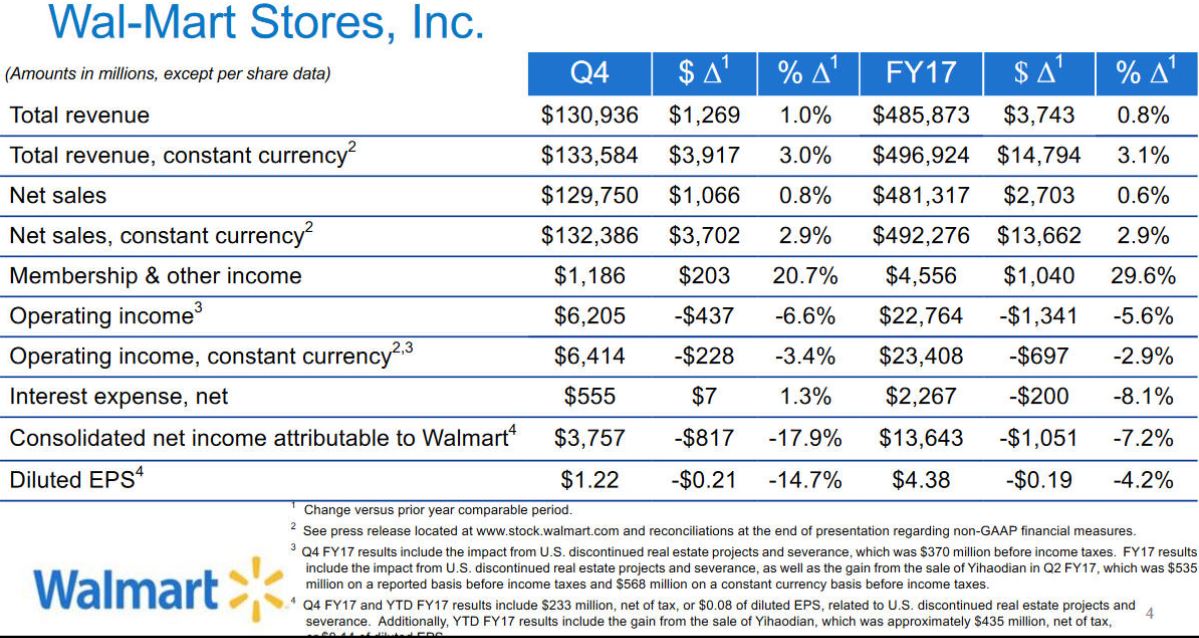

Q4 and FY2017 Financial Results

On February 21, 2017 WMT released its Q4 and FY2017 results. Note that WMT’s fiscal year end was January 31, 2017.

Q4 Highlights

- Diluted EPS of$1.22, which includes the impact of items detailed in the February 21, 2017 press release (refer to Reconciliations of and Other Information Regarding Non-GAAP Financial Measures) or $1.30 when excluded.

- Total revenue of $130.9B increased 1%. Excluding currency adjustments, total revenue was $133.6B a 3.0% increase.

- S. comp sales increased 1.8%, driven by 1.4% traffic increase and Neighborhood Market comps increased approximately 5.3%.

- E-commerce growth at WMT U.S. and Gross Merchandise Volume (GMV) increased 29.0% and 36.1%, respectively, including Jet.com and online grocery.

- Net sales at WMT International decreased 5.1% to $31.0B. Excluding currency adjustments, net sales increased 3% to $33.7B.

- $11.9B in operating cash flow $3.6B in dividends and share repurchases.

Fiscal 2017 highlights

- $4.38 Diluted EPS from continuing operations which includes certain discrete items detailed in WMT’s press release. Excluding these items, EPS was $4.32.

- Total revenue of $485.9B increased 0.8%. Excluding currency adjustments, total revenue increased 3.1% to $496.9B.

- Operating income decreased 5.6% to $22.8B. Excluding currency adjustments, operating income decreased 2.9% to $23.4B.

- $31.5B in operating cash flow and $14.5B in dividends and share repurchases.

WMT Q4 and FY 2017 results

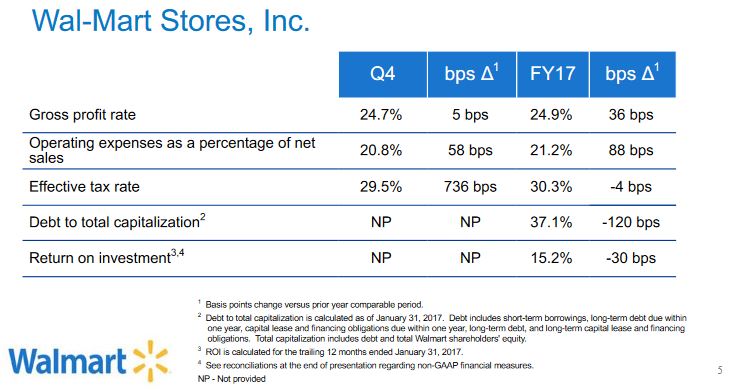

WMT FY2017 GP, Op Exp, Eff Tax Rate

WMT FY2017 Dividends, Share Repurchases, FCF

Outlook for Fiscal 2018

I won’t go into detail on WMT’s outlook for FY 2018. It you wish to see its guidance for WMT as a whole, WMT US, WMT International, and Sam’s Club you can look at WMT’s February 21, 2017 “Presentation Supporting Transcript”.

Wal-Mart 2018 Guidance

Valuation

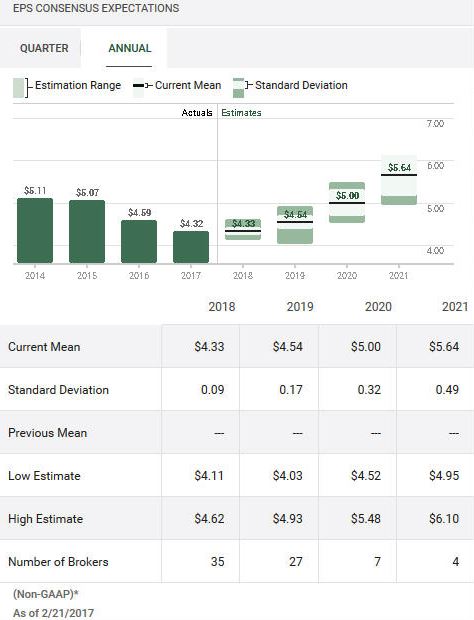

So, WMT releases guidance for FY2018 for EPS of $4.20 – $4.40 on the basis of FX rates remaining at current levels. If you look at the projected mean EPS from 35 analysts you will see they expect WMT to hit $4.33. Another source I use reflects a projected mean EPS of $4.31.

I like to be conservative so let’s say I arbitrarily go with $4.31. The current stock price as I compose this is $71.52 so on the basis of a projected EPS of $4.31, I get a PE of 16.60. Is that an acceptable level for a company of WMT’s quality? From my perspective….absolutely.

Source: TD WebBroker – WMT Quarterly EPS estimates

Source: TD WebBroker – Annual EPS estimates

Source: ValuEngine – WMT Quarterly EPS estimates

Source: ValuEngine – WMT Annual EPS estimates

Let’s look at WMT on the basis of its dividend yield. WMT’s dividend history can be found here and the Press Release announcing the increase to the current $0.50/quarter can be found here).

I recognize some readers will frown upon WMT’s $0.01/quarter dividend increase and 2.80% dividend yield. Sure, the increase is definitely on the skinny side. I, however, feel far more confident WMT will be able to continue to increase its dividend when the dividend payout ratio is only 45.5% – 47.6% (using WMT’s guidance for FY2018 EPS of $4.20 – $4.40) versus many other companies with far more dramatic growth in their dividend but far higher dividend payout ratios. I am also aware that some high dividend yielding companies are not just returning money in the form of a return on capital but also in the form of a return OF capital.

Why I Think Now Is the Time to Buy Wal-Mart

There are various reasons why investors invest in companies. You can either be seeking dividend income or capital gains. I recognize you may have other reasons for investing in a company but I think these are the most two common reasons.

I know we always want to get the best price possible when we buy shares but you and I know that rarely happens. Furthermore, how many of us are buying tens of thousands of shares? So WMT popped a bit today which means if you buy today versus yesterday you’re going to pay a bit more. Put it in perspective. Think many years down the road when you hopefully still own your WMT shares. Today’s jump will seem insignificant in the great scheme of things.

In addition to the dividend increase to $2.00/year, what appeals to me is that WMT is repurchasing a TON of its shares. In the past fiscal year WMT returned $6.2B in dividends and $8.3B in share repurchases.

The diluted weighted average number of shares outstanding as at FYE 2014, 2015, 2016, and 2017 amounted to (expressed in millions) 3,283: 3,243: 3,217: 3,112. Guess how many shares were outstanding on a diluted basis as at FYE2007? 4,168. Not a bad reduction in outstanding shares from my perspective.

How does that stack up against Amazon.com, Inc. (NASDAQ: AMZN)? Hint: Their share count isn’t going down.

Now don’t get me wrong. AMZN might have far more appeal than WMT to some investors. I am just reminded, however, that I witnessed some of my friends and coworkers who got decimated when they loaded up on the equivalent of FANG (Facebook, Amazon, Netflix, and Google) companies during the dot.com era.

Furthermore, I am in the retirement phase of my life. AMZN would be a totally inappropriate investment for me.

I also received an email this morning from a couple currently enjoying a ski vacation in the Rockies. In their email they indicated that their ability to retire at 58/60 was in no small part from their decision several years ago to invest in sound financial companies with a track record of success and a solid dividend history as opposed to high fliers.

You think boring isn’t sexy when it comes to investing? WRONG!

Option Strategy

While I include this section based on feedback received from some readers, I have avoided the use of Options for the very vast majority of my investment history. I do this because I have been successful without the use of options and because I am in general agreement with the findings of the 2008 Option Trading and Individual Investor Performance study.

Some readers, however, are far more astute than me when it comes to making money through the use of options strategies. If they work for you, continue to use to use them but be advised that any options suggestions I make will be pure plain vanilla strategies. I will not, for example, discuss the use of Butterflies and Condors. That, for me, would be like going down a rabbit hole.

Now that I have cleared that out of the way, let’s say you already own some WMT shares and you want to perhaps enhance your return. You could write a September 15, 2017 Call with a $75 strike price. You would receive about $1.57 for each share. Since each contract consists of 100 shares, if you decided to write 3 contracts you would receive 300 x $1.57 = $471 less commission.

Source: TD WebBroker: Wal-Mart CALL Option Chain September 2017 Expiry

If WMT stays below $75 between now and September 15, 2017, you would keep your shares and the option premium.

If it rises above this level, you could get called away which means you only get $75/share, you keep your option premium, but you no longer own the shares.

Should you not want to part with your WMT shares, you could close your option contracts at whatever the going rate is at the time (you could end up paying more than you received when you first wrote the contract) but then you could turn around and write new contracts further out into the future at a higher strike price. The premiums you receive for these new contracts could cover whatever money you laid out to close out your first set of contracts.

NOTE: As the owner of WMT shares, you receive the dividends during the period in which your option contracts are open.

Clear as mud? Sorry. There are certainly folks out there who can probably explain this way better than me.

Personally, I am not writing any options at this stage on the WMT shares we own. I perceive volatility to be very low which impacts option values. As mentioned in my Pepsico post I don’t mean to be flippant but writing a few contracts to make a few extra hundred dollars is not worth my time. In addition, I am also leaving for a ski vacation in a few days and I plan on taking other vacations in the not too distant future. I don’t want to be forced to always be checking to see the status of my option contracts.

Wal-Mart Stock Analysis – Final Thoughts

In my recent VF Corporation post I wrote that I was not prepared to buy VFC and that I thought there were better options out there. Some of you inquired what they were. Well…WMT.

Okay, I know. Some of you are raising your eyebrows right about now considering Berkshire Hathaway (NYSE: BRK.a, NYSE: BRK.b) unloaded a huge amount of its WMT shares. You’re probably thinking to yourself “Say no to crack!”.

No problem but here are the reasons I like WMT.

- When many investors are zigging, I try to zag. WMT is not an investment darling for many investors and has probably been written off as a “has been”.

- So many investors are going after the sexy stocks where PE ratios are either in the nosebleed levels of the investment stadium or are non-existent because there is no “E”.

- The stock price has really done nothing for a few years.

- The dividend yield is sub 3%. Yes, that can be a good thing just like dividend yields of 8%+ in this day and age can be a bad thing.

- WMT is buying back a ton of stock.

- WMT is making HUGE investments in its business to remain competitive and to bring consumers back to the stores.

- It is generating a ton of FCF!!!!

I hate to come across as a pessimist but I am becoming increasingly cautious about the North American stock market in general. I think way too many investors think stock prices can only go in one direction OR they think that if there is a correction it will only be of a very temporary nature. I’m not so sure about this.

I know WMT will likely never make it into many investment portfolios simply because some investors have an intense dislike for how they perceive WMT’s treatment of its suppliers and employees.

If you think AMZN is a far better company than WMT, perform a quick “How does Amazon treat its employees?” Google search. I don’t think it is going to win any “Employer of the Year” award.

In addition, Amazon opened two massive new warehouses within the past year about 10 – 15km from where I live. I saw billboards where they were advertising that they were looking for employees to work at these two locations. I don’t specifically remember the amount the billboards indicated you could earn per hour but I didn’t think the hourly rates that were posted were anything to write home about. And people complain about WMT’s pay brackets! NOTE: I am not talking about positions where you need some special skill.

Just because I think WMT is a decent investment opportunity at this stage does not mean that I encourage you to overweight WMT. Also keep in mind, that you know your investment profile and investment criteria far better than I do. If you are dead set against owning WMT for whatever reason…no problem.

Remember that if you chose to focus exclusively on stocks that soar with the eagles, be sure you don’t fly too high and get too close to the sun. You don’t want to burn your feathers and to come crashing down to earth because once you do, you’ll be in a whole different predicament and you’ll have pigeons poopin’ on your head and that’s no fun.

On a final note, this will be my last post until at least the second week of March. I’m going skiing!

I wish you continued success with your investments. Cheers.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long WMT.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.