Summary

Summary

- This UPS stock analysis is based on Q1 2017 results and forecast for the remainder of FY2017 which were released April 27, 2017.

- UPS has provided 2017 non-GAAP adjusted diluted EPS guidance of $5.80 – $6.10 with mean estimates from 26 brokers being $5.95 for FY2017.

- Amazon’s decision to reduce its reliance on traditional logistics companies is a risk UPS is addressing.

- UPS’s shares are at the upper end of my “buy zone”. I am buying with the view of holding shares long-term.

Introduction

On February 1, 2017, I wrote a post indicating United Parcel Service, Inc.’s (NYSE: UPS) stock price had retraced to the upper end of my “buy zone”.

Subsequent to my February post, the following events have transpired:

- Amazon (NASDAQ: AMZN) announced a major expansion plan in Kentucky in an effort to reduce its reliance on traditional logistics companies like UPS.

- UPS held an Investor Conference in February and released it Q1 2017 results at the end of April.

This post touches upon the above.

UPS’s February Investor Conference

This year’s central theme at UPS’s Investor Conference was “Invest. Grow. Deliver.” At this conference, management laid out its investment strategy for the next 3 – 5 years and indicated it was accelerating investment in its smart global logistics network; UPS expects $0.8B – $1B in annual cost savings and avoidance. This represents the most sweeping transformation of UPS’ network in decades.

A key focus going forward is to:

- Align price with cost-to-serve;

- Be compensated for product mix;

- Manage volume surges.

UPS’s plans include:

- Accelerating investment in its next-generation “Smart Logistics Network”;

- Leveraging the capital efficiency of the company’s global business model;

- Capturing market growth for on-line B-to-B and B-to-C customers;

- Investing aggressively in automation to drive improved performance;

- Providing customers with innovative solutions that drive their future growth;

- Deepening and widening capabilities in developed and emerging markets;

- Delivering long-term UPS shareowner value;

- Capital investments of 6% – 7% of revenue annually.

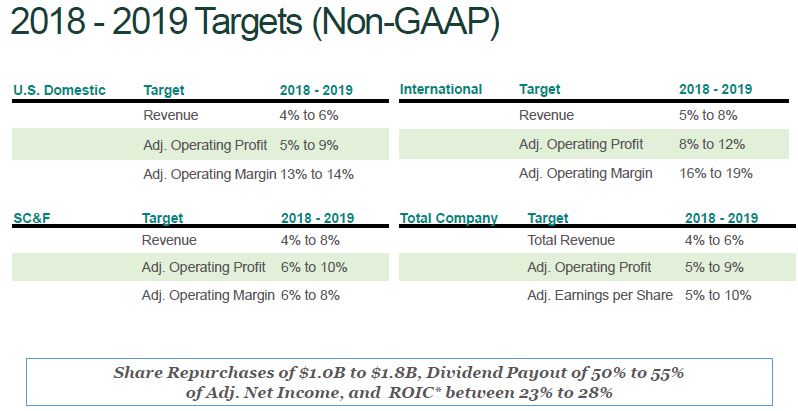

Highlights for the 2018 and 2019 long-term financial targets are:

- Total Revenue Growth: 4% – 6%;

- Adjusted Operating Profit: 5% – 9%;

- Adjusted Diluted EPS: 5% to 10%;

- Return on Invested Capital: 23% – 28%;

- Planned $1B – $1.8B in annual share repurchases;

- Dividend Payout of 50% – 55% of Adjusted Net Income.

As evidence of UPS’ commitment to Investing to Grow and Deliver, it:

- Has a number of global network automation projects underway;

- Will expand its U.S. delivery and pickup schedule to include 6 days for ground shipments. Rollout of Saturday delivery options to the largest metropolitan areas throughout the U.S. has already commenced;

- Deepened and widened its presence in key international markets;

- Purchased 14 new 747-8F from Boeing.

Q1 2017 Financial results, Outlook for remainder of Fiscal 2017, and 2018 – 2019 Targets

UPS reported its Q1 results on April 27, 2017. Highlights include:

- 2% revenue growth or 7.5% on a currency-neutral basis and $1.32 in Q1 EPS;

- A 5% increase in U.S. domestic revenue as package yield expanded on continued Ecommerce demand;

- $0.529B in International reported Operating Profit and currency-neutral Operating Profit of $0.648B;

- Building momentum in Supply Chain & Freight as Operating Profit jumped 22% on 13% Revenue growth;

- A $0.187B, or 43% over Q1 2016, total fuel expense increase. The fuel surcharge revenue lagged expense but a February 2017 surcharge change mitigates this negative variance for future periods;

- Dividends of $0.774B, a 6.4% increase from prior year. It also repurchased 4.2 million shares for approximately $0.45B.

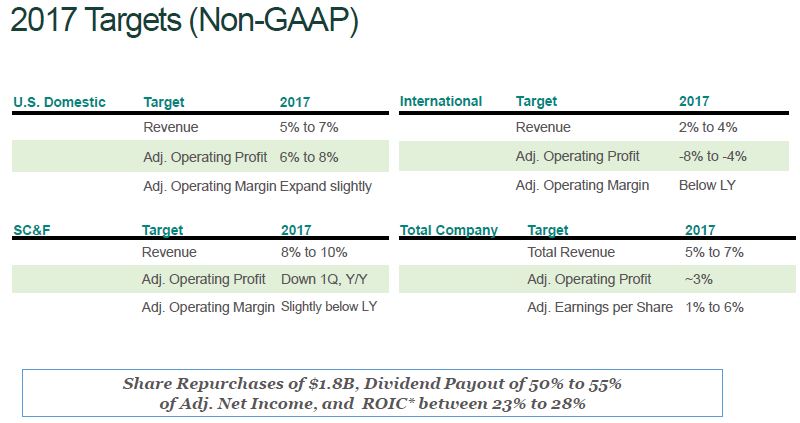

March 17, 2017 Presentation: UPS 2017 Targets

March 17, 2017 Presentation: UPS 2018 – 2019 Targets

In its 2017 forecast, UPS provided guidance on an adjusted (non-GAAP) basis. UPS’s reasoning for using adjusted figures is that it is not possible to predict or provide a reconciliation reflecting the impact of future pension mark-to-market adjustments, which would be included in reported (GAAP) results and could be material.

UPS is already seeing tangible results from its investment in ORION. Bottom-line results, however, are being challenged by a shift in product mix and the continued softness in industrial production.

UPS expects 2017 adjusted diluted EPS to be $5.80 – $6.10, which includes more than $0.4B of pre-tax currency headwinds. This currency drag is expected to lower the adjusted diluted EPS by $0.30 in 2017.

Competition from Amazon

AMZN recently announced it will build a $1.49B worldwide air services hub at Cincinnati/Northern Kentucky International Airport. The Amazon Prime Air hub will be the company’s largest in the world and will add to the 10,000 AMZN employees already based in Kentucky.

In an effort to reduce its reliance on traditional logistics companies like UPS and FedEx (NYSE: FDX), AMZN began leasing planes from air freight companies in 2016. Plans are to lease 40 cargo planes for its own shipping needs; 16 are already operating in its fleet.

In addition, AMZN has expanded its ground and sea transportation operations. It has a fleet of 4,000 semi-trucks for long-haul ground transportation. It also operates its own network of couriers which make deliveries in major urban areas.

Twenty different partners currently share the duties of shipping AMZN’s 600 million packages a year; FedEx, USPS, and UPS move the vast majority. Certainly, if AMZN were to handle the movement of all these packages through its own operations, this would be a huge blow to its existing partners. Fortunately, there are countless other companies which are expanding the e-commerce aspect of their business.

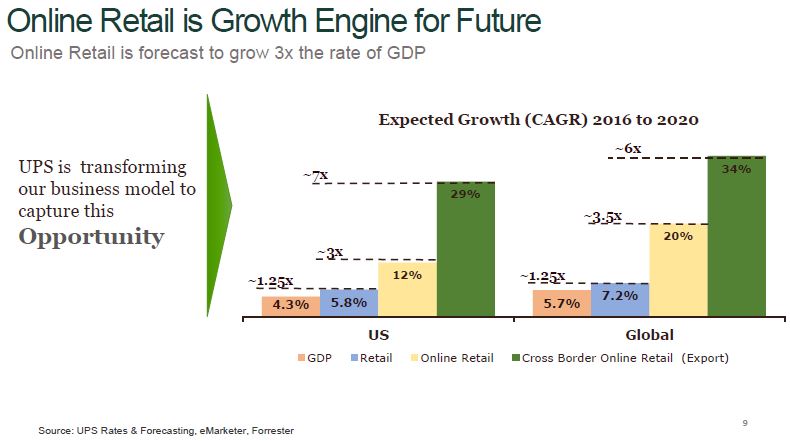

March 17, 2017 presentation: UPS Online Retail is Growth Engine for Future

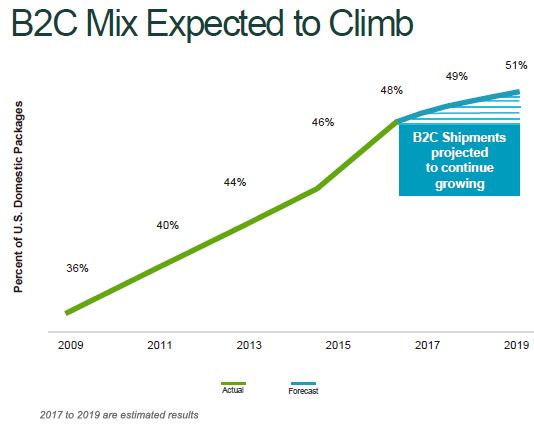

March 17, 2017 presentation: B2C Mix Expected to Climb

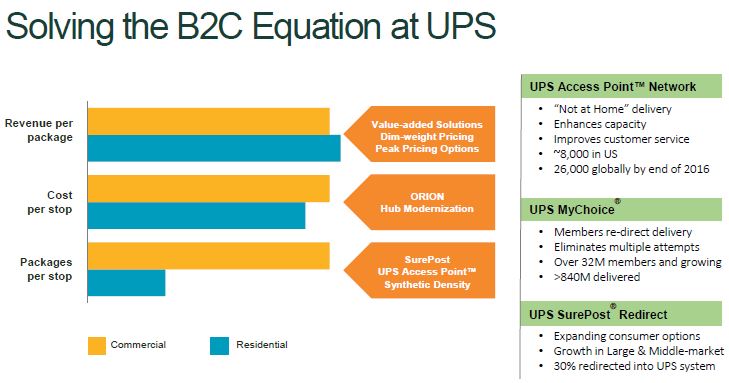

March 17, 2017 presentation: Solving the B2C Equation at UPS

AMZN’s entry into the logistics business is a risk that certainly did not exist a few years ago to the extent it exists today. Having said this, UPS’ senior management has had the foresight to identify this huge potential risk and several initiatives are in various stages of roll-out so as to remain at the cutting edge in the logistics business. Examples of such initiatives include:

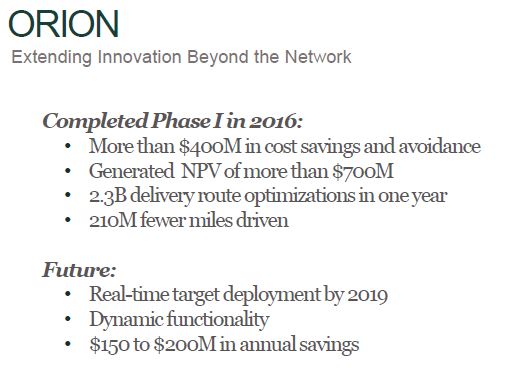

Project ORION (On-Road Integrated Optimization and Navigation).

March 17, 2017 Presentation: ORION Extending Innovation Beyond the Network

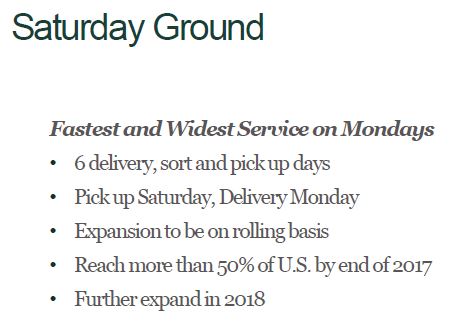

The expansion of Saturday ground delivery.

March 17, 2017 Presentation: UPS Saturday Ground

UPS is also embarking on the most sweeping transformation of its network in decades. This global transformation is being undertaken to further its “Smart Logistics Network”.

Over the next several years UPS will dedicate additional capital to the global UPS network. It will invest aggressively in new sorting capacity, new technology, new automation and new capabilities.

Further very high level details can be found in UPS’s March 16, 2017 presentation.

Valuation

At the time I wrote my UPS – It is Now in My “Buy Zone” post, the mean non-GAAP EPS earnings estimates from 24 brokers was $6.16 and $6.73 for FY2017 and FY2018.

Management is now projecting 2017 adjusted diluted EPS between $5.80 and $6.10. Revised non-GAAP EPS earnings estimates from 26 brokers are now $5.95 and $6.45 for FY2017 and FY2018.

Source: TD Bank WebBroker – UPS – Annual Earnings Estimates as at April 2017

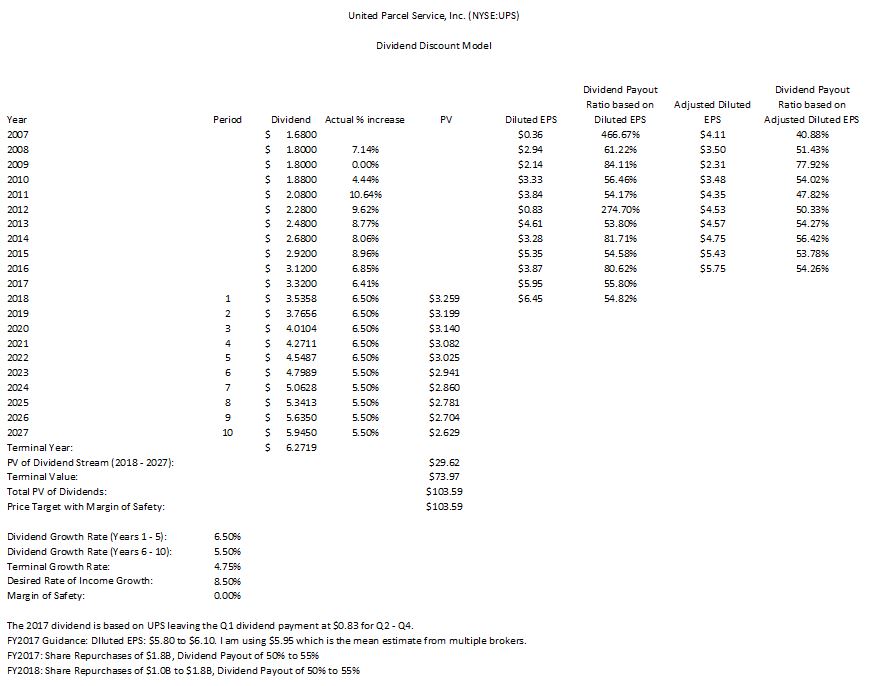

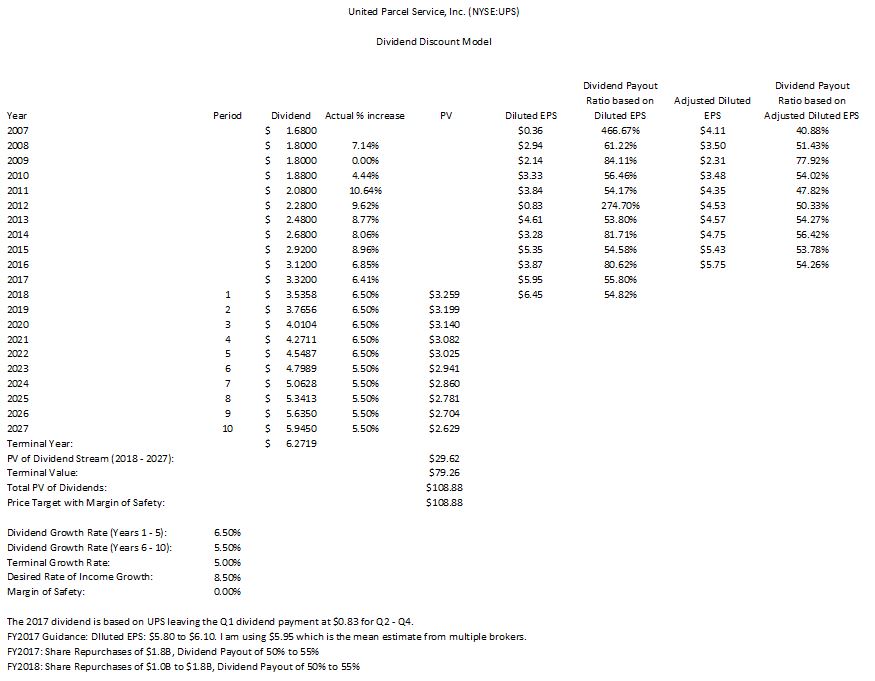

I reference my Dividend Discount Model (DDM) calculations below. There are multiple variables used in this model and slight variations in the metrics can materially impact the fair value calculation.

As you can see from my calculations below, if I use a terminal growth rate of 4.75% and leave the other metrics constant, the DDM generates a value of $103.59. If I use 5% for the terminal growth rate I get a value of $108.88.

UPS – Discount Dividend Model using a 4.75% terminal growth rate

UPS – Discount Dividend Model using a 5.00% terminal growth rate

Based on the historical dividend growth rate for 2007 – 2017, I have used an estimated dividend growth rate of 6.50% and 5.50% for years 1 – 5 and 6 – 10. I think these values are conservative and realistic.

Since the input values can materially impact the output from the DDM calculator, I also look at whether UPS’s current market value is reasonable by calculating its PE ratio using management’s EPS forecast range and the mean EPS estimate from multiple brokers.

UPS is currently trading at $107.46. Using 2017’s estimated mean EPS of $5.95 from 26 brokers, I arrive at a forward PE of 18.06. This PE level differs substantially from that found on Google Finance and Morningstar because these sites use actual EPS versus adjusted diluted EPS.

UPS, however, has clearly indicated (the bottom of page 3 of its Q1 earnings release) that guidance is provided on an adjusted (non-GAAP) basis because it is not possible to predict or provide a reconciliation reflecting the impact of future pension mark-to- market adjustments, which would be included in reported (GAAP) results and could be material.

In my opinion, an estimated forward PE of 18.06 is acceptable for a company of UPS’s quality.

I wish to avoid the need to liquidate investments for the purpose of funding our retirement lifestyle. I, therefore, look at the level of income I can generate from an investment and the relative safety of this stream of income. UPS’s dividend history gives me a reasonable level of confidence I can expect to continue to receive an uninterrupted stream of dividends.

March 17, 2017 Presentation: UPS Dividend History

UPS increased its $0.78 quarterly dividend to $0.83 in Q1 ($3.12/year in 2016 and $3.32 in 2017). On the basis of this dividend remaining constant throughout 2017 and the current $107.46 stock price, I get a dividend yield of 3.08%. This yield is acceptable to me given the current interest rate environment.

UPS Stock Analysis – Final Thoughts

I appreciate the risks posed by AMZN’s entry into UPS’s space. I am confident, however, that UPS’s management is taking the appropriate measures to remain at the forefront of its industry.

On a final note, the market correction I eagerly anticipate is taking far longer to materialize than I had hoped. While I continue to keep “powder dry” for deployment when stock prices retrace to bargain levels, I have been making occasional small share purchases in companies I desire to hold long term. In this regard, I have purchased additional UPS shares over the past 3 months.

Note: I appreciate the time you took to read this article and hope you got something out of it. As always, please email me any feedback and questions you may have.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence, and consulting your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long UPS, FDX (1.9% and 0.4%) of our overall holdings (not just in the FFJ Portfolio).

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.

Thanks for your research & blog. Could you tell your readers / followers what percentage of your portfolio each stock ( in this case UPS) represents. I doubt this is a core holding in your portfolio.

Secondly, I will like to know how your portfolio performs compared to IVV or DVY. Can an average investor beat a broadly Divesified index. I would hate to painstakingly build a portfolio of stocks that ends up under performing an ETF like NOBL. Since my ultimate goal is to achieve the highest return on my investment I am not keen on building a portfolio that ends up being self defeating.

Your research, thoughts and insights are appreciated. They have increase my investing “huttspa”.

Lovemydividends

Henry,

Excellent suggestion! I have amended my UPS post to address your suggestion as well as my TELUS post which I just uploaded earlier this morning. Please let me know if what I have done addresses your request.

As for how our overall holdings have performed relative to the ETFs you reference. Oh my! That would take me a bit of work. We hold 15 different investment accounts at 2 different financial institutions. UGH!

In order to answer your question without spending an inordinate amount of time on this exercise, I took all the investment statements as at December 31, 2016 and April 30, 2017. The difference between the 2 totals is ~$244K and the growth during the first 4 months of the year is ~7.72%. There have been no significant additional contributions made to any of the investment accounts other than the auto reinvestment of a little over $30K in dividends in the first 4 months of 2017. I let the difference between the dividends earned and the amount auto reinvested accumulate in cash. When this cash figure builds to a reasonable level, I buy more shares.

I know is this a very, very rudimentary way of calculating growth/return but I hope it meets your needs.

You can certainly acquire the ETFs referenced in your message. I prefer not to acquire ETFs since there are so many companies in each ETF I would never consider owning. Having said that, there are several companies in each ETF I do not own but wouldn’t mind owning. I just like purchasing shares versus ETFs because I am then in control of what I own. I also pay very little in the way of fees…probably lower than the ETFs you reference.

I think it all comes down to personal preference.

I would like to add more but have to rush off to a prior commitment. I hope this helps but if you want to discuss further I would be more than happy to.

Cheers.

Charles