All dollar values in this article are in Canadian Dollars (CDN) unless otherwise noted.

Summary

- This Intact Financial stock analysis is based on Q1 2017 results and OneBeacon proposed acquisition details which were both released May 2, 2017.

- Intact has an estimated 17% of Canada’s property and casualty insurance market.

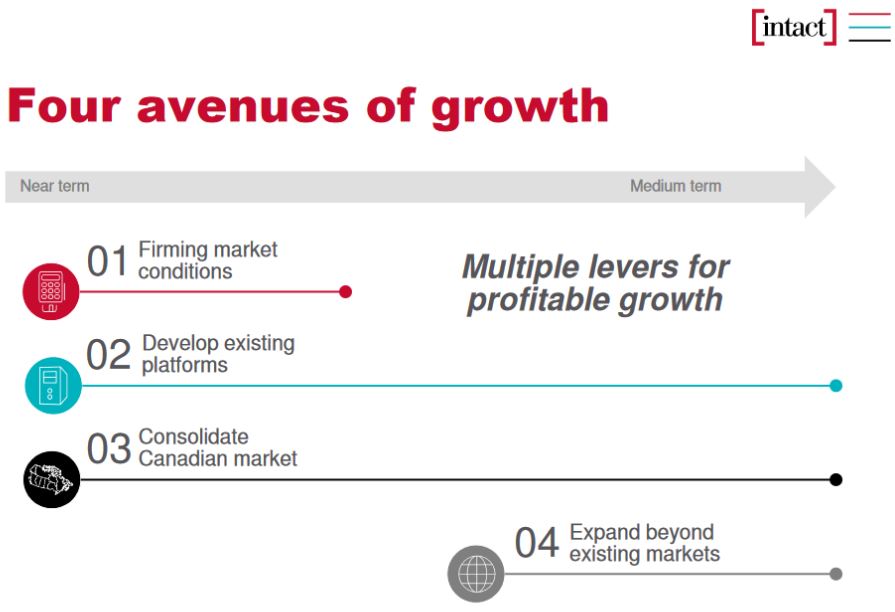

- Management previously communicated the expansion beyond existing markets as one of its 4 avenues of growth.

- On May 2, 2017, Intact released Q1 2017 results and announced the acquisition of OneBeacon, a US Specialty insurer. The acquisition is expected to close in Q4 2017.

- Intact appears overvalued but this is because earnings were temporarily depressed. I view Intact as fairly valued.

Introduction

I think it is only fair I describe my investor profile at the outset of this post. My rationale for doing this is so that you can quickly determine whether the companies I am prepared to expend time and energy to analyze for the purpose of potentially initiating a position or increasing a position would also suit your investor profile.

My wife and I retired in our early/mid 50s. Our game plan is to rely on a portion of our rental and dividend income to sustain our lifestyle; we wish to delay the collection of a Government of Canada pension as long as permitted. As a result, we primarily focus large- to mega-cap dividend-growth companies. We will, however, invest in mid-cap companies if they have:

- strong, experienced management teams;

- broad economic moats/sustainable competitive advantage;

- strong growth potential.

We acquire shares at what we believe to be fair prices, automatically reinvest the majority of the dividends we receive, and become more aggressive with our purchases when market conditions are depressed. I would like to think that we practice patience when initiating a position or making a meaningful addition to an existing position. This brings me to the subject of today’s post, Intact Financial Corporation (TSX: IFC).

In December 2004, ING Canada Inc. completed its IPO and in January 2007, we initiated a position in ING Canada Inc..

In early 2009, ING Groep, the Dutch banking and insurance giant, sold its interest in the Canadian entity. Following a CDN $2.2B private placement and secondary offering, the company was renamed Intact Insurance Company and institutional and retail investors acquired an ownership interest in one of Canada’s 60 largest publicly-traded companies. At the time it had a market cap of CDN ~$3.3B.

Business Overview

IFC currently has a market cap in excess of CDN $12B. It is Canada’s largest provider of property and casualty (“P&C”) insurance with almost CDN $8.3B in annual direct premiums written (“DPW”) and an estimated market share of 17%. It manages its investments which total CDN ~$14.4B and it insures in excess of 5 million individuals and businesses through its insurance subsidiaries (Intact Insurance Company, Belair Insurance Company Inc., The Nordic Insurance Company of Canada, Novex Insurance Company, Jevco Insurance Company, Canadian Direct Insurance Inc. (“CDI”), Trafalgar Insurance Company of Canada, Equisure Financial Network Inc., Canada Brokerlink Inc., Intact Farm Insurance Inc. and IB Reinsurance Inc.). It is the largest private sector provider of P&C insurance in British Columbia, Alberta, Ontario, Québec, Nova Scotia and Newfoundland & Labrador.

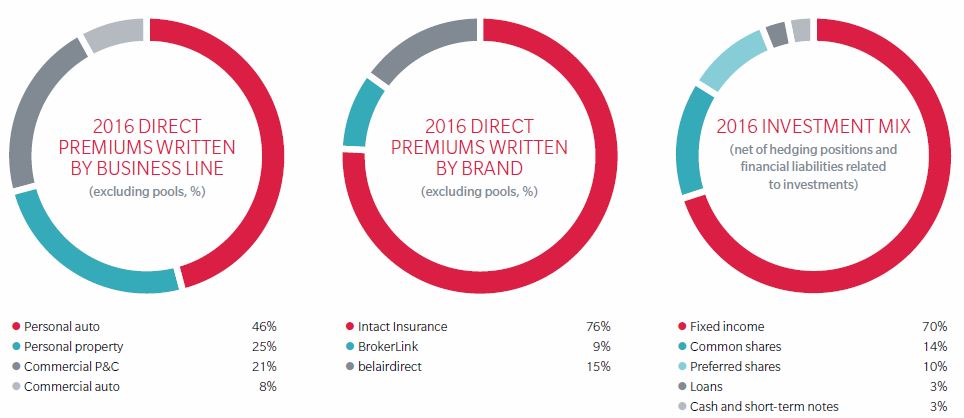

The following provides a high level overview of IFC’s source of revenue and investment mix.

IFC – Revenue and Investment Mix Source: IFC 2016 Annual Report

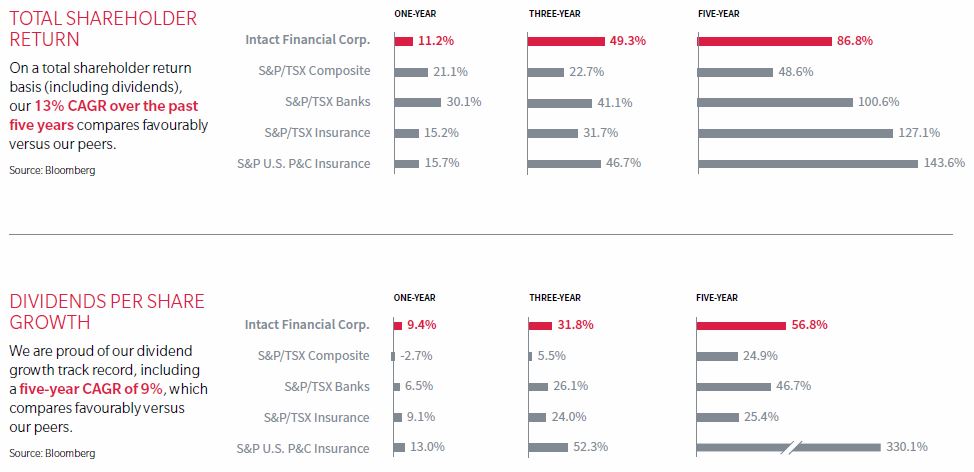

Subsequent to it 2004 IPO, IFC has rewarded its shareholders well although not to the same extent as its US peers.

IFC – Shareholder Return and DPS Growth Source: 2016 Annual Report

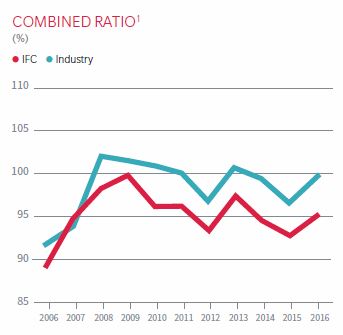

Conservative Underwriting

One of the best ways to measure the success of an insurance company is through the Combined Ratio. This is a measure of profitability which indicates the performance of daily operations. It does not include investment income and only includes profit earned through efficient management.

The Combined Ratio, expressed as a percentage, is calculated by dividing the sum of incurred losses and expenses by earned premium. A ratio below 100% indicates the company is making underwriting profit while a ratio above 100% means it is paying out more money in claims than it is generates in premiums.

It is important to note that even if the Combined Ratio exceeds 100%, a company can potentially still make a profit. This is because the ratio does not include the income received from investments. Having said this, an insurance company does not want to sustain a Combined Ratio in excess of 100% for an extended period.

IFC’s sophisticated pricing, underwriting discipline, and in-house claims expertise has enabled it to outperform the industry’s Combined Ratio.

Source: 2016 Annual Report

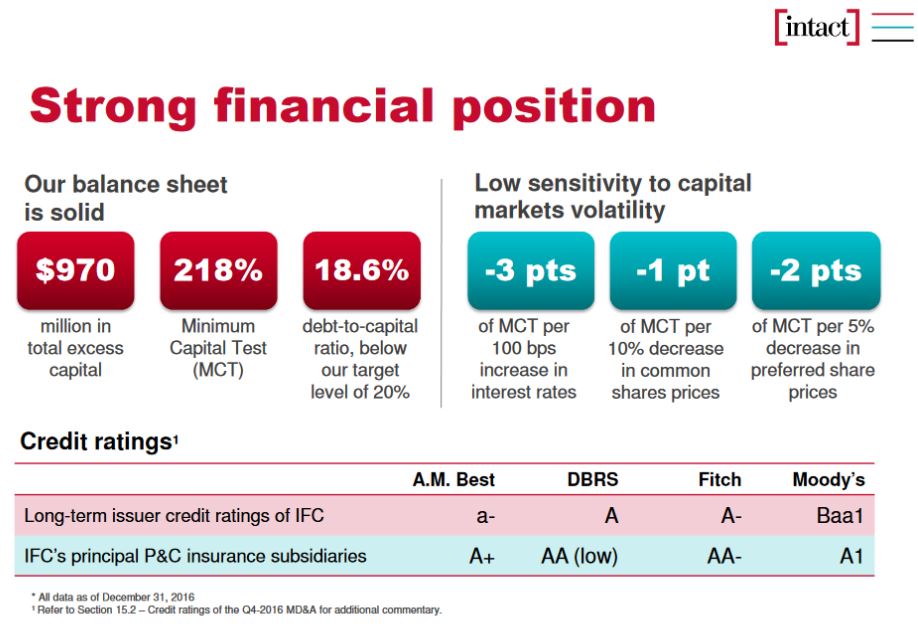

Financial Strength

IFC continues to maintain a strong financial position. Ratings agencies deem IFC’s debt to be “Good” credit quality with the capacity for the payment of financial obligations as substantial. While it may be vulnerable to future events, qualifying negative factors are considered manageable.

Source: March 6 2017 Investor Presentation

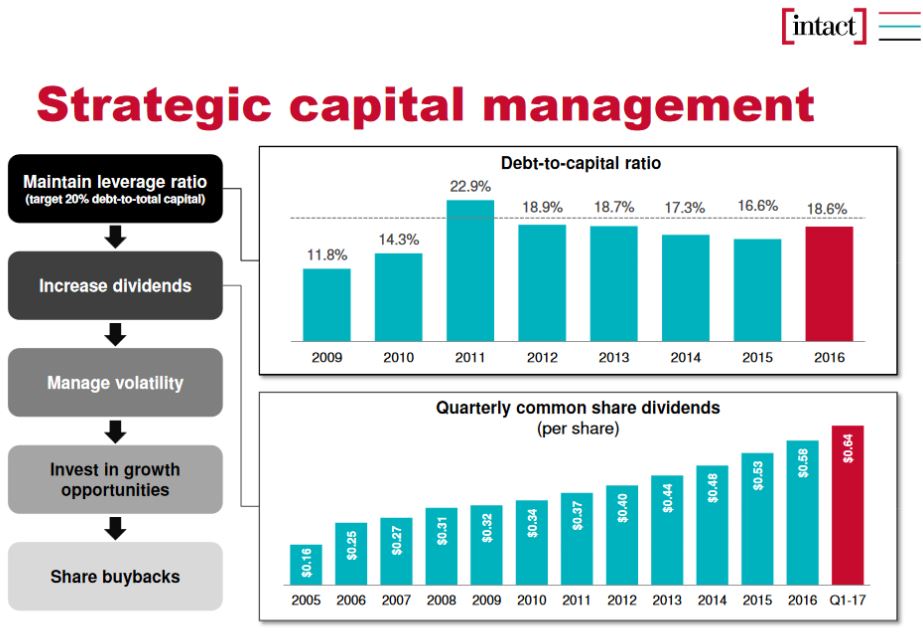

The following image provides a high level overview of how IFC manages its strategic capital.

Source: IFC March 6, 2017 Investor Presentation

Q1 2017 Financial Results

On May 2, 2017, IFC released its Q1 2017 results.

While IFC’s premiums grew 4% driven by personal and specialty lines, its performance was negatively impacted by severe weather events over the winter months and sub-par personal auto insurance results; the all important Combined Ratio metric increased to 98.2%. The was 5.7 points worse than the same period in the previous year and was due to an increase in weather related claims; this included 3.3 points of additional catastrophe losses, and lower favourable prior year claims development.

IFC’s Minimum Capital Test (MCT) at the end of Q1 2017 was estimated to be 223%. The MCT is a ratio of available capital to required capital. Canadian federally regulated property and casualty insurers, including IFC’s Canadian insurance subsidiaries, must meet a minimum capital test that assesses the insurer’s available capital in relation to its required capital and requires that available capital equal at least the minimum capital requirement. The Office of the Superintendent of Financial Institutions (OSFI) expects insurers to establish a target capital level above the minimum requirement, and maintain ongoing capital, at no less than the supervisory target of 150% of required capital under MCT. IFC has an internal operating target of 170%.

IFC had over CDN $1B in total excess capital and its CDN $43.14 book value per share represented an increase of 8% from a year ago.

Industry premiums are forecast to grow at a low to mid single digit rate.

- Personal auto: claims cost inflation should lead to further rate increases in all markets.

- Personal property: the current firm market conditions are expected to continue as companies are adjusting to changing weather patterns.

- Commercial lines: expected to remain competitive and the economy in Western Canada continues to pressure industry growth.

The industry’s ROE is expected to improve but remain slightly below its long-term average of 10% over the next 12 months.

Proposed Acquisition of OneBeacon

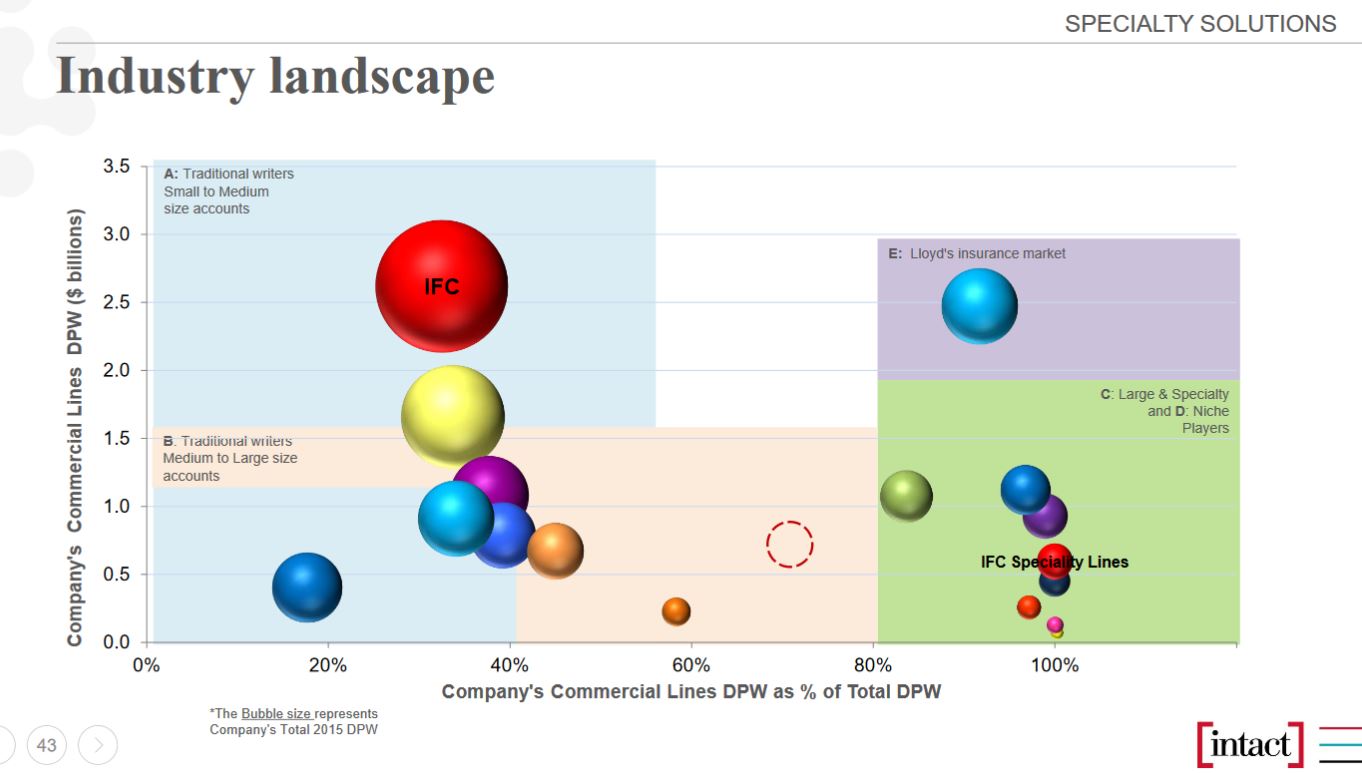

IFC outlined its 4 avenues of growth in its March 6, 2017 Investor Presentation. These avenues included expanding beyond existing markets.

Source: IFC March 6, 2017 Investor Presentation

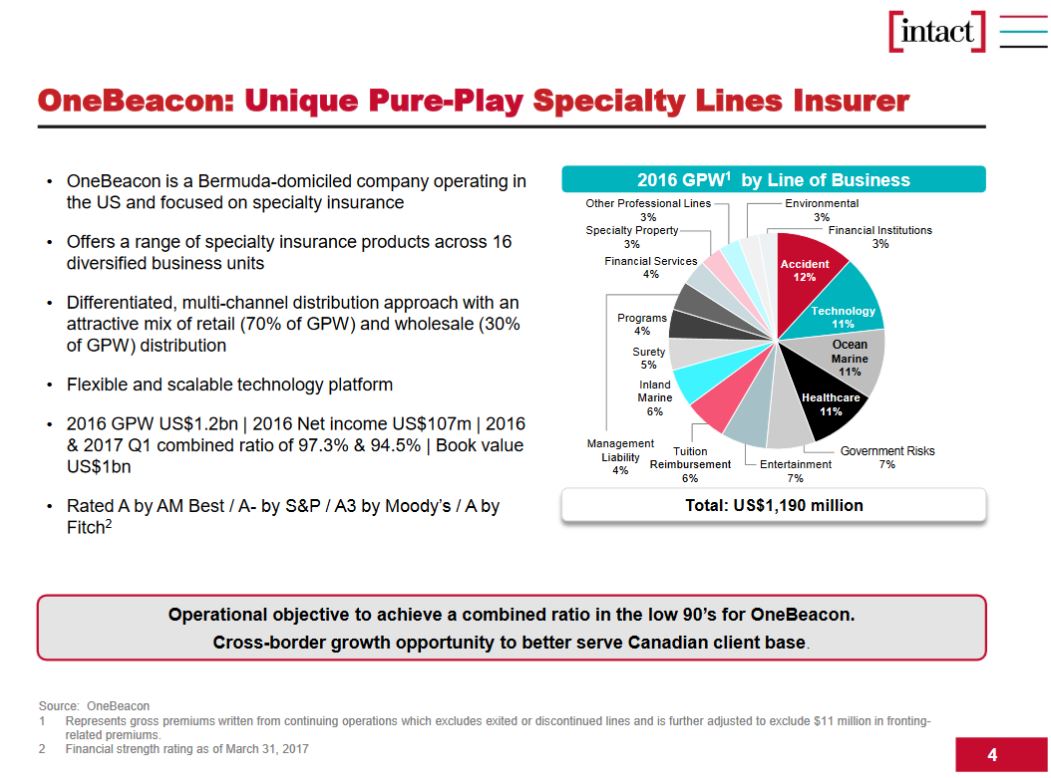

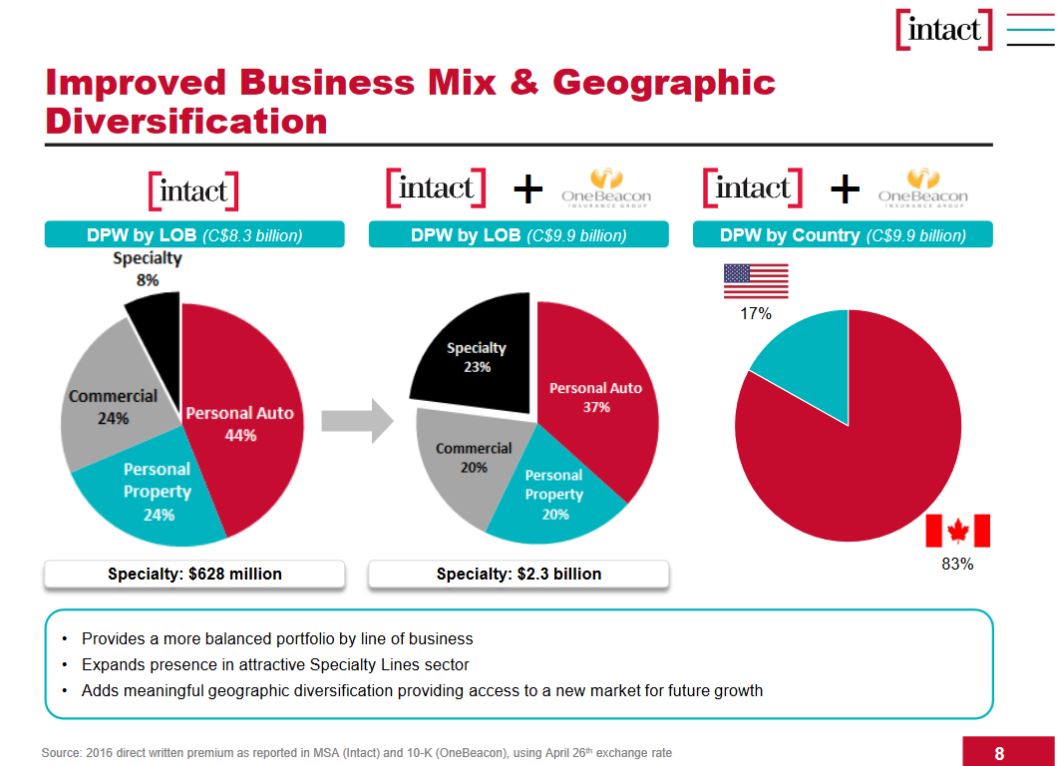

On May 2, 2017, IFC announced that it had entered into an agreement to purchase OneBeacon Insurance Group, Ltd. (NYSE: OB). OB, controlled by White Mountains Insurance Group Ltd. (NYSE: WTM), is a Bermuda-domiciled holding company which is a leading US specialty insurer which operates 15 specialty businesses with a variety of coverages and dedicated services in 50 states.

NOTE: WTM owned 75.7% of OB’s outstanding common shares, representing 96.9% of the voting power.

Source: IFC May 2, 2017 OneBeacon Proposed Acquisition Presentation

Source: IFC May 2, 2017 OneBeacon Proposed Acquisition Presentation

OB, headquartered in Minnesota, writes approximately $1.2B in annual premiums.

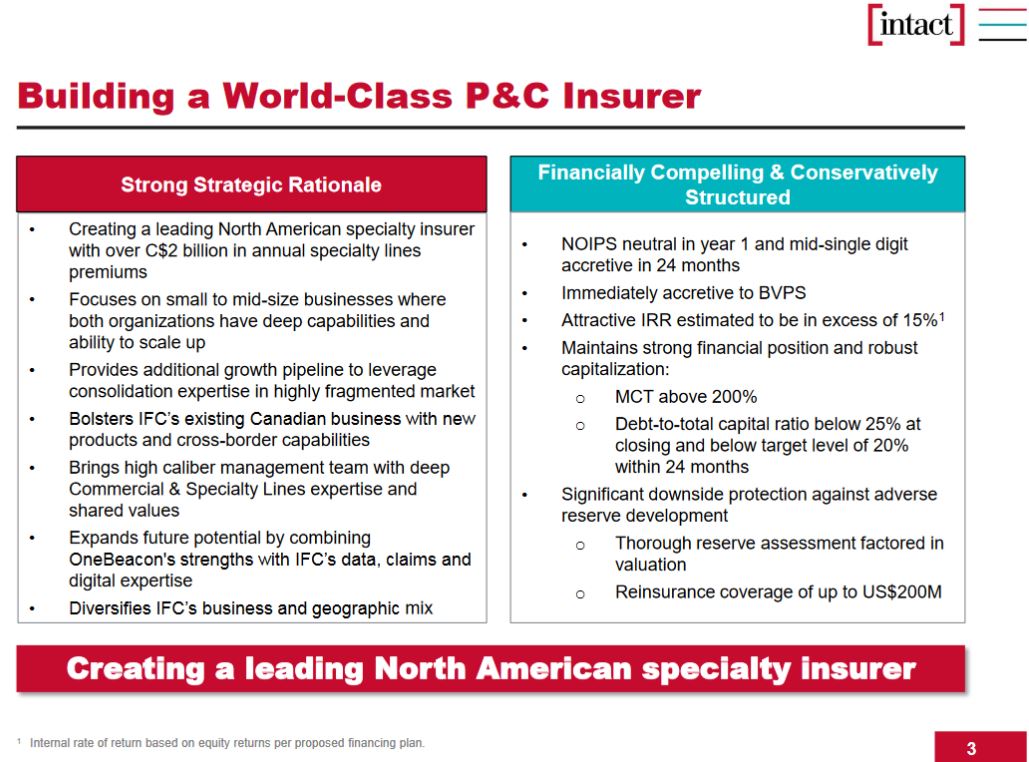

Combined with IFC’s existing specialty lines division in Canada, IFC will be creating a leading North American specialty insurer with over CDN $2B in specialty lines premiums with a focus on small- to mid-sized businesses.

Source: IFC May 2, 2017 OneBeacon Proposed Acquisition Presentation

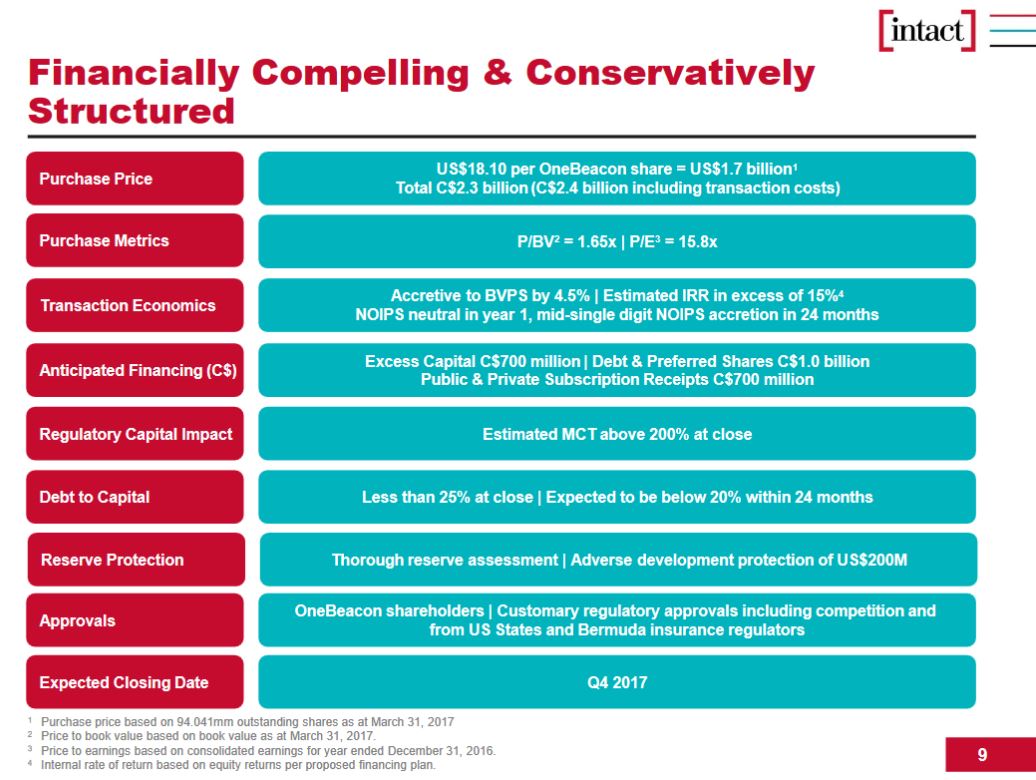

The purchase price of $1.7B or $18.10/share represents a Price to Book Value ratio of 1.66x and 15.8x earnings based on OB’s most recent financial statements. The total purchase price, including costs, will amount to roughly $2.4B. In addition OB’s existing debt (~$0.274B) will remain outstanding.

Financing is to be consistent with what has been telegraphed to investors and is also taking into consideration the needs of regulators and ratings agencies.

Approximately CDN $0.7B of excess capital will be used and IFC’s MCT is still expected to remain above 200% at close.

A combination of debt and preferred shares up to CDN $1B will be issued with a goal of maintaining debt to capital below 25% at closing. The cashflow from the combined businesses will be used to reduce leverage below IFC’s target 20% level before the end of 2019.

The acquisition is expected to be neutral to Net Operating Income per share in year 1 and should generate mid-single digit accretion within 24 months. The Internal Rate of Return will be in excess of 15% due to multiple top and bottom line opportunities and is expected to immediately add 5% to book value per share.

IFC will be temporarily halting all purchases under its Normal-Course Issuer Bid (NCIB); NCIB is a Canadian term for a company repurchasing its own stock from the public in order to cancel it. In a NCIB, a company is allowed to repurchase 5 – 10% of its shares depending on how the transaction is conducted.

The remaining ~ CDN $0.7B will be financed by the issuance of subscription receipts of which CDN $0.34B has already been sold on a private placement basis; the remainder is currently in the process of being issued.

The subscription receipts are convertible into common shares at the close of the transaction which, subject to regulatory approvals, is expected to take place in Q4 2017.

Source: IFC May 2, 2017 OneBeacon Proposed Acquisition Presentation

Potential Risks

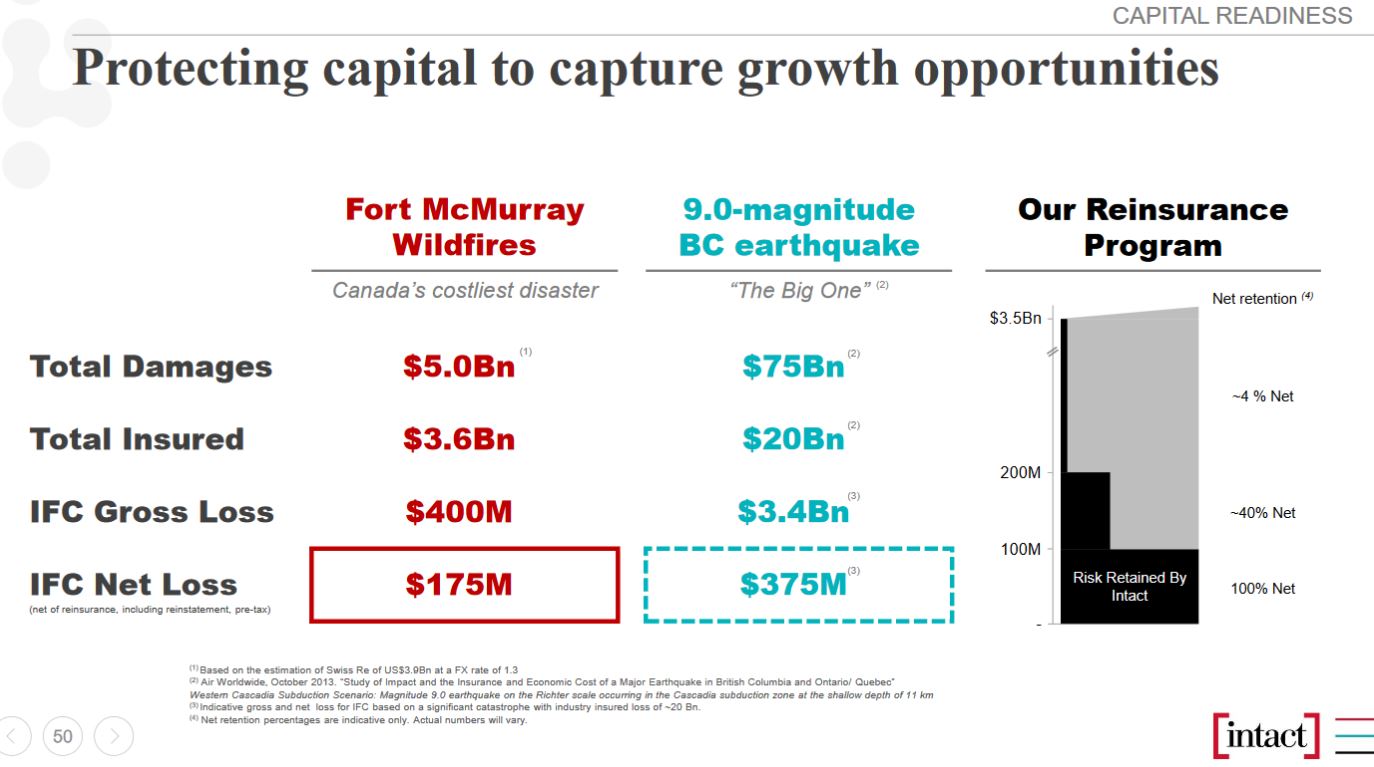

IFC is in the business of insuring risks and some of the risks it insures are becoming more catastrophic (eg. 2016 wildfire which southwest of Fort McMurray, Alberta which destroyed approximately 2,400 homes and buildings and which spread across approximately 590,000 hectares (1,500,000 acres) before it was declared to be under control on July 5, 2016). The very nature of expanding the business means IFC is taking on more risk. IFC, however, prudently offloads a significant proportion of this risk through the use of reinsurance.

Source: IFC February 15, 2017 Investor Day Presentation

OB is in the specialty insurance business. Typically, insurers in this space have a superior ability to evaluate the unique risks associated with non-standard business lines. The Specialty insurance business has higher barriers to entry than the standard property and casualty insurance business which results in fewer competitors and thus translates into the issuance of higher profit margin policies.

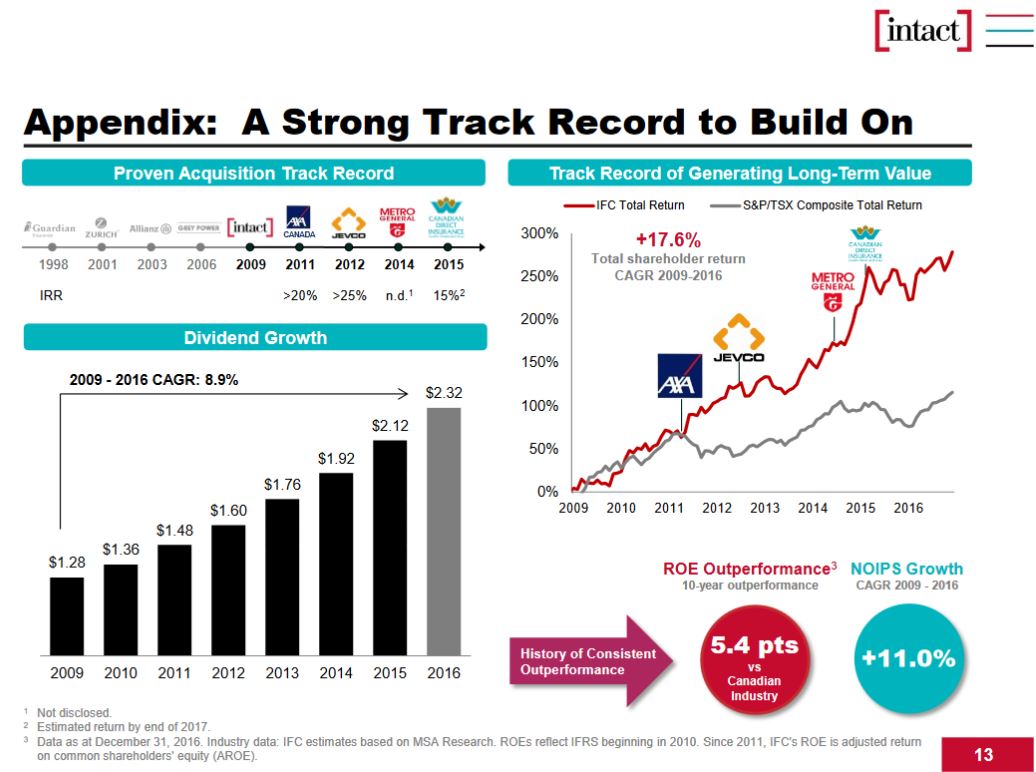

The road is littered with acquisitions that have not gone as planned. Occasionally, the acquirer finds the expected synergies between the existing and the acquired businesses are not as anticipated. In the case of the OB acquisition, IFC has conducted extensive due diligence and is of the view OB is a very strong specialty insurer with leading positions in the niche areas in which it operates. This is expected to complement IFC’s Specialty lines portfolio which it has developed over the years and which has volume in excess of CDN $0.6B at high profit margins. Furthermore, IFC has a track record of successful integrations; it has integrated 4 companies it has acquired subsequent to 2010.

Source: IFC May 2, 2017 OneBeacon Proposed Acquisition Presentation

Source: IFC February 15, 2017 Investor Day Presentation

IFC has developed a plan on how best to leverage the acquisition of OB to maximize growth in the US and in Canada. There will be opportunities for cross border business. In addition, IFC intends to use OB’s expertise and to bring some of its product offerings to Canada (eg. Technology, Entertainment, and Environmental Insurance). A similar opportunity exists where IFC believes its leading position in such lines as Contract Surety and Farm could be used to expand OB’s offering in the US.

IFC is acquiring a US company in USD thus exposing it to foreign exchange risk. This risk has been addressed in that IFC has hedged the USD purchase to avoid any change to its CDN equivalent between now and closing.

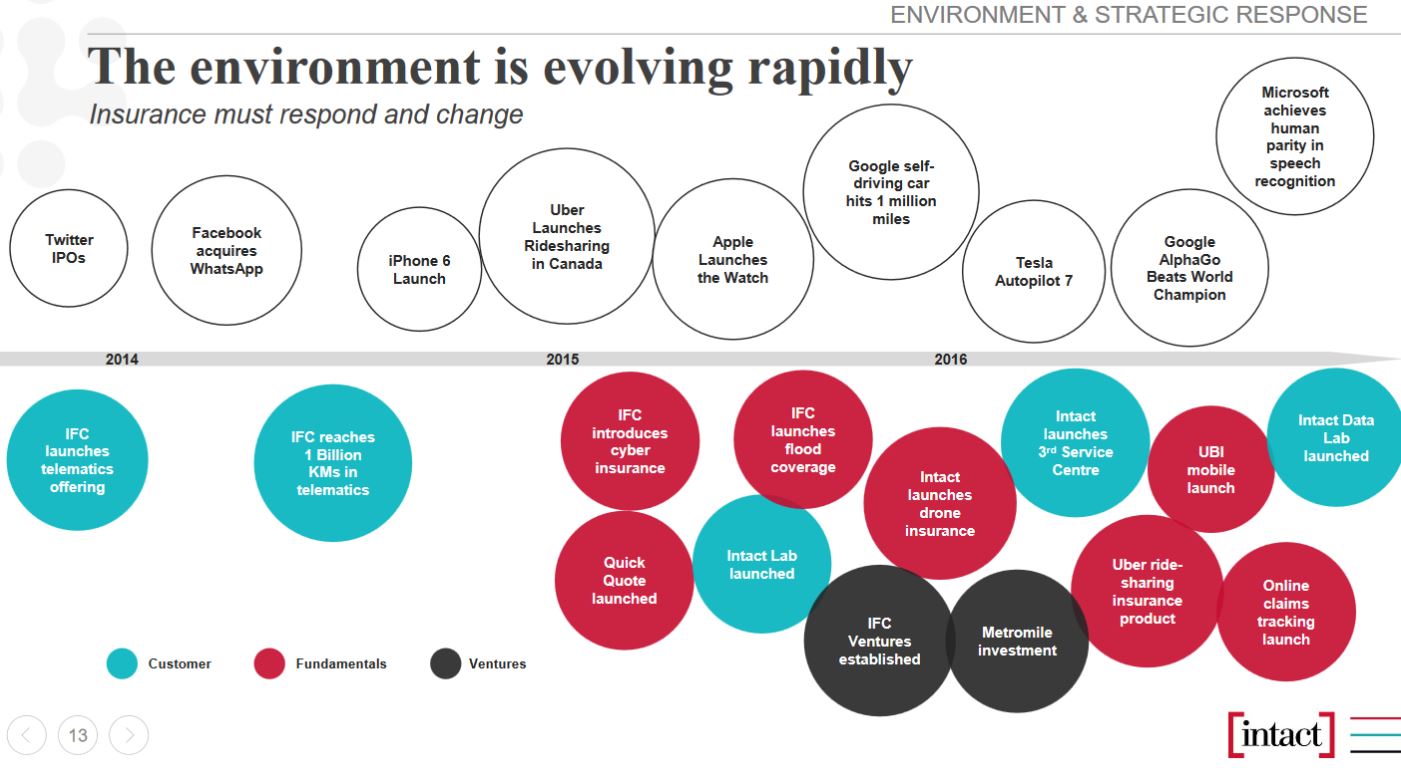

The environment in which IFC operates is evolving quickly. IFC must prudently deploy its resources in order to respond and change. Readers are encouraged to review IFC’s February 15, 2017 Leading Through Innovation Investor Day presentation.

Source: IFC February 15, 2017 Investor Day Presentation

Source: IFC February 15, 2017 Investor Day Presentation

The OB acquisition provides a scalable platform to grow organically in the US and in Specialty lines in Canada. In addition, it provides IFC with the opportunity to leverage its M&A track record to consolidate a fragmented market.

IFC has identified the expansion beyond existing markets as one of its 4 avenues for growth. If this acquisition does not go smoothly it will be extremely difficult for IFC to engage other US-based insurance companies in “friendly take-over” discussions. Given this, I am confident “all hands will be on deck” to ensure this integration goes smoothly.

The US insurance market is far more competitive than that in Canada. IFC is currently the leader in the Canadian market but it will only be a small player in the US. Having said this, I am certain IFC’s management is well aware of this risk hence the decision to make its foray into the US through the Specialty insurance market.

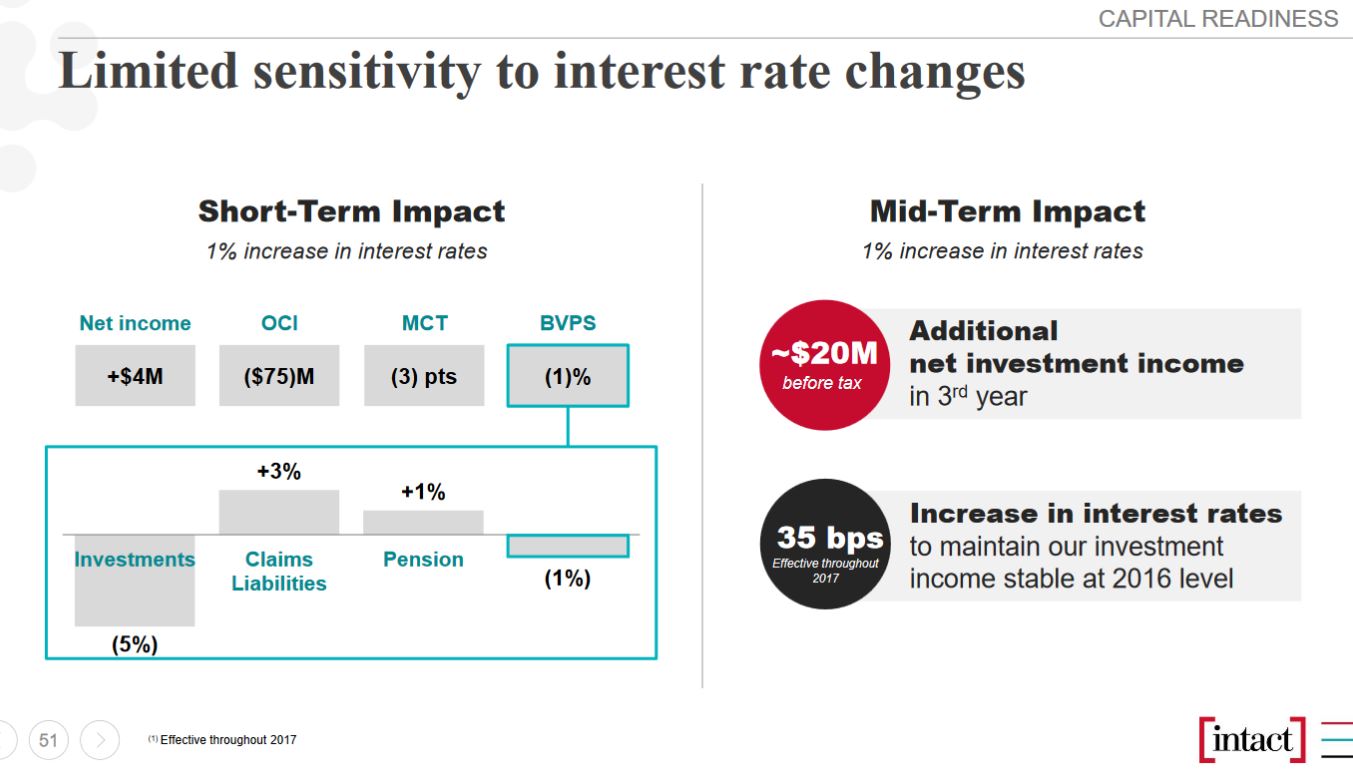

Pricing competition from hedge funds, as well as low interest rates, are squeezing margins at some property and casualty insurers.

The profitability of life insurance companies is negatively impacted by the low interest rate environment and volatile financial markets. IFC does not face this risk as borne out by the following page from its February 15, 2017 Investor Day presentation.

Source: IFC February 15, 2017 Investor Day Presentation

IFC has a prudent dividend policy. This helps make IFC’s stock more attractive to investors who suspect there is an element of irrational exuberance on the part of many investors and that a market correction of some magnitude will occur within the next 12 months.

Valuation

As I compose this post, IFC is trading at CDN $92.41 and has a 23.51 PE. IFC’s PE levels for the past several years have typically been sub-17.

Source: CFRA May 5, 2017 report generated from TD WebBroker

Management attributes the pressure on earnings to:

- personal auto results which were negatively impacted by higher weather related losses;

- the ongoing difficult economic conditions in Western Canada;

- the elevated Catastrophic (CAT) losses which contributed to the Combined Ratio of 98.2% in Q1 which was well above historical levels.

In fact, 3 of the last 4 quarters included unusually high levels of CAT losses yet IFC outperformed the industry by a margin of 580 bps in 2016 which is above its 500 bps target.

On the May 2, 2017 conference call in which Q1 results were reviewed, management indicated it was seeing positive momentum in specialty lines.

Given the above, I am of the opinion the current elevated PE is an anomaly. Were it not for the above noted pressures on earnings, IFC’s PE would be closer to historical levels.

It appears I am not alone with this opinion. Multiple analysts expect a mean EPS of CDN $6.21 and CDN $7.32 for 2017 and 2018 respectively.

Source: TD WebBroker

If we use the current market price and the mean EPS of CDN $6.21, we get a forward PE of 14.88. This level is more in line with what I would expect from a P&C insurance company.

Let’s look at IFC from a dividend yield perspective. The quarterly and annual dividend is CDN $0.64/$2.56, respectively. Using the current market price of CDN $92.41 we get a dividend yield of 2.77%. While definitely not a level to “write home about”, I would much rather receive a sustainable dividend. I have no desire to receive a dividend from a company whose dividend yield is in the stratosphere since this suggests to me that:

- a dividend cut is imminent or

- the dividend is composed of a return on equity AND a return of equity.

Intact Financial Stock Analysis – Final Thoughts

In my opinion, IFC’s foray into the US market through its acquisition of OB is a precursor of additional US acquisitions which will likely occur after it digests OB and restores its debt to capital and MCT ratios to target levels; this is unlikely to occur prior to the completion of FY2019.

I suspect that if IFC continues with its growth plans in the US, IFC will likely list on a US exchange. My rationale for this train of thought is reinforced in the fact that OB is already a publicly traded entity on the NYSE and the soon to be combined entity will be much larger than the currently publicly traded OB.

If IFC were to eventually list on a US exchange, I suspect there would be a much larger pool of investors interested in adding IFC to their portfolio. This could potentially result in an upward movement in IFC’s stock price.

IFC currently appears overpriced at this juncture given the PE which exceeds 23. As noted in the Valuation section of this post, I think this PE level is distorted by temporarily depressed earnings .

I view IFC as fairly valued and intend to acquire additional IFC shares within the next 72 hours with the view of holding them long-term.

Note: I appreciate the time you took to read this article and hope you got something out of it. As always, please leave any feedback and questions you may have.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence, and consulting your financial advisor about your specific situation.

Disclosure: I am long IFC.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.