Summary

Summary

- UTX released Q3 results on October 23 and provided an upward revision to its adjusted EPS for FY2018.

- The Rockwell Collins acquisition has received approval from the EU Commission and from the U.S. Department of Justice.

- The deal is currently under review in China and the acquisition is expected to close in 2 – 6 weeks.

- UTX’s board continues to evaluate strategic options for the company’s future and a decision is expected before the end of 2018.

Introduction

Judging from the way stock prices have been behaving recently I suspect there are many nervous investors. Here are a few factors causing investor angst:

- U.S. – China trade tensions;

- Brexit;

- Major financial challenges in Italy;

- Worry about how higher interest rates could impact the US economy (the Federal Reserve has indicated a move to tighten up monetary policy by year’s end);

- Uncertainty surrounding US mid-term elections.

Frankly, I have had my concerns for quite some time about what I have perceived to be lofty valuations. In many cases, the outcome of several of my analyses has been to ‘pass’ and to patiently sit on the sidelines. A few of my calls have proven to be incorrect and I have watched the stock prices of some companies in which I have opted to ‘pass’ continue to rise in value.

Recently, however, I am pleased to see that several companies I perceived to be overvalued have been pulling back. Rather than fear a market pullback my outlook on market pullbacks is much like that of Buffett/Munger wherein they recommend investors be ‘fearful when others are greedy and greedy when others are fearful’.

This brings us to the subject of this article….United Technologies (NYSE: UTX). When I wrote my January 30th UTX article the stock was trading at ~$138. Based on my analysis I indicated that I would patiently wait for a pullback to a price of $130 or below. UTX’s share price dropped below $130 in mid-March and drifted to as low as ~$115 (early May) but other investment opportunities arose and I did not add to my existing UTX position.

In mid-September, UTX’s share price rose to the ~$142 level. It has, however, has since pulled back to ~$128 (as I compose this article).

Given…

- UTX’s reasonable valuation after this pullback;

- my anticipation of some decent Q3 results (released October 23rd);

- my positive long-term outlook on the company;

…I acquired another 300 shares @ ~$126 on October 22nd; these shares are held in one of the ‘side accounts’ of the FFJ Portfolio. For the sake of full disclosure I also own shares in undisclosed accounts which were acquired mid-April 2008.

The following are my thoughts as to why I decided to acquire additional UTX shares.

Overview

In my January 30th UTX article I indicated that UTX’s offer to acquire Rockwell Collins (NYSE: COL) had been overwhelmingly approved by COL shareholders. The rationale for this acquisition was to enable UTX to broaden its aerospace portfolio which is currently highly dependent on the geared turbofan engine.

In May 2018 the acquisition was approved by the EU Commission subject to conditions that included both companies divesting of certain operations. In order to mitigate regulators’ concerns about reduced competition in the production of trimmable horizontal stabilizer actuators, certain pilot controls, pneumatic ice-wing protection and oxygen systems, both COL and UTX agreed to divest themselves of certain activities. COL had offered to divest its entire trimmable horizontal stabilizer actuator production and pilot-control business and its global business in ice protection while UTX had offered to divest two research projects in oxygen systems.

On October 2nd, the U.S. Department of Justice approved the sale of COL to UTX. This approval was granted on the condition that COL’s pneumatic ice protection systems business and its trimmable horizontal stabilizer actuator business be divested; COL already has a signed agreement to sell its actuators, pilot controls, and special products business to Safran, a French aerospace company. The sale is expected to finalize in the first half of 2019.

UTX’s management still requires necessary approvals from Chinese authorities but they are cautiously optimistic this approval will be received shortly.

While the closing of this transaction has taken longer than originally anticipated, work has been ongoing regarding the combining of the two entities. Based on the work done to date, UTX is confident that following the acquisition, UTX’s $30B business is likely to swell to $50B by ~2020. Furthermore, the UTX and COL teams have already identified $50 million in cost synergies.

In addition to the work going on regarding the merger of both companies, UTX’s board has continued to evaluate strategic options for the company’s future. Originally the thought was that UTX would begin to evaluate options once the COL deal had closed. UTX’s CEO, however, has indicated that UTX has not been waiting for the COL deal to close and that analysis has been ongoing for roughly the past year regarding a potential split up of UTX. Further details on this front are tentatively expected to be released before the end of 2018.

In my opinion, I envision that UTX will come to the decision that one or two segments of the company is/are to be spun off into totally independent publicly listed entity(ies), or sold, following the completion of the evaluation of strategic options for the company’s future. Proceeds would then likely be deployed toward the enhancement of the competitive position of the segments UTX has deemed to be core versus the repayment of debt.

Q3 2018 Update

On October 23rd, UTX released its Q3 results.

While profits dropped ~7% as higher costs offset a 10% jump in revenue, organic sales rose ~8% from a year ago (excludes acquisitions).

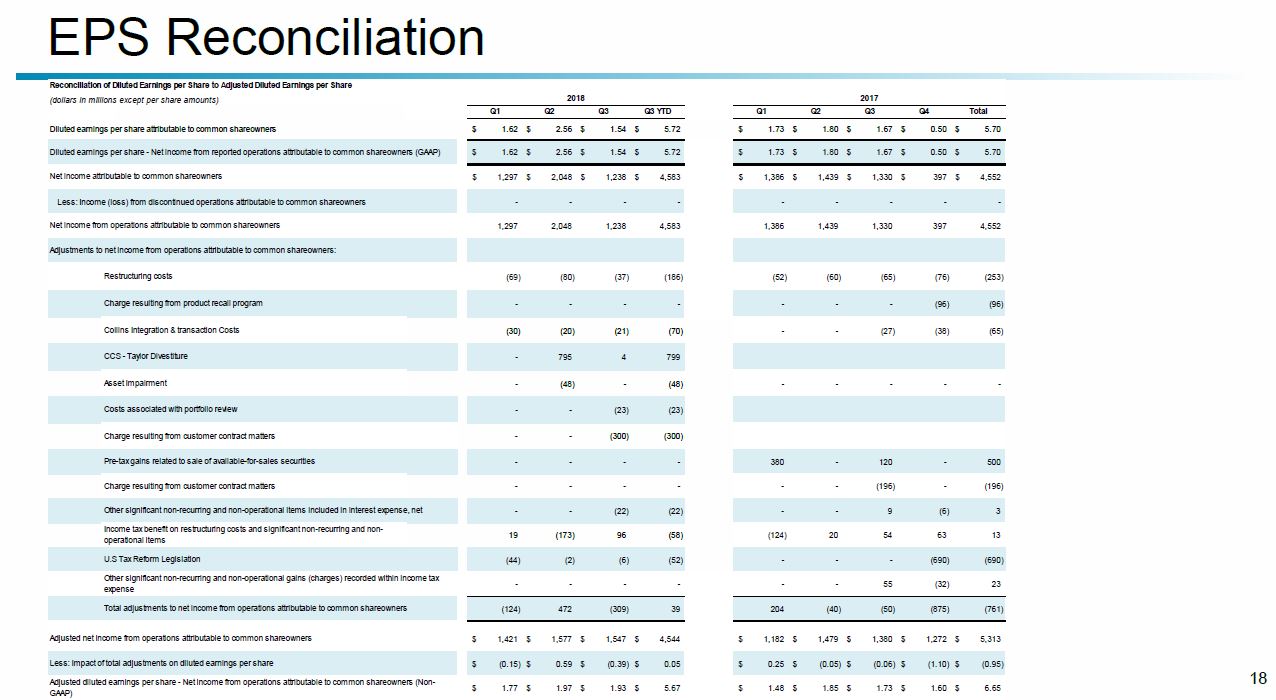

The following image reflects various adjustments UTX has made to its EPS. The use and definitions of Non-GAAP Financial Measures can be found in its Q3 Press Release.

UTX – Q3 2018 Earnings Presentation – October 23 2018

2018 Outlook

UTX’s outlook for the full year is as follows:

UTX – Q3 2018 Earnings Presentation – October 23 2018

The all important Free Cash Flow forecast of $4.5B – $5B is in line with historical levels.

On the Q3 conference call UTX’s CEO indicated that he does not see any drama in the deal’s review in China and that he expects the Rockwell Collins deal to close in 2 – 6 weeks.

Credit Ratings

Moody’s downgraded UTX’s long-term debt one notch from A3 to Baa1 in August 2018. This rating is the upper tier of the lower medium grade category and is investor grade.

S&P Global rates UTX’s long-term debt A-. This rating is the lower tier of the upper medium grade category and is investor grade.

Valuation

Using the YTD EPS of $5.72, adjusted EPS of $5.67, and the revised adjusted EPS range of $7.20 – $7.30 I anticipate that UTX’s full year EPS will be reasonably close to $7.25. As I compose this article, UTX is trading at ~$128 which gives us a forward PE of ~17.66. This compares favorably with UTX’s 5 year average PE of ~18.5.

Historical Performance

UTX is a $100B+ market cap ‘Industrial’ company; it pales in market value when compared with Apple, Microsoft, Facebook, Alphabet, Amazon, and Visa which all fall within the top 25 companies of the S&P500 from a weighting perspective. I am not, therefore, surprised to see that UTX has underperformed the S&P 500 over a 5 and 10 year period given how well these much larger companies have performed in recent years.

Source: Tickertech

I have not, however, invested in UTX on the basis of how it has performed in recent years but rather on the basis of how I think it will perform in the future. I am optimistic on UTX’s future.

Dividend, Dividend Yield, Dividend Payout Ratio

UTX’s dividend history can be found here and its stock split history can be found here.

At the time of my January 30th article, UTX was trading at ~$138 and the annual $2.72 dividend provided investors with a ~1.97% dividend yield. With UTX currently trading at ~$128 and the annual dividend now $2.835, UTX’s dividend yield is ~2.21%; this excludes any withholding tax considerations that impact non-US citizens who hold these shares in non-tax advantaged accounts.

Some investors will likely opt to pass on a UTX investment given the drop off in the CAGR of UTX’s dividend in recent years and the relatively low dividend yield. In my opinion, this might be somewhat short-sighted but I recognize that my long-term goals and objectives may differ from that of other investors.

The $2.835 annual dividend is a ~39% payout ratio if we use UTX’s estimated full year EPS of $7.25. This is in line with historical levels and I view the dividend as safe given the low payout ratio.

Final Thoughts

I recognize the COL acquisition still requires approval from Chinese authorities but I anticipate they will approve the transaction; I view this acquisition as a huge positive for UTX.

I further envision that UTX’s Board will come to the conclusion that 1 or 2 segments of the company should be spun-off or sold. Proceeds would then likely be deployed toward the enhancement of UTX’s competitive position in the segments it retains as opposed to debt repayment.

Based on the recent pullback in UTX’s stock price and the projected earnings I anticipate for FY2018 I acquired additional UTX shares on October 22. These shares are being held in ‘side accounts’ within the FFJ Portfolio.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long UTX.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.