![]()

Summary

- PG has struggled in recent years with sales having dropped from $82B in 2012 to $65B in 2017.

- PG has recently signed an agreement to acquire the Consumer Health business of Merck KGaA, for ~$4.1B which will add ~$1B in annual revenue.

- Strong cash flow has enabled PG to shower investors with dividends and to be able to significantly reduce share count.

- While the ~4% dividend yield is enticing I would prefer to invest in a company that is in growth mode as opposed to a ‘turnaround story’.

- I present an option strategy if you are adamant that PG is a company in which you wish to invest but you would like to see the effectiveness of the turnaround strategy.

Introduction

A subscriber recently asked me for my opinion on the Consumer Goods space with specific reference made to The Procter & Gamble Company (NYSE: PG). I have never owned PG nor have I ever reviewed it but given its ~$20/share pullback subsequent to the beginning of December 2017, this seems as good a time as any to analyze PG.

Business Overview

Most readers are undoubtedly familiar with PG to some extent in that this branded consumer packaged goods company was founded in 1837 and now sells products in more than 180 countries and territories.

PG has five reportable segments: Beauty; Grooming; Health Care; Fabric & Home Care; and Baby, Feminine & Family Care. In FY2017, grooming and baby care accounted for ~1/3 of total sales. Sales in the Beauty segment accounted for ~1/5 of sales and Fabric Care accounted for ~1/3 of sales.

Source: PG – CAGNY February 22 2018 Presentation – page 15

Its customers include mass merchandisers, grocery stores, membership club stores, drug stores, department stores, distributors, wholesalers, baby stores, specialty beauty stores, e-commerce, high-frequency stores, and pharmacies. Sales to Wal-Mart Stores, Inc. and its affiliates represent approximately 16%, 15%, and 15% of PG’s total FY2017, FY2016, and FY2015 sales. No other customer represents more than 10% of total sales and its top 10 ten customers accounted for ~35% of total sales in 2017, 2016, and 2015.

PG has suffered from lagging sales as competition from local peers, as opposed to global branded players, in emerging markets has intensified.

In PG’s FY2017 10-K it specifically states:

‘The markets in which our products are sold are highly competitive. Our products compete against similar products of many large and small companies, including well-known global competitors. In many of the markets and industry segments in which we sell our products we compete against other branded products as well as retailers’ private-label brands.’

In an effort to adapt to the changing global environment, PG has made a concerted effort to refocus the business by way of shedding brands. This multiyear effort has resulted in the reduction from 170 brands/16 categories to the current 65 brands/10 categories. Of the remaining brands, 21 generate ~$1B – ~$10B in annual sales and another 11 generate ~$0.5B – ~$1B in annual sales. As a result, PG’s top line has shrunk from FY2008 annual revenue of $81.8B to FY2017 annual revenue of $65B.

Recent Events

PG’s challenges at maintaining market share and in executing its turnaround strategy has certainly irked investors. In fact, shareholders recently voted against management’s recommendation and activist investor Nelson Peltz was added to PG’s Board late 2017.

In an effort to renew its focus on growth, PG recently made the following announcements that it:

- intends to terminate its PGT Healthcare Partnership with Teva which was formed in November 2011;

- has signed an agreement to acquire the Consumer Health business of Merck KGaA for a purchase price of ~$4.1B.

This acquisition, expected to close within the next 18 months, should replace the scale and technological know-how lost following the dissolution of its joint venture with Teva. It will bring consumer health brands into its portfolio which generate ~$1B in annual revenue that is growing in the mid-single digits in large part due to popular over-the-counter franchises like Neurobion, Nasivin, and Bion3.

Q3 and YTD 2018 Results

PG’s Q3 and YTD 2018 results reported April 19, 2018 can be found here.

Source: PG Q3 2018 Earnings Release – April 19, 2018

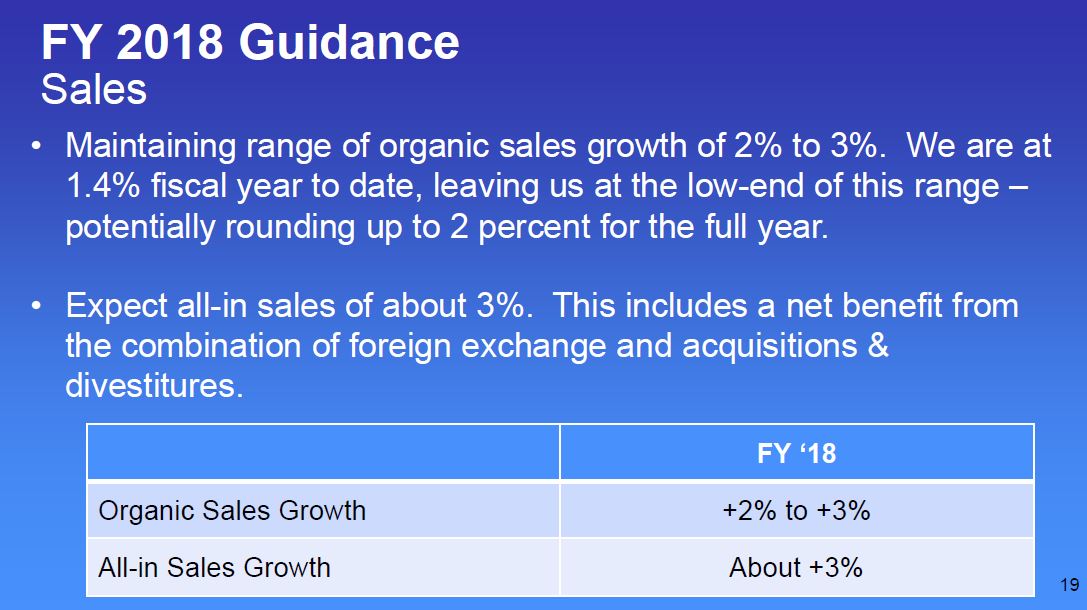

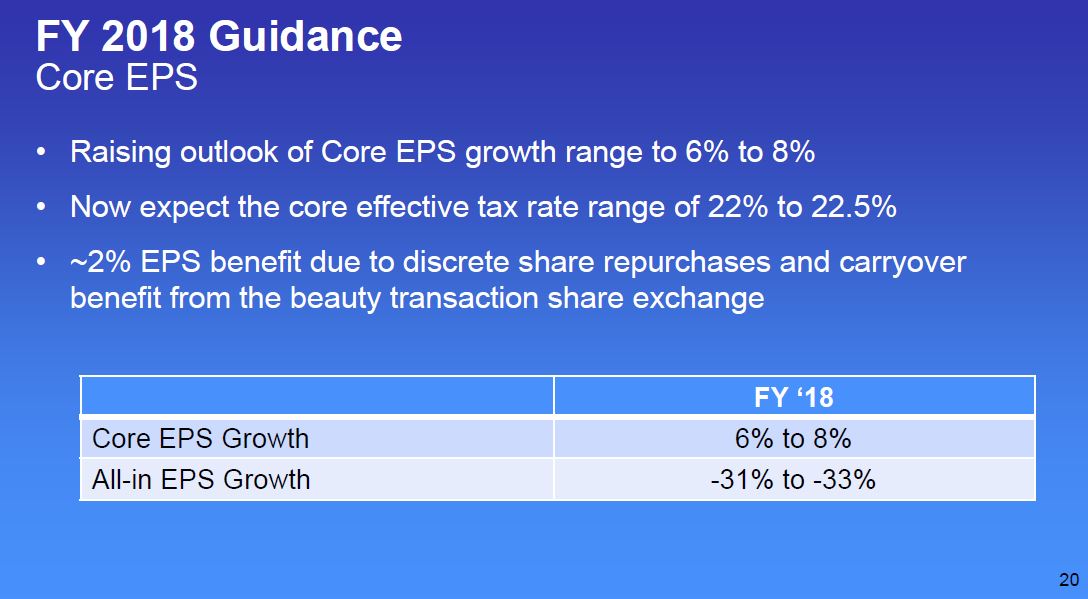

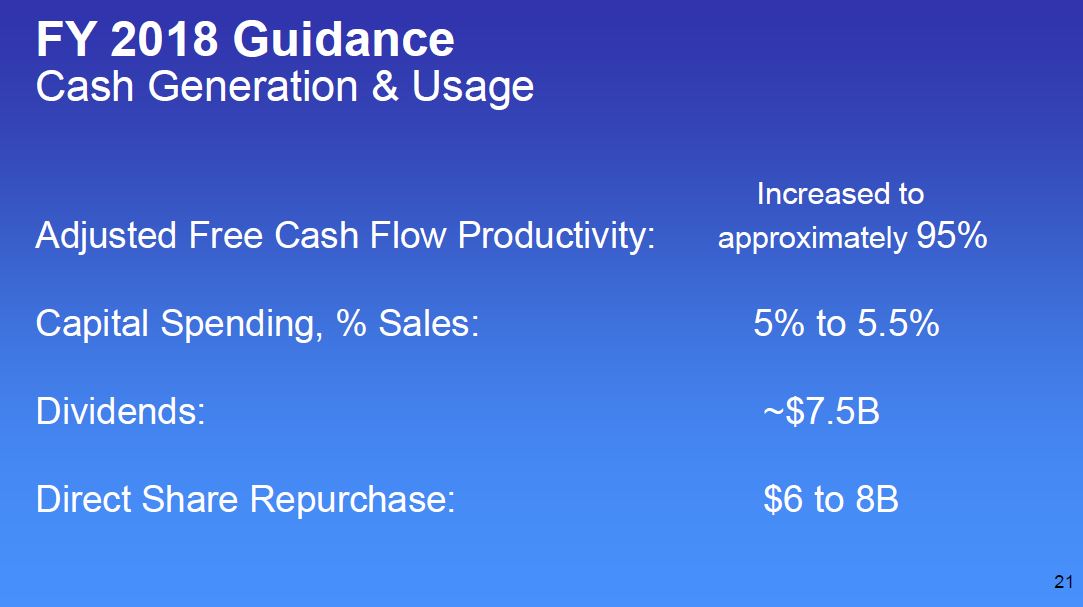

2018 Guidance

In its Q3 2018 earnings presentation, PG provided the following guidance for FY2018.

In FY2017, PG reported Core EPS (a measure of PG’s diluted net EPS from continuing operations) of $3.69. A 6% – 8% increase in Core EPS for FY2018 (increased from the prior 5% – 8% range) would suggest we can expect PG to generate ~$3.9 – ~$4 in EPS.

Cash flow conversion has also been revised upward to 95% from the previous 90% goal.

Long-Term Debt

PG has definitely taken advantage of the low interest rate environment over the past several years as evidenced by Note 10 in PG’s FY2017 10-K (page 65 of 213). PG reported a long-term weighted average interest rate of 2.6% versus 3.3% in FY2012 and FY2013 (page 49 of 146 in FY2013’s 10-K). This certainly makes a difference when you have ~$18B – $19B in long-term debt.

Credit Ratings

Moody’s has rated PG’s long-term debt Aa3 since October 2001 when it downgraded the company 2 notches. S&P Global has rated PG’s long-term debt AA- since November 2001. Both ratings are at the low end of the High Grade scale. Both ratings agencies have a stable outlook on PG.

Valuation

Based on PG’s FY2018 GAAP EPS projection of ~$3.9 – ~$4 and a current share price of $71.33, I arrive at a forward PE of ~18 which is below its 5 year average of ~23.

Dividend, Dividend Yield, Dividend Payout Ratio, and Share Repurchases

In its April 19th Q3 2018 earnings release, PG indicated it had returned $3.2B of cash to shareholders through $1.8B of dividend payments and $1.4B of common stock repurchase.

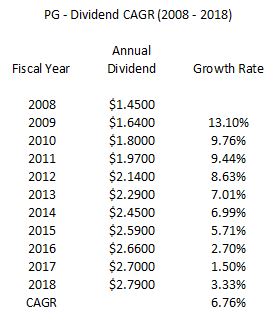

In addition, in April 2018, PG announced a 4% increase in its quarterly dividend. This increase marks the 62nd consecutive year in which PG has increased its dividend. Furthermore, PG has paid a dividend for 128 consecutive years since its incorporation in 1890.

PG also continues to generate strong free cash flow (FCF) with $9.4B FCF in FY2017 being on the low side of annual FCF generated over the last 10 years

PG’s dividend history can be found here. The compound annual growth rate over 2008 – 2018 has been calculated on the basis of PG’s fiscal year. We can see that the annual growth rate of PG’s annual dividend has certainly tailed off in recent years.

The forward dividend yield is ~4% based on the May 3, 2018 closing stock price of $71.33.

In FY2017, PG reported $3.69 in diluted EPS from continuing operations and $1.90 in diluted EPS from discontinued operations for a total of $5.59. PG’s quarterly dividend of $2.70 in FY2017 represented a dividend payout ratio of ~48% of total EPS but ~73% of EPS from continuing operations.

On the basis of the FY2018 GAAP EPS projection of ~$3.9 – ~$4, the current ~$2.87 ($0.7172/quarter) annual dividend represents a dividend payout ratio of ~72.3%. While this is a high level, PG continues to be a cash generating machine. It can certainly service the dividend and also repurchase a significant number of shares (share count has been reduced from 3,317 million in FY2008 to 2,740 million in FY2017.

Option Strategy

PG has certainly encountered its share of challenges in recent years but management is making a concerted effort to restore PG to better times. If you have confidence PG will see better days, you could acquire shares and be rewarded with a ~4% dividend yield.

An alternative to acquiring the shares outright would be to enter into an option strategy. I present the following option strategy for your consideration.

Write a June 21, 2019 PUT with a $65.00 strike price for which you would receive ~$2.91 (at the time of writing) for each contract; each contract equals 100 shares. If you write 4 contracts, you would need to set aside $26,000 in your brokerage account or you would need to have sufficient margin available. This is required in the event the option gets exercised and you find yourself having to make good on the purchase of 400 PG shares.

If PG does not drop below $65.00, the option will expire worthless as nobody on the other side of the contract would be prepared to sell their shares for $65.00 if they are trading for a higher value. You would pocket the $1,164 in premium from the 4 contracts (excludes commission) but you would not own any PG shares.

If PG were to drop below $65.00 and the options were exercised, you would acquire 400 shares at $65.00 ($26,000). Keep in mind that you already collected a $1.164 premium so your net cost would be $24,836 or $62.09/share (excludes commission).

Suppose PG were to plunge to $50/share. You probably would not want the 400 shares to be PUT to you at $65.00 so you need to know how/what to do if you do not want to be obligated to purchase the PG shares.

I recognize option strategies are not for everyone and I am presenting this strategy without knowing your investor profile.

Final Thoughts

Despite PG’s challenges, it continues to generate strong free cash flow which it showers upon investors in the form of dividends and share repurchases. Since it generates substantial free cash flow, I am of the opinion PG’s ongoing ability to service its dividend and to repurchase outstanding shares is not at risk.

The 4% dividend yield and the significant number of shares being repurchased make PG an alluring investment. My concern with PG, however, is that cost cutting can only go so far. At some stage, a company needs to grow. PG is a company in transition and there are no assurances that the steps taken to date will reverse the negative trend in revenue.

What I see in PG is a company that faces intense competition. I think this competition will intensify as time progresses and PG’s management will likely be forced to make further tough decisions.

I would prefer to invest in a business which is experiencing growth and am not looking to invest in a potential ‘turnaround story’.

I will pass on investing in PG and will continue to seek opportune investments in companies which are in growth mode.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this post. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I do not currently hold a position in PG and do not intend to initiate a position within the next 72 hours.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.