Summary

Summary

- This PepsiCo stock analysis is based on Q4 and FY2016 financial results and its outlook for 2017 which were released on February 15, 2016.

- Organic revenue, which excludes the impact of various items, grew 3.7%.

- 2017 core earnings of $5.09/share expected compared to $4.85/share in 2016.

- 2016 Free Cash Flow (FCF) of $7.786B with approximately $10B in cash flow from operating activities and $7B FCF projected for 2017.

- PEP announced an increase in its quarterly dividend ($0.7525 increased to $0.805) effective with the June 2017 dividend.

Introduction

PepsiCo, Inc. (NYSE: PEP) released its Q4 2016 and FY2016 results on February 15, 2017 and also provided guidance on 2017. Given the release of its results and the fact our initial PEP purchase was made February 18, 2009, I thought it would be fitting that I would review PEP and provide my opinion on whether I deem it to be a wise investment for investors who have a long-term investment perspective.

Using PEP’s Investment Calculator I see that our initial investment ($50.80/share) has appreciated in value by 107.49%. The reinvestment of the quarterly PEP dividends is on auto-pilot and we have subsequently acquired additional PEP shares, albeit not at similarly attractive valuations, but the market value of our PEP holdings is still up roughly 75% from our average cost.

The PEP shares we own are held in a Spousal Registered Retirement Savings Plan (RRSP), which for non-Canadian readers, is a retirement account established for my wife and in which I make the contributions and receive the tax benefits. When she makes withdrawals from this account, they are taxed in her name unless withdrawals are made within a certain number of years after the last contribution. Here is a link to Canada Revenue Agency’s website which explains the tax implications of spousal RRSP withdrawals.

At the time of our initial PEP purchase, PEP’s quarterly dividend was $0.425/share. Where do we stand now? Well, the dividend payable March 31, 2017 will be $0.7525 and on February 15, 2017, PEP announced a 7% increase in its annualized dividend to $3.22/share from $3.01/share with the increase to occur with the dividend payable in June 2017.

Clearly, we are extremely pleased with our PEP investment.

Should Pepsi Spin-Off Its Food Business?

Periodically I hear rumblings of activist investors who want PEP to spin-off its food business from its beverage business.

After having been in various sales and sales management roles in Commercial and Corporate Cash Management at a couple of major Canadian banks, I can’t tell you how many opportunities can come your way, or that you can feed to internal partners, when you have multiple “touch points” with a client. Not only that but people move within an organization. I am certain there have been instances where decision makers have moved from PEP’s beverage business to their snack business or vice versa. Just think of how much this can be to PEP’s advantage versus its major competitors which do not have both business lines.

I have noticed that within the past couple of years, PEP’s drinks have displaced Coke in the Subway restaurants in Canada. Unless my memory fails me, I am certain I was purchasing Doritos at Subway several years ago. I would venture to guess that PEP’s extensive face time with Subway’s decision makers on the snacks front helped it land the drinks side of Subway’s business.

Do I know if the drinks side or the snacks side of the Subway business is profitable? No, but common sense would lead me to believe that the PEP/Subway relationship is mutually beneficial.

Pepsi’s Food and Beverage Products

Let’s not kid ourselves. PEP does not spring to mind when I think of healthy products and I am reasonably confident most of you are on the same page as me.

Having said this, I am of the opinion that PEP is doing the right things to improve its image; refer to page 7 of PEP’s 2015 Annual Report. I also sincerely applaud PEP’s trend in making its food products healthier and in its acquisition of additional beverage brands.

As a concerned parent, I also want to know that companies are making efforts to improve the quality of life for the current generation and future generations. In this regard, you may wish to look at page 4 of PEP’s 2015 Annual Report to see how PEP is performing. I recognize PEP can still make further improvements but it is comforting to know that it is a socially responsible company.

Q4 and FY2016 Financial Results

Highlights of PEP’s results can be found in its February 15, 2017 Earnings release and in the Reconciliation of GAAP and Non-GAAP Information (unaudited) document.

This section is going to be relatively brief in that you can easily skim through PEP’s documents to which I have provided links.

I will, however, take a moment to highlight PEP’s strong FCF evidenced over the years.

When I look at the 2015 and 2016 Reconciliation of GAAP and Non-GAAP Information I see the following:

Source: Morningstar – PEP Net Cash Provided by Operating Activities and FCF 2013 – 2016

Some of you will likely take the time to dissect the financials to ascertain the reason for the variances. I understand. Some of you might follow the Russian proverb “Trust, but verify.” to a T. I know my personality, however, and will trust the team of high priced PEP Executives and the team from KPMG LLP (PEP’s Auditors) are reasonably confident that the numbers they have reported are accurate. Furthermore, when I see FCF numbers of this magnitude, I don’t question the reason for the relatively insignificant variances.

Outlook for Fiscal 2017

PEP’s 8-K released February 15, 2017 reflects the following outlook for FY2017:

- organic revenue growth of at least 3% with FX translation expected to negatively impact reported net revenue growth by approximately 3% and the 53rd week in 2016 expected to negatively impact reported net revenue growth by 1%.

- $5.09 EPS in core earnings expected in FY2017 which is driven by the following expectations and factors:

Source: PEP’s February 15, 2017 8-K

Approximately:

- $10B and $7B projected cash flow from operating activities and FCF (excluding certain items), respectively.

- $3B in net capital spending.

As previously noted, PEP has announced a 7% increase in its annualized dividend ($3.01 increased to $3.22) effective with the June 2017 dividend.

Total dividends to shareholders will be approximately $4.5B in 2017 and PEP anticipates it will repurchase approximately $2B in shares. It won’t be buying our shares!

Valuation

As I compose this, PEP’s shares are trading at $106.86.

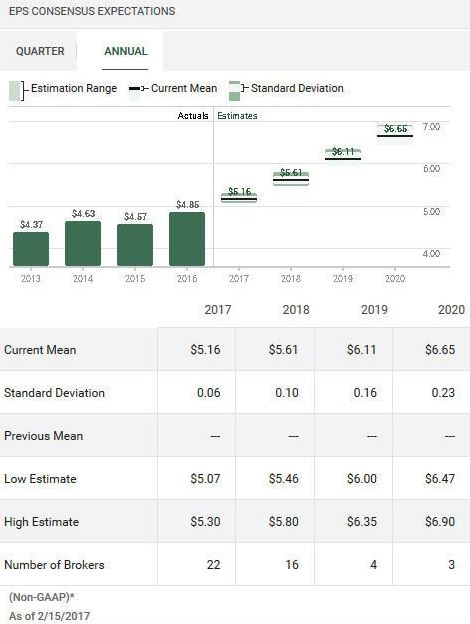

The projected Mean EPS for FY2017 from 22 brokers is $5.16. PEP’s earnings announcement today, however, calls for $5.09 EPS in core earnings in FY2017.

Source: TD WebBroker PEP Projected Quarterly 2017 EPS

Source: TD WebBroker PEP Projected Annual EPS

Source: ValuEngine PEP Projected Quarterly 2017 EPS

Source: ValueEngine PEP Projected Annual EPS

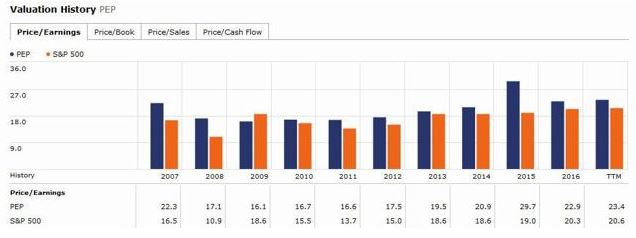

Using PEP’s figure of $5.09 and the current price of $106.86, we’re looking at a forward PE of 21. While this ratio is higher than I would like to pay, PEP doesn’t go on sale that often and the current level seems reasonable to me; I just lucked out when we acquired our first few hundred shares in February 2009.

Source: Morningstar – PEP and S&P500 2007 – 2016 PE

I also plan on holding these shares for a very long time. We have structured our estate so that our investments will be around long after we depart this planet (hopefully many years from now) to continually generate a nice stream of dividend income. I am reasonably confident the next generations won’t be wondering why we paid X versus 0.8X when we periodically acquired our PEP shares. In all likelihood they will be wondering why we didn’t buy more.

In a recent post entitled I Am Concerned About The Recent Rapid Increase in Stock Valuations I gave several examples of companies we hold in various investment accounts which have experienced meteoric increases in price between December 31, 2015 and February 13, 2017. Fortunately, PEP having experienced only an 8.03% appreciation in stock price during this period, is not one of the stocks where the price has become totally disconnected with the underlying business.

Some investors get fixated on the dividend yield and unless a company has a dividend yield north of 5% (for example), the company is eliminated as an investment possibility. In my opinion, that’s a real shame but to each their own.

As I compose this, PEP’s dividend yield is about 2.8% which is based on an annual dividend of $3.01. We know that PEP has announced an increase in its annual dividend to $3.22 (I fully expect them to make good on this) so using the current stock price of $106.86 we get a dividend yield of 3%. This dividend yield from a company of PEP’s quality is acceptable from my perspective. Furthermore, if you look at PEP’s historical dividend growth, it is outpacing the rate of inflation. I am also confident that PEP will continue to have the wherewithal to meet its dividend obligations. This all looks good to me.

Option Strategy

I don’t see why you would not want to acquire PEP shares at current levels but perhaps you are concerned that the market is overdue for a correction. I know how you feel. I feel the same way.

If you do not own PEP shares and wish to establish a position, perhaps you could acquire shares over time until your PEP holding reaches a level where it constitutes a reasonable level within your portfolio.

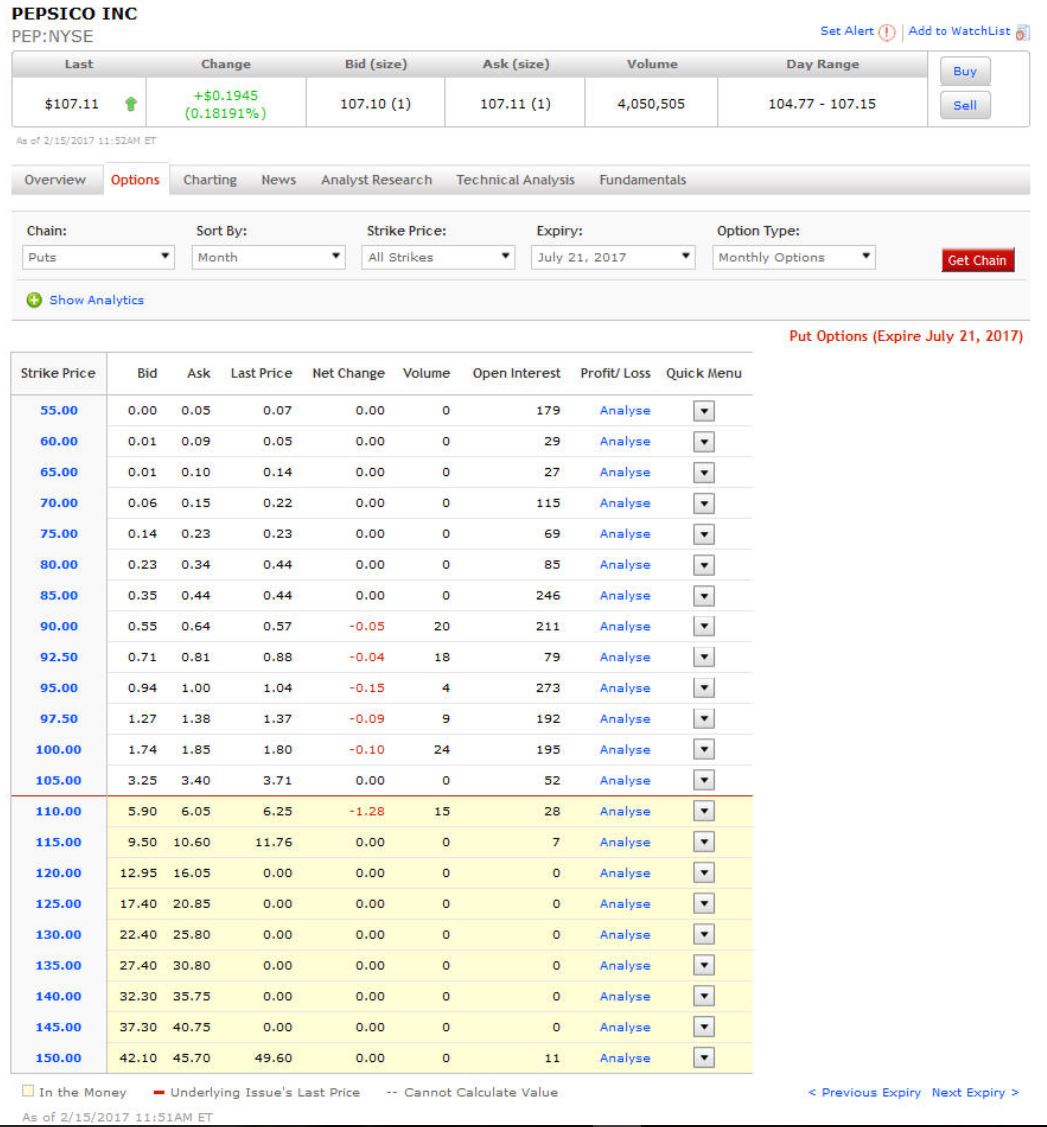

Another alternative would be to write a July 21, 2017 PUT with a $100 strike price. Each contract represents 100 shares so looking at the chart below you would likely receive around $1.80/share or $180/contract. While I anticipate a market correction, I certainly am unable to forecast one with any degree of accuracy and this is why I am not recommending a $97.50 strike price since I don’t think PEP will drop to that level by expiry date. If you just want to collect option premiums and owning PEP shares is a secondary benefit from your perspective then perhaps a $97.50 strike price would tickle your fancy. NOTE: Be aware that your money will be tied up while the contract is open.

Source: Scotiabank CSCO PUT July 2017 Option Chain

Personally, I am not writing any options at this stage since I perceive volatility to be very low which impacts option values. I don’t mean to be flippant but writing a few contracts to make a few extra hundred dollars is not worth my time. In addition, I plan to take some vacation time and want to go off the radar for a bit. I don’t want to be forced to always be checking to see the status of my option contracts.

PepsiCo Stock Analysis – Final Thoughts

In my humble opinion, I think some investors just over-complicate their investment decision-making process when it comes to companies with a pedigree such as PEP’s. In my case, when it comes to a company such as PEP, I don’t spend a whole lot of time analyzing the details of every line item of the financial statements.

I also see comments such as “I’ve owned PEP for X years but other than the dividend, it’s been pretty flat. I will continue to hold another year or two to see if it can pick up a head of steam.” Seriously?

Look, the folks at the top of PEP’s house are far brighter than many of us writing posts or making comments on posts. They are also closer to the pulse of the company, the industry, and their key customers. In addition, they have far more skin in the game than the average individual investor. Just look at the Official notification to shareholders of matters to be brought to a vote (“Proxy”) on the company’s website. I can’t imagine why they would make business decisions that would negatively impact the company.

I can’t speak for you but I would far prefer to spend quality time with family and friends than to analyze PEP’s financials. This is why I leave our PEP shares alone and just periodically add to our holdings without deliberating over a purchase for days on end. As a matter of fact, I purchased additional PEP shares for my wife’s Spousal RRSP earlier today. She doesn’t really care about investing so I’ll tell her…one day.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long PEP.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.