Summary

Summary

- This McDonald’s stock analysis is based on Q4 and FY 2016 results and outlook for fiscal 2017 released January 23, 2017.

- McDonald’s FY2016 results reflect a drop in revenue but a corresponding larger drop in expenses.

- It has been repurchasing its share at a torrid pace using LTD under attractive terms.

- I am prepared to acquire additional shares under $117.

Introduction

This morning when I returned from my morning ritual of picking up coffee from our local McDonald’s (NYSE: MCD) I got to thinking how grateful I am that our annual MCD dividends more than cover my annual MCD coffee budget ($800 – $900/year).

Given that MCD released it FY 2016 results the morning of Janauary 23, 2017, I thought I would analyze its results to see if I can feel confident it will continue to finance my coffee vice.

Business Overview

MCD is the world’s leading global food service retailer with over 36,000 locations in over 100 countries. More than 80% of their restaurants worldwide are owned and operated by independent local business people.

MCD started operating under a new organizational structure beginning July1, 2015. The following four segments combine markets with similar characteristics, challenges, and opportunities for growth.

US Market

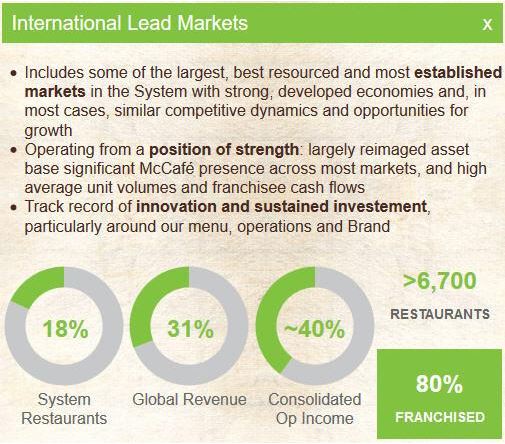

International Lead Markets

High Growth Markets

Foundational Markets

Q4 and FY2016 Financial Results

On January 23, 2017, MCD reported the following Q4 and FY2016 results.

Q4 results

- Global comparable sales increased 2.7%, including positive comparable sales in the International Lead, High Growth and Foundational segments

- Consolidated revenues decreased 5% (3% in constant currencies), due to the impact of refranchising

- Consolidated operating income increased 5% (7% in constant currencies)

- Diluted EPS of $1.44 increased 10% (12% in constant currencies)

FY2016 results

- Global comparable sales increased 3.8%, including positive comparable sales across all segments

- Consolidated revenues decreased 3% (flat in constant currencies), due to the impact of refranchising

- Consolidated operating income increased 8% (11% in constant currencies)

- Diluted EPS of $5.44 increased 13% (16% in constant currencies)

- Returned $2.2B to shareholders through share repurchases and dividends in Q4 and $14.2B for FY2016. MCD had targeted a return of $30B for the 3 year period ending 2016 and achieved same.

- MCD increased its quarterly dividend 6% beginning with the December 15, 2016 payment date (increased from $0.89 to $0.94/share).

US Q4 results

- Comparable sales declined 1.3% in the U.S., reflecting the challenging comparison against the prior year launch of the very successful All-Day Breakfast.

- Operating income for the quarter decreased 11%, as the U.S. lapped a prior year gain on the strategic sale of a unique restaurant property.

International Q4 results

- Comparable sales increased 2.8% for the quarter.

- U.K. operating income increased 1% (6% in constant currencies), fueled by sales-driven improvements in franchised margin dollars across most markets.

High Growth markets Q4 results

- Comparable sales increased 7% led by strong performance in China and positive results across the entire segment.

- Operating income rose 16% (18% in constant currencies), driven primarily by improved restaurant profitability in China, which benefited from recent VAT reform.

Foundational Markets Q4 results

- Comparable sales rose 11.1% led by strong performance in Japan and certain markets in Latin America, as well as solid results across the segment’s remaining geographic regions.

- Operating income increased with results primarily reflecting a gain from the sale of MCD Singapore in connection with refranchising initiatives, as well as improved performance in Japan.

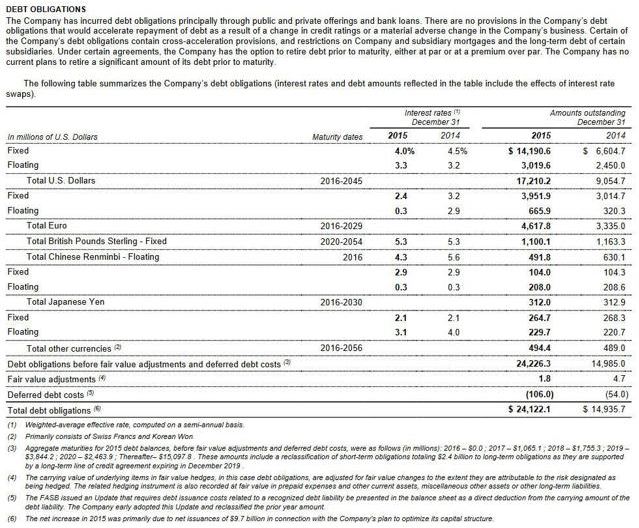

Long-Term Debt

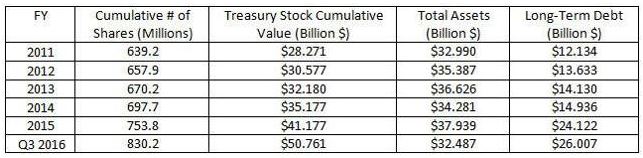

MCD has taken full advantage of the low interest rate environment and has raised a substantial amount of debt under attractive terms to repurchase roughly 191 million shares between Jan 1, 2012 – September 30, 2016.

McDonald’s Treasury Stock and Long-Term Debt

MCD reported an annual interest expense of $884.8MM in FY2016 vs. $638.3MM in FY2015, a $246.5MM or 39% increase; the December 31, 2016 Balance Sheet has not yet been publicly disseminated so I am using Q3 2016 data.

I reference the following chart from MCD’s FY2015 10-K. While the FY2016 10-K has not yet been released I am confident MCD has raised additional LTD in 2016 for the repurchase of its shares under similarly attractive terms.

McDonald’s Long-Term Debt 2015 and 2014

Outlook for Fiscal 2017

MCD’s financial goals and business turnaround plan include:

- refranchise about 4,000 restaurants by the end of 2018.

- reduce net annual G&A spending by $500 million with the vast majority to be realized by the end of 2017.

- continue ongoing efforts to strengthen business to drive long-term sustainable growth. This includes focus on customers, right-sizing structure, and having the right talent in the right areas.

- refranchising efforts and financial discipline is expected to enable MCD to direct capital and G&A resources toward new strategic opportunities to deliver on long-term strategy.

- in 2016 MCD benefited from leap year, favourable weather, and continued momentum from All-Day Breakfast in the U.S.. These factors should be taken into consideration when compared with the release of Q1 2017 results in a few months’ time.

Recent press releases regarding MCD’s ongoing efforts to expand its global reach include:

- early December 2016 – selects Lionhorn Pte. Ltd. as the Developmental Licensee (DL) for its Malaysia and Singapore

- early January 2017 – the formation of a partnership and company that will act as the master franchisee responsible for McDonald’s businesses in mainland China and Hong Kong for a term of 20 years.

- early January 2017 – inviting bids for its 33% stake in its Japanese subsidiary.

Valuation

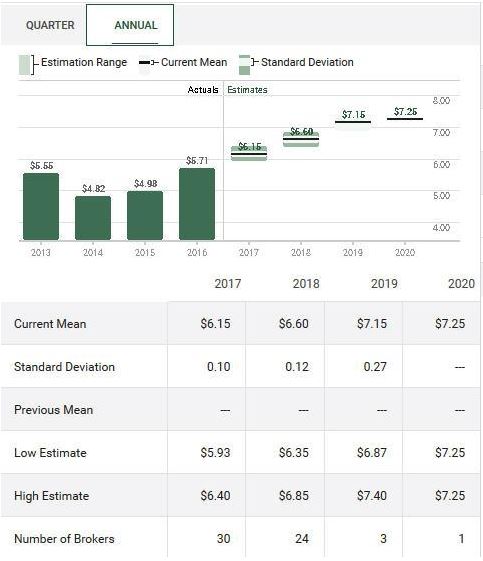

The current mean EPS of $6.15 for 2017 as provided by 30 brokers can be found in the following chart.

Source: TD WebBroker – MCD Earnings Estimates

Using this level and a PE ratio of 19 (currently 22.68) which I deem acceptable for MCD, I would be prepared to acquire additional MCD shares at any price below $116.85 (call it $117).

McDonald’s Stock Analysis – Final Thoughts

Given that MCD:

- has ample FCF to service its obligations, including the servicing of its long-term low cost debt.

- is taking the proper steps to strengthen its business to drive long-term sustainable growth.

I support management’s decision to have gone on an aggressive share repurchase program.

I think current valuation levels are somewhat detached from reality and wish an overdue market correction would occur in the not too distant future. Should my wish be granted, and the current PE ratio of 22.68 drop to 19 or lower, I would acquire shares below $117.

Until such time as this level is reached I shall:

- patiently wait for an overdue market correction.

- continue to collect MCD dividends so I can carry on with my daily coffee consumption.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you to conduct your own research and due diligence and to consult your financial advisor about your situation.

Disclosure: I am long MCD.

I wrote this article myself and it expresses my opinions. I am not receiving compensation for it and have no business relationship with any company mentioned.