Summary

Summary

- This 3M stock analysis is based on Q4 and FY 2016 results and outlook for fiscal 2017 released January 24, 2017.

- 3M reported strong result in FY2016 thus enabling it to return $6.431B to shareholders via share repurchases or dividends.

- 3M has been taking advantage of favorable interest rates and has increased LTD from $4.3B in FY2013 to over $11B as at end of Q3 2016.

- 2017 projections include EPS range of $8.45 to $8.80 (a 4% – 8% increase) and FCF conversion range of 95% to 105%.

- I would be prepared to acquire additional 3M shares below $164.

Introduction

I periodically check on the performance of the companies in which we own shares. In today’s post I review 3M (NYSE: MMM) which we (my better 50% and me) hold in the FFJ Portfolio and in other portfolios.

Business Overview

What started as a small-scale mining venture in 1902 is now a global powerhouse with operations in 70 countries and sales in 200 countries.

When I look at 3M’s product line, the industries it serves, and its brands (look at the bottom of this page if you want to see the list of industries and brands), I am awestruck.

3M Company operates through the following five segments:

- Industrial – serves markets, such as automotive original equipment manufacturer and automotive after-market, electronics, appliance, paper and printing, packaging, food and beverage, and construction.

- Safety and Graphics – serves markets for the safety, security and productivity of people, facilities and systems.

- Health Care – serves markets that include medical clinics and hospitals, pharmaceuticals, dental and orthodontic practitioners, health information systems, and food manufacturing and testing.

- Electronics and Energy – serves customers in electronics and energy markets, including solutions for electronic devices; electrical products; telecommunications networks, and power generation and distribution.

- Consumer – serves markets that include consumer retail, office business to business, home improvement, drug and pharmacy retail, and other markets.

Q4 and FY2016 Financial Results

On January 24, 2017, 3M reported the following Q4 and FY2016 results.

Q4 Results

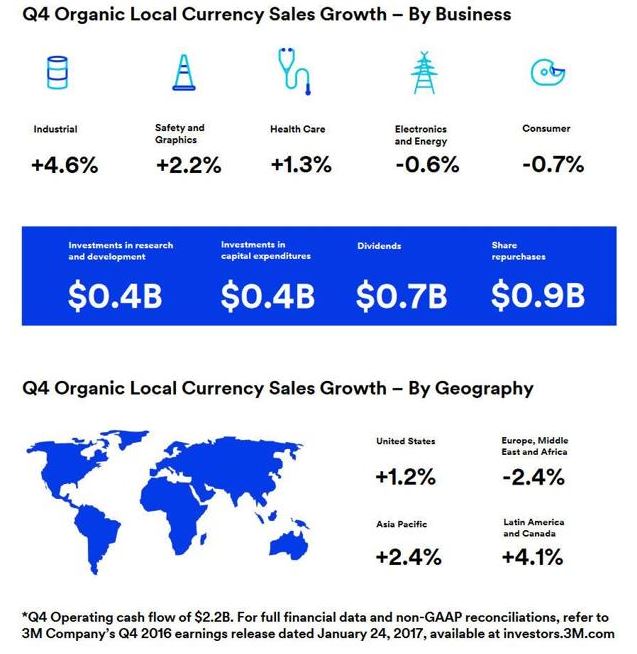

- Sales of $7.3B, up 0.4 percent; organic local-currency increased 1.6 percent

- GAAP EPS of $1.88, up 13.3% YOY

- GAAP operating income margins of 22.7%, up 2.20%

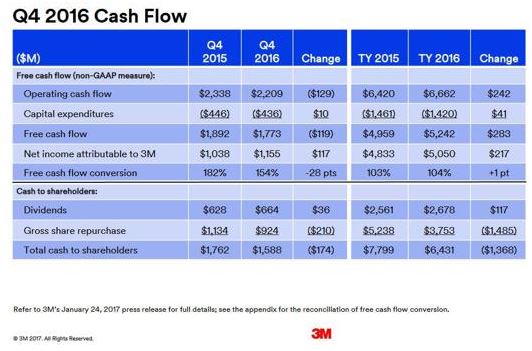

- Operating cash flow of $2.2B contributed to FCF conversion of 154%

- $1.6B returned to shareholders through dividends and gross share repurchases

In Q4, a decline in Organic Local Currency Sales Growth within the Electronics and Energy and Consumer segments was more than offset by sales growth in the other 3 segments. Growth in the US, Asia Pacific, Latin America and Canada offset a reduction in sales growth in Europe, Middle East and Africa.

3M Q4 Organic Local Currency Sales Growth

FY2016 Results

- Sales of $30.1B, down from $30.274B in FY2015

- GAAP EPS of $8.16, up 7.7% YOY

- GAAP operating income margins of 24.0%, up 1.10%

- Operating cash flow of $6.7B contributed to FCF conversion of 104%

- Return on invested capital of 23%

- $6.4B returned to shareholders through dividends and gross share repurchases

- FY2016 was the 100th consecutive year in which 3M has paid dividends

Details on the full year results for each of 3M’s five business segments can be found in its January 24, 2016 Press Release.

Strong FCF of $5.242B in FY2016 funded the majority of the $6.4B returned to shareholders.

3M Q4 and FY2016 Cash Flow

The variance between FCF and the amount returned to shareholders was funded via an increase in LTD. While the Q4 Balance Sheet has yet to be released, Q3 2016 results reflect LTD of $11.079B vs. $8.753B as at December 31, 2015.

Several companies, including 3M, have been taking advantage of the low interest rate environment to repurchase their stock.

The following chart reflects the change in MMM’s Cumulative Treasury Stock Value, Total Assets, and LTD for FY 2011 – 2015 and Q3 2016. Further details on the rates and maturity dates of 3M’s LTD which 3M has partially used to assist in the acquisition of its shares can be found on page 85 of 132 of MMM’s 2015 Annual Report. Similar details for FY2016 are not yet available.

Source: Morningstar – 3M Treasury Share History

Outlook for Fiscal 2017

- 3M affirmed its 2017 full-year performance expectations and expects:

- 2017 EPS to be in the range of $8.45 to $8.80, an increase of 4% – 8%

- organic local-currency sales growth of 1% to 3%.

- FCF conversion to be in the range of 95% to 105%.

- Effective tax rate of 28% – 29%.

It is possible that Trump’s proposed tax holiday would allow 3M to repatriate additional money currently held overseas thus enabling it to further reduce the number of outstanding shares.

While Congress initiated a tax holiday in 2004, some corporations opted not to take advantage of the “offer” because of the restrictions banning the use of repatriated funds for shareholder-friendly actions. This time around, Moody’s anticipates companies would take advantage of the tax holiday to the maximum extent possible.

Given 3M’s track record of using debt to repurchase it shares and its ample FCF, I would be supportive of the continued repurchase of shares. This assumes interest rate arrangements continue to be favorable.

Valuation

The mid-point of 3M’s 2017 EPS estimate is $8.625. The mean 2017 EPS provided by 17 brokers is $8.63.

Source: TD WebBroker – 3M Annual EPS Estimates

I am of the opinion 3M’s current price, as I compose this post, of $175.53 and its PE of 22.11 are somewhat elevated. I would prefer to acquire shares when the PE is 19 or lower. Using this PE and the $8.625 mid-point of 3M’s 2017 EPS estimate range, I would be prepared to acquire additional shares at any price below $163.88 ($164 rounded).

3M Stock Analysis – Final Thoughts

MMM has been one of our long-term core holdings and we fully intend to pass these shares on to the next generation….hopefully in the distant future. I would certainly we willing to add to our position but I think valuations are a bit rich at the moment.

I am cautiously optimistic we will experience a long overdue correction in 2017. Should same occur and shares drop to $164 or less, I will most likely add to our existing position. Until such time, however, I patiently wait and merely continue to reinvest all dividends we receive from our current 3M holdings.

Disclaimer: I have no knowledge of your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence and consulting your financial advisor about your specific situation.

Disclosure: I am long MMM.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company mentioned in this article.