Summary

Summary

- This Manulife Financial Corporation stock analysis is based on Q1 2017 results.

- Manulife is the largest life-insurance company in Canada and ranks among the top 5 globally.

- Manulife has either been a wonderful or a terrible investment with much dependent on when you acquired shares subsequent to it being demutualized in 1999.

- I suggest readers take a “pass” on Manulife. There are far better investment opportunities in the universe of publicly listed companies.

All figures are expressed in Canadian dollars unless otherwise noted.

Introduction

I have had more than my share of “winners” but on occasion I have made an investment decision which has turned out to be a dud. Today’s post is about one of those duds. Manulife Financial Corporation (NYSE: MFC) is Canada’s largest life insurance company. Details regarding MFC’s business can be found here and here and here.

On October 17, 2008 I thought I would buy myself a birthday present and so I acquired 500 MFC shares on the Toronto Stock Exchange. My rationale for investing in MFC at the time was that I:

- was grossly underweight the insurance sector;

- had had MFC on my radar but it had been too expensive for my liking since about mid-2006 and the pullback brought MFC to a more reasonable valuation level;

- was damned if I wasn’t going to collect dividends from Canada’s largest insurance company which had been collecting insurance premiums from me for years;

- was comfortable with MFC’s dividend track record and felt MFC’s earnings could continue to support moderate annual increases.

Check out MFC’s stock chart to see how that birthday gift has panned out. Brutal!

Industry Overview

Large insurers/asset managers, such as MFC are essentially, in the financial services industry. A low interest rate environment like we have had for the past several years coupled with market volatility make for difficult conditions if you are in this industry.

It is also common knowledge that the global financial services industry is in a state of consolidation and transformation. Customer needs are changing and insurers must adapt and respond to these changing needs with financial products/services that best meet their needs. I suspect some of MFC’s competitors will be unable to successfully adapt.

The financial performance of large insurers/asset managers typically suffers in a persistently low interest rate environment. While many life insurance companies have been able to hedge their balance sheet exposure to low interest rates, this is becoming increasingly challenging since we have been in a “low yield” environment for several years.

Another huge factor that impacts members of the life insurance industry is demographics. Firstly, insurers must meet the savings and retirement needs of baby boomers. Secondly, the manner in which products and services were marketed and sold to baby boomers is foreign to millennials. This presents challenges from product, marketing and distribution perspectives.

Given the macro changes life insurance companies face, some industry participants are rationalizing their businesses. Changes are being made through the revamping of products and/or the exiting of high-risk or non-strategic businesses. I recognize it is important for businesses to evolve with the times but there are generally risks associated with acquisitions, divestitures, and other form of restructuring/realignment.

Additional factors that can have a significant impact on this industry include, but are not limited to:

- currency fluctuations;

- unfavorable political developments;

- changes to accounting and regulatory rules;

- adequacy of actuarial assumptions.

Readers interested in learning more about the risks faced by industry participants, and MFC in particular, can go to page 53 where the Risk Management section within MFC’s 2016 Annual Report commences.

Business Overview

While Manulife was founded in 1887, it was not until 1999 when Manufacturers Life Insurance Company demutualized, became Manulife Financial, and became a publicly listed company.

Should you be unfamiliar with the concept of demutualization, it is the process of converting a mutual life insurance company, owned by its policyholders, to a publicly traded stock company owned by shareholders, pursuant to a plan of conversion approved by government regulators.

The amount paid to each policyholder is based on a number of factors including:

- length of time the policy has been in force

- face value of the policy

- total premiums paid.

In the Manulife demutualization process, compensation took the form of a fixed component of 186 Manulife Financial common shares plus a variable component based on policy value. Cash compensation was set at $18/share entitlement; the total value of stock and cash distributed amounted to $8.3B.

In 2004, Manulife closed its acquisition of John Hancock Financial Services Inc. This acquisition vaulted Manulife to the position of the second largest life-insurance company in North America, and the fifth-largest in the world, with more than 20,000 employees in North America and Asia.

In early 2015, Manulife completed its acquisition of Standard Life’s Canadian operations. In addition, Manulife’s U.S. Division (John Hancock Financial) successfully completed the acquisition of New York Life’s Retirement Plan Services business in early 2015. The business was combined with John Hancock Retirement Plan Services (JHRPS) to significantly increase its retirement plan assets under administration.

MFC is organized into four operating divisions:

- U.S. (36% of 2016 segment core operating profits)

- Canada (31%)

- Asia (33%)

- Corporate and other (0%)

Each division has profit and loss responsibility and develops products, services, and distribution and marketing strategies based on the profile of its business and the needs of its market.

The company’s global corporate strategy includes four key strategies for growth.

- Maximize opportunities in Asia by building a premier, top-tier pan-Asian insurance franchise that is well positioned to satisfy the protection and retirement needs of the fast-growing customer base in the region.

- Focus on growing the wealth and asset management businesses in Asia, Canada and the U.S. by building a world-class asset management company by providing simple and innovative investment solutions to retail and institutional investors

- Continue to build its balanced Canadian franchise by building a broad-based, diversified financial services company that develops and delivers integrated solutions to address its customers’ protection and retirement needs.

- Continue to grow higher return on equity, lower-risk U.S. businesses that help Americans with their retirement, long-term care and estate planning needs.

Dividend History – I Don’t Like Cuts

At the time I acquired 500 MFC shares, the quarterly dividend was $0.26 so I was getting a dividend yield of about 3.5 – 3.75%. I collected that dividend for 3 consecutive quarters after which time, MFC deemed it necessary to cut its quarterly dividend in half to $0.13. This dividend stayed frozen for almost 5 years! See dividend history here.

While moderate dividend increases were reinstated in mid-2015, the current dividend of $0.205 is still well below the $0.26 which I was receiving at the time of purchase in 2008. Factor in the time value of money and the picture is even more heartbreaking.

Credit Rating Downgrade

When I acquired MFC shares, S&P had assigned an AA+ credit rating to The Manufacturers Life Insurance Company. That rating is now AA-. While still a high rating, it is nonetheless two steps below the rating at the time I acquired MFC shares.

Executive Compensation

Given MFC’s performance over the past several years, I am astonished/flabbergasted to see that MFC’s CEO, who recently announced his intent to retire September 30, 2017, is one of the highest paid CEOs in Canada…#6 in 2016 at $15.6 Million, #6 in 2015 at $14.48 Million, #14 in 2014 at $12.76, and #21 in 2013 at $10.45 Million.

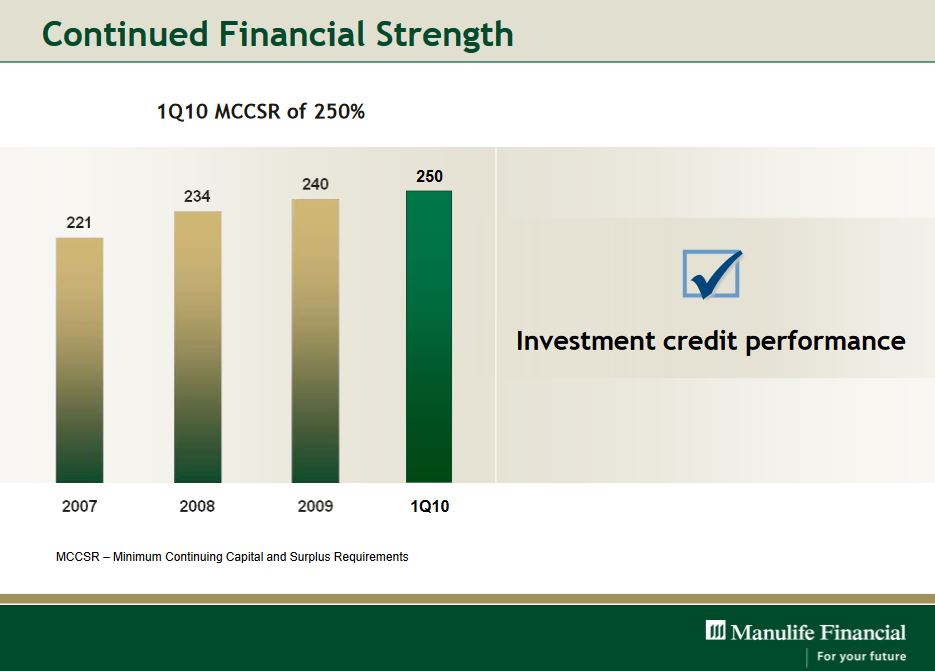

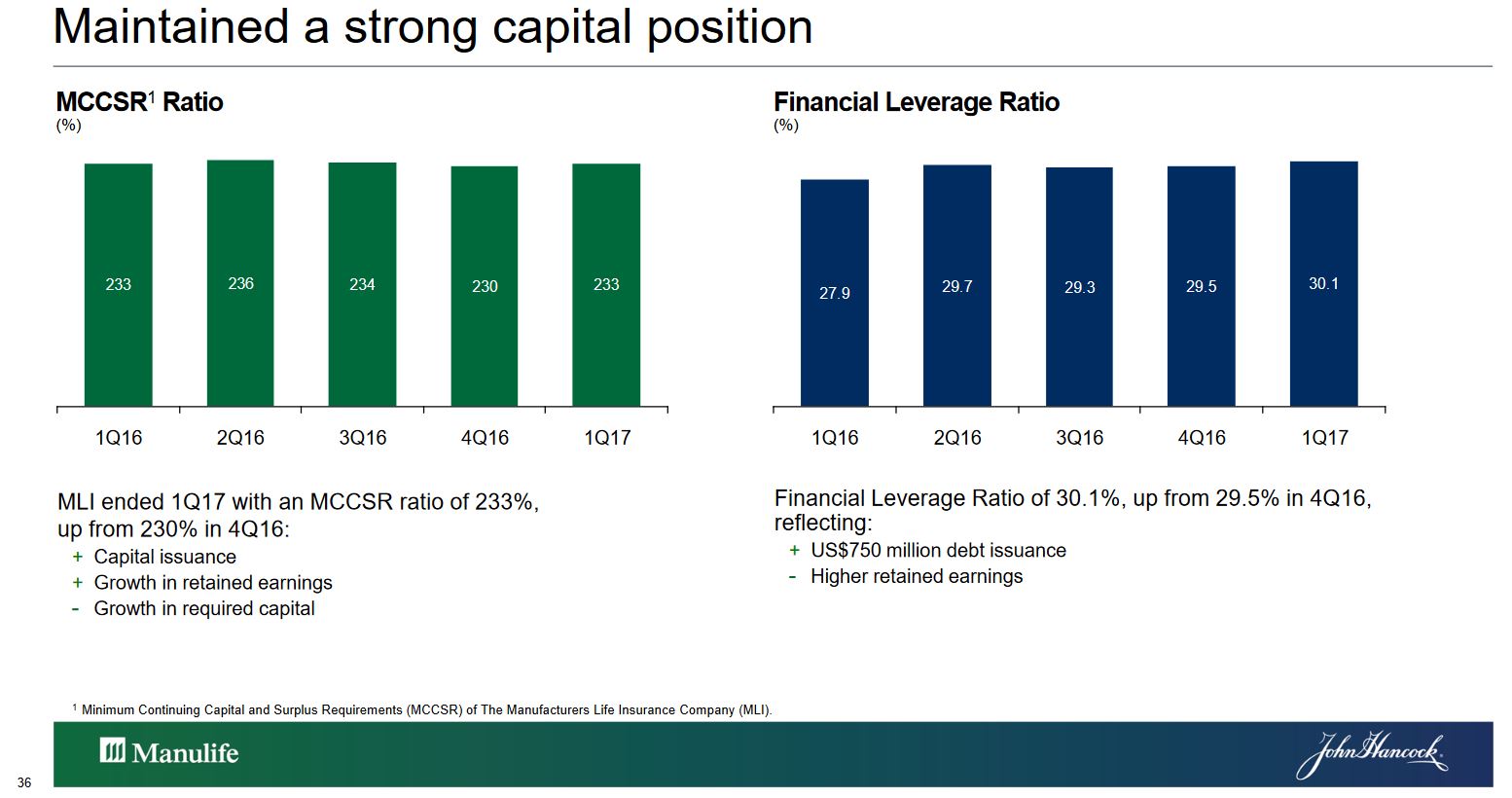

Minimum Continuing Capital and Surplus Requirements

Insurance companies can well attest as to how difficult it is to preserve capital in a low-rate, high-volatility environment. Multiple strategies must be used to maintain the high capital requirements needed to cover claims.

Amid the retreat in average bond yields, insurance companies must maintain capital by hedging, repositioning or repricing products, and through proactive management, including asset acquisition.

MFC must continually meet regulatory capital requirements for insurers. The minimum continuing capital and surplus requirements (MCCSR) guideline is a ratio that indicates a long-term ability to pay insurance claims (the higher the ratio is better). This capital ratio is set by the Office of the Superintendent of Financial Institutions (OSFI) and the MCCSR must be at least 120%, with a target of at least 150%.

Here are MFC’s MCCSR metrics for 2007 – Q1 2010.

MFC – MCCSR from 2007 to Q1 2010

Here are MFC’s MCCSR metrics for Q1 2016 – Q1 2017.

MFC – MCCSR from Q1 2016 to Q1 2017

While this guideline has deteriorated, MFC still greatly exceeds the 150% target.

Q1 2017 Financial Results

On May 3, 2017, MFC released its Q1 2017 results.

MFC has a strong market share position, strong balance sheet with a solid minimum continuing capital and surplus requirements ratio. It has a varied product lineup which it continues to expand (see here and here).

The U.S. insurance business is likely to benefit from price hikes for the long-term care business. While these price hikes are designed to boost profitability it is possible that revenue growth may slow.

MFC is sensitive to foreign exchange and interest rates risks which clouds its earnings outlook. It has, however, been making progress addressing these risks through hedging, product redesign, and repricing.

The company’s size, scale, and distribution capabilities provide it with a competitive advantage. It also has sizable exposure to the faster-growing insurance markets in Asia, despite some regulatory uncertainty.

Dividend

MFC’s dividend distribution history can be found here.

I have calculated the compound annual growth rate (CAGR) for two different time frames (2000 – 2017) and (2009 – 2017). As you can see, the CAGR is far different under these two time frames.

MFC – 8 year & 17 year CAGR Dividends

If you are interested in knowing how an investment in MFC would have panned out at different timeframes than those I have provided, you can access the access the MFC investment calculator here. Unfortunately the return calculations do not include reinvested cash dividends.

Valuation

The current mean FY2017 adjusted EPS estimates from various brokers is $2.23 and the consensus is for $2.44 in 2018.

MFC – EPS Projections June 2017

MFC is currently trading at $24.09. Using the adjusted EPS estimates reflected above, I get PE projections of 10.8 and 9.87 for 2017 and 2018. I view the ratios as acceptable under current market conditions for a company whose stock price is essentially at the same level as it was at the beginning of 2014.

Manulife Financial Corporation Stock Analsysis – Final Thoughts

MFC has been a less than stellar investment and ranks as one of the worst holdings in our portfolio of 48 different companies. Fortunately it only represents a rounding error relative to our overall portfolio.

While MFC might be a good insurance company and stronger relative to many of its peers, many MFC investors could have generated far greater returns by investing in other companies. When you compare how Sun Life Financial (NYSE: SLF) and Industrial Alliance Insurance and Financial Services (OTCPK: IDLLF) have performed relative to MFC from the date of my purchase (October 17, 2008), you can see why my experience with MFC has not been entirely pleasant. I do, however, recognize my “loser” might be your “winner”.

MFC – Stock price performance comparison

Had I been patient for just another 6 months, I could have purchased MFC in March 2009 when MFC’s stock price plunged to the single digit; the summer of 2012 would have been another good time to acquire MFC shares. The only saving grace is that I have been automatically reinvesting all dividends so my average price has dropped to a level where it is close to the current market price.

I recognize some readers cut loose any investment as soon as there has been a dividend cut. I, however, do not practice this strategy. If the business is fundamentally sound, I am prepared to give management time to rectify the issues which have resulted in a dividend cut.

As for you, if you do not currently own MFC, I suggest you refrain from initiating a position; there are far better investment opportunities. If you currently own MFC, I leave it to you to decide what to do with your MFC shares. Your MFC experience may be far more pleasant than mine.

Note: I sincerely appreciate the time you took to read this post. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: At the time of writing this post I am long MFC.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.

agree on your analysis on MFC. It’s heartbreaking to own and will take ‘pass’ on timely manner. Thanks.

Turbo Tong,

Glad I was able to save you some heartbreak. Thanks for reading.