I last reviewed CME Group (CME) in this August 1, 2023 post at which time the most recently available financial information was for Q2 and YTD2023. With the release of Q3 and YTD2023 results on October 25, I revisit this holding.

Overview

A high-level overview of the company is provided in previous posts that are accessible in the FFJ Archives. The best way to familiarize yourself with CME, however, is to read Part 1 in the 2022 Form 10-K.

Exchanges have been consolidating over the years and some have expanded beyond market-sensitive businesses like trading to pursue more predictable revenue; I reference my recent Nasdaq Is Targeting Higher Annual Recurring Revenue and Intercontinental Exchange – Consistent Growth and Value Creation posts.

CME’s last big acquisition was Nex Group in 2018 for $5.5B, following large deals to acquire the Chicago Board of Trade (2007) and the New York Mercantile Exchange (2008).

Over the past few years, investors have speculated that CME may look to acquire/merge with Cboe Global Markets (CBOE), the smaller Chicago-based derivatives exchange. I do not think this will happen since it would likely involve spin-offs and antitrust concerns.

CME is benefiting from increased demand for hedging because of market volatility and is in a strong position to make acquisitions given its low leverage and strong earnings and cash flow. CME’s CEO, however, has recently reiterated that 80% of their business is derived from transactions which, because of their nature, are recurring. There is, therefore, no urgency to pursue an acquisition. CME has stated that it will only entertain M&A transactions that can strategically benefit its investors and clients.

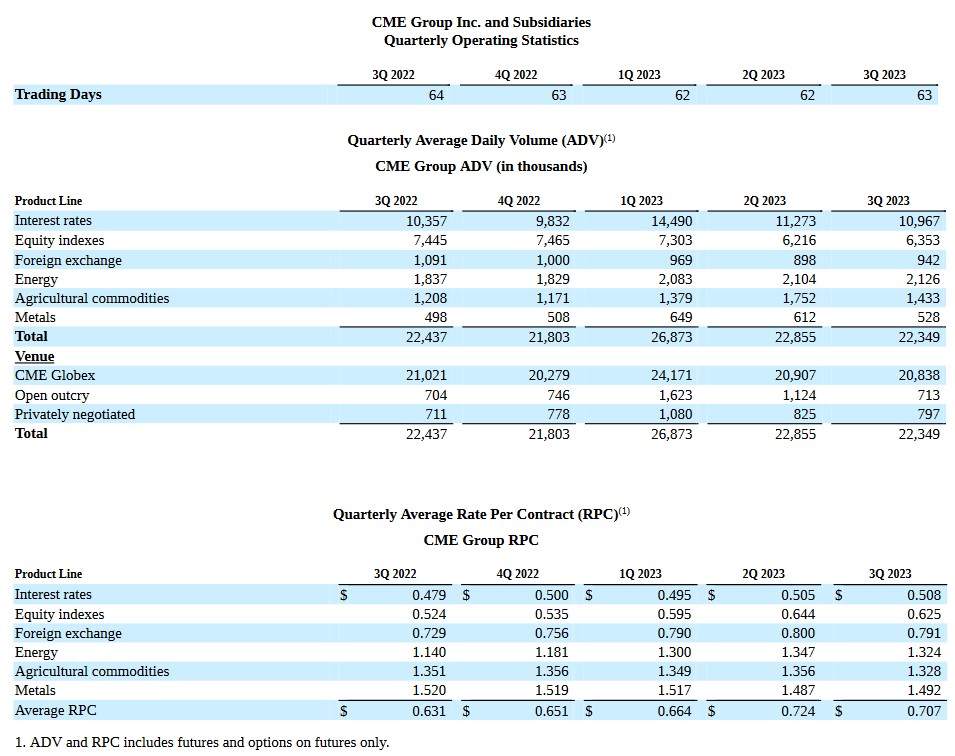

Financials

Q3 and YTD2023 Results

CME’s Q3 and YTD2023 results are reflected in its Form 8-K.

YTD2023 results are benefiting from a 4% – 5% price hike this year which is well above the typical 1% – 2% annual price hike. Future price increases are likely to revert to the historical norm.

CME is benefiting from higher volatility across multiple asset classes which is driving increased trading volume.

Increased retail interest in the equity markets has also benefited CME.

Outlook

Predicting volumes or market conditions over the short term is extremely difficult. However, over a 5-, 7- or 10-year period, CME has grown earnings by a compound annual growth rate of 10% – 12%. This growth has been achieved despite multiple periods of 0% rate policy and the impact of the pandemic on the global economy.

CME is ideally positioned to capitalize on the need for greater risk management. The plan is to accelerate growth through customer expansion, and new product and service innovation while enhancing capital efficiency. Management has stated that its goal is to deliver growth in the coming decade above historical averages.

Credit Ratings

From a risk perspective, CME’s debt is less than one times its EBITDA, well below that of rivals Intercontinental Exchange (ICE), Nasdaq (NDAQ) and CBOE (CBOE).

CME has yet to release its Q3 2023 Form 10-Q in which we can find the details of its debt. However, looking at CME’s schedule of outstanding debt found in the Q1 and Q2 Form 10-Q, we see very little difference between the amounts owing at the end of Q1, Q2 and Q3; long-term debt at the end of Q3 was $3,424.7 (page 7 of 10 in the Form 8-K).

Source: CME – Q2 2023 Form 10-Q

Source: CME – Q1 2023 Form 10-Q

There are no changes to CME’s senior unsecured long-term debt ratings from those at the time of my November 14, 2022 post.

- Moody’s: Aa3 with a stable outlook

- S&P Global: AA- with a stable outlook

- Fitch: AA- with a stable outlook

All are the lowest tier of the high-grade category and are investment grade. These ratings define CME as having a VERY STRONG capacity to meet its financial commitments. It differs from the highest-rated obligors only to a small degree.

CME’s credit risk is acceptable for my purposes.

Dividend and Dividend Yield

CME’s dividend history is accessible here.

CME’s dividend policy targets a regular quarterly dividend of between 50% – 60% of the prior year’s cash earnings. In addition, CME declares its ‘special annual variable dividend’ within the first 2 weeks of December for distribution in mid-January.

NOTE: Since the implementation of the special annual variable dividend policy in early 2012, CME has returned over $22B to shareholders in the form of dividends.

This ‘special annual variable dividend’ increases or decreases from year to year based on operating results, capital expenditures, potential merger and acquisition activity and other forms of capital return, including regular dividends and share buybacks during the prior year.

Given how this ‘special annual variable dividend’ is determined, it is very difficult to predict the amount to be declared. I do, however, compare Q3 results for the current fiscal year with Q3 results in prior recent years to try and predict the upcoming ‘special annual variable dividend’.

When I wrote my November 14, 2022 post, I envisioned the declaration of at least a $3/share ‘special dividend’. Based on 4 quarterly $1/share dividends plus the $3/share ‘special annual variable dividend’, investors who held shares since at least the beginning of 2022 would receive $7/share in total annual dividend income.

CME ended up declaring a $4.50 special dividend on December 8 for distribution on January 18, 2023. As a result, my $7 estimate ended up being $8.50. Using the ~$174 share price, the dividend yield was ~4.88%.

I also anticipated that CME would declare a $0.05 dividend increase in February for distribution near the end of March. CME ended up declaring a $0.10 dividend increase; the quarterly dividend is now $1.10.

A comparison of CME’s YTD2023 results with those for the first 3 quarters of FY2020, FY2021, and FY2022 suggests CME’s ‘special annual variable dividend’ could be $5. CME could also raise its quarterly dividend from $1.10 to $1.20. If I conservatively estimate a $4.75 ‘special annual variable dividend’ and a $1.15 quarterly dividend, the forward dividend yield is ~4.47%. This is based on the current ~$209 share price and $9.35 ($4.75 + (4 x $1.15)) in dividends that could be distributed in FY2024.

CME has not repurchased shares in recent years; the weighted average number of issued and outstanding shares in FY2011 – FY2022 (in millions) is 334, 332, 334, 336, 338, 339, 340, 344, 358, 359, 359, and 359. The weighted average number of issued and outstanding shares in Q3 2023 is approaching 360.

While management continues to discuss alternative means by which to return capital to shareholders including share repurchases, the current dividend policy appeals to CME’s shareholders. It is, therefore, unlikely CME will start to repurchase shares in the foreseeable future.

Valuation

CME’s diluted PE in FY2011 – FY2022 is 12.92, 18.77, 27.53, 29.45, 24.22, 26.89, 33.12, 14.20, 35.28, 30.34, 33.70, and 22.94.

I reference my August 1, 2023 post in which I reflect CME’s valuation at the time I wrote prior posts. For ease of comparison, below is CME’s valuation when I wrote my most recent 3 prior posts.

On July 27, 2022, I acquired additional shares at $195.135. Using the current broker estimates, the forward adjusted diluted PE levels were:

- FY2022 – 17 brokers – mean of $7.91 and low/high of $7.33 – $8.23. Using the mean estimate, the forward adjusted diluted PE is ~24.7.

- FY2023 – 17 brokers – mean of $8.43 and low/high of $7.87 – $9.21. Using the mean estimate, the forward adjusted diluted PE is ~23.

- FY2024 – 12 brokers – mean of $8.88 and low/high of $8.14 – $9.94. Using the mean estimate, the forward adjusted diluted PE is ~22.

On November 14, 2022, shares were trading at ~$174. Using the current broker estimates, the forward adjusted diluted PE levels were:

- FY2022 – 14 brokers – mean of $7.98 and low/high of $7.82 – $8.07. Using the mean estimate, the forward adjusted diluted PE is ~22.

- FY2023 – 15 brokers – mean of $8.36 and low/high of $7.73 – $8.70. Using the mean estimate, the forward adjusted diluted PE is ~21.

- FY2024 – 13 brokers – mean of $8.69 and low/high of $7.96 – $9.38. Using the mean estimate, the forward adjusted diluted PE is ~20.

Shares closed at ~$199 on July 31. Using the current broker estimates, the forward adjusted diluted PE levels are:

- FY2023 – 17 brokers – mean of $9.03 and low/high of $8.81 – $9.27. Using the mean estimate, the forward adjusted diluted PE is ~22.

- FY2024 – 17 brokers – mean of $9.22 and low/high of $8.58 – $9.74. Using the mean estimate, the forward adjusted diluted PE is ~21.6.

- FY2025 – 10 brokers – mean of $9.77 and low/high of $8.96 – $10.34. Using the mean estimate, the forward adjusted diluted PE is ~20.4.

Shares closed at ~$209 on October 27. Using the current broker estimates, the forward adjusted diluted PE levels are:

- FY2023 – 16 brokers – mean of $9.15 and low/high of $8.97 – $9.33. Using the mean estimate, the forward adjusted diluted PE is ~22.8.

- FY2024 – 16 brokers – mean of $9.39 and low/high of $8.84 – $10.48. Using the mean estimate, the forward adjusted diluted PE is ~22.2.

- FY2025 – 13 brokers – mean of $9.72 and low/high of $8.97 – $10.53. Using the mean estimate, the forward adjusted diluted PE is ~21.5.

Final Thoughts

CME appeals to me in that it provides products and services to help investors hedge their risks. While 80% of CME’s business is transactional in nature, investors need to continually hedge their risks so its business is somewhat recurring in nature.

Over the long term, I think CME will continue to benefit from the need to hedge energy, interest rates, and commodity exposure. In addition, CME’s growth also comes through the introduction of new futures contracts, like the micro E-mini S&P 500 contract and bitcoin futures.

Having said this, the question arises as to whether CME can sustain growth internally when interest rates become more predictable, volatility decreases and more competition enters the exchange space. I think CME will adapt to changes in its business environment and am in agreement that the acquisition of CBOE is not necessary for CME to thrive.

My CME exposure currently consists of 449 shares in a ‘Core’ account and 331 shares in a ‘Side’ account within the FFJ Portfolio. Other than the automatic reinvestment of dividend income, I am not looking to add to my exposure.

If CME appeals to you, I consider shares to be fairly valued.

I wish you much success on your journey to financial freedom!

Note: Thanks for reading this article. Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long CME, ICE, and NDAQ.

Disclaimer: I do not know your circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decisions without conducting your research and due diligence. You should also consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.