Summary

Summary

- This Church & Dwight analysis is based on Q4 and Fy2017 results released February 5th, 2018.

- CHD outperforms all members of its peer group from a free cash flow conversion process.

- In FY2016, 82% of CHD’s sales were in the US. CHD is now making a concerted effort to expand its international sales.

- CHD represents my/my wife’s 5th holding in our investment portfolio.

- CHD is currently fairly valued and I have recently acquired another 200 shares.

Introduction

This article touches upon Church & Dwight’s (NYSE: CHD) Q4 and FY2017 results and FY2018 forecast; these were released February 5, 2018.

If you’re interested, you may also want to have a quick look at my previous CHD articles which can be found here and here.

Company Overview

CHD might be an unfamiliar name to some readers but these same readers are likely very familiar with several of CHD’s brands.

CHD was founded in 1846. It develops, manufactures and markets a broad range of household, personal care and specialty products. It has a variety of consumer branded products which are sold through a broad distribution platform that includes supermarkets, mass merchandisers, wholesale clubs, drugstores, convenience stores, home stores, dollar, pet and other specialty stores and websites. CHD also sells specialty products to industrial customers and distributors.

CHD focuses its consumer products marketing efforts principally on its 11 ‘Power Brands’. These 11 brands represent more than 80% of CHD’s sales and profits.

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Subsequent to our initial CHD investment around the 2004 – 2005 timeframe, CHD has undergone a massive transformation. Six of CHD’s 11 Power Brands have been added to the CHD portfolio in 2005 or later and CHD’s annual revenue has increased ~2.5Xs.

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Q4 and FY2017 Results

CHD’s most recent results can be found here.

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Source: CHD 2018 Analyst Day Presentation February 5, 2018

CHD’s annual revenue in FY2017 only amounted to ~$3.776B which pales in comparison to its much larger peers. While CHD is barely a blip on the radar when viewed next to Procter and Gamble (NYSE: PG) and Unilever (NYSE: UL), it has this propensity to generate considerable free cash flow.

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Source: CHD 2018 Analyst Day Presentation February 5, 2018

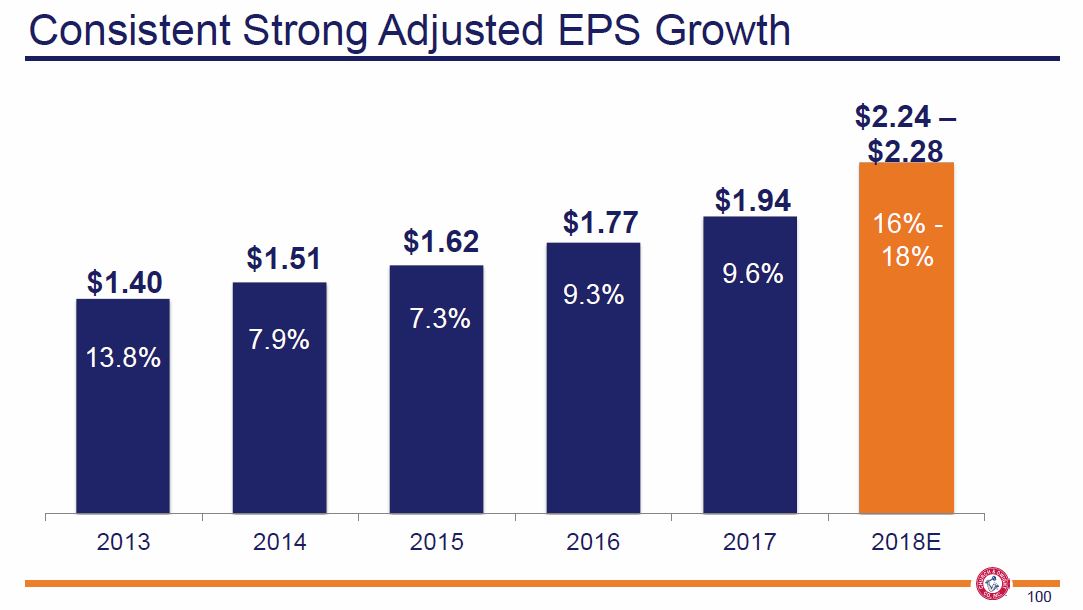

FY2018 Projections

Management has indicated that innovation continues to be a big driver of CHD’s success. Several new product launches in several categories are expected to occur in 2018.

Earnings per Share in the $2.24 – $2.28 range is expected. In addition, adjusted EPS growth of 16%-18%, or 21% to 23% on a non-adjusted basis, is forecast.

Source: CHD 2018 Analyst Day Presentation February 5 2018

Source: CHD 2018 Analyst Day Presentation February 5 2018

CHD also expects sales growth of ~8% and organic sales growth of ~3%. Its gross margin is expected to remain flat.

CHD has plans to grow its international business. It has recently established a new subsidiary in Germany and has established export offices in Panama, Singapore, and the UK.

In 2017, over $0.6B of CHD’s net sales were generated through international markets. CHD is now positioned for 6% organic growth from international markets and exports are expected to grow in the double digits.

Credit Ratings

Moody’s currently rates CHD’s long-term debt as Baa1 which is classified as lower medium grade. Standard & Poors rates the debt BBB+ which is also lower medium grade. Neither agency has CHD’s debt under review.

Insider Buys

I place more weight on ‘Insider Buys’ than ‘Insider Sells’ as ‘Insider Sells’ can occur for a variety of reasons that are unrelated to how the insiders view the future direction of the company’s stock price.

Matthew T. Farrell, President and Chief Executive Officer and Richard A. Dierker, Executive Vice President & Chief Financial Officer acquired 5,000 and 1,146 shares, respectively, in November 2017 when CHD’s stock price was ~$43.

Free Cash Flow Conversion

CHD continues to generate strong FCF and outpaces its much larger peers in this regard.

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Dividend, Dividend Yield, and Dividend Payout Ratio

CHD’s dividend history can be found here.

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Looking at CHD’s dividend history we see that shareholders received $0.06/share/year in dividends in 2005. In 2017, the annual dividend had increased to $0.76/share.

On February 5, 2018, CHD’s Board of Directors declared a 14% increase in the regular quarterly dividend from $0.19/share to $0.2175/share which is the equivalent to an annual dividend of $0.87/share; this new quarterly dividend will be payable March 1, 2018 to stockholders of record at the close of business on February 15, 2018.

This marks the 22nd consecutive year in which CHD has increased its dividend. In addition, CHD has paid a regular consecutive quarterly dividend for 117 years.

At a current stock price of ~$48, the annual $0.76 dividend generates a ~1.6% dividend yield. The new $0.87 annual dividend yields ~1.8%. This yield may be unappealing to dividend yield hungry investors but the forward dividend yield is the most attractive it has been in several years.

On the basis of 2017 Reported EPS of $2.90, the $0.76 dividend represents a ~26% dividend payout ratio. On the basis of 2017 Adjusted EPS of $1.94, the $0.76 dividend represents a ~39% dividend payout ratio.

Share Repurchases

On November 1, 2017, CHD’s Board authorized a new stock repurchase program under which up to $0.5B of outstanding common stock may be repurchased to reduce the number of outstanding shares. There is also a separate repurchase program intended to neutralize the dilution associated with the exercise of stock options issued.

CHD has repurchased a considerable number of shares over the years. In fiscal 2011 the weighted average shares outstanding (Basic and Diluted) amounted to 286.4 million and 291.6 million, respectively. In fiscal 2017, these figures were 250.6 million and 256.1 million.

Despite the significant reduction in shares outstanding and the dramatic growth in the company’s dividend, management has stipulated that return of cash to shareholders is the 5th item on the list of priorities with respect to the use of free cash flow.

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Valuation

On the basis of 2017 Reported EPS of $2.90 and a ~$48 stock price, we get a ~16.5 PE. On the basis of 2017 Adjusted EPS of $1.94, we get a ~24.74 adjusted PE.

Management has forecast 2018 adjusted EPS of $2.24 – $2.28. Using this range and the current stock price of ~$48, we get a forward adjusted PE range of ~21 – ~21.4.

Source: CHD 2018 Analyst Day Presentation February 5, 2018

Source: CHD 2018 Analyst Day Presentation February 5, 2018

I view this as a reasonably attractive valuation for a company with CHD’s long-term growth potential.

Final Thoughts

Many readers prefer the ‘Shotgun’ approach to investing where they own shares in multiple companies. I, however, prefer the ‘Rifle’ approach; our investments are concentrated. Our Top 10 holdings represent ~53% of our overall portfolio and the next 10 represent ~21% of our portfolio; CHD is our 5th largest holding.

I have followed CHD for years and continue to be impressed with the manner in which the company is run. As evidence of my confidence in management I acquired another 200 shares on February 6, 2018.

I hope you enjoyed this post and I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this post. As always, please leave any feedback and questions you may have in the “Contact Me Here” section to the right.

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I am long CHD.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.