On May 5, 2021, I wrote a Broadridge Financial Solutions (BR) stock analysis. For whatever reason, I decided to keep it in ‘draft’ format and completely forgot about it; at the time, BR had just reported Q3 2021 results.

Fast forward to December 4, 2021, and BR is currently in Q2 2022; the company’s fiscal year-end is the end of June.

As a BR shareholder since its spin-off from Automatic Data processing (ADP) in March 2007, I watched the share price languish for ~6 years. In hindsight, I should have been ‘backing up the truck’ during this timeframe. As is the case with most of my investment errors, this was an error of omission versus an error of commission and my exposure currently only consists of 534 shares in one of the ‘Side’ accounts in the FFJ Portfolio and shares in a retirement account for which I do not disclose details.

Unfortunately, this ‘hidden gem’ joined the companies that comprise the S&P500 in June 2018. Since such time, BR has gone from an attractively valued investment to one that is generally richly valued.

Broadridge – Stock Analysis – Business Overview

Part 1 (Item 1) in BR’s FY2021 10-K provides a comprehensive overview of the company’s two reportable segments: Investor Communication Solutions (ICS) and Global Technology and Operations (GTO).

Item 1A then goes on to provide a host of potential risks and uncertainties that, if they develop into actual events, could have a material adverse effect on the business, financial condition, or results of operations. Each risk carries a different degree of probability and how each investor views the probability of these events occurring will influence their decision-making process.

One such risk, for example, is that BR derives a large percentage of its revenue from a small number of clients in the financial services industry. While this is a very real risk, I view this risk as acceptable.

Investors unfamiliar with BR can find additional information in the September 9, 2021, Investor Presentation.

A similar presentation prepared in February 2021 identified BR’s market opportunity as being $46B. This market opportunity now stands at $52B with the $6B increase attributed to the ‘Capital Markets’ space.

Itiviti Acquisition

On March 29, 2021, BR announced the ~$2.5B acquisition of Itiviti; this acquisition closed in May 2021.

Further details are included in the March 29, 2021 Itiviti Acquisition Presentation.

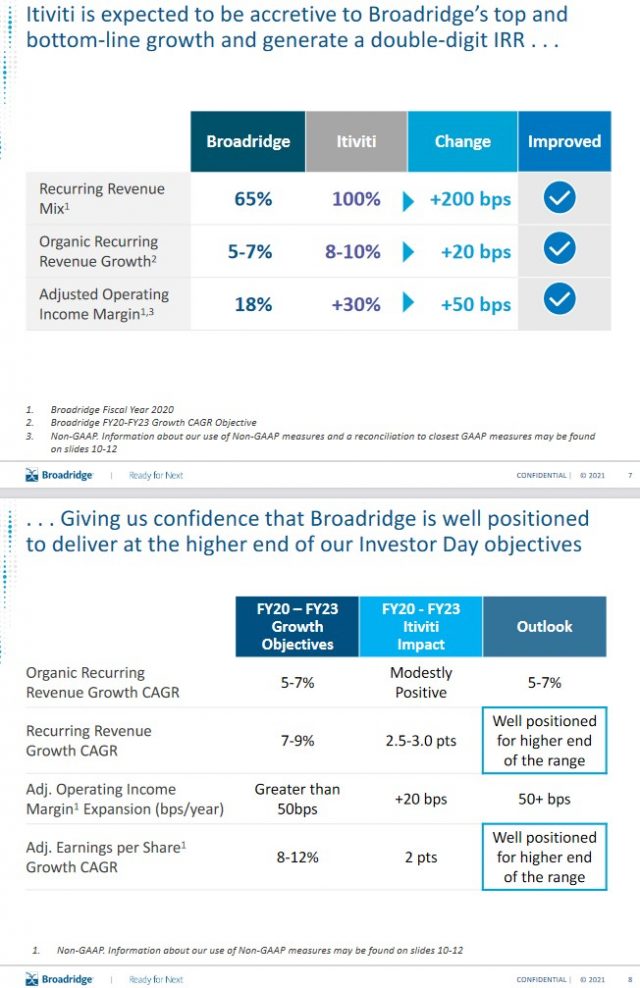

Itiviti is a leading provider of order management and trade execution technology and connectivity solutions for financial institutions. By bringing Itiviti into the BR fold, BR increases its opportunity to extend its capital market service offering. The combination of Itiviti’s front-office trading solutions and BR’s leading post-trade back-office capabilities will allow BR to serve a client’s entire trade life cycle from order to settlement. This is becoming increasingly important given the growth in high frequency and algorithm trading.

Itiviti adds more than $6B to BR’s total addressable market and should drive stronger growth, margins, and earnings.

In March 2021, BR entered into a term credit agreement providing for term loan commitments in an aggregate principal amount of $2.55B to acquire Itiviti; the final consideration paid, net of cash acquired, amounted to $2.5804B; BR borrowed under its established credit facilities in May 2021 to finance the acquisition. Details of its existing credit facilities are found on page 42 of 86 in the Q1 2022 10-Q.

BR plans to rapidly de-lever over the next 2 years.

BR expects near-term dilution from Itiviti but has indicated this acquisition positions it to deliver 11% – 13% adjusted EPS growth.

With the inclusion of this acquisition, BR appears to be well-positioned to achieve the higher end of the 3 year 7 – 9% recurring revenue growth and 8 – 12% Adjusted EPS growth CAGRs presented at the December 2020 Investor Day.

Despite this sizable acquisition funded primarily by debt, BR is not changing its capital allocation priorities. It remains committed to funding internal investments, growing its dividend, and making tuck-in acquisitions.

Acquisitions in Q1 2022

On July 1, 2021, BR announced that it is further enhancing its regulatory compliance capabilities for broker-dealers with the tuck-in acquisition of the cloud-based Execution Compliance and Surveillance Service (ECS) assets from Jordan & Jordan. The acquired solution provides a combination of surveillance and regulatory reporting as well as compliance consulting capabilities for US regulations.

On August 2, 2021, BR announced the acquisition of the remaining 68% of Alpha Omega it did not previously own; Alpha Omega is a market-leading FIX-based post-trade solutions provider for the investment management industry.

This acquisition builds on Broadridge’s recent acquisition of Itiviti. With this acquisition, BR will be able to fully consolidate Alpha Omega’s post-trade matching and consolidation solution into its existing NYFIX connectivity and FIX infrastructure to better automate buy-side and sell-side firms’ trade matching processes and further accelerate BR’s product roadmap. Further details on these solutions can be found here.

Both acquisitions are reported in BR’s GTO segment.

Q1 2022 Results

I provide links to BR’s Q1 2022 10-Q, November 3 Q1 Earnings Release, and Q1 Earnings Presentation for ease of reference.

BR’s regulatory business continues to benefit from the retail trading boom.

Management indicates the move to reducing trading commissions has triggered a significant expansion in the number of market participants. This has contributed to the increase in equity record growth. This strong growth is broad-based across BR’s broker clients but is even more pronounced at the online brokers. BR has also evidenced broad-based growth across issuers with 20% growth across both widely held stocks and those with more medium-sized shareholder bases.

Large increases have come from a handful of names such as meme stocks like GameStop; a meme stock is a stock that has seen an increase in volume because of hype on social media and online forums like Reddit and not because of the company’s underlying performance. These stocks often become overvalued with drastic price increases in a short timeframe.

The increase from such stocks contributed very little to BR’s growth.

BR acknowledges that commission-free trading is the latest step in a long-term trend. It includes the rise of ETFs, lower trading costs across all participants and changes in investor interfaces that have helped propel high single-digit equity and fund record growth over the past decade. Given these trends, BR has invested to scale its capabilities to:

- meet the rise in demand;

- increase the digitization of critical regulatory communications;

- ensure new and existing investors receive the information needed to understand the risks; and

- participate in the governance of investors’ investments.

FY2022 Guidance

BR’s FY2022 guidance reflects no changes from guidance provided August 12, 2021 when FY2021 earnings were released.

Free Cash Flow (FCF)

Looking at BR’s Consolidated Statements of Cash Flows in the FY2021 10-K (page 60 of 183), we see significant amortization expenses. These non-cash expenses distort GAAP earnings. As a result, it is important to look at BR’s Operating Cash Flow and Free Cash Flow.

Management views FCF to be a liquidity measure that provides useful information about the amount of cash generated that could be used for dividends, share repurchases, strategic acquisitions, other investments, as well as debt servicing. It is a Non–GAAP financial measure and is defined by BR as net cash flows provided by operating activities plus proceeds from asset sales, minus capital expenditures as well as software purchases and capitalized internal use software.

Looking at the Consolidated Statement of Cash Flows in the FY2011 – FY2021 10-Ks, we see FCF of 167, 238, 220, 334, 365, 362, 312, 556, 544, 500, and 557 (in millions of $). In Q1 2022, FCF was (~$151.4).

Free cash flow is typically negative in Q1. This was again the case in Q1 2022 as BR’s net cash outflow used in operating activities (GAAP) was $135.4 million and it incurred $15.9 million toward capital expenditures and software purchases and capitalized internal use software; there were no proceeds from asset sales.

BR’s strong free cash flow business model enables it to:

- pursue balanced capital allocation;

- commit to a rising dividend;

- fund investments in the company’s platform and products; and

- make a significant M&A investment to grow the capital markets franchise.

I see no reason to expect any changes going forward.

Broadridge – Stock Analysis – Credit Ratings

All BR’s domestic senior unsecured debt ratings are the top tier of the lower-medium grade investment-grade category.

- Moody’s: Baa1 and stable;

- S&P Global: BBB+ with a negative outlook since March 29, 2021;

- Fitch: BBB+ and stable.

These ratings define BR as having an ADEQUATE capacity to meet its financial commitments. Adverse economic conditions or changing circumstances, however, are more likely to lead to a weakened capacity of the obligor to meet its financial commitments.

Even if S&P Global downgrades BR to BBB, the definition reflected above still applies.

I view BR’s credit risk as acceptable for my purposes.

Broadridge – Stock Analysis – Dividends and Share Repurchases

Dividend and Dividend Yield

Looking at BR’s dividend history we see that on October 5, BR distributed its first $0.64 quarterly dividend; this dividend was increased ~11.3% from the prior $0.575.

When I looked at BR in early May, the dividend yield was ~1.4% based on a ~$164 share price. Shares are now trading at ~$171 and the current dividend yield is ~1.5%.

Investors should temper their dividend yield expectations with BR; its dividend yield is habitually in this range.

As indicated in several posts, I suggest investors approach investments from a total potential investment return as opposed to fixating on dividend income/dividend yield.

The weighted average diluted shares outstanding in FY2011 – 2021 was 128.3, 127.5, 125.4, 124.1, 124, 121.6, 120.8, 120.4, 118.8, 117, and 117.8 (millions of shares); this increased to 118.3 in Q1 2022.

BR calculates diluted EPS using the treasury stock method. This method reflects the potential dilution that could occur if outstanding stock options are exercised and restricted stock unit awards have vested.

I envision share repurchases will be lower than in recent years as BR works toward reducing the debt used to acquire Itiviti.

Broadridge – Stock Analysis – Valuation

My last major BR purchases were in November 2018 and February 2019.

At the time of my November 2018 purchase, BR’s share price had retraced to ~$105. Based on reaffirmed guidance, BR’s forward PE was ~25.4 – ~26.3 and its forward adjusted PE was ~22.2 – ~22.98.

In February 2019, guidance had just been reaffirmed and using the ~$95.80 share price, the forward PE range was ~23.2 – ~24 and its forward adjusted PE range was ~20.3 – ~20.96.

When I composed my draft post based on BR’s May 4, 2021 earnings release, BR was trading at ~$164 and guidance was for adjusted diluted EPS to increase 11 – 13%. The earnings estimates from the two online brokerage firms I use were:

- FY2021 – 8 brokers – mean adjusted earnings estimate of ~$5.55 for a forward adjusted diluted PE of ~29.5.

- FY2022 – 8 brokers – mean adjusted earnings estimate of ~$6.10 for a forward adjusted diluted PE of ~27.

Shares are now trading at ~$171 and broker guidance is:

- FY2022 – 8 brokers – mean of $6.43 and low/high of $6.22 – $6.65. Using the mean, the forward adjusted diluted PE is ~26.6.

- FY2023 – 8 brokers – mean of $7.05 and low/high of $6.89 – $7.31. Using the mean, the forward adjusted diluted PE was ~24.3.

- FY2024 – 3 brokers – mean of $7.46 and low/high of $7.35 – $7.55. Using the mean, the forward adjusted diluted PE was ~23.

I am reluctant to use FY2024 estimates since only 3 brokers have provided guidance and so much can change within 2 years.

Broadridge – Stock Analysis – Final Thoughts

On May 2, 2021, I wrote a post entitled The Importance Of Margin Of Safety.

In several recent articles, I have reiterated my concern about a stock market that appears to be a casino. Many investors appear to be making investment decisions solely based on stock prices.

As recently as late October, BR’s share price was ~$185. Based on current FY2022 earnings estimates from 8 brokers, BR’s forward adjusted diluted PE was ~29 based on a mean estimate of $6.43.

The recent pullback in BR’s share price has led to a slightly more attractive valuation. However, I have a nagging suspicion that the growing number of Omicron coronavirus variant cases is going to lead to volatile market conditions; BR’s share price could experience a further drop thus leading to a somewhat better valuation.

I am in no rush to acquire additional shares and will apply the Patience and Discipline personal attributes Charlie Munger encourages investors to use to improve investment success.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BR.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.