Benefit from Blackstone’s (BX) durable model. This durable model along with the benefits of thematic investing enables BX to invest on behalf of pension funds and other leading institutions so as to continue expanding even in the most difficult of times.

With $950.9B in total Assets Under Management (AUM) at the end of Q3 2022, it is not surprising most investors have no idea BX fully/partially owns many well-known companies.

Take, for example, the Great Wolf Lodge (see image above). How many investors know that in October 2019, Blackstone Real Estate Partners IX, an affiliate of BX, and affiliates of Centerbridge Partners, L.P. (the owner of Great Wolfe Lodge) announced that BX was to acquire a 65% controlling interest in Great Wolf Resorts, Inc. to form a new $2.9B joint venture? When BX acquired a stake in Great Wolf, the largest family of indoor water park resorts in North America, there were 18 locations. Great Wolf now has 21 locations in the US and 1 in Canada.

If you are interested in learning about some of BX’s acquisition/divestiture activities, look at the ‘Press Releases‘ within the Shareholders section of the company’s website.

I last reviewed BX in my July 22, 2022 post at which time it had just released Q2 and YTD2022 results. In that post, I disclosed the purchase of additional shares on July 21 at $94.83/share. This purchase brought my total BX exposure to 1231 shares. I hold these shares in a ‘Core’ account within the FFJ Portfolio.

On October 20, BX released Q3 and YTD results. I, therefore, take this opportunity to briefly revisit BX.

Business Overview

Investors unfamiliar with BX are encouraged to review the company’s website and Part 1 of the FY2021 10-K.

The ‘Our Businesses‘ section of BX’s website has a menu of the areas in which BX invests.

At the end of Q3 2022, BX had $950.9B in total Assets Under Management (AUM) versus $940.8B at the end of Q2 2022 and $880.9B at FYE2021.

Page 18 of 20 in BX’s Q3 2022 Supplemental Financial Data reflects its Investment Records as of September 30, 2022. Three columns are labelled Multiple on Invested Capital (MOIC). A good explanation of MOIC is found here.

Financials

Q3 and YTD2022 Results

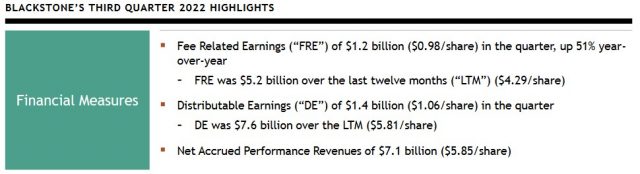

BX’s Q3 and YTD2022 results are accessible here. Additional information is found in the accompanying Supplemental Financial Data.

The ~83.0% YoY decline in Total Revenue includes the effects of unrealized activity driven by mark-to-market adjustments. This is not uncommon for Asset Managers when there is a downturn in equity and credit markets.

On the positive side, we see that management and advisory fee income was up 22% YoY ($1.612B in Q3 2022 versus $1.32B in Q3 2021) as fee rates remained stable and AUM levels improved YoY.

BX has a diverse range of growth engines that drove total inflows of ~$44.8B in Q3 and a record ~$183 YTD and ~$337.8B in the last 12 months.

Source: BX – Q3 2022 Earnings Presentation – October 20, 2022

BX also has ~$182B of dry powder capital to take advantage of dislocations.

Credit Ratings

BX’s senior unsecured domestic long-term debt ratings are in the top tier in the upper-medium-grade investment-grade tier. There is no change from prior reviews.

- S&P Global assigns an A+ long-term unsecured debt credit rating with a stable outlook; and

- Fitch assigns an A+ long-term unsecured debt credit rating with a stable outlook;

These ratings define BX as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

BX’s current deconsolidated Balance Sheet highlights for Q3 2021 and 2022 and Q2 2021 and 2022 are provided for ease of reference.

Source: BX – Q3 2022 Earnings Presentation – October 20, 2022

Source: BX – Q2 2022 Investor Presentation – July 21, 2022

Dividends and Share Repurchases

Dividend and Dividend Yield

On October 20, 2022, BX declared a $0.90/share quarterly dividend payable on November 7 bringing the total dividend distributions over the last 12 months to $4.94/share.

With shares currently trading at ~$85.40, some investors may think the dividend yield is ~4.2% (($0.90 x 4)/$85.40). BX’s dividend policy, however, clearly spells out that the quarterly dividend will fluctuate.

BX’s dividend policy is based on Distributable Earnings (DE):

‘Our intention is to pay to holders of common stock a quarterly dividend representing approximately 85% of The Blackstone Group Inc.’s share of Distributable Earnings, subject to adjustment by amounts determined by our board of directors to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and funds, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, clawback obligations and dividends to shareholders for any ensuing quarter. The dividend amount could also be adjusted upward in any one quarter.’

In my opinion, investors should not fixate on dividend and dividend yield but rather look at an investment from a total potential long-term return perspective (capital gains and dividend income).

Source: BX – Q3 2022 Earnings Presentation – October 20, 2022

Share Repurchases

The magnitude of share buybacks is heavily dependent on whether there is a meaningful deterioration in BX’s share price relative to the true underlying value.

BX is hyper-focused on capital allocation. I have no concern when I see an increase in the number of outstanding shares. My interest lies in knowing that the underlying value of each share shall likely appreciate over the long term.

Source: BX – Q3 2022 Earnings Presentation – October 20, 2022

When we include the Q3 dividend and share repurchases, BX has distributed $7.5B over the last 12 months.

Valuation

As explained in previous BX posts, I typically look at:

- diluted EPS;

- adjusted diluted EPS; and

- Free Cash Flow (FCF)

metrics to gauge the valuation of most companies I analyze. These metrics, however, are of little relevance when trying to assess BX’s performance and outlook.

BX uses Distributable Earnings (DE) and Fee Related Earnings (FRE) to more accurately measure its performance; these, and other terms, are defined at the end of the Q3 2022 Earnings Presentation and within the FY2021 Form 10-K.

The very manner in which BX operates makes it virtually impossible to estimate future DE and FRE. Furthermore, BX does not provide guidance.

The reason BX is not easy to value is that it raises large pools of capital from clients for deployment thus resulting in multiple multi-billion-dollar acquisitions annually. Because it continually makes sizable investment transactions (acquisitions or divestitures) earnings estimates can quickly become outdated.

Some of the acquired assets are meant to be perpetual holdings. In other cases, BX uses its expertise to improve the performance of the companies in which it invests with the intent of monetizing these assets as part of its capital recycling programs. It is not, therefore, unusual to see wide swings in YoY GAAP results.

Looking at DE and FRE results extracted from the FYE 2017 – FY2021 and Q1 – Q3 2022 Earnings Presentations, however, we see that BX consistently generates impressive results.

Final Thoughts

Although BX’s current ~$85.40 share price is well off its ~$150 52-week high, long-term investors should not be concerned.

At the end of Q3, BX reported $705.9B billion in fee-earning assets under management which is a ~33.6% YoY increase. Q3 adjusted net inflows amounted to ~$26.2B as a result of strong fundraising and capital deployment. These inflows are in line with the ~$25.7B quarterly run rate BX has seen over the prior two years and is even more impressive considering the worst declines in the equity and credit markets since the Great Financial Crisis.

As noted in my previous post, some asset managers will experience challenges in this environment. We must not, therefore, view all asset managers equally. BX’s reputation sets it apart from many of its peers. The sheer magnitude of its operations and sources of capital enables it to enter transactions most other asset managers would not even be able to contemplate.

Furthermore, asset managers such as Franklin Resources, BlackRock, and T. Rowe Price focus more heavily on traditional asset classes like equity, fixed-income, balanced and money market funds. BX, however, is an alternative asset manager that focuses on less-liquid alternative investments like private equity, credit alternatives, real estate, and hedge funds.

In my opinion, BX should richly reward long-term shareholders. View the current share price weakness as a window of opportunity.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BX.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.