Summary

Summary

- Altra is a small cap company which does not fit my investor profile. Some readers, however, have requested I conduct the occasional review on small cap investment opportunities hence this analysis.

- Altra released its Q4 and FY2017 results on February 21, 2018 and within days it announced a proposal to amalgamate with 4 operating companies within the Fortive Corporation group of companies.

- Shareholder and regulatory approvals are still required. Closing is expected to occur before the end of 2018.

Introduction

Altra Industrial Motion Corp. (NASDQ: AIMC) is a leading global designer, producer and marketer of a wide range of mechanical power transmission components. Its products are used to control and transmit power and torque in virtually any industrial application involving movement. Its products are sold in over 70 countries to customers in multiple industries such as energy, general industrial, material handling, metals, mining, special machinery, transportation, and turf and garden. The product portfolio includes clutches and brakes, couplings and gearing and other power transmission components.

What prompted me to write this article is that I was initially looking to analyze Danaher Corporation (NYSE: DHR). As I started my review I changed my mind and decided to first analyze Fortive Corporation (NYSE: FTV) which was a portion of DHR’s business which was spun-off in July 2016.

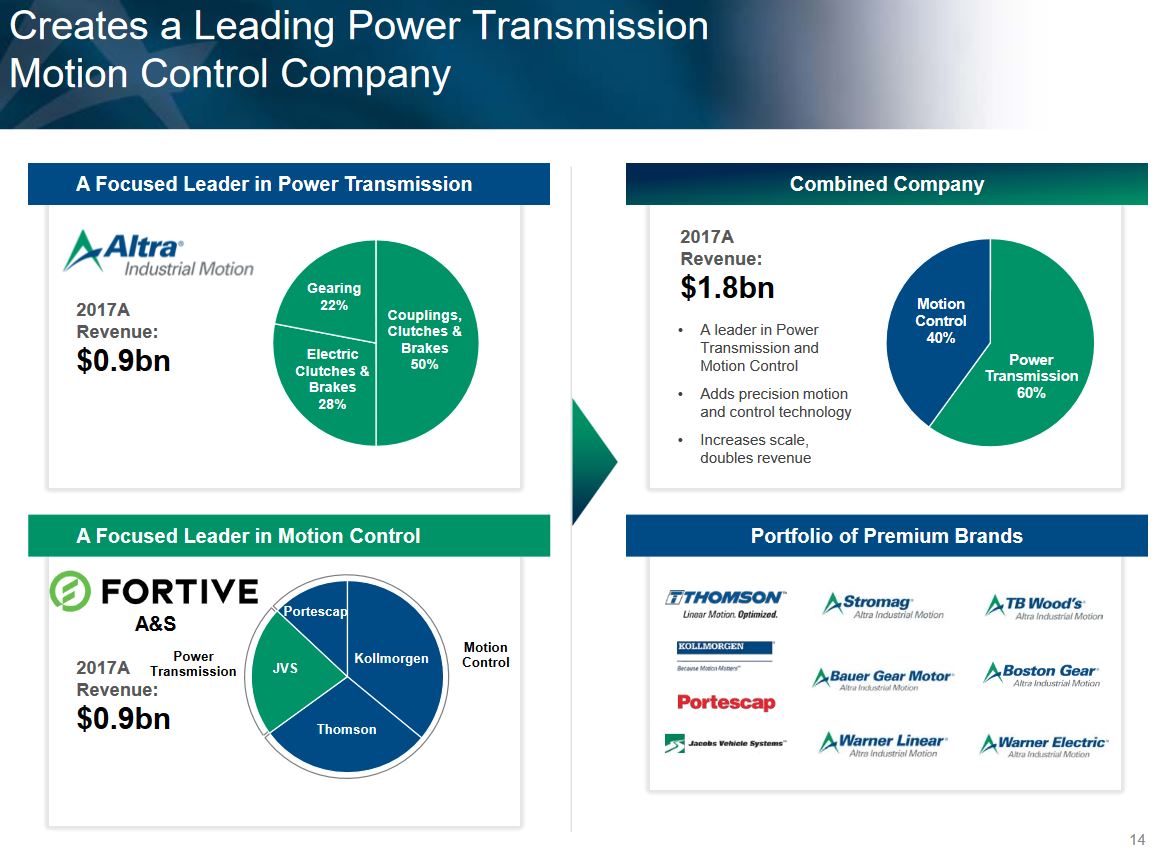

In reviewing FTV’s recent results and Press Releases, I noticed FTV had announced at the same time as AIMC in early March 2018, the intent to amalgamate 4 operating companies within FTV’s Automation and Specialty Components business with AIMC. The 4 operating companies are the market-leading brands of Kollmorgen, Thomson, Portescap, and Jacobs Vehicle Systems which generated ~$907 million in revenue for FTV’s fiscal year ended December 2017.

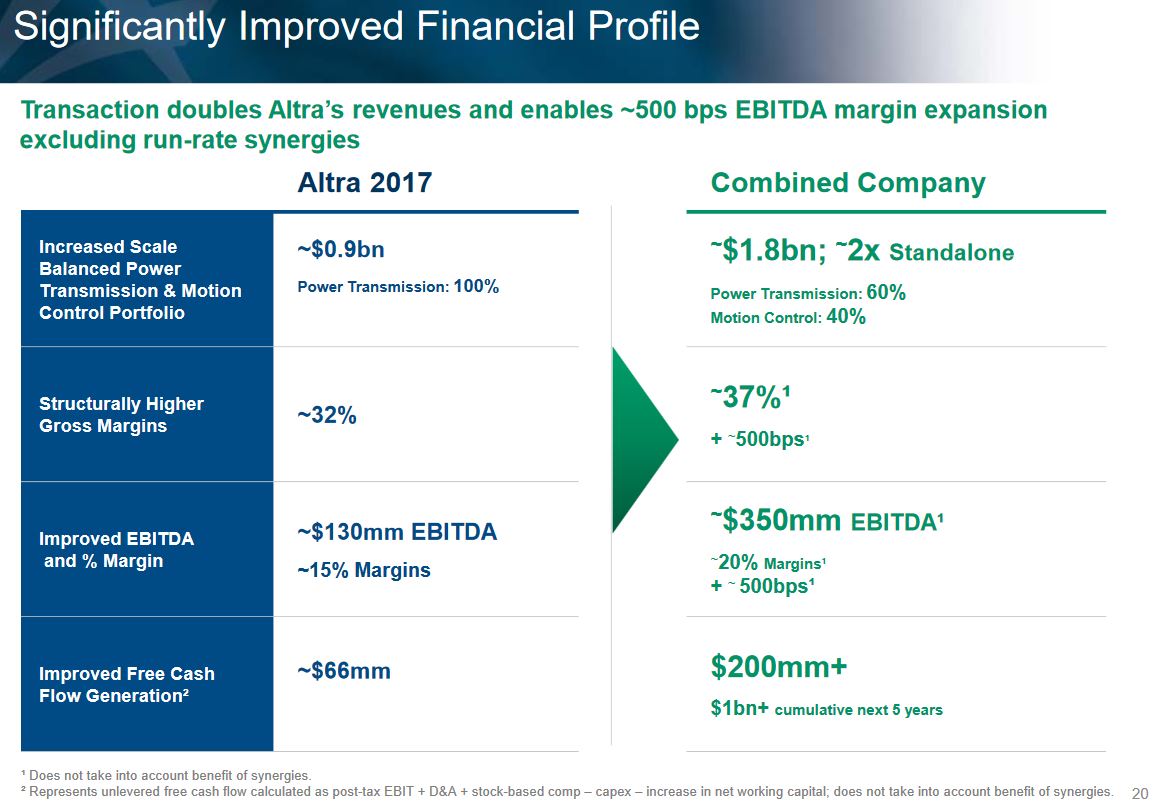

AIMC and FTV are awaiting shareholder and regulatory approval on this proposed transaction and same is expected in 2018. If the appropriate approvals are granted, AIMC would go from a business which generated revenue of ~$877 million in FY2017 (FY2018 sales projections of $895 – $915 million) to a company with combined revenue of ~$1.8B in FY2017. The essential doubling of AIMC would then take a business from a current ~$1.33B market cap to a business that would likely have a market cap in excess of ~$2.6B.

While a company this size is small relative to the companies in which I invest, I know there are readers who are interested in investing in smaller market cap companies. As a result, I am entirely open to periodically analyzing companies below my market cap threshold.

Business Analysis

AIMC is a global designer, producer and marketer of a wide range of mechanical power transmission components. Its products are used to control and transmit power and torque in virtually any industrial application involving movement.

The product portfolio includes clutches and brakes, couplings and gearing and other power transmission components. These products are used in a wide variety of high-volume manufacturing processes, where product reliability and accuracy are critical in both avoiding costly down time and enhancing the overall efficiency of the manufacturing operations. AIMC’s products are also used in non-manufacturing applications where product quality and reliability are especially critical, such as clutches and brakes for elevators and residential and commercial lawnmowers.

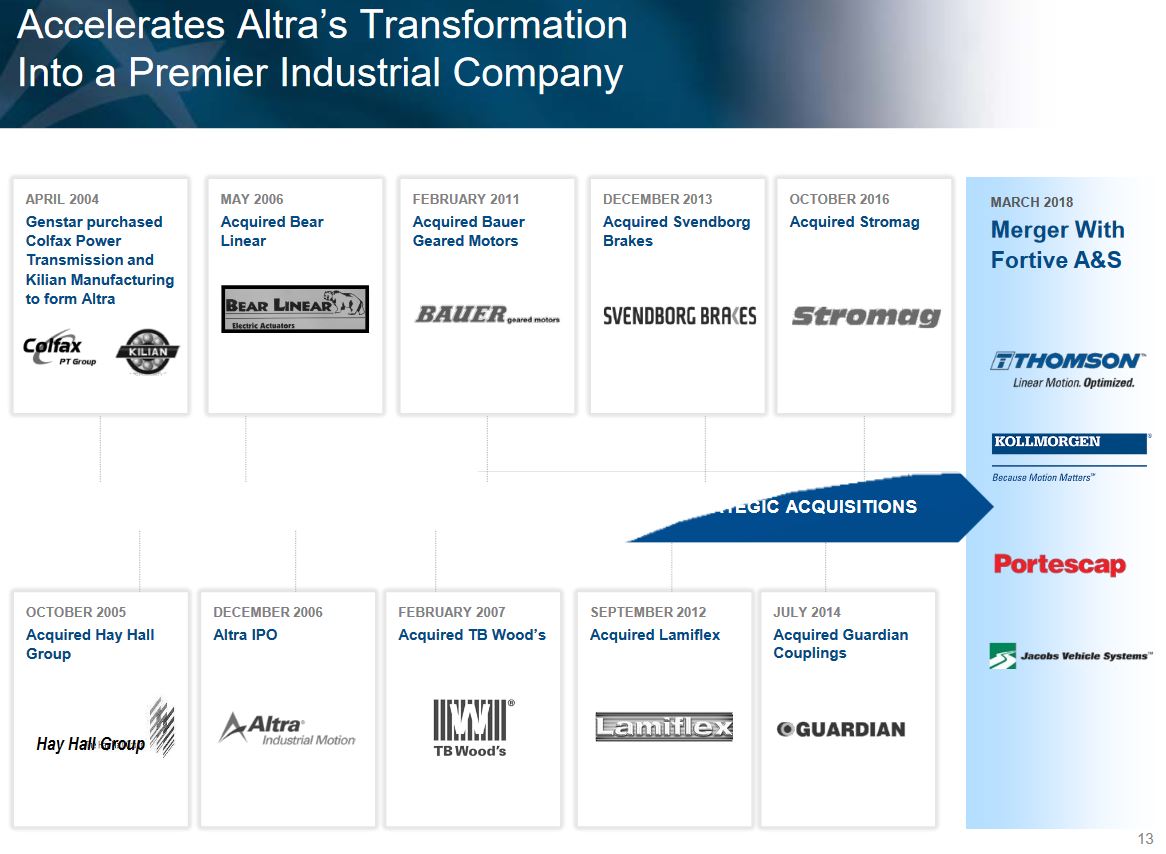

If you read a comprehensive overview of AIMC’s business starting on page 3 of its 2017 10-K which was filed February 23, 2018, you will note that AIMC has completed a few acquisitions in recent years.

I suspect growth by acquisition will continue in coming years, and therefore, what is currently a small cap business will likely become as mid-cap business within the next several years. Once this happens there will likely be stronger investor interest.

Q4 and FY2017 Results and 2018 Guidance

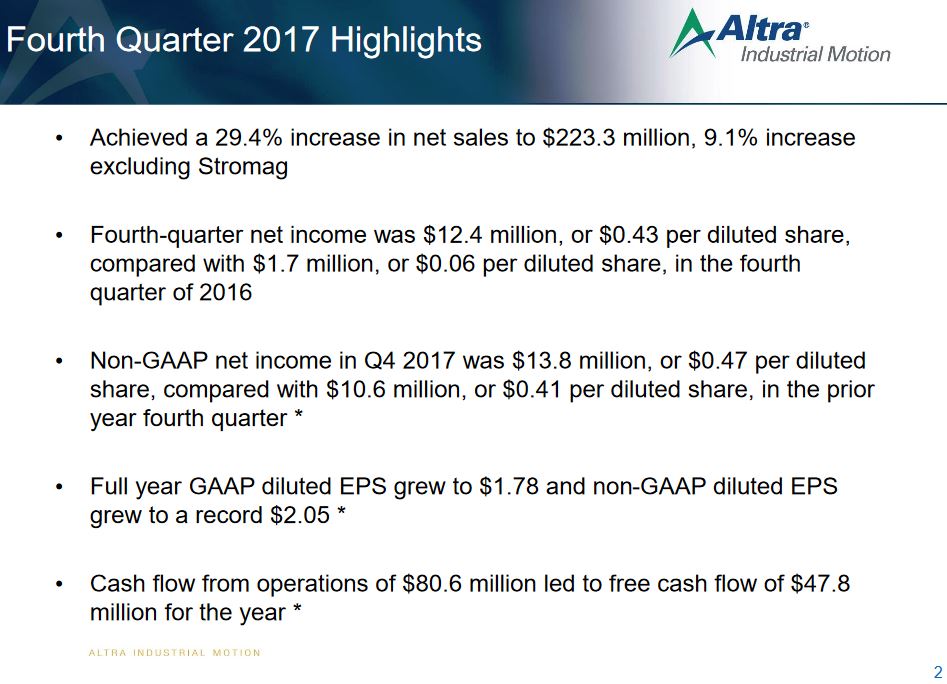

On February 21, 2018 AIMC released its Q4 and FY2017 results.

It reported record sales of ~$876.7 million versus ~$709 million in FY2016 (~23.7% growth) and non-GAAP diluted EPS of $2.05 versus $1.56 in FY2016.

AIMC recorded GAAP diluted EPS of $1.78 versus $0.79 in FY2016, an increase of ~83.5%. Non-GAAP diluted EPS of $2.05 was a ~31.4% increase from $1.56 reported in FY2016.

Source: AIMC – Q4 and FY2017 Earnings Conference Call February 21 2018 Presentation

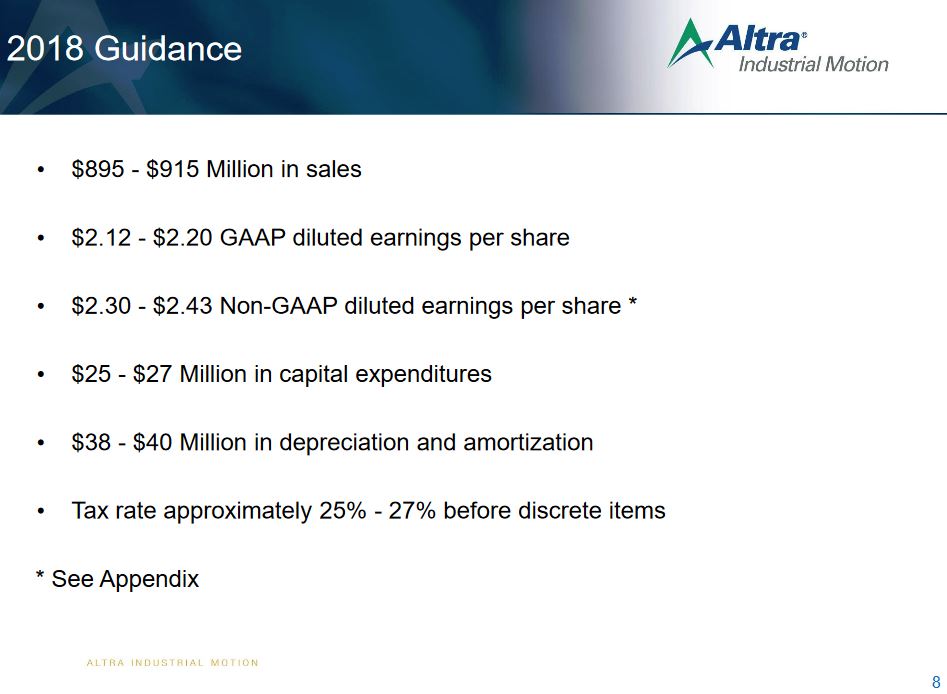

AIMC’s FY2018 guidance for sales is in the $895 – $915 million range and GAAP diluted EPS is in the range of $2.12 – $2.20 and non-GAAP diluted EPS is in the range of $2.30 – $2.43.

This FY2018 guidance will likely remain in effect until such time as regulatory approval is provided for the recently announced proposed amalgamation with FTV’s Automation & Specialty Components Business Segments.

Source: AIMC – Q4 and FY2017 Earnings Conference Call February 21 2018 Presentation

Source: AIMC – Q4 and FY2017 Earnings Conference Call February 21 2018 Presentation

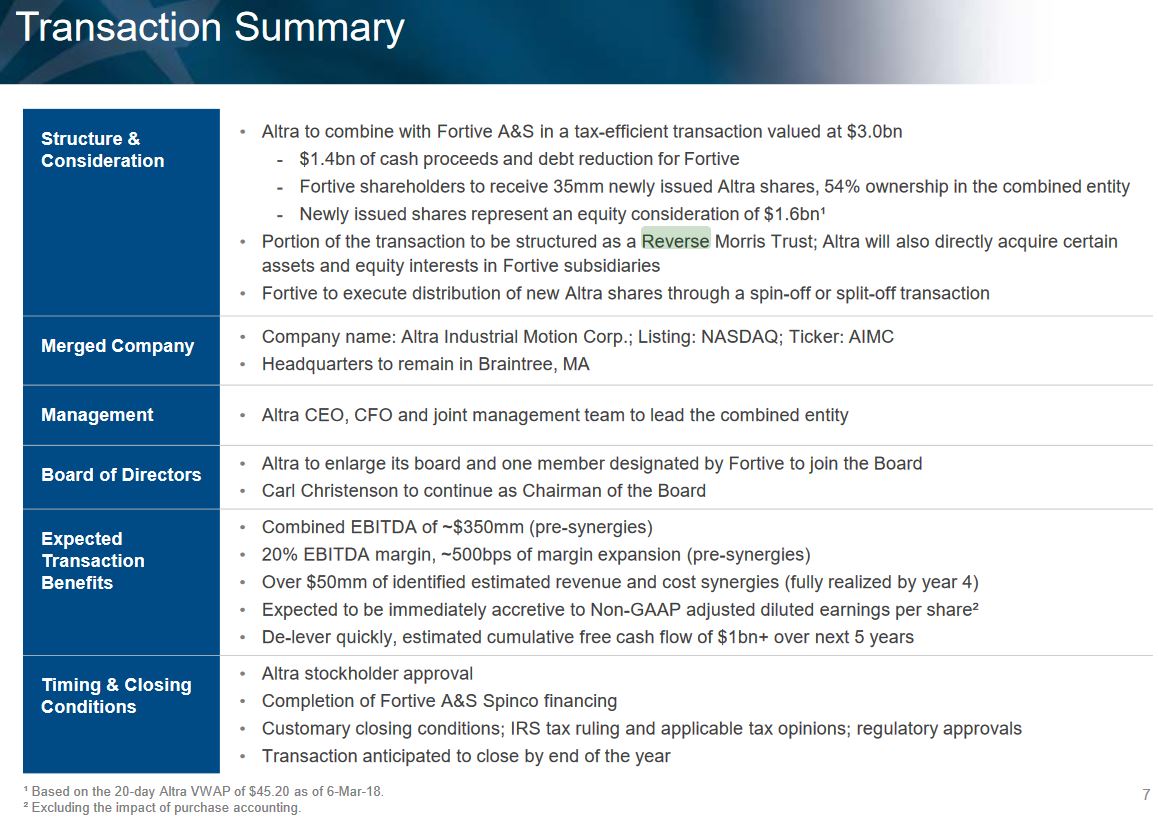

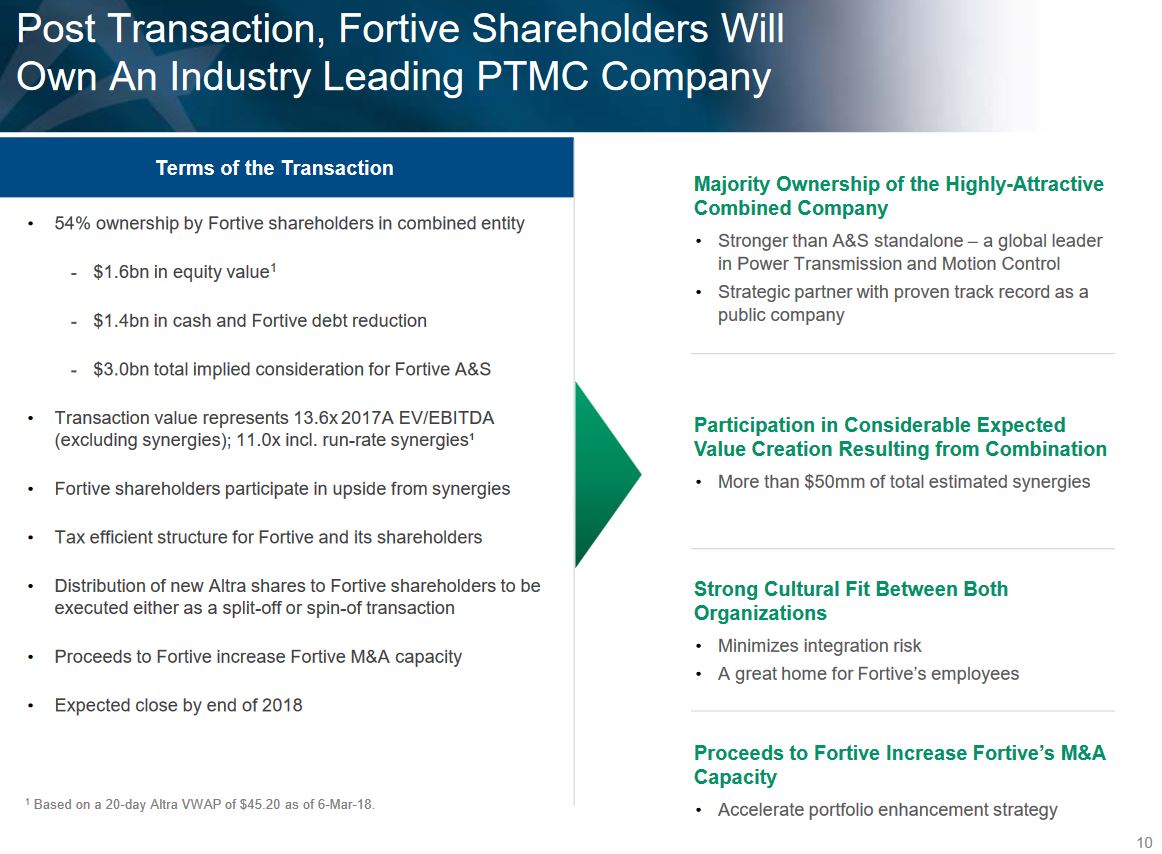

Proposed Amalgamation of AIMC with FTV’s Corporation’s Automation & Specialty Components Business Segments

Should the amalgamation be completed as planned, annual revenue will exceed the combined 2017 annual revenue of ~$1.8B thereby making it a global leader in Power Transmission and Motion Control.

Details, including the Strategic and Financial Benefits of the transaction, can be found here.

Source: Altra Combination with Fortive A&S March 7, 2018 Presentation

Source: Altra Combination with Fortive A&S March 7, 2018 Presentation

Reference is made to a portion of the transaction as being structured as a Reverse Morris Trust. This type of Trust in United States law is a transaction that combines a divisive reorganization (spin-off) with an acquisitive reorganization (statutory merger) to allow a tax-free transfer (in the guise of a merger) of a subsidiary.

This Trust is used when a parent company has a subsidiary it wants to sell in a tax-efficient manner. The parent company completes a spin-off of a subsidiary to the parent company’s shareholders.

Under Internal Revenue Code section 355, this could be tax-free if certain criteria are met. The former subsidiary (now owned by the parent company’s shareholders, but separate from the parent company) then merges with a target company to create a merged company. Under Internal Revenue Code section 368(a)(1)(A), this transaction could be largely tax-free if the former subsidiary is considered the ‘buyer’ of the target company. The former subsidiary is the ‘buyer’ if its shareholders (also the original parent company’s shareholders) own more than 50% of the merged company. Thus, the former subsidiary will usually have a bigger market capitalization than the target company.

The target company’s managers rarely run the merged company. In this case, however, the combined company will continue to be led by AIMC’s current Chairman and CEO and AIMC’s CFO will remain in his current capacity. AIMC’s senior management team will be expanded to include both AIMC and FTV A&S employees. In addition, AIMC will increase the size of its Board with the addition of one board member designated by FTV.

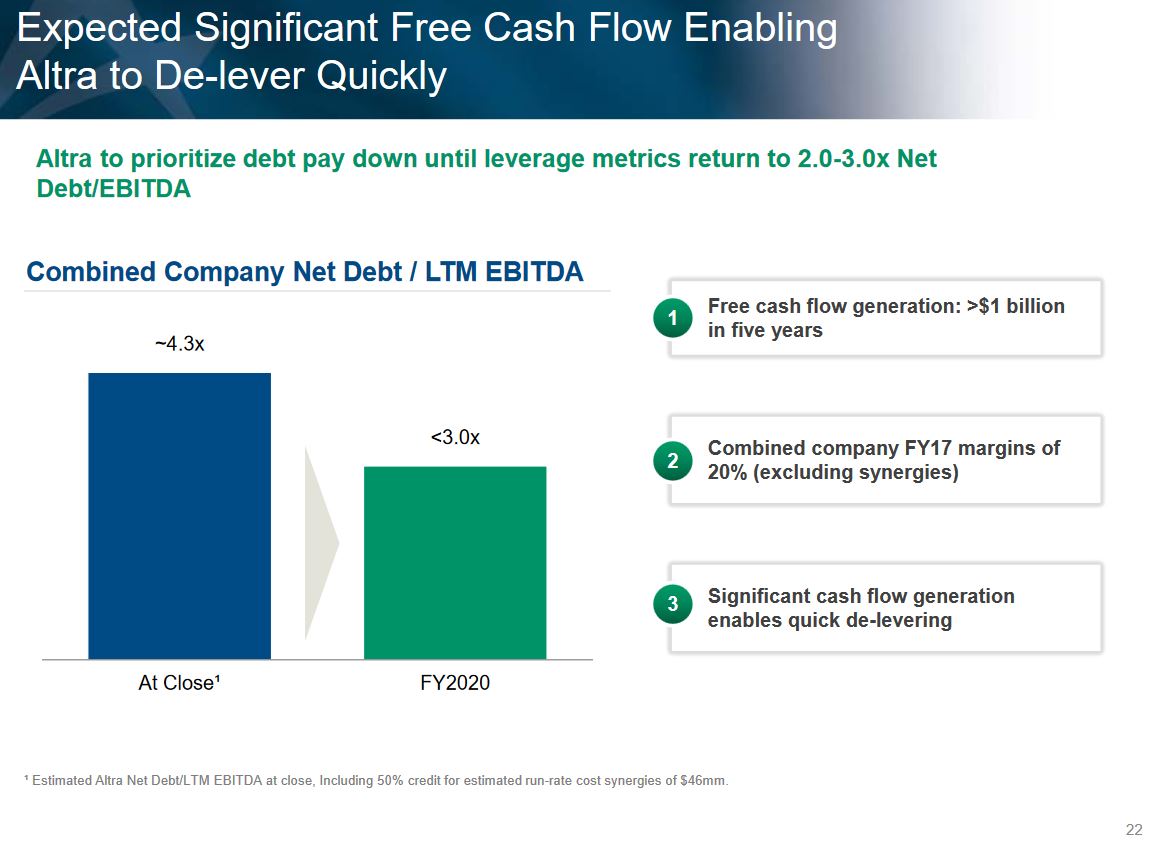

This transaction is subject to customary closing conditions, including the approval of AIMC and FTV shareholders, IRS tax ruling and applicable tax opinions, and regulatory approvals. At this juncture, the transaction is expected to close by the end of 2018.

Credit Ratings

AIMC is currently not rated by Moody’s and S&P Global.

Valuation

With AIMC having closed at $45.15 on April 12, 2018 and FY2017 GAAP diluted EPS of $1.78, we arrive at a diluted PE of 25.4. The forward PE is ~20.9 on the basis of a GAAP diluted EPS of $2.16 (mid-point of projection).

AIMC is certainly in growth mode and the projected growth in margins and free cash flow appear to already have been baked in to the current stock price.

Dividend, Dividend Yield, Dividend Payout Ratio, Stock Splits, and Share Repurchases

On February 13, 2018, AIMC announced that its Board of Directors had approved the payment of a quarterly cash dividend of $0.17/share for Q1 2018 (paid April 3, 2018). This dividend is the twenty-fourth consecutive dividend in the Company’s history.

The Q1 2017 dividend of $0.15/share was increased to $0.17/share for Q2 – Q4 thus resulting in a $0.66 annual dividend in FY2017.

On the basis of AIMC’s ~$45 stock price and the $0.66/year dividend, the dividend yield is ~1.46%.

I suspect AIMC’s Board of Directors will approve a $0.01 – $0.02/quarter increase in AIMC’s quarterly dividend when Q1 2018 results are released April 27, 2018.

A current AIMC investor has very likely placed little emphasis on the company’s dividend yield in their investment analysis process. Interestingly, there is no section on the company’s website devoted to the company’s dividend/dividend history.

If you wish to see how an investment in AIMC would have performed over time, an investment calculator can be accessed here. Below the calculator is a clause which states ‘Return calculations do not include reinvested cash dividends.’; please keep this caveat in mind if you decide to check out the calculator.

The current $0.66/share annual dividend represents a dividend payout ratio of ~37.1% of FY2017’s GAAP diluted EPS of $1.78/share and ~30.6% of the mid-point of the projected FY2018 GAAP diluted EPS range. This payout ratio will change once the companies have been amalgamated.

Final Thoughts

AIMC appears to be a great little small cap company operating in rather protected niche markets in the industrials space. This proposed amalgamation certainly is appealing but everyone has their personal risk tolerance level. In my case, I am retired and I seek to invest in much larger and far better capitalized companies which have a consistent track record of paying increasing dividends on at least an annual basis; I do not, however, chase yield.

I do not dispute that AIMC has a promising future but I will not be initiating a position and will continue to seek other investment opportunities.

I wish you much success on your journey to financial freedom.

Thanks for reading!

Note: I sincerely appreciate the time you took to read this article. Please send any feedback, corrections, or questions to charles@financialfreedomisajourney.com

Disclaimer: I have no knowledge of your individual circumstances and am not providing individualized advice or recommendations. I encourage you not to make any investment decision without conducting your own research and due diligence. You should also consult your financial advisor about your specific situation.

Disclosure: I do not currently hold a position in AIMC and do not intend to initiate a position within the next 72 hours.

I wrote this article myself and it expresses my own opinions. I am not receiving compensation for it and have no business relationship with any company whose stock is mentioned in this article.