Alternative asset exposure (eg. private equity, private debt, hedge funds, real estate, commodities, structured products, venture capital) can produce attractive long-term investment returns. Directly investing in alternative assets, however, is beyond my risk tolerance. This is why a portion of my alternative asset exposure is through Blackstone (BX).

I last reviewed Blackstone (BX) in this January 27, 2023 post at which time it had just released its Q4 and FY2022 results. I subsequently wrote a brief post on May 12 in which I disclose my May 9 purchase of 100 shares @ $81.649/share bringing my total exposure to 1,462 shares. In both posts, I consider BX to be undervalued. Following a recent share price surge, however, I think Blackstone is now fairly valued.

Now that BX has released its Q2 and YTD2023 results on July 20, I take this opportunity to revisit this existing holding.

Business Overview

I encourage you to review the company’s website and Part 1 of the FY2022 10-K.

The ‘Our Businesses‘ section of BX’s website has a menu of the areas in which BX invests.

BX has finally surpassed the $1T level in total Assets Under Management (AUM). Remarkably, BX is the first alternative manager to do so. Even more impressive is that it reached this level more than three years ahead of the aspirational road map presented at the 2018 Investor Day (see presentation).

It is remarkable how Steven Schwartzman and his partner, Pete Peterson, founded BX in 1985 with $400,000 of startup capital. When they started BX, they sent out 450 personal announcements regarding their new venture and published a full-page newspaper ad with the expectation that the phone would start ringing off the hook. Interestingly, no one called other than a few people wishing them luck.

Looking at BX today, it has established an unparalleled global platform of leading business lines, offering over 70 distinct investment strategies.

Want to Work At BX? Good Luck!

Read this and this to find out just how difficult it is to receive an employment offer from BX.

There were 62,000 applicants for positions at BX this year. Only 169 were accepted. This is an entry rate of 0.27% or 1 in ~400 applicants.

In comparison, ~350,000 apply to Goldman Sachs (GS). GS, however, has ~3,000 open graduate positions thereby giving it an acceptance rate of ~1.27%.

Harvard has an acceptance rate of ~4%. The Navy Seals have a ~6% acceptance rate.

Financials

Q2 and YTD2023 Results

The most recent results are accessible here and in the accompanying Q2 2023 Supplemental Financial Data. In particular, refer to pages 18 and 19 which reflect a high-level overview of the various funds BX manages.

A huge drawback investors face when investing in BX is that it is impossible to know what investments are held within each fund. My BX investment is made on the premise that BX is in the business of making money for highly sophisticated investors. If these investors entrust billions with BX, who am I to suggest they are making a mistake?

Furthermore, senior BX executives have significant share ownership. They have considerable incentive to ensure BX’s long-term success.

As noted earlier, BX’s total AUM reached $1T (a 6% YoY increase). The earning AUM rose 7% YoY to $731.1B driving management fees up 9% to a record $1.7B.

The following is a very high-level overview of BX’s Q2 2023 results.

The second quarter marked the 54th consecutive quarter of YoY growth in base management fees. Fee-related earnings (FRE) increased 12% YoY to $1.1B or $0.94/share.

Distributable earnings (DE) were $1.2B in Q2 or $0.93/share. The YoY comparison was affected by a material decline in net realizations relative to Q2 2022.

Source: BX – Q2 2023 Earnings Presentation – July 20, 2023

BX has a diverse range of growth engines that enables it to continually generate inflows, deploy capital, and generate realizations.

Source: BX – Q2 2023 Earnings Presentation – July 20, 2023

As BX has increased its AUM, picking the right sectors and markets has become more important than ever.

In Q2, BX’s winning areas of investment such as global logistics, digital infrastructure, and energy transition, have been among the largest drivers of appreciation in BX’s funds.

BX is also witnessing sustained strength in key sectors in terms of cash flow growth. Half of its owned real estate is in logistics, student housing and data centers. These areas of real estate have experienced double-digit YoY growth in market rents. In the US rental housing holdings overall, for example, fundamentals are stable with cash flow increasing at a high single-digit rate.

With strong signs of inflation flowing across BX’s portfolio, management expects valuations for BX-owned companies and real estate holdings to continue to improve.

Despite a very challenging fundraising environment, BX’s reputation enabled it to generate $30B of total inflows in Q2 and $158B over the past 12 months; BX now has record ‘dry powder’ of ~$200B. Currently, the greatest demand is for private credit solutions with BX’s corporate credit insurance and real estate debt businesses comprising over 50% of Q2 inflows.

Several areas have particularly attractive long-term dynamics for BX’s business.

In credit, there is a structural shift underway in the market.

Traditional financing providers are cautious and US regional banks and finance companies are increasingly selling off their consumer loans as funding them becomes increasingly difficult and more expensive. Of late, traditional lenders have been flooding private credit firms and hedge funds with requests to buy the debt at a discount.

On JP Morgan’s Q2 2023 earnings call with analysts, Jamie Morgan (Chief Executive Officer) stated that ‘they’re dancing in the streets’ when speaking about hedge funds, private equity, private credit, and firms such as BX.

BX, for example, has a $362B credit and real estate credit platform with leading capabilities to directly and efficiently originate high-quality assets. It is also partnering with banks and other originators that are facing greater lending constraints but want to continue to serve their customers in areas like home improvement, auto finance and renewables.

BX has already processed five of these partnerships totalling $6B and the plan is to add more.

In the $40T insurance channel, BX currently manages $174B. Inflows from this channel in Q2 exceeded $7B with more than $4B from BX’s four clients. BX expects a strong pace of inflows from them going forward, including from two clients who, on a combined basis, are the second largest sellers of fixed annuities in the US. In addition, BX has a pipeline of prospects.

While Blackstone Private Credit Fund (BCRED) and Blackstone Real Estate Income Trust (BREIT) face some near-term headwinds, management remains confident in the reacceleration of growth in this channel, given BX’s portfolio positioning and exceptional performance.

FY2023 Outlook

BX does not provide specific targets. However, management’s expectation is for a pickup in activity.

Inflation uncertainty makes it hard to do mergers and acquisitions and IPOs. In addition, there has been considerable uncertainty around:

- banking issues;

- inflation; and

- the extent to which the Fed will raise rates.

Of late, however, there appears to be less uncertainty which is a reason why BX thinks markets are becoming more enthused.

There is, nevertheless, the possibility of an economic slowdown which would lead to a market pullback.

Fortunately, BX has considerable experience in navigating through different business conditions. It also has an excellent reputation for protecting investors’ investments.

Credit Ratings

BX’s senior unsecured domestic long-term debt ratings are at the top of the upper-medium-grade investment-grade tier. There is no change from prior reviews.

- S&P Global assigns an A+ long-term unsecured debt credit rating with a stable outlook; and

- Fitch assigns an A+ long-term unsecured debt credit rating with a stable outlook;

These ratings define BX as having a STRONG capacity to meet its financial commitments. It is, however, somewhat more susceptible to the adverse effects of changes in circumstances and economic conditions than obligors in higher-rated categories.

This is BX’s deconsolidated Balance Sheet highlights for Q2 2023.

Source: BX – Q2 2023 Earnings Presentation – July 20, 2023

This is BX’s deconsolidated Balance Sheet highlights for Q4 2022.

BX’s cash and net investments have declined $1.748B in two quarters and its outstanding debt (at par) has declined $0.319B.

Dividends and Share Repurchases

Dividend and Dividend Yield

Although BX distributes a quarterly dividend, it may not appeal to investors who prefer a long-term track record of dividend increases.

BX’s dividend policy is based on Distributable Earnings (DE) so its quarterly dividend will naturally fluctuate quarterly:

‘We intend to pay to holders of common stock a quarterly dividend representing approximately 85% of The Blackstone Group Inc.’s share of Distributable Earnings, subject to adjustment by amounts determined by our board of directors to be necessary or appropriate to provide for the conduct of our business, to make appropriate investments in our business and funds, to comply with applicable law, any of our debt instruments or other agreements, or to provide for future cash requirements such as tax-related payments, clawback obligations and dividends to shareholders for any ensuing quarter. The dividend amount could also be adjusted upward in any one quarter.’

On July 20, 2023, BX declared a $0.79/share quarterly dividend payable on August 7. Since BX’s quarterly dividend fluctuates, I do not calculate BX’s forward dividend yield.

Source: BX – Q2 2023 Earnings Presentation – July 20, 2023

I look at an investment’s total potential long-term return perspective (capital gains and dividend income). It is for this reason that changes in BX’s quarterly dividend do not influence my investment decision-making process.

Share Repurchases

BX is hyper-focused on capital allocation. The extent to which it repurchases shares depends on whether there is a meaningful deterioration in BX’s share price relative to the true underlying value.

Despite an increase in the number of outstanding shares over the past several quarters, my interest lies in the potential for appreciation in the underlying value of each share over the long term.

Source: BX – Q2 2023 Earnings Presentation – July 20, 2023

Valuation

I typically look at:

- diluted EPS;

- adjusted diluted EPS; and

- Free Cash Flow (FCF)

metrics to gauge the valuation of most companies I analyze. These metrics, however, are of little relevance when trying to assess BX’s performance and outlook.

BX uses Distributable Earnings (DE) and Fee Related Earnings (FRE) to more accurately measure its performance; these, and other terms, are defined within the FY2022 Form 10-K.

The very manner in which BX operates makes it virtually impossible to estimate future DE and FRE. Furthermore, BX does not provide guidance.

The reason BX is not easy to value is that it raises large pools of capital from clients for deployment thus resulting in multiple multi-billion-dollar acquisitions annually. Because it continually makes sizable investment transactions (acquisitions or divestitures), earnings estimates can quickly become outdated.

Some of the acquired assets are meant to be perpetual holdings. In other cases, BX uses its expertise to improve the performance of the companies in which it invests with the intent of monetizing these assets as part of its capital recycling programs. It is not, therefore, unusual to see wide swings in YoY GAAP results.

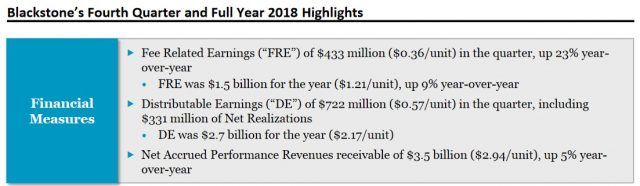

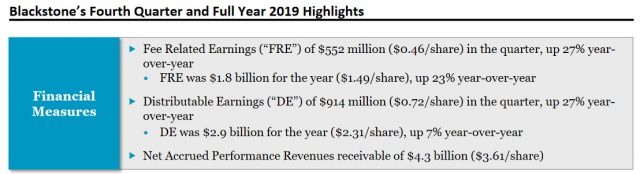

Looking at DE and FRE results extracted from the FYE 2017 – FY2022 Earnings Presentations, we see BX’s impressive track record.

")

Final Thoughts

Investing directly in alternative assets is beyond my risk tolerance, and therefore, I choose to have alternative asset exposure through my Blackstone investment.

Currently, 1462 BX shares are held in a ‘Core’ account in the FFJ Portfolio.

BX was my 20th largest holding when I completed my Mid-2023 Investment Holdings Review, at which time the share price was ~$93; shares now trade at $104.89. The share price of most of my holdings has risen after that review so I do not know if BX is still a top 20 holding.

I previously considered BX to be undervalued but following a ~$23 share price increase after my May 9 purchase, I now consider shares to be fairly valued. Rather than add to my BX exposure at this point, I intend to deploy excess capital toward investments in other great companies that have temporarily fallen out of favour.

I wish you much success on your journey to financial freedom!

Note: Please send any feedback, corrections, or questions to finfreejourney@gmail.com.

Disclosure: I am long BX and GS.

Disclaimer: I do not know your circumstances and do not provide individualized advice or recommendations. I encourage you to make investment decisions by conducting your own research and due diligence. Consult your financial advisor about your specific situation.

I wrote this article myself and it expresses my own opinions. I do not receive compensation for it and have no business relationship with any company mentioned in this article.